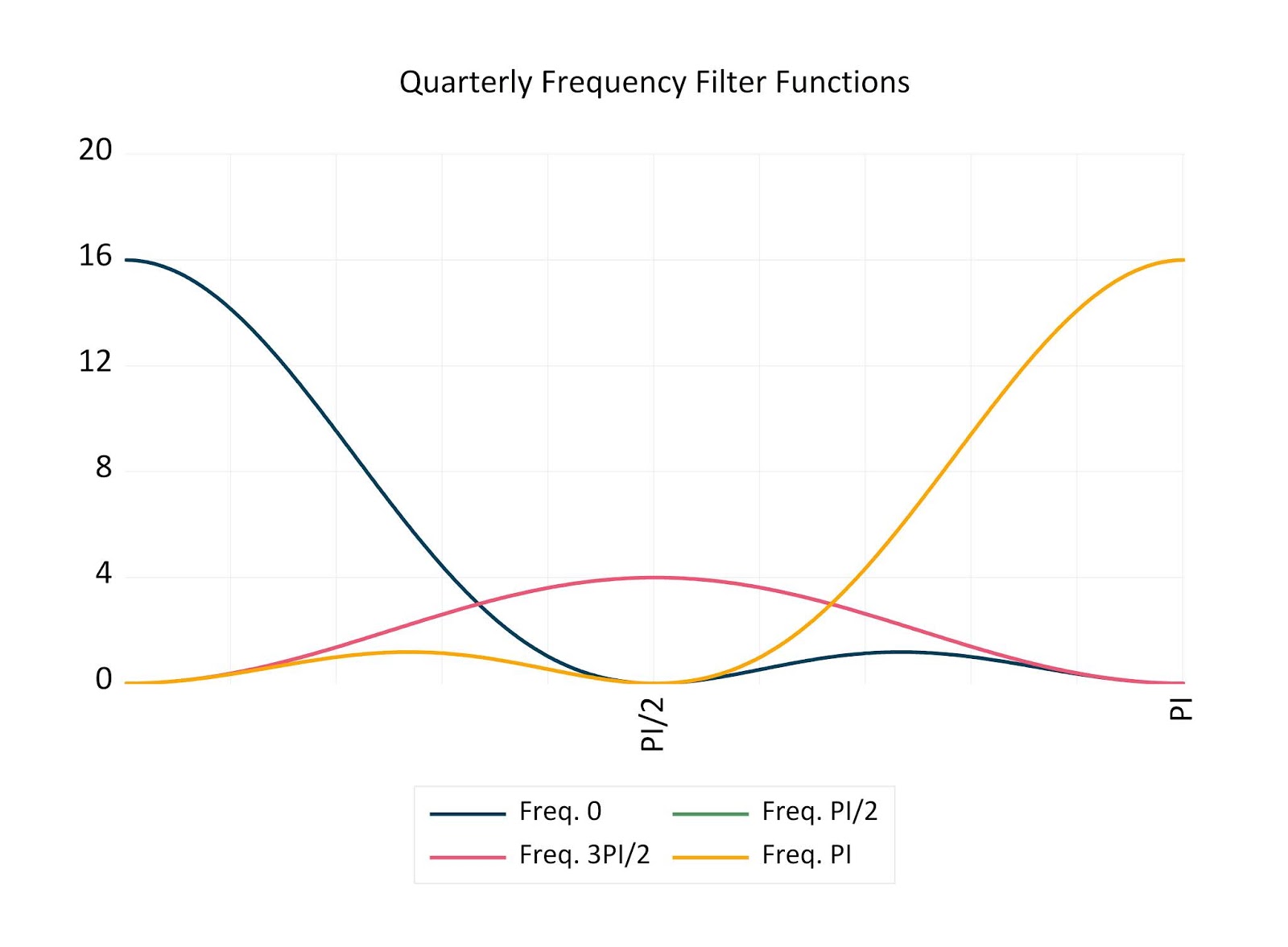

Seasonal Unit Root Test . In this entry we gave a brief introduction into the subject of seasonal unit root tests. Hegy.test ( x , deterministic = c ( 1 , 0 , 0 ). This chapter starts from dickey, hasza, and fuller (1984; Dhf hereafter), who use the ar (s) model (s denotes the number of seasons) to test for. Unit root tests cannot be used to assess whether a time series is stationary, or not. They can only detect integrated time series. Hylleberg, engle, granger and yoo (hegy) test statistics for the null hypothesis seasonal unit roots. Stationary components of y are in a(l), while deterministic seasonality is in μt when there are no seasonal unit roots in d(l). We highlighted the need to distinguish between deterministic. And the same holds for seasonal. Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test can be achieved by basing the seasonal unit root test.

