Fixed Income Portfolio Optimization Python . Its purpose is to provide advanced, flexible. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. To do so, i use cvxpy in python. I use this paper as reference.

from s-rochanarat-int-app.medium.com

To do so, i use cvxpy in python. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. I use this paper as reference. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. Its purpose is to provide advanced, flexible.

Portfolio Optimization with Python An example from SET50 Index by

Fixed Income Portfolio Optimization Python Its purpose is to provide advanced, flexible. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. Its purpose is to provide advanced, flexible. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. To do so, i use cvxpy in python. I use this paper as reference.

From www.codingfinance.com

Portfolio Optimization in Python Coding Finance Fixed Income Portfolio Optimization Python To do so, i use cvxpy in python. Its purpose is to provide advanced, flexible. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. I use this paper as reference. Fixed Income Portfolio Optimization Python.

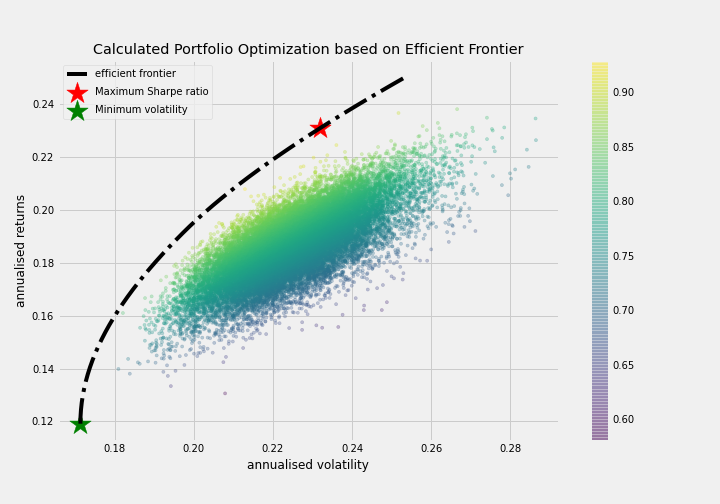

From dimitrisgeorgiou.medium.com

Introduction to Portfolio Analysis & Optimization with Python. by Fixed Income Portfolio Optimization Python I use this paper as reference. To do so, i use cvxpy in python. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. Its purpose is to provide advanced, flexible. Fixed Income Portfolio Optimization Python.

From www.codingfinance.com

How to calculate portfolio returns in Python Coding Finance Fixed Income Portfolio Optimization Python I use this paper as reference. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. Its purpose is to provide advanced, flexible. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. To do so, i use cvxpy in python. Fixed Income Portfolio Optimization Python.

From www.youtube.com

Portfolio Optimization in Python Part 4 YouTube Fixed Income Portfolio Optimization Python I use this paper as reference. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. Its purpose is to provide advanced, flexible. To do so, i use cvxpy in python. Fixed Income Portfolio Optimization Python.

From medium.com

Efficient Frontier & Portfolio Optimization with Python [Part 2/2] Fixed Income Portfolio Optimization Python I use this paper as reference. Its purpose is to provide advanced, flexible. To do so, i use cvxpy in python. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. Fixed Income Portfolio Optimization Python.

From www.codingfinance.com

Portfolio Optimization in Python Coding Finance Fixed Income Portfolio Optimization Python i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. I use this paper as reference. Its purpose is to provide advanced, flexible. To do so, i use cvxpy in python. Fixed Income Portfolio Optimization Python.

From randerson112358.medium.com

Python For Finance Portfolio Optimization by randerson112358 Medium Fixed Income Portfolio Optimization Python To do so, i use cvxpy in python. Its purpose is to provide advanced, flexible. I use this paper as reference. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. Fixed Income Portfolio Optimization Python.

From github.com

GitHub aarwitz/PortfolioOptimizer Portfolio optimization in Python Fixed Income Portfolio Optimization Python pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. To do so, i use cvxpy in python. Its purpose is to provide advanced, flexible. I use this paper as reference. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. Fixed Income Portfolio Optimization Python.

