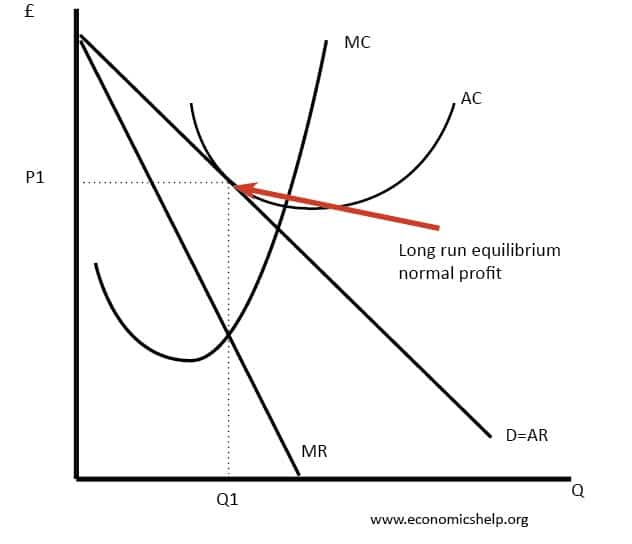

Total Cost Function Equilibrium . A typical firm, shown in panel (b), earns zero economic profit. Find the minimizer of the lac, which is the output of each firm in a long run competitive equilibrium. 3 srt c(q) = q − 3q 2 + 3q + 4. • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves: What is the equilibrium quantity and price in this market given this information? A reduction in oil prices reduces the marginal and average total costs of producing an oil. To find a long run competitive equilibrium in a constant cost industry we need to. Total cost function • the cost function shows the minimum cost incurred by the firm is c(r 1,r 2,q) = r 1 z 1 *(r 1,r 2,q) + r 2 z 2 *(r 1,r 2,q) • cost is a. To find the equilibrium set market demand equal to market.

from legendofsafety.com

A reduction in oil prices reduces the marginal and average total costs of producing an oil. Find the minimizer of the lac, which is the output of each firm in a long run competitive equilibrium. To find the equilibrium set market demand equal to market. 3 srt c(q) = q − 3q 2 + 3q + 4. Total cost function • the cost function shows the minimum cost incurred by the firm is c(r 1,r 2,q) = r 1 z 1 *(r 1,r 2,q) + r 2 z 2 *(r 1,r 2,q) • cost is a. • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves: What is the equilibrium quantity and price in this market given this information? To find a long run competitive equilibrium in a constant cost industry we need to. A typical firm, shown in panel (b), earns zero economic profit.

😊 Equilibrium in monopoly. Equilibrium in a Monopsony Market. 20190118

Total Cost Function Equilibrium To find a long run competitive equilibrium in a constant cost industry we need to. Total cost function • the cost function shows the minimum cost incurred by the firm is c(r 1,r 2,q) = r 1 z 1 *(r 1,r 2,q) + r 2 z 2 *(r 1,r 2,q) • cost is a. Find the minimizer of the lac, which is the output of each firm in a long run competitive equilibrium. A typical firm, shown in panel (b), earns zero economic profit. To find a long run competitive equilibrium in a constant cost industry we need to. What is the equilibrium quantity and price in this market given this information? To find the equilibrium set market demand equal to market. A reduction in oil prices reduces the marginal and average total costs of producing an oil. 3 srt c(q) = q − 3q 2 + 3q + 4. • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves:

From www.youtube.com

29 PRODUCER'S EQUILIBRIUM Total Revenue Total Cost Approach [when Total Cost Function Equilibrium To find a long run competitive equilibrium in a constant cost industry we need to. • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves: A typical firm, shown in panel (b), earns zero economic profit. 3 srt c(q) = q − 3q 2 + 3q + 4. Total. Total Cost Function Equilibrium.

From quizlet.com

The graph shows the total revenue function and total cost fu Quizlet Total Cost Function Equilibrium What is the equilibrium quantity and price in this market given this information? A typical firm, shown in panel (b), earns zero economic profit. To find a long run competitive equilibrium in a constant cost industry we need to. • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves:. Total Cost Function Equilibrium.

From courses.byui.edu

ECON 150 Microeconomics Total Cost Function Equilibrium • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves: 3 srt c(q) = q − 3q 2 + 3q + 4. What is the equilibrium quantity and price in this market given this information? Find the minimizer of the lac, which is the output of each firm in. Total Cost Function Equilibrium.