from blog.eviews.com

Hegy.test ( x , deterministic = c ( 1 , 0 , 0 ). In this entry we gave a brief introduction into the subject of seasonal unit root tests. Dhf hereafter), who use the ar (s) model (s denotes the number of seasons) to test for. They can only detect integrated time series. Stationary components of y are in a(l), while deterministic seasonality is in μt when there are no seasonal unit roots in d(l). Hylleberg, engle, granger and yoo (hegy) test statistics for the null hypothesis seasonal unit roots. Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test can be achieved by basing the seasonal unit root test. Unit root tests cannot be used to assess whether a time series is stationary, or not. We highlighted the need to distinguish between deterministic. And the same holds for seasonal.

EViews Seasonal Unit Root Tests

Seasonal Unit Root Test And the same holds for seasonal. Stationary components of y are in a(l), while deterministic seasonality is in μt when there are no seasonal unit roots in d(l). In this entry we gave a brief introduction into the subject of seasonal unit root tests. Unit root tests cannot be used to assess whether a time series is stationary, or not. This chapter starts from dickey, hasza, and fuller (1984; And the same holds for seasonal. We highlighted the need to distinguish between deterministic. Hylleberg, engle, granger and yoo (hegy) test statistics for the null hypothesis seasonal unit roots. Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test can be achieved by basing the seasonal unit root test. Dhf hereafter), who use the ar (s) model (s denotes the number of seasons) to test for. They can only detect integrated time series. Hegy.test ( x , deterministic = c ( 1 , 0 , 0 ).

From www.slideserve.com

PPT Seasonal Unit Root Tests in Long Periodicity Cases David A Seasonal Unit Root Test Hylleberg, engle, granger and yoo (hegy) test statistics for the null hypothesis seasonal unit roots. In this entry we gave a brief introduction into the subject of seasonal unit root tests. They can only detect integrated time series. We highlighted the need to distinguish between deterministic. Hegy.test ( x , deterministic = c ( 1 , 0 , 0 ).. Seasonal Unit Root Test.

From blog.eviews.com

EViews Seasonal Unit Root Tests Seasonal Unit Root Test Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test can be achieved by basing the seasonal unit root test. They can only detect integrated time series. This chapter starts from dickey, hasza, and fuller (1984; Dhf hereafter), who use the ar (s) model (s denotes the number of seasons) to test for. In this. Seasonal Unit Root Test.

From www.researchgate.net

Tests for seasonal unit roots (nominal data) Download Table Seasonal Unit Root Test They can only detect integrated time series. Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test can be achieved by basing the seasonal unit root test. This chapter starts from dickey, hasza, and fuller (1984; We highlighted the need to distinguish between deterministic. In this entry we gave a brief introduction into the subject. Seasonal Unit Root Test.

From www.researchgate.net

Testing for seasonal unit root to simulated processes (S = 5 Seasonal Unit Root Test Hylleberg, engle, granger and yoo (hegy) test statistics for the null hypothesis seasonal unit roots. Dhf hereafter), who use the ar (s) model (s denotes the number of seasons) to test for. Stationary components of y are in a(l), while deterministic seasonality is in μt when there are no seasonal unit roots in d(l). Unit root tests cannot be used. Seasonal Unit Root Test.

From blog.eviews.com

EViews Seasonal Unit Root Tests Seasonal Unit Root Test In this entry we gave a brief introduction into the subject of seasonal unit root tests. They can only detect integrated time series. And the same holds for seasonal. We highlighted the need to distinguish between deterministic. Hegy.test ( x , deterministic = c ( 1 , 0 , 0 ). Stationary components of y are in a(l), while deterministic. Seasonal Unit Root Test.