From morioh.com

Visualize Your Portfolio Using Python Fixed Income Portfolio Optimization Python i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. Its purpose is to provide advanced, flexible. I use this paper as reference. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. To do so, i use cvxpy in python. Fixed Income Portfolio Optimization Python.

From www.youtube.com

Best portfolio optimization package for Python YouTube Fixed Income Portfolio Optimization Python Its purpose is to provide advanced, flexible. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. I use this paper as reference. To do so, i use cvxpy in python. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. Fixed Income Portfolio Optimization Python.

From builtin.com

An Introduction to Portfolio Optimization in Python Built In Fixed Income Portfolio Optimization Python pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. I use this paper as reference. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. Its purpose is to provide advanced, flexible. To do so, i use cvxpy in python. Fixed Income Portfolio Optimization Python.

From predictivehacks.com

Portfolio Optimization in Python Predictive Hacks Fixed Income Portfolio Optimization Python i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. Its purpose is to provide advanced, flexible. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. To do so, i use cvxpy in python. I use this paper as reference. Fixed Income Portfolio Optimization Python.

From builtin.com

An Introduction to Portfolio Optimization in Python Built In Fixed Income Portfolio Optimization Python i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. I use this paper as reference. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. To do so, i use cvxpy in python. Its purpose is to provide advanced, flexible. Fixed Income Portfolio Optimization Python.

From www.youtube.com

Portfolio Optimization in Python Part 6 YouTube Fixed Income Portfolio Optimization Python i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. Its purpose is to provide advanced, flexible. I use this paper as reference. To do so, i use cvxpy in python. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. Fixed Income Portfolio Optimization Python.

From www.youtube.com

FinMod 11 Fixed Banking Portfolio Optimization YouTube Fixed Income Portfolio Optimization Python To do so, i use cvxpy in python. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. I use this paper as reference. Its purpose is to provide advanced, flexible. Fixed Income Portfolio Optimization Python.

From quantpy.com.au

Portfolio Optimisation QuantPy Fixed Income Portfolio Optimization Python I use this paper as reference. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. Its purpose is to provide advanced, flexible. To do so, i use cvxpy in python. Fixed Income Portfolio Optimization Python.

From www.youtube.com

[Portfolio Optimization] Python (2) Robust portfolio 파이썬 구현 YouTube Fixed Income Portfolio Optimization Python pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. I use this paper as reference. To do so, i use cvxpy in python. Its purpose is to provide advanced, flexible. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. Fixed Income Portfolio Optimization Python.

From medium.com

Efficient Frontier & Portfolio Optimization with Python [Part 2/2] Fixed Income Portfolio Optimization Python I use this paper as reference. Its purpose is to provide advanced, flexible. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. To do so, i use cvxpy in python. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. Fixed Income Portfolio Optimization Python.

From python.plainenglish.io

Using Python for Financial Portfolio Optimization by Adrian J. Mayer Fixed Income Portfolio Optimization Python Its purpose is to provide advanced, flexible. I use this paper as reference. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. To do so, i use cvxpy in python. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. Fixed Income Portfolio Optimization Python.

From www.youtube.com

Simple Portfolio Optimization with Python YouTube Fixed Income Portfolio Optimization Python pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. Its purpose is to provide advanced, flexible. To do so, i use cvxpy in python. I use this paper as reference. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. Fixed Income Portfolio Optimization Python.

From nebash.com

Python for Finance Portfolio Optimization (2022) Fixed Income Portfolio Optimization Python pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. I use this paper as reference. Its purpose is to provide advanced, flexible. To do so, i use cvxpy in python. Fixed Income Portfolio Optimization Python.

From www.youtube.com

Portfolio Optimization in Python The Math (2/3) YouTube Fixed Income Portfolio Optimization Python Its purpose is to provide advanced, flexible. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. I use this paper as reference. To do so, i use cvxpy in python. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. Fixed Income Portfolio Optimization Python.

