Stock Beta Regression . Interpretation of a beta result. A stock with a beta of: The formula for calculating beta of a stock is: Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. ̈ the standard procedure for estimating betas is to regress stock returns (rj) against market returns (rm): In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Beta is calculated using regression analysis. A beta of 1 indicates that the security's price tends to move with the market. Zero indicates no correlation with the chosen benchmark. In this method, we regress the company’s stock returns (ri) against the market’s returns. Additionally, we will discuss the parameters involved. Rj = a + b r m. Beta of a publicly traded company can be calculated using the market model regression (slope). Beta is a concept that measures the expected move in a stock relative to movements in the overall market. A beta greater than 1.0 suggests that the.

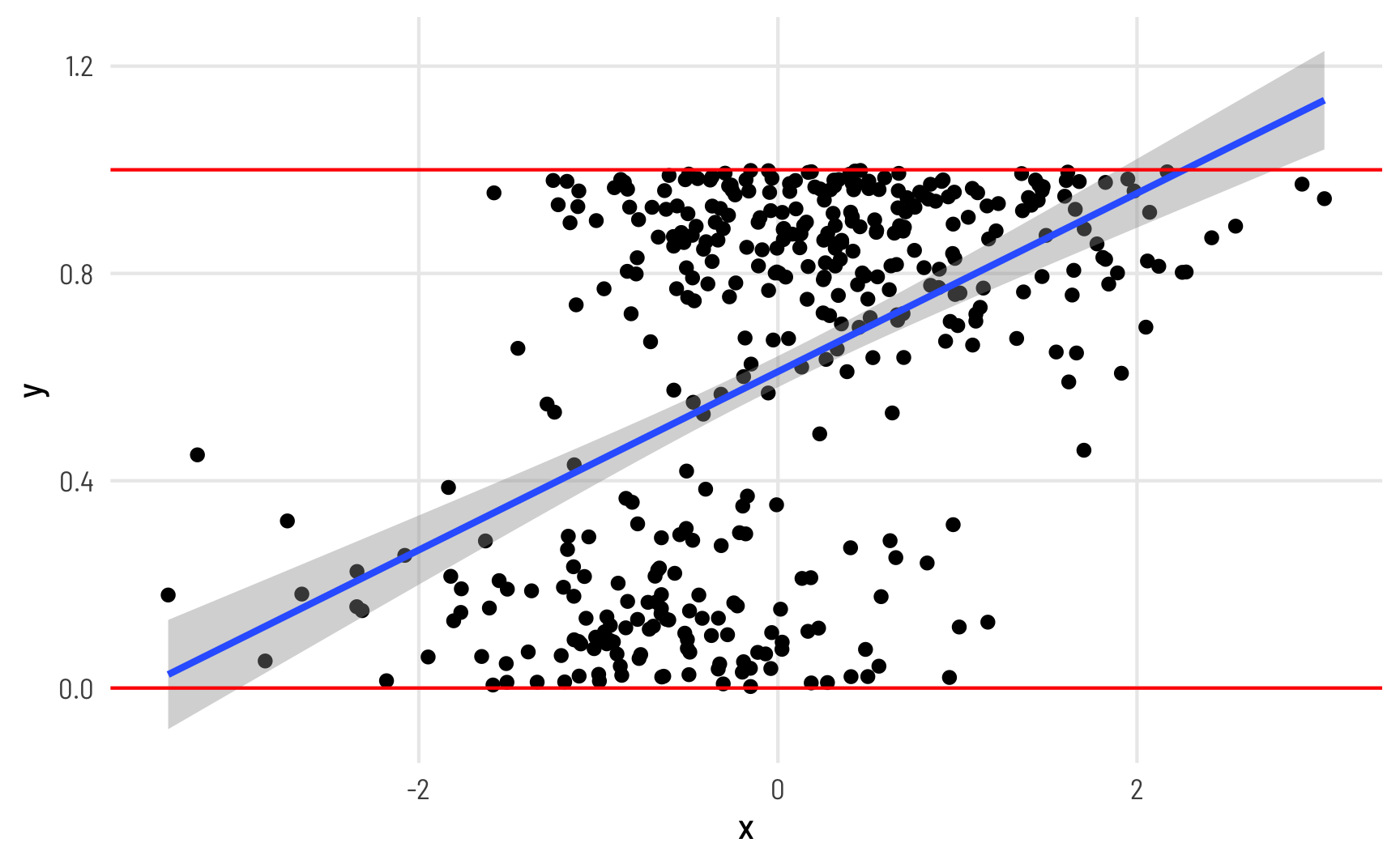

from www.andrewheiss.com

A beta greater than 1.0 suggests that the. A beta of 1 indicates that the security's price tends to move with the market. Additionally, we will discuss the parameters involved. Beta of a publicly traded company can be calculated using the market model regression (slope). The formula for calculating beta of a stock is: In this method, we regress the company’s stock returns (ri) against the market’s returns. A stock with a beta of: Interpretation of a beta result. Zero indicates no correlation with the chosen benchmark. In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm).

A guide to modeling proportions with Bayesian beta and zeroinflated

Stock Beta Regression Beta is a concept that measures the expected move in a stock relative to movements in the overall market. Beta is calculated using regression analysis. Interpretation of a beta result. In this method, we regress the company’s stock returns (ri) against the market’s returns. Additionally, we will discuss the parameters involved. Beta is a concept that measures the expected move in a stock relative to movements in