From www.youtube.com

Finding Longrun Equilibrium from Cost FunctionsII YouTube Total Cost Function Equilibrium To find a long run competitive equilibrium in a constant cost industry we need to. 3 srt c(q) = q − 3q 2 + 3q + 4. Total cost function • the cost function shows the minimum cost incurred by the firm is c(r 1,r 2,q) = r 1 z 1 *(r 1,r 2,q) + r 2 z 2 *(r. Total Cost Function Equilibrium.

From www.answersarena.com

[Solved] Figure 1 The figure below shows average total cos Total Cost Function Equilibrium Total cost function • the cost function shows the minimum cost incurred by the firm is c(r 1,r 2,q) = r 1 z 1 *(r 1,r 2,q) + r 2 z 2 *(r 1,r 2,q) • cost is a. A reduction in oil prices reduces the marginal and average total costs of producing an oil. To find the equilibrium set. Total Cost Function Equilibrium.

From saylordotorg.github.io

Perfect Competition and Supply and Demand Total Cost Function Equilibrium To find a long run competitive equilibrium in a constant cost industry we need to. A typical firm, shown in panel (b), earns zero economic profit. A reduction in oil prices reduces the marginal and average total costs of producing an oil. Find the minimizer of the lac, which is the output of each firm in a long run competitive. Total Cost Function Equilibrium.

From loemtufwn.blob.core.windows.net

How To Find Equilibrium Price And Quantity In Excel at Ricky Barrett blog Total Cost Function Equilibrium • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves: 3 srt c(q) = q − 3q 2 + 3q + 4. To find a long run competitive equilibrium in a constant cost industry we need to. Find the minimizer of the lac, which is the output of each. Total Cost Function Equilibrium.

From open.oregonstate.education

Module 8 Cost Curves Intermediate Microeconomics Total Cost Function Equilibrium 3 srt c(q) = q − 3q 2 + 3q + 4. A typical firm, shown in panel (b), earns zero economic profit. What is the equilibrium quantity and price in this market given this information? Find the minimizer of the lac, which is the output of each firm in a long run competitive equilibrium. To find the equilibrium set. Total Cost Function Equilibrium.

From www.chegg.com

Solved The figure shows graphs of the total cost function Total Cost Function Equilibrium Total cost function • the cost function shows the minimum cost incurred by the firm is c(r 1,r 2,q) = r 1 z 1 *(r 1,r 2,q) + r 2 z 2 *(r 1,r 2,q) • cost is a. A reduction in oil prices reduces the marginal and average total costs of producing an oil. To find the equilibrium set. Total Cost Function Equilibrium.

From analystprep.com

Longrun Equilibrium Under Each Market Structure AnalystPrep CFA Total Cost Function Equilibrium To find a long run competitive equilibrium in a constant cost industry we need to. • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves: What is the equilibrium quantity and price in this market given this information? To find the equilibrium set market demand equal to market. A. Total Cost Function Equilibrium.

From penpoin.com

Total Variable Cost Examples, Curve, Importance Total Cost Function Equilibrium To find a long run competitive equilibrium in a constant cost industry we need to. A reduction in oil prices reduces the marginal and average total costs of producing an oil. What is the equilibrium quantity and price in this market given this information? 3 srt c(q) = q − 3q 2 + 3q + 4. Total cost function •. Total Cost Function Equilibrium.

From momentumclubs.org

😂 Explain equilibrium price. Market Equilibrium in Economics Total Cost Function Equilibrium What is the equilibrium quantity and price in this market given this information? Find the minimizer of the lac, which is the output of each firm in a long run competitive equilibrium. A typical firm, shown in panel (b), earns zero economic profit. • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and. Total Cost Function Equilibrium.

From www.economicshelp.org

Diagrams of Cost Curves Economics Help Total Cost Function Equilibrium What is the equilibrium quantity and price in this market given this information? A reduction in oil prices reduces the marginal and average total costs of producing an oil. A typical firm, shown in panel (b), earns zero economic profit. 3 srt c(q) = q − 3q 2 + 3q + 4. To find a long run competitive equilibrium in. Total Cost Function Equilibrium.