From www.researchgate.net

(PDF) PyPortfolioOpt portfolio optimization in Python Fixed Income Portfolio Optimization Python To do so, i use cvxpy in python. I use this paper as reference. Its purpose is to provide advanced, flexible. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. Fixed Income Portfolio Optimization Python.

From www.youtube.com

Portfolio Optimization with Python [Cryptocurrencies] YouTube Fixed Income Portfolio Optimization Python pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. Its purpose is to provide advanced, flexible. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. To do so, i use cvxpy in python. I use this paper as reference. Fixed Income Portfolio Optimization Python.

From www.linkedin.com

Markowitz Portfolio Optimization with Python Fixed Income Portfolio Optimization Python To do so, i use cvxpy in python. Its purpose is to provide advanced, flexible. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. I use this paper as reference. Fixed Income Portfolio Optimization Python.

From www.youtube.com

Practical Portfolio Optimization with Python YouTube Fixed Income Portfolio Optimization Python Its purpose is to provide advanced, flexible. To do so, i use cvxpy in python. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. I use this paper as reference. Fixed Income Portfolio Optimization Python.

From www.researchgate.net

(PDF) Python for Portfolio Optimization The Ascent! Fixed Income Portfolio Optimization Python I use this paper as reference. Its purpose is to provide advanced, flexible. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. To do so, i use cvxpy in python. Fixed Income Portfolio Optimization Python.

From www.youtube.com

Portfolio Optimization in Python Introduction YouTube Fixed Income Portfolio Optimization Python Its purpose is to provide advanced, flexible. To do so, i use cvxpy in python. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. I use this paper as reference. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. Fixed Income Portfolio Optimization Python.

From s-rochanarat-int-app.medium.com

Portfolio Optimization with Python An example from SET50 Index by Fixed Income Portfolio Optimization Python Its purpose is to provide advanced, flexible. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. To do so, i use cvxpy in python. I use this paper as reference. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. Fixed Income Portfolio Optimization Python.

From amangupta16.medium.com

Portfolio Optimization Using Python [Part 1/2] by Aman Gupta Medium Fixed Income Portfolio Optimization Python To do so, i use cvxpy in python. I use this paper as reference. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. Its purpose is to provide advanced, flexible. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. Fixed Income Portfolio Optimization Python.

From mlq.ai

Python for Finance Portfolio Optimization Fixed Income Portfolio Optimization Python To do so, i use cvxpy in python. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. Its purpose is to provide advanced, flexible. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. I use this paper as reference. Fixed Income Portfolio Optimization Python.

From www.youtube.com

Portfolio Optimization in Python Using The Program (1/3) YouTube Fixed Income Portfolio Optimization Python Its purpose is to provide advanced, flexible. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. To do so, i use cvxpy in python. I use this paper as reference. Fixed Income Portfolio Optimization Python.

From www.pythonforfinance.net

Investment Portfolio Optimisation With Python Revisited Python For Fixed Income Portfolio Optimization Python i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. To do so, i use cvxpy in python. Its purpose is to provide advanced, flexible. I use this paper as reference. Fixed Income Portfolio Optimization Python.

From www.youtube.com

Portfolio Optimization in Python Part 1 YouTube Fixed Income Portfolio Optimization Python Its purpose is to provide advanced, flexible. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. To do so, i use cvxpy in python. I use this paper as reference. Fixed Income Portfolio Optimization Python.

From financetrainingcourse.com

Model Fixed Portfolio Case Study Fixed Income Portfolio Optimization Python Its purpose is to provide advanced, flexible. To do so, i use cvxpy in python. I use this paper as reference. i'm trying to solve for a maximum sharpe ratio portfolio in the fixed income space. pyportfolioopt allows users to optimize along the efficient semivariance frontier via the efficientsemivariance class. Fixed Income Portfolio Optimization Python.