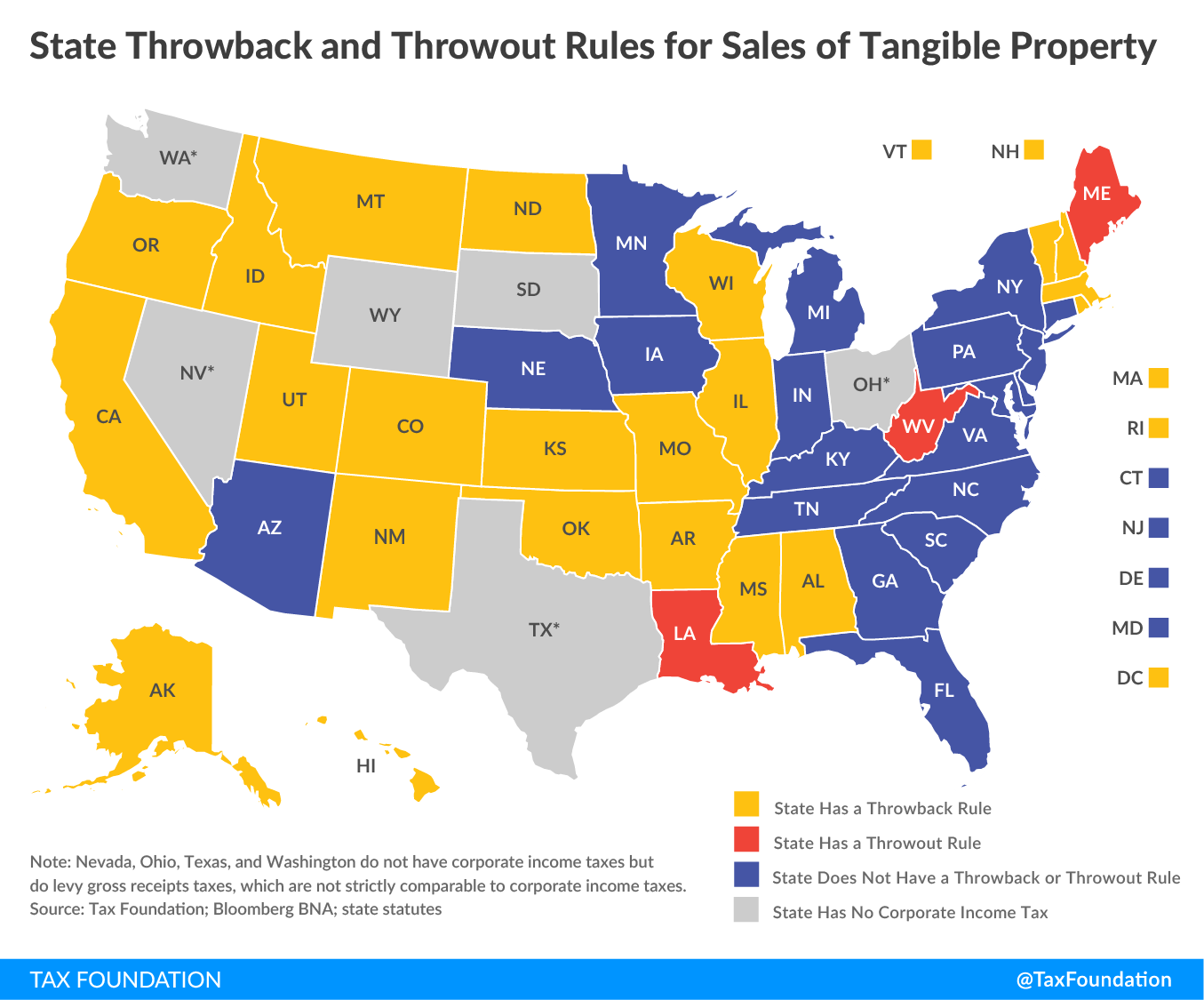

Throwback Method . Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. They also generally increase the tax base of. The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income, or uni. Throwout and throwback rules are ostensibly designed to promote full apportionment of income; The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. With the throwback rule, nowhere income is placed in the numerator (the amount allocated to the state); Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though.

from taxfoundation.org

They also generally increase the tax base of. Throwout and throwback rules are ostensibly designed to promote full apportionment of income; Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income, or uni. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. With the throwback rule, nowhere income is placed in the numerator (the amount allocated to the state); The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness.

Throwback Rules and Throwout Rules A Primer Tax Foundation

Throwback Method Throwout and throwback rules are ostensibly designed to promote full apportionment of income; They also generally increase the tax base of. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income, or uni. Throwout and throwback rules are ostensibly designed to promote full apportionment of income; The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. With the throwback rule, nowhere income is placed in the numerator (the amount allocated to the state);

From www.youtube.com

A Throwback to the James Method YouTube Throwback Method Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. Throwout and throwback rules are ostensibly designed to promote full apportionment of income; Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the. Throwback Method.