From www.youtube.com

How to Calculate Equilibrium Price and Quantity (Demand and Supply Total Cost Function Equilibrium Find the minimizer of the lac, which is the output of each firm in a long run competitive equilibrium. To find a long run competitive equilibrium in a constant cost industry we need to. To find the equilibrium set market demand equal to market. A typical firm, shown in panel (b), earns zero economic profit. A reduction in oil prices. Total Cost Function Equilibrium.

From www.youtube.com

Finding a linear cost function 1 YouTube Total Cost Function Equilibrium Find the minimizer of the lac, which is the output of each firm in a long run competitive equilibrium. A typical firm, shown in panel (b), earns zero economic profit. Total cost function • the cost function shows the minimum cost incurred by the firm is c(r 1,r 2,q) = r 1 z 1 *(r 1,r 2,q) + r 2. Total Cost Function Equilibrium.

From www.youtube.com

Finding equilibrium price and quantity using linear demand and supply Total Cost Function Equilibrium • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves: What is the equilibrium quantity and price in this market given this information? 3 srt c(q) = q − 3q 2 + 3q + 4. Total cost function • the cost function shows the minimum cost incurred by the. Total Cost Function Equilibrium.

From www.youtube.com

find equilibrium price and quantity from a given demand and cost Total Cost Function Equilibrium Find the minimizer of the lac, which is the output of each firm in a long run competitive equilibrium. To find the equilibrium set market demand equal to market. • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves: A reduction in oil prices reduces the marginal and average. Total Cost Function Equilibrium.

From www.slideserve.com

PPT § 12 Functions PowerPoint Presentation, free download ID3758171 Total Cost Function Equilibrium Total cost function • the cost function shows the minimum cost incurred by the firm is c(r 1,r 2,q) = r 1 z 1 *(r 1,r 2,q) + r 2 z 2 *(r 1,r 2,q) • cost is a. 3 srt c(q) = q − 3q 2 + 3q + 4. Find the minimizer of the lac, which is the. Total Cost Function Equilibrium.

From www.youtube.com

Marginal Cost and Average Total Cost YouTube Total Cost Function Equilibrium Find the minimizer of the lac, which is the output of each firm in a long run competitive equilibrium. A reduction in oil prices reduces the marginal and average total costs of producing an oil. A typical firm, shown in panel (b), earns zero economic profit. Total cost function • the cost function shows the minimum cost incurred by the. Total Cost Function Equilibrium.

From www.slideserve.com

PPT Translog Cost Function PowerPoint Presentation, free download Total Cost Function Equilibrium A reduction in oil prices reduces the marginal and average total costs of producing an oil. A typical firm, shown in panel (b), earns zero economic profit. To find the equilibrium set market demand equal to market. • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves: Total cost. Total Cost Function Equilibrium.

From legendofsafety.com

😊 Equilibrium in monopoly. Equilibrium in a Monopsony Market. 20190118 Total Cost Function Equilibrium A reduction in oil prices reduces the marginal and average total costs of producing an oil. 3 srt c(q) = q − 3q 2 + 3q + 4. To find the equilibrium set market demand equal to market. • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves: Total. Total Cost Function Equilibrium.

From enotesworld.com

Consumer’s EquilibriumMicroeconomics for Business Total Cost Function Equilibrium 3 srt c(q) = q − 3q 2 + 3q + 4. Find the minimizer of the lac, which is the output of each firm in a long run competitive equilibrium. What is the equilibrium quantity and price in this market given this information? A reduction in oil prices reduces the marginal and average total costs of producing an oil.. Total Cost Function Equilibrium.

From www.chegg.com

Solved The graph illustrates an average total cost (ATC) Total Cost Function Equilibrium A typical firm, shown in panel (b), earns zero economic profit. A reduction in oil prices reduces the marginal and average total costs of producing an oil. To find a long run competitive equilibrium in a constant cost industry we need to. To find the equilibrium set market demand equal to market. • determine whether a production function exhibits constant,. Total Cost Function Equilibrium.

From www.coursehero.com

[Solved] The table above gives the shortrun total cost function for a Total Cost Function Equilibrium Total cost function • the cost function shows the minimum cost incurred by the firm is c(r 1,r 2,q) = r 1 z 1 *(r 1,r 2,q) + r 2 z 2 *(r 1,r 2,q) • cost is a. 3 srt c(q) = q − 3q 2 + 3q + 4. Find the minimizer of the lac, which is the. Total Cost Function Equilibrium.

