Market Beta Vs Correlation . beta denotes volatility, or systematic risk, of a security or portfolio compared to the market. Predicting these successfully is at the core of several aspects of investing, including both. Both are essential financial metrics, primarily when used alongside each other. focusing on correlated relative volatility. Beta is a statistical measure of the volatility of a stock versus the overall market. This equation shows that the idiosyncratic risk. where is the correlation of the two returns, and , are the respective volatilities. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. It is used in the capital asset pricing model. beta measures a stock's correlation to the market, which can help project its returns. covariance, correlation and beta are all measures that quantify relationships between variables.

from cameronharrison.com.au

focusing on correlated relative volatility. This equation shows that the idiosyncratic risk. beta measures a stock's correlation to the market, which can help project its returns. It is used in the capital asset pricing model. Predicting these successfully is at the core of several aspects of investing, including both. Beta is a statistical measure of the volatility of a stock versus the overall market. covariance, correlation and beta are all measures that quantify relationships between variables. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. beta denotes volatility, or systematic risk, of a security or portfolio compared to the market. where is the correlation of the two returns, and , are the respective volatilities.

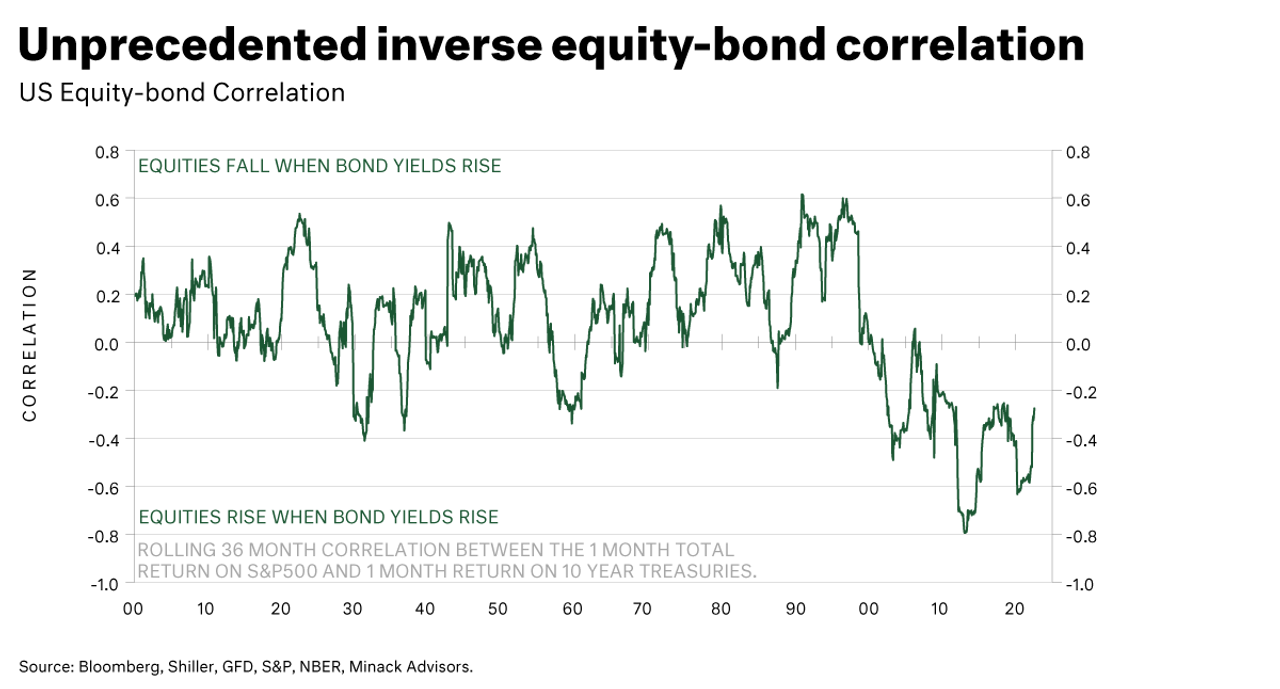

Market beta's free lunch has finished! Cameron Harrison

Market Beta Vs Correlation This equation shows that the idiosyncratic risk. Predicting these successfully is at the core of several aspects of investing, including both. where is the correlation of the two returns, and , are the respective volatilities. This equation shows that the idiosyncratic risk. covariance, correlation and beta are all measures that quantify relationships between variables. It is used in the capital asset pricing model. Beta is a statistical measure of the volatility of a stock versus the overall market. beta measures a stock's correlation to the market, which can help project its returns. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. beta denotes volatility, or systematic risk, of a security or portfolio compared to the market. focusing on correlated relative volatility. Both are essential financial metrics, primarily when used alongside each other.