From hipstrumentals.com

Method Man & Redman Da Rockwilder (Instrumental) (Prod. By Rockwilder) Throwback Thursdays Throwback Method They also generally increase the tax base of. The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income, or uni. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. Throwout and throwback rules are ostensibly. Throwback Method.

From hiphopdx.com

Never Before Heard Throwback Method Man Freestyles In 2004 HipHopDX Throwback Method With the throwback rule, nowhere income is placed in the numerator (the amount allocated to the state); They also generally increase the tax base of. The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income, or uni. The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness.. Throwback Method.

From www.musicgrotto.com

55 Best Throwback Songs Of All Time (Ultimate List) Music Grotto Throwback Method Throwout and throwback rules are ostensibly designed to promote full apportionment of income; The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income, or uni. They also generally increase the tax base of. With the throwback rule, nowhere income is placed in the numerator (the amount allocated to the state); The throwback rule. Throwback Method.

From www.youtube.com

THROWBACK MARQUEE MATCHUPS METHOD COMPLETED 18/06/20 (NO LOYALTY CHEAPEST WAY) YouTube Throwback Method Throwout and throwback rules are ostensibly designed to promote full apportionment of income; They also generally increase the tax base of. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. The throwback rule ensures corporations pay taxes on all profits, closing tax. Throwback Method.

From www.youtube.com

Throwback Bowling! OG Brunswick Method On A Pattern. YouTube Throwback Method Throwout and throwback rules are ostensibly designed to promote full apportionment of income; They also generally increase the tax base of. The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. With the throwback rule, nowhere income is placed in the numerator (the amount allocated to the state); Under throwback rules, sales of tangible. Throwback Method.

From www.sandiegouniontribune.com

UnionTribune photographer uses a throwback method to document Padres in spring training The Throwback Method Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income,. Throwback Method.

From gosupercreative.com

Throwback Traits Overview Products, Customer Services Of Throwback Traits, Benefits, Features Throwback Method Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. They also generally increase the tax base of. The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. With the throwback rule, nowhere income is placed in. Throwback Method.

From www.kickmag.net

Throwback Method ManBring The Pain Kick Mag Throwback Method The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income, or uni. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated,. Throwback Method.

From wtcfolife.blogspot.com

WTCFoLife Blog [Throwback] Method Man & Sharleen Spiteri On the cover of The Face Magazine (Dec 97) Throwback Method The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income, or uni. The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. Throwout and throwback rules are ostensibly designed to promote full apportionment of income; They also generally increase the tax base of. With the throwback rule,. Throwback Method.

From www.pinterest.com

90s Trend Throwback Methods to Get Nia Longs Look 90s fashion, Fashion, Black girl fashion Throwback Method Throwout and throwback rules are ostensibly designed to promote full apportionment of income; Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. With the throwback rule, nowhere income is placed in the numerator (the amount allocated to the state); The throwback rule. Throwback Method.

From www.sandiegouniontribune.com

UnionTribune photographer uses a throwback method to document Padres in spring training The Throwback Method They also generally increase the tax base of. With the throwback rule, nowhere income is placed in the numerator (the amount allocated to the state); Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. The throwback rule ensures corporations pay taxes on. Throwback Method.

From www.thecoderschool.com

Coding Classes and Camps for Kids Near You theCoderSchool Blog Throwbackstudymethodsthat Throwback Method With the throwback rule, nowhere income is placed in the numerator (the amount allocated to the state); The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. Throwout and throwback rules are ostensibly designed to promote full apportionment of income; Under throwback rules, sales of tangible property that are not taxable in the destination. Throwback Method.

From wtcfolife.blogspot.com

WTCFoLife Blog [Throwback] Method Man, Raekwon & RZA On the cover of The Source (1995) Throwback Method The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income, or uni. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. Throwout and throwback rules are ostensibly designed to promote full apportionment of income; They. Throwback Method.

From wtcfolife.blogspot.com

WTCFoLife Blog [Throwback] Method Man, Ghostface Killah & Raekwon On the cover of The Source Throwback Method The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income, or uni. They also generally increase the tax base of. With the throwback rule, nowhere income is placed in the numerator (the amount allocated to the state);. Throwback Method.

From www.youtube.com

THROWBACK Method Man x Busta Rhymes Whats Happenin Reaction YouTube Throwback Method They also generally increase the tax base of. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. With the throwback rule, nowhere income is placed in the numerator (the amount allocated to the state); Under throwback rules, sales of tangible property that. Throwback Method.

From www.yahoo.com

Drake shares throwback Method Man clip in response to recent Yasiin Bey critique Throwback Method The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income, or uni. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and. Throwback Method.