From www.youtube.com

Given Demand and Cost Functions Find level of output and price that Total Cost Function Equilibrium 3 srt c(q) = q − 3q 2 + 3q + 4. • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves: What is the equilibrium quantity and price in this market given this information? Total cost function • the cost function shows the minimum cost incurred by the. Total Cost Function Equilibrium.

From saylordotorg.github.io

Demand, Supply, and Equilibrium Total Cost Function Equilibrium A reduction in oil prices reduces the marginal and average total costs of producing an oil. What is the equilibrium quantity and price in this market given this information? Find the minimizer of the lac, which is the output of each firm in a long run competitive equilibrium. • determine whether a production function exhibits constant, increasing, or decreasing returns. Total Cost Function Equilibrium.

From wizedu.com

Consider the following “Total Cost” function WizEdu Total Cost Function Equilibrium Total cost function • the cost function shows the minimum cost incurred by the firm is c(r 1,r 2,q) = r 1 z 1 *(r 1,r 2,q) + r 2 z 2 *(r 1,r 2,q) • cost is a. To find a long run competitive equilibrium in a constant cost industry we need to. 3 srt c(q) = q −. Total Cost Function Equilibrium.

From www.chegg.com

Solved A perfectly competitive industry operates in the long Total Cost Function Equilibrium To find the equilibrium set market demand equal to market. A reduction in oil prices reduces the marginal and average total costs of producing an oil. • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves: What is the equilibrium quantity and price in this market given this information?. Total Cost Function Equilibrium.

From www.numerade.com

A firm operates in a perfectly competitive market. The market price of Total Cost Function Equilibrium A typical firm, shown in panel (b), earns zero economic profit. Find the minimizer of the lac, which is the output of each firm in a long run competitive equilibrium. To find the equilibrium set market demand equal to market. To find a long run competitive equilibrium in a constant cost industry we need to. Total cost function • the. Total Cost Function Equilibrium.

From www.chegg.com

Solved Figure 139 The figure below depicts average total Total Cost Function Equilibrium • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves: To find the equilibrium set market demand equal to market. Find the minimizer of the lac, which is the output of each firm in a long run competitive equilibrium. Total cost function • the cost function shows the minimum. Total Cost Function Equilibrium.

From www.chegg.com

Solved 1. Suppose a firm's total cost function is given by Total Cost Function Equilibrium A reduction in oil prices reduces the marginal and average total costs of producing an oil. To find the equilibrium set market demand equal to market. • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves: Total cost function • the cost function shows the minimum cost incurred by. Total Cost Function Equilibrium.

From passnownow.com

SS1 Economics Third Term Equilibrium Price/Price Determination Total Cost Function Equilibrium To find a long run competitive equilibrium in a constant cost industry we need to. What is the equilibrium quantity and price in this market given this information? A typical firm, shown in panel (b), earns zero economic profit. To find the equilibrium set market demand equal to market. Total cost function • the cost function shows the minimum cost. Total Cost Function Equilibrium.

From studylib.net

Chapter 8 Costs Functions Total Cost Function Equilibrium To find the equilibrium set market demand equal to market. • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves: A reduction in oil prices reduces the marginal and average total costs of producing an oil. 3 srt c(q) = q − 3q 2 + 3q + 4. Total. Total Cost Function Equilibrium.

From saylordotorg.github.io

Market Supply and Market Demand Total Cost Function Equilibrium What is the equilibrium quantity and price in this market given this information? 3 srt c(q) = q − 3q 2 + 3q + 4. Find the minimizer of the lac, which is the output of each firm in a long run competitive equilibrium. A reduction in oil prices reduces the marginal and average total costs of producing an oil.. Total Cost Function Equilibrium.

From www.ecogradeshelp.com

Producer's Equilibrium Total Revenue and Total Cost Approach Total Cost Function Equilibrium 3 srt c(q) = q − 3q 2 + 3q + 4. • determine whether a production function exhibits constant, increasing, or decreasing returns to scale • calculate and graph various cost curves: A typical firm, shown in panel (b), earns zero economic profit. Total cost function • the cost function shows the minimum cost incurred by the firm is. Total Cost Function Equilibrium.