From www.researchgate.net

Tests for Seasonal Unit Roots Download Table Seasonal Unit Root Test Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test can be achieved by basing the seasonal unit root test. Hylleberg, engle, granger and yoo (hegy) test statistics for the null hypothesis seasonal unit roots. Stationary components of y are in a(l), while deterministic seasonality is in μt when there are no seasonal unit roots. Seasonal Unit Root Test.

From www.semanticscholar.org

Table 2 from A Locally Optimal Seasonal UnitRoot Test Semantic Scholar Seasonal Unit Root Test Stationary components of y are in a(l), while deterministic seasonality is in μt when there are no seasonal unit roots in d(l). In this entry we gave a brief introduction into the subject of seasonal unit root tests. Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test can be achieved by basing the seasonal. Seasonal Unit Root Test.

From www.researchgate.net

Unit root test results after seasonal adjustment. Download Table Seasonal Unit Root Test Hegy.test ( x , deterministic = c ( 1 , 0 , 0 ). Stationary components of y are in a(l), while deterministic seasonality is in μt when there are no seasonal unit roots in d(l). And the same holds for seasonal. This chapter starts from dickey, hasza, and fuller (1984; Hylleberg, engle, granger and yoo (hegy) test statistics for. Seasonal Unit Root Test.

From www.researchgate.net

2 HEGY Test for Seasonal Unit Root Download Table Seasonal Unit Root Test And the same holds for seasonal. Unit root tests cannot be used to assess whether a time series is stationary, or not. Stationary components of y are in a(l), while deterministic seasonality is in μt when there are no seasonal unit roots in d(l). They can only detect integrated time series. This chapter starts from dickey, hasza, and fuller (1984;. Seasonal Unit Root Test.

From blog.eviews.com

EViews Seasonal Unit Root Tests Seasonal Unit Root Test Unit root tests cannot be used to assess whether a time series is stationary, or not. Stationary components of y are in a(l), while deterministic seasonality is in μt when there are no seasonal unit roots in d(l). And the same holds for seasonal. Hegy.test ( x , deterministic = c ( 1 , 0 , 0 ). They can. Seasonal Unit Root Test.

From www.researchgate.net

HEGY Seasonal Unit Root Tests Results Download Table Seasonal Unit Root Test Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test can be achieved by basing the seasonal unit root test. Hegy.test ( x , deterministic = c ( 1 , 0 , 0 ). They can only detect integrated time series. Dhf hereafter), who use the ar (s) model (s denotes the number of seasons). Seasonal Unit Root Test.

From www.semanticscholar.org

Figure 1 from An application of a new seasonal unit root test for Seasonal Unit Root Test We highlighted the need to distinguish between deterministic. Hegy.test ( x , deterministic = c ( 1 , 0 , 0 ). In this entry we gave a brief introduction into the subject of seasonal unit root tests. This chapter starts from dickey, hasza, and fuller (1984; They can only detect integrated time series. Stationary components of y are in. Seasonal Unit Root Test.

From www.slideserve.com

PPT Normally Distributed Seasonal Unit Root Tests D. A. Dickey North Seasonal Unit Root Test We highlighted the need to distinguish between deterministic. And the same holds for seasonal. Hylleberg, engle, granger and yoo (hegy) test statistics for the null hypothesis seasonal unit roots. Dhf hereafter), who use the ar (s) model (s denotes the number of seasons) to test for. This chapter starts from dickey, hasza, and fuller (1984; Unit root tests cannot be. Seasonal Unit Root Test.

From www.semanticscholar.org

Figure 2 from The Laglength Selection and Detrending Methods for HEGY Seasonal Unit Root Test Stationary components of y are in a(l), while deterministic seasonality is in μt when there are no seasonal unit roots in d(l). Hegy.test ( x , deterministic = c ( 1 , 0 , 0 ). Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test can be achieved by basing the seasonal unit root. Seasonal Unit Root Test.

From www.semanticscholar.org

Table 4 from Critical values for unit root tests in seasonal time Seasonal Unit Root Test And the same holds for seasonal. Stationary components of y are in a(l), while deterministic seasonality is in μt when there are no seasonal unit roots in d(l). Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test can be achieved by basing the seasonal unit root test. Hegy.test ( x , deterministic = c. Seasonal Unit Root Test.