From centerpointsecurities.com

Interconnectedness of Markets How It All Fits Together Market Beta Vs Correlation This equation shows that the idiosyncratic risk. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. covariance, correlation and beta are all measures that quantify relationships between variables. Beta is a statistical measure of the volatility of a stock versus the overall market. where is the correlation of the two returns, and , are the. Market Beta Vs Correlation.

From gregorygundersen.com

Simple Linear Regression and Correlation Market Beta Vs Correlation This equation shows that the idiosyncratic risk. where is the correlation of the two returns, and , are the respective volatilities. Beta is a statistical measure of the volatility of a stock versus the overall market. focusing on correlated relative volatility. Both are essential financial metrics, primarily when used alongside each other. Meanwhile, alpha compares a particular stock's. Market Beta Vs Correlation.

From endel.afphila.com

Unlevered Beta (Asset Beta) Formula, Calculation, and Examples Market Beta Vs Correlation beta measures a stock's correlation to the market, which can help project its returns. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. It is used in the capital asset pricing model. focusing on correlated relative volatility. beta denotes volatility, or systematic risk, of a security or portfolio compared to the market. where. Market Beta Vs Correlation.

From www.researchgate.net

Correlation Matrix of Market Indices. Download Scientific Diagram Market Beta Vs Correlation This equation shows that the idiosyncratic risk. focusing on correlated relative volatility. beta measures a stock's correlation to the market, which can help project its returns. Beta is a statistical measure of the volatility of a stock versus the overall market. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. It is used in the. Market Beta Vs Correlation.

From www.slideserve.com

PPT Weighted average cost of capital PowerPoint Presentation, free download ID1222875 Market Beta Vs Correlation Both are essential financial metrics, primarily when used alongside each other. beta measures a stock's correlation to the market, which can help project its returns. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. where is the correlation of the two returns, and , are the respective volatilities. Predicting these successfully is at the core. Market Beta Vs Correlation.

From nilssonhedge.com

NilssonHedge A Managed Futures & Hedge Fund Database Hedge Fund Correlation and Beta Market Beta Vs Correlation Meanwhile, alpha compares a particular stock's actual performance to the market's performance. It is used in the capital asset pricing model. Beta is a statistical measure of the volatility of a stock versus the overall market. beta measures a stock's correlation to the market, which can help project its returns. covariance, correlation and beta are all measures that. Market Beta Vs Correlation.

From www.researchgate.net

Market beta (The results of market model) Download Scientific Diagram Market Beta Vs Correlation covariance, correlation and beta are all measures that quantify relationships between variables. It is used in the capital asset pricing model. beta denotes volatility, or systematic risk, of a security or portfolio compared to the market. beta measures a stock's correlation to the market, which can help project its returns. This equation shows that the idiosyncratic risk.. Market Beta Vs Correlation.

From coinswitch.co

Understanding Beta In Stock Market Formula, Types & More [2024] Market Beta Vs Correlation Beta is a statistical measure of the volatility of a stock versus the overall market. It is used in the capital asset pricing model. Both are essential financial metrics, primarily when used alongside each other. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. beta denotes volatility, or systematic risk, of a security or portfolio compared. Market Beta Vs Correlation.

From www.reit.com

In the Wake of Stock Market Turmoil Returns, Volatility, Correlation, Beta, Diversification Market Beta Vs Correlation It is used in the capital asset pricing model. Predicting these successfully is at the core of several aspects of investing, including both. where is the correlation of the two returns, and , are the respective volatilities. This equation shows that the idiosyncratic risk. covariance, correlation and beta are all measures that quantify relationships between variables. focusing. Market Beta Vs Correlation.

From www.slideshare.net

Correlation and Beta Listed Equity REITs and Stocks Market Beta Vs Correlation where is the correlation of the two returns, and , are the respective volatilities. Predicting these successfully is at the core of several aspects of investing, including both. covariance, correlation and beta are all measures that quantify relationships between variables. Beta is a statistical measure of the volatility of a stock versus the overall market. focusing on. Market Beta Vs Correlation.

From tradedevils-indicators.com

Market Strength Correlation tradedevilsindicators Market Beta Vs Correlation beta denotes volatility, or systematic risk, of a security or portfolio compared to the market. This equation shows that the idiosyncratic risk. It is used in the capital asset pricing model. Predicting these successfully is at the core of several aspects of investing, including both. where is the correlation of the two returns, and , are the respective. Market Beta Vs Correlation.

From www.reit.com

Listed REITStock Correlation and Beta at 12year Low Nareit Market Beta Vs Correlation Meanwhile, alpha compares a particular stock's actual performance to the market's performance. beta denotes volatility, or systematic risk, of a security or portfolio compared to the market. It is used in the capital asset pricing model. Both are essential financial metrics, primarily when used alongside each other. where is the correlation of the two returns, and , are. Market Beta Vs Correlation.