From wtcfolife.blogspot.com

WTCFoLife Blog [Throwback] Method Man On the cover of Dub Magazine (2004) Throwback Method They also generally increase the tax base of. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated,. Throwback Method.

From www.reddit.com

Ran out of kings so have to use the throwback method r/ArtOfRolling Throwback Method Throwout and throwback rules are ostensibly designed to promote full apportionment of income; The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. Under throwback rules, sales. Throwback Method.

From wtcfolife.blogspot.com

WTCFoLife Blog [Throwback] Method Man On the cover of High Times Magazine (Aug 96) Throwback Method Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown. Throwback Method.

From soundcloud.com

Stream Method Man & Redman freestyle BEST EVER! unreleased throwback 1999 Westwood Blackout by Throwback Method They also generally increase the tax base of. The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income, or uni. Throwout and throwback rules are ostensibly designed to promote full apportionment of income; Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the. Throwback Method.

From wtcfolife.blogspot.com

WTCFoLife Blog [Throwback] Method Man On the cover of Rap Sheet Magazine (Jan 95) Throwback Method Throwout and throwback rules are ostensibly designed to promote full apportionment of income; Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. With the throwback rule,. Throwback Method.

From www.sandiegouniontribune.com

UT photographer uses a throwback method to document Padres in spring training San Diego Union Throwback Method Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income, or uni. With the throwback rule, nowhere income is placed in the numerator (the amount allocated. Throwback Method.

From www.youtube.com

Throwback Party Eclectic Method // Dennis Lopes // DJ Gio YouTube Throwback Method Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. They also generally increase the tax base of. Throwout and throwback rules are ostensibly designed to promote full apportionment of income; Under throwback rules, sales of tangible property that are not taxable in. Throwback Method.

From www.youtube.com

Method Man greatest ever freestyle! Throwback '95 Westwood YouTube Throwback Method Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. The throwback rule ensures corporations pay. Throwback Method.

From www.youtube.com

Method Man & Redman freestyle BEST EVER! unreleased throwback 1999 Westwood Blackout YouTube Throwback Method Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. Throwout and throwback rules are ostensibly designed to promote full apportionment of income; Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the. Throwback Method.

From wtcfolife.blogspot.com

WTCFoLife Blog [Throwback] Method Man & Iverson On the cover of Complex Magazine (June 2003) Throwback Method Throwout and throwback rules are ostensibly designed to promote full apportionment of income; Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income, or uni. With. Throwback Method.

From wtcfolife.blogspot.com

WTCFoLife Blog [Throwback] Method Man & RZA On the cover of HHC Magazine (Jan 99) Throwback Method With the throwback rule, nowhere income is placed in the numerator (the amount allocated to the state); Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net. Throwback Method.

From www.freebeerandhotwings.com

Segment 17 A Throwback Method Of Recording Free Beer and Hot Wings Throwback Method The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income, or uni. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. Throwout and throwback rules are ostensibly designed to promote full apportionment of income; With. Throwback Method.

From taxfoundation.org

Throwback Rules and Throwout Rules A Primer Tax Foundation Throwback Method They also generally increase the tax base of. The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. Under throwback rules, sales of tangible property that are. Throwback Method.

From www.kickmag.net

Throwback Method ManBring The Pain Kick Mag Throwback Method The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. They also generally increase the tax base of. With the throwback rule, nowhere income is placed in. Throwback Method.

From www.vanndigital.com

Video Method Man The Riddler [VDN Throwback] Throwback Method The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. They also generally increase the tax base of. Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. The throwback rules hinge upon the distinction between distributable. Throwback Method.

From www.reddit.com

Had to use the old throwback method r/Tinder Throwback Method With the throwback rule, nowhere income is placed in the numerator (the amount allocated to the state); The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. Throwout and throwback rules are ostensibly designed to promote full apportionment of income; They also generally increase the tax base of. Under throwback rules, sales of tangible. Throwback Method.

From wtcfolife.blogspot.com

WTCFoLife Blog [Throwback] Method Man On the cover of Juice Magazine (March 2003) Throwback Method The throwback rule ensures corporations pay taxes on all profits, closing tax loopholes and promoting fairness. The throwback rules hinge upon the distinction between distributable net income, or dni, and undistributed net income, or uni. Throwout and throwback rules are ostensibly designed to promote full apportionment of income; Under throwback rules, sales of tangible property that are not taxable in. Throwback Method.

From soundcloud.com

Stream Method Man freestyle goes off on The Set Up Throwback 2004 Westwood by timwestwood Throwback Method Under throwback rules, sales of tangible property that are not taxable in the destination state are “thrown back” into the state where the sale originated, even though. Throwout and throwback rules are ostensibly designed to promote full apportionment of income; With the throwback rule, nowhere income is placed in the numerator (the amount allocated to the state); They also generally. Throwback Method.