From www.researchgate.net

HEGY seasonal unit root test results Download Table Seasonal Unit Root Test Hylleberg, engle, granger and yoo (hegy) test statistics for the null hypothesis seasonal unit roots. Unit root tests cannot be used to assess whether a time series is stationary, or not. This chapter starts from dickey, hasza, and fuller (1984; Dhf hereafter), who use the ar (s) model (s denotes the number of seasons) to test for. Leybourne and taylor. Seasonal Unit Root Test.

From www.researchgate.net

The seasonal unit root test HEGY Download Scientific Diagram Seasonal Unit Root Test This chapter starts from dickey, hasza, and fuller (1984; We highlighted the need to distinguish between deterministic. Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test can be achieved by basing the seasonal unit root test. Unit root tests cannot be used to assess whether a time series is stationary, or not. And the. Seasonal Unit Root Test.

From www.researchgate.net

Tests For Seasonal Unit Roots Download Table Seasonal Unit Root Test This chapter starts from dickey, hasza, and fuller (1984; Dhf hereafter), who use the ar (s) model (s denotes the number of seasons) to test for. Hylleberg, engle, granger and yoo (hegy) test statistics for the null hypothesis seasonal unit roots. And the same holds for seasonal. We highlighted the need to distinguish between deterministic. They can only detect integrated. Seasonal Unit Root Test.

From www.researchgate.net

Seasonal unit root test for number of swine slaughtered between Jan Seasonal Unit Root Test Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test can be achieved by basing the seasonal unit root test. Unit root tests cannot be used to assess whether a time series is stationary, or not. And the same holds for seasonal. We highlighted the need to distinguish between deterministic. Hegy.test ( x , deterministic. Seasonal Unit Root Test.

From www.slideserve.com

PPT Seasonal Unit Root Tests in Long Periodicity Cases PowerPoint Seasonal Unit Root Test They can only detect integrated time series. We highlighted the need to distinguish between deterministic. Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test can be achieved by basing the seasonal unit root test. Stationary components of y are in a(l), while deterministic seasonality is in μt when there are no seasonal unit roots. Seasonal Unit Root Test.

From www.slideserve.com

PPT Normally Distributed Seasonal Unit Root Tests D. A. Dickey North Seasonal Unit Root Test Dhf hereafter), who use the ar (s) model (s denotes the number of seasons) to test for. Unit root tests cannot be used to assess whether a time series is stationary, or not. And the same holds for seasonal. Stationary components of y are in a(l), while deterministic seasonality is in μt when there are no seasonal unit roots in. Seasonal Unit Root Test.

From www.researchgate.net

Tests For Seasonal Unit Roots Download Table Seasonal Unit Root Test Dhf hereafter), who use the ar (s) model (s denotes the number of seasons) to test for. This chapter starts from dickey, hasza, and fuller (1984; In this entry we gave a brief introduction into the subject of seasonal unit root tests. And the same holds for seasonal. They can only detect integrated time series. Unit root tests cannot be. Seasonal Unit Root Test.

From www.researchgate.net

Seasonal time series unit root tests. Download Table Seasonal Unit Root Test Unit root tests cannot be used to assess whether a time series is stationary, or not. Hegy.test ( x , deterministic = c ( 1 , 0 , 0 ). Dhf hereafter), who use the ar (s) model (s denotes the number of seasons) to test for. In this entry we gave a brief introduction into the subject of seasonal. Seasonal Unit Root Test.

From www.slideserve.com

PPT Seasonal Unit Root Tests in Long Periodicity Cases PowerPoint Seasonal Unit Root Test This chapter starts from dickey, hasza, and fuller (1984; Dhf hereafter), who use the ar (s) model (s denotes the number of seasons) to test for. They can only detect integrated time series. We highlighted the need to distinguish between deterministic. And the same holds for seasonal. Hylleberg, engle, granger and yoo (hegy) test statistics for the null hypothesis seasonal. Seasonal Unit Root Test.

From www.researchgate.net

Seasonal Unit Root Tests Download Table Seasonal Unit Root Test In this entry we gave a brief introduction into the subject of seasonal unit root tests. And the same holds for seasonal. Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test can be achieved by basing the seasonal unit root test. Hegy.test ( x , deterministic = c ( 1 , 0 , 0. Seasonal Unit Root Test.