From finance.yahoo.com

Portfolio Beta vs. Stock Beta What's the Difference? Market Beta Vs Correlation Predicting these successfully is at the core of several aspects of investing, including both. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. This equation shows that the idiosyncratic risk. Both are essential financial metrics, primarily when used alongside each other. It is used in the capital asset pricing model. covariance, correlation and beta are all. Market Beta Vs Correlation.

From match-prime.com

Market Basics Correlation. Its Types & Examples Market Beta Vs Correlation Predicting these successfully is at the core of several aspects of investing, including both. Beta is a statistical measure of the volatility of a stock versus the overall market. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. beta measures a stock's correlation to the market, which can help project its returns. It is used in. Market Beta Vs Correlation.

From www.businessinsider.nl

Beta can help you determine how much your portfolio will swing when the market moves Market Beta Vs Correlation where is the correlation of the two returns, and , are the respective volatilities. beta measures a stock's correlation to the market, which can help project its returns. It is used in the capital asset pricing model. Predicting these successfully is at the core of several aspects of investing, including both. Beta is a statistical measure of the. Market Beta Vs Correlation.

From design.udlvirtual.edu.pe

Scatter Plots Model 3 Types Of Correlation Design Talk Market Beta Vs Correlation beta measures a stock's correlation to the market, which can help project its returns. focusing on correlated relative volatility. Both are essential financial metrics, primarily when used alongside each other. covariance, correlation and beta are all measures that quantify relationships between variables. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. Beta is a. Market Beta Vs Correlation.

From slideplayer.com

Corporate Financial Theory ppt download Market Beta Vs Correlation beta measures a stock's correlation to the market, which can help project its returns. covariance, correlation and beta are all measures that quantify relationships between variables. This equation shows that the idiosyncratic risk. Both are essential financial metrics, primarily when used alongside each other. where is the correlation of the two returns, and , are the respective. Market Beta Vs Correlation.

From www.countingaccounting.com

How to Calculate Beta using Correlation and Volatility. Overview and Explanation Market Beta Vs Correlation It is used in the capital asset pricing model. beta denotes volatility, or systematic risk, of a security or portfolio compared to the market. where is the correlation of the two returns, and , are the respective volatilities. Both are essential financial metrics, primarily when used alongside each other. Meanwhile, alpha compares a particular stock's actual performance to. Market Beta Vs Correlation.

From cameronharrison.com.au

Market beta's free lunch has finished! Cameron Harrison Market Beta Vs Correlation Both are essential financial metrics, primarily when used alongside each other. where is the correlation of the two returns, and , are the respective volatilities. It is used in the capital asset pricing model. beta denotes volatility, or systematic risk, of a security or portfolio compared to the market. beta measures a stock's correlation to the market,. Market Beta Vs Correlation.

From ca.news.yahoo.com

Portfolio Beta vs. Stock Beta What's the Difference? Market Beta Vs Correlation Beta is a statistical measure of the volatility of a stock versus the overall market. focusing on correlated relative volatility. where is the correlation of the two returns, and , are the respective volatilities. beta measures a stock's correlation to the market, which can help project its returns. Meanwhile, alpha compares a particular stock's actual performance to. Market Beta Vs Correlation.

From indicatorspot.com

Market Correlation Indicator For MT4 Download FREE IndicatorsPot Market Beta Vs Correlation Meanwhile, alpha compares a particular stock's actual performance to the market's performance. Beta is a statistical measure of the volatility of a stock versus the overall market. This equation shows that the idiosyncratic risk. beta denotes volatility, or systematic risk, of a security or portfolio compared to the market. Predicting these successfully is at the core of several aspects. Market Beta Vs Correlation.

From blog.dhan.co

What is Beta in Stock Market Definition, Calculation & Uses Dhan Blog Market Beta Vs Correlation Beta is a statistical measure of the volatility of a stock versus the overall market. where is the correlation of the two returns, and , are the respective volatilities. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. Predicting these successfully is at the core of several aspects of investing, including both. beta measures a. Market Beta Vs Correlation.

From www.chegg.com

Solved Problem 1129 Correlation and Beta You have been Market Beta Vs Correlation beta measures a stock's correlation to the market, which can help project its returns. focusing on correlated relative volatility. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. This equation shows that the idiosyncratic risk. where is the correlation of the two returns, and , are the respective volatilities. Both are essential financial metrics,. Market Beta Vs Correlation.

