Short Run Equilibrium Price Microeconomics . Define equilibrium price and quantity and identify them in a market; Differentiate between total and marginal product. Understand the relationship between production and costs. Identify a demand curve and a supply curve. Define surpluses and shortages and explain how they cause the price to move towards equilibrium Understand that every factor of production has a corresponding factor price. First let’s first focus on. Differentiate between production in the short run and in the long run. Explain equilibrium, equilibrium price, and equilibrium quantity. The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant (taken to be exogenous).

from www.slideserve.com

Understand that every factor of production has a corresponding factor price. The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant (taken to be exogenous). Define equilibrium price and quantity and identify them in a market; Define surpluses and shortages and explain how they cause the price to move towards equilibrium Differentiate between production in the short run and in the long run. Explain equilibrium, equilibrium price, and equilibrium quantity. First let’s first focus on. Identify a demand curve and a supply curve. Understand the relationship between production and costs. Differentiate between total and marginal product.

PPT Competitive Markets PowerPoint Presentation, free download ID942310

Short Run Equilibrium Price Microeconomics Differentiate between total and marginal product. The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant (taken to be exogenous). Define equilibrium price and quantity and identify them in a market; Identify a demand curve and a supply curve. Differentiate between production in the short run and in the long run. Differentiate between total and marginal product. Explain equilibrium, equilibrium price, and equilibrium quantity. Define surpluses and shortages and explain how they cause the price to move towards equilibrium Understand that every factor of production has a corresponding factor price. Understand the relationship between production and costs. First let’s first focus on.

From negativoapositivo.com

Example Of Short Run In Economics Short Run Equilibrium Price Microeconomics Understand that every factor of production has a corresponding factor price. Understand the relationship between production and costs. The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant (taken to be exogenous). Define surpluses and shortages and explain how they cause the price to move towards equilibrium Differentiate between total. Short Run Equilibrium Price Microeconomics.

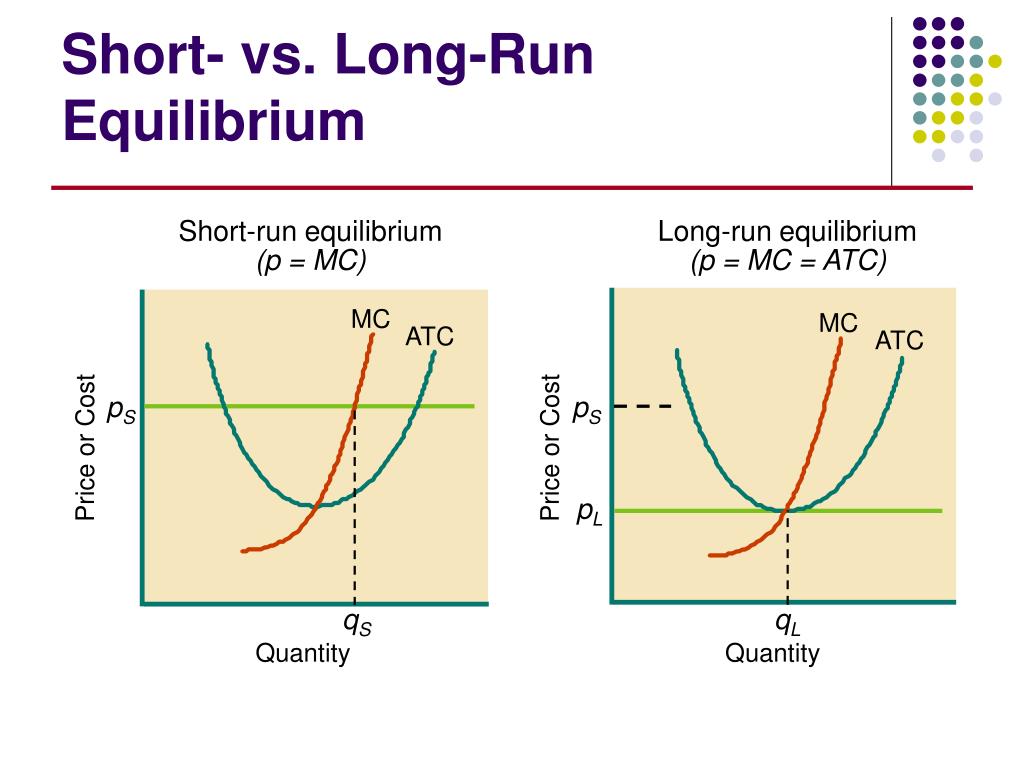

From slidetodoc.com

Aggregate Equilibrium Macroeconomic Theory Recessionary Gap Inflationary Gap Short Run Equilibrium Price Microeconomics Identify a demand curve and a supply curve. Understand that every factor of production has a corresponding factor price. Define equilibrium price and quantity and identify them in a market; Differentiate between total and marginal product. Define surpluses and shortages and explain how they cause the price to move towards equilibrium Explain equilibrium, equilibrium price, and equilibrium quantity. First let’s. Short Run Equilibrium Price Microeconomics.

From www.wizeprep.com

Short Run vs Long Run Equilibrium Wize University Microeconomics Textbook Wizeprep Short Run Equilibrium Price Microeconomics Understand the relationship between production and costs. Differentiate between total and marginal product. First let’s first focus on. The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant (taken to be exogenous). Identify a demand curve and a supply curve. Define surpluses and shortages and explain how they cause the. Short Run Equilibrium Price Microeconomics.

From www.intelligenteconomist.com

Perfect Competition Short Run Intelligent Economist Short Run Equilibrium Price Microeconomics First let’s first focus on. Differentiate between total and marginal product. Differentiate between production in the short run and in the long run. Understand the relationship between production and costs. Define surpluses and shortages and explain how they cause the price to move towards equilibrium Explain equilibrium, equilibrium price, and equilibrium quantity. Define equilibrium price and quantity and identify them. Short Run Equilibrium Price Microeconomics.

From www.intelligenteconomist.com

Monopoly Market Structure Intelligent Economist Short Run Equilibrium Price Microeconomics Define equilibrium price and quantity and identify them in a market; Differentiate between production in the short run and in the long run. Define surpluses and shortages and explain how they cause the price to move towards equilibrium First let’s first focus on. Understand the relationship between production and costs. Explain equilibrium, equilibrium price, and equilibrium quantity. Identify a demand. Short Run Equilibrium Price Microeconomics.

From www.economicshelp.org

Perfect competition Economics Help Short Run Equilibrium Price Microeconomics Define surpluses and shortages and explain how they cause the price to move towards equilibrium Understand that every factor of production has a corresponding factor price. Differentiate between total and marginal product. Define equilibrium price and quantity and identify them in a market; Explain equilibrium, equilibrium price, and equilibrium quantity. Understand the relationship between production and costs. First let’s first. Short Run Equilibrium Price Microeconomics.

From saylordotorg.github.io

Supply and Demand Short Run Equilibrium Price Microeconomics The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant (taken to be exogenous). Understand that every factor of production has a corresponding factor price. Identify a demand curve and a supply curve. Understand the relationship between production and costs. Explain equilibrium, equilibrium price, and equilibrium quantity. Differentiate between total. Short Run Equilibrium Price Microeconomics.

From open.lib.umn.edu

9.2 Output Determination in the Short Run Principles of Economics Short Run Equilibrium Price Microeconomics Define surpluses and shortages and explain how they cause the price to move towards equilibrium Differentiate between total and marginal product. Define equilibrium price and quantity and identify them in a market; Understand that every factor of production has a corresponding factor price. Explain equilibrium, equilibrium price, and equilibrium quantity. Identify a demand curve and a supply curve. Differentiate between. Short Run Equilibrium Price Microeconomics.

From econknowhow.blogspot.com

EconKnowHow Perfect Competition Short Run Equilibrium Short Run Equilibrium Price Microeconomics Define equilibrium price and quantity and identify them in a market; Understand that every factor of production has a corresponding factor price. Define surpluses and shortages and explain how they cause the price to move towards equilibrium Differentiate between total and marginal product. Explain equilibrium, equilibrium price, and equilibrium quantity. Understand the relationship between production and costs. Differentiate between production. Short Run Equilibrium Price Microeconomics.

From 2012books.lardbucket.org

Perfect Competition in the Long Run Short Run Equilibrium Price Microeconomics Define surpluses and shortages and explain how they cause the price to move towards equilibrium The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant (taken to be exogenous). First let’s first focus on. Differentiate between production in the short run and in the long run. Understand that every factor. Short Run Equilibrium Price Microeconomics.

From uw.pressbooks.pub

Demand, Supply, and Equilibrium Microeconomics for Managers Short Run Equilibrium Price Microeconomics Explain equilibrium, equilibrium price, and equilibrium quantity. Differentiate between production in the short run and in the long run. Differentiate between total and marginal product. Define equilibrium price and quantity and identify them in a market; First let’s first focus on. The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held. Short Run Equilibrium Price Microeconomics.

From analystprep.com

Marginal Cost and Revenue, Economic Profit CFA Level 1 AnalystPrep Short Run Equilibrium Price Microeconomics First let’s first focus on. Differentiate between production in the short run and in the long run. Understand the relationship between production and costs. The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant (taken to be exogenous). Understand that every factor of production has a corresponding factor price. Define. Short Run Equilibrium Price Microeconomics.

From www.youtube.com

Perfect Competition ShortRun Equilibrium of a Firm Super Normal Profit YouTube Short Run Equilibrium Price Microeconomics Understand the relationship between production and costs. Differentiate between production in the short run and in the long run. Explain equilibrium, equilibrium price, and equilibrium quantity. The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant (taken to be exogenous). Define equilibrium price and quantity and identify them in a. Short Run Equilibrium Price Microeconomics.

From www.studocu.com

Microeconomics short run equilibrium Studocu Short Run Equilibrium Price Microeconomics Differentiate between production in the short run and in the long run. Understand that every factor of production has a corresponding factor price. Understand the relationship between production and costs. Define equilibrium price and quantity and identify them in a market; Explain equilibrium, equilibrium price, and equilibrium quantity. First let’s first focus on. Differentiate between total and marginal product. The. Short Run Equilibrium Price Microeconomics.

From ecampusontario.pressbooks.pub

10.4 Markup and Excess Capacity Principles of Microeconomics Short Run Equilibrium Price Microeconomics Define equilibrium price and quantity and identify them in a market; Understand that every factor of production has a corresponding factor price. Understand the relationship between production and costs. Differentiate between total and marginal product. Define surpluses and shortages and explain how they cause the price to move towards equilibrium Differentiate between production in the short run and in the. Short Run Equilibrium Price Microeconomics.

From www.youtube.com

Calculation of Profit or Loss in the Short Run Microeconomics YouTube Short Run Equilibrium Price Microeconomics Define surpluses and shortages and explain how they cause the price to move towards equilibrium Explain equilibrium, equilibrium price, and equilibrium quantity. Differentiate between production in the short run and in the long run. Differentiate between total and marginal product. Identify a demand curve and a supply curve. Define equilibrium price and quantity and identify them in a market; The. Short Run Equilibrium Price Microeconomics.

From www.youtube.com

Short Run Macroeconomic Equilibrium YouTube Short Run Equilibrium Price Microeconomics Identify a demand curve and a supply curve. Understand that every factor of production has a corresponding factor price. Define surpluses and shortages and explain how they cause the price to move towards equilibrium Differentiate between production in the short run and in the long run. Explain equilibrium, equilibrium price, and equilibrium quantity. First let’s first focus on. Define equilibrium. Short Run Equilibrium Price Microeconomics.

From www.tutor2u.net

Monopolistic Competition tutor2u Economics Short Run Equilibrium Price Microeconomics Understand that every factor of production has a corresponding factor price. Explain equilibrium, equilibrium price, and equilibrium quantity. Identify a demand curve and a supply curve. Define equilibrium price and quantity and identify them in a market; First let’s first focus on. Differentiate between total and marginal product. Understand the relationship between production and costs. Differentiate between production in the. Short Run Equilibrium Price Microeconomics.

From passnownow.com

SS1 Economics Third Term Equilibrium Price/Price Determination Passnownow Short Run Equilibrium Price Microeconomics Differentiate between production in the short run and in the long run. Define surpluses and shortages and explain how they cause the price to move towards equilibrium Understand the relationship between production and costs. First let’s first focus on. The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant (taken. Short Run Equilibrium Price Microeconomics.

From articles.outlier.org

What Is Equilibrium In Microeconomics? Outlier Short Run Equilibrium Price Microeconomics Differentiate between total and marginal product. First let’s first focus on. Differentiate between production in the short run and in the long run. The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant (taken to be exogenous). Understand that every factor of production has a corresponding factor price. Understand the. Short Run Equilibrium Price Microeconomics.

From www.mrbanks.co.uk

Perfect Competition — Mr Banks Economics Hub Resources, Tutoring & Exam Prep Short Run Equilibrium Price Microeconomics Differentiate between production in the short run and in the long run. Define equilibrium price and quantity and identify them in a market; Identify a demand curve and a supply curve. The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant (taken to be exogenous). Explain equilibrium, equilibrium price, and. Short Run Equilibrium Price Microeconomics.

From courses.lumenlearning.com

Equilibrium, Price, and Quantity Introduction to Business Short Run Equilibrium Price Microeconomics First let’s first focus on. Understand the relationship between production and costs. Define surpluses and shortages and explain how they cause the price to move towards equilibrium Identify a demand curve and a supply curve. Explain equilibrium, equilibrium price, and equilibrium quantity. Understand that every factor of production has a corresponding factor price. Define equilibrium price and quantity and identify. Short Run Equilibrium Price Microeconomics.

From www.tutor2u.net

Perfect Competition Short Run Price and Output… tutor2u Economics Short Run Equilibrium Price Microeconomics Understand that every factor of production has a corresponding factor price. Differentiate between production in the short run and in the long run. Explain equilibrium, equilibrium price, and equilibrium quantity. Define surpluses and shortages and explain how they cause the price to move towards equilibrium Understand the relationship between production and costs. Define equilibrium price and quantity and identify them. Short Run Equilibrium Price Microeconomics.

From psu.pb.unizin.org

Perfect Competition Introduction to Microeconomics Short Run Equilibrium Price Microeconomics Differentiate between total and marginal product. Define surpluses and shortages and explain how they cause the price to move towards equilibrium The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant (taken to be exogenous). Differentiate between production in the short run and in the long run. First let’s first. Short Run Equilibrium Price Microeconomics.

From webapi.bu.edu

🎉 Short run macroeconomic equilibrium. Macroeconomic Equilibrium Definition, Short Run & Long Short Run Equilibrium Price Microeconomics Understand that every factor of production has a corresponding factor price. Differentiate between production in the short run and in the long run. Explain equilibrium, equilibrium price, and equilibrium quantity. Define equilibrium price and quantity and identify them in a market; Differentiate between total and marginal product. Identify a demand curve and a supply curve. The short run refers to. Short Run Equilibrium Price Microeconomics.

From courses.lumenlearning.com

Equilibrium, Surplus, and Shortage Microeconomics Short Run Equilibrium Price Microeconomics Differentiate between production in the short run and in the long run. Identify a demand curve and a supply curve. Understand the relationship between production and costs. Explain equilibrium, equilibrium price, and equilibrium quantity. First let’s first focus on. Define equilibrium price and quantity and identify them in a market; The short run refers to what happens while some variables. Short Run Equilibrium Price Microeconomics.

From www.economicshelp.org

Diagram of Perfect Competition Economics Help Short Run Equilibrium Price Microeconomics Define equilibrium price and quantity and identify them in a market; Understand the relationship between production and costs. First let’s first focus on. Explain equilibrium, equilibrium price, and equilibrium quantity. Define surpluses and shortages and explain how they cause the price to move towards equilibrium Differentiate between total and marginal product. Understand that every factor of production has a corresponding. Short Run Equilibrium Price Microeconomics.

From www.coursehero.com

[Solved] Short run supply and longrun equilibrium Consider the competitive... Course Hero Short Run Equilibrium Price Microeconomics First let’s first focus on. Define equilibrium price and quantity and identify them in a market; Differentiate between production in the short run and in the long run. Differentiate between total and marginal product. Identify a demand curve and a supply curve. Explain equilibrium, equilibrium price, and equilibrium quantity. Understand the relationship between production and costs. The short run refers. Short Run Equilibrium Price Microeconomics.

From www.slideserve.com

PPT Competitive Markets PowerPoint Presentation, free download ID942310 Short Run Equilibrium Price Microeconomics Understand that every factor of production has a corresponding factor price. Differentiate between total and marginal product. Identify a demand curve and a supply curve. Define surpluses and shortages and explain how they cause the price to move towards equilibrium Understand the relationship between production and costs. First let’s first focus on. Define equilibrium price and quantity and identify them. Short Run Equilibrium Price Microeconomics.

From www.slideserve.com

PPT CHAPTER 12 Perfect Competition PowerPoint Presentation, free download ID6134615 Short Run Equilibrium Price Microeconomics Define surpluses and shortages and explain how they cause the price to move towards equilibrium Understand that every factor of production has a corresponding factor price. Differentiate between total and marginal product. Identify a demand curve and a supply curve. The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant. Short Run Equilibrium Price Microeconomics.

From www.chegg.com

Solved Shortrun equilibrium Consider a perfectly Short Run Equilibrium Price Microeconomics Define equilibrium price and quantity and identify them in a market; Define surpluses and shortages and explain how they cause the price to move towards equilibrium The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant (taken to be exogenous). Identify a demand curve and a supply curve. Understand the. Short Run Equilibrium Price Microeconomics.

From www.economicshelp.org

Monopoly diagram short run and long run Economics Help Short Run Equilibrium Price Microeconomics Understand the relationship between production and costs. Explain equilibrium, equilibrium price, and equilibrium quantity. Identify a demand curve and a supply curve. Understand that every factor of production has a corresponding factor price. Differentiate between total and marginal product. Define surpluses and shortages and explain how they cause the price to move towards equilibrium First let’s first focus on. Differentiate. Short Run Equilibrium Price Microeconomics.

From www.tutor2u.net

Market Equilibrium Transition to New Equilibrium tutor2u Short Run Equilibrium Price Microeconomics Identify a demand curve and a supply curve. Explain equilibrium, equilibrium price, and equilibrium quantity. Define equilibrium price and quantity and identify them in a market; Understand that every factor of production has a corresponding factor price. Differentiate between production in the short run and in the long run. Define surpluses and shortages and explain how they cause the price. Short Run Equilibrium Price Microeconomics.

From www.chegg.com

7. Shortrun supply and Iongrun equilibrium Consider Short Run Equilibrium Price Microeconomics The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant (taken to be exogenous). First let’s first focus on. Define surpluses and shortages and explain how they cause the price to move towards equilibrium Differentiate between total and marginal product. Identify a demand curve and a supply curve. Define equilibrium. Short Run Equilibrium Price Microeconomics.

From ecampusontario.pressbooks.pub

8.5 Economic Loss and Shut Down in the Short Run Principles of Microeconomics Short Run Equilibrium Price Microeconomics Identify a demand curve and a supply curve. Define surpluses and shortages and explain how they cause the price to move towards equilibrium Differentiate between production in the short run and in the long run. The short run refers to what happens while some variables (such as prices, wages, or capital stock) are held constant (taken to be exogenous). Differentiate. Short Run Equilibrium Price Microeconomics.