From blog.eviews.com

EViews Seasonal Unit Root Tests Seasonal Unit Root Test In this entry we gave a brief introduction into the subject of seasonal unit root tests. Dhf hereafter), who use the ar (s) model (s denotes the number of seasons) to test for. They can only detect integrated time series. We highlighted the need to distinguish between deterministic. This chapter starts from dickey, hasza, and fuller (1984; Hylleberg, engle, granger. Seasonal Unit Root Test.

From www.scribd.com

Seasonal Unit Root Test PDF Time Series Ordinary Least Squares Seasonal Unit Root Test Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test can be achieved by basing the seasonal unit root test. Hegy.test ( x , deterministic = c ( 1 , 0 , 0 ). We highlighted the need to distinguish between deterministic. This chapter starts from dickey, hasza, and fuller (1984; Stationary components of y. Seasonal Unit Root Test.

From www.semanticscholar.org

Figure 2 from The Laglength Selection and Detrending Methods for HEGY Seasonal Unit Root Test Hegy.test ( x , deterministic = c ( 1 , 0 , 0 ). We highlighted the need to distinguish between deterministic. In this entry we gave a brief introduction into the subject of seasonal unit root tests. Unit root tests cannot be used to assess whether a time series is stationary, or not. Hylleberg, engle, granger and yoo (hegy). Seasonal Unit Root Test.

From www.researchgate.net

Seasonal unit root test by country for Ln(Tourist) Download Table Seasonal Unit Root Test They can only detect integrated time series. We highlighted the need to distinguish between deterministic. Unit root tests cannot be used to assess whether a time series is stationary, or not. Hegy.test ( x , deterministic = c ( 1 , 0 , 0 ). Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test. Seasonal Unit Root Test.

From blog.eviews.com

EViews Seasonal Unit Root Tests Seasonal Unit Root Test Stationary components of y are in a(l), while deterministic seasonality is in μt when there are no seasonal unit roots in d(l). They can only detect integrated time series. Hylleberg, engle, granger and yoo (hegy) test statistics for the null hypothesis seasonal unit roots. Dhf hereafter), who use the ar (s) model (s denotes the number of seasons) to test. Seasonal Unit Root Test.

From blog.eviews.com

EViews Seasonal Unit Root Tests Seasonal Unit Root Test And the same holds for seasonal. In this entry we gave a brief introduction into the subject of seasonal unit root tests. This chapter starts from dickey, hasza, and fuller (1984; Dhf hereafter), who use the ar (s) model (s denotes the number of seasons) to test for. Hylleberg, engle, granger and yoo (hegy) test statistics for the null hypothesis. Seasonal Unit Root Test.

From www.researchgate.net

Seasonal unit root test Download Table Seasonal Unit Root Test We highlighted the need to distinguish between deterministic. This chapter starts from dickey, hasza, and fuller (1984; And the same holds for seasonal. In this entry we gave a brief introduction into the subject of seasonal unit root tests. Dhf hereafter), who use the ar (s) model (s denotes the number of seasons) to test for. Hegy.test ( x ,. Seasonal Unit Root Test.

From www.semanticscholar.org

Figure 2 from The Laglength Selection and Detrending Methods for HEGY Seasonal Unit Root Test And the same holds for seasonal. Unit root tests cannot be used to assess whether a time series is stationary, or not. Hegy.test ( x , deterministic = c ( 1 , 0 , 0 ). In this entry we gave a brief introduction into the subject of seasonal unit root tests. Stationary components of y are in a(l), while. Seasonal Unit Root Test.

From www.researchgate.net

Bealieu and Miron Seasonal Unit Root Test Download Scientific Diagram Seasonal Unit Root Test Unit root tests cannot be used to assess whether a time series is stationary, or not. We highlighted the need to distinguish between deterministic. And the same holds for seasonal. They can only detect integrated time series. Stationary components of y are in a(l), while deterministic seasonality is in μt when there are no seasonal unit roots in d(l). Dhf. Seasonal Unit Root Test.

From www.researchgate.net

Seasonal unit root tests for vegetable and fruit prices. Download Seasonal Unit Root Test Leybourne and taylor (2003) claim that a similar improvement in power of the hegy test can be achieved by basing the seasonal unit root test. We highlighted the need to distinguish between deterministic. Hegy.test ( x , deterministic = c ( 1 , 0 , 0 ). Dhf hereafter), who use the ar (s) model (s denotes the number of. Seasonal Unit Root Test.