From www.slideserve.com

PPT Final project Exploring the structure of correlation PowerPoint Presentation ID2257352 Market Beta Vs Correlation Both are essential financial metrics, primarily when used alongside each other. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. covariance, correlation and beta are all measures that quantify relationships between variables. where is the correlation of the two returns, and , are the respective volatilities. It is used in the capital asset pricing model.. Market Beta Vs Correlation.

From www.ferventlearning.com

What is Systematic Risk (aka Beta)? How to Calculate Beta of a Stock? Everything You Need to Know. Market Beta Vs Correlation beta denotes volatility, or systematic risk, of a security or portfolio compared to the market. beta measures a stock's correlation to the market, which can help project its returns. It is used in the capital asset pricing model. Predicting these successfully is at the core of several aspects of investing, including both. Meanwhile, alpha compares a particular stock's. Market Beta Vs Correlation.

From www.slideserve.com

PPT CAPM Implications PowerPoint Presentation, free download ID2333274 Market Beta Vs Correlation beta denotes volatility, or systematic risk, of a security or portfolio compared to the market. Predicting these successfully is at the core of several aspects of investing, including both. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. This equation shows that the idiosyncratic risk. It is used in the capital asset pricing model. where. Market Beta Vs Correlation.

From www.tastylive.com

Beta Correlation May Not Tell All Market Measures tastylive Market Beta Vs Correlation Predicting these successfully is at the core of several aspects of investing, including both. Beta is a statistical measure of the volatility of a stock versus the overall market. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. focusing on correlated relative volatility. It is used in the capital asset pricing model. where is the. Market Beta Vs Correlation.

From www.businessinsider.com

CHART Global Equity Market Correlation Business Insider Market Beta Vs Correlation This equation shows that the idiosyncratic risk. Beta is a statistical measure of the volatility of a stock versus the overall market. Predicting these successfully is at the core of several aspects of investing, including both. beta measures a stock's correlation to the market, which can help project its returns. Both are essential financial metrics, primarily when used alongside. Market Beta Vs Correlation.

From topforeignstocks.com

Relationship between Stock Market, GDP and Earnings Market Beta Vs Correlation focusing on correlated relative volatility. Predicting these successfully is at the core of several aspects of investing, including both. It is used in the capital asset pricing model. This equation shows that the idiosyncratic risk. beta denotes volatility, or systematic risk, of a security or portfolio compared to the market. Both are essential financial metrics, primarily when used. Market Beta Vs Correlation.

From www.cnbc.com

Delivering beta the stocks tracking closest to market Market Beta Vs Correlation focusing on correlated relative volatility. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. It is used in the capital asset pricing model. Both are essential financial metrics, primarily when used alongside each other. where is the correlation of the two returns, and , are the respective volatilities. beta denotes volatility, or systematic risk,. Market Beta Vs Correlation.

From hedgenordic.com

Correlation and Beta Searching for Diversification HedgeNordic Market Beta Vs Correlation Predicting these successfully is at the core of several aspects of investing, including both. This equation shows that the idiosyncratic risk. It is used in the capital asset pricing model. covariance, correlation and beta are all measures that quantify relationships between variables. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. beta measures a stock's. Market Beta Vs Correlation.

From abwinsights.com

What Fraction of Smart Beta is Dumb Beta? AlphaBetaWorks Insights Market Beta Vs Correlation Both are essential financial metrics, primarily when used alongside each other. Beta is a statistical measure of the volatility of a stock versus the overall market. focusing on correlated relative volatility. beta denotes volatility, or systematic risk, of a security or portfolio compared to the market. It is used in the capital asset pricing model. This equation shows. Market Beta Vs Correlation.

From www.educba.com

Beta Formula Calculator for Beta Formula (With Excel template) Market Beta Vs Correlation covariance, correlation and beta are all measures that quantify relationships between variables. This equation shows that the idiosyncratic risk. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. focusing on correlated relative volatility. Both are essential financial metrics, primarily when used alongside each other. Beta is a statistical measure of the volatility of a stock. Market Beta Vs Correlation.

From endel.afphila.com

Beta What is Beta (β) in Finance? Guide and Examples Market Beta Vs Correlation It is used in the capital asset pricing model. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. Both are essential financial metrics, primarily when used alongside each other. beta denotes volatility, or systematic risk, of a security or portfolio compared to the market. focusing on correlated relative volatility. This equation shows that the idiosyncratic. Market Beta Vs Correlation.

From www.pinterest.com

What is Beta? Stock trading strategies, Stock trading learning, Startup business plan Market Beta Vs Correlation Predicting these successfully is at the core of several aspects of investing, including both. Meanwhile, alpha compares a particular stock's actual performance to the market's performance. It is used in the capital asset pricing model. Both are essential financial metrics, primarily when used alongside each other. where is the correlation of the two returns, and , are the respective. Market Beta Vs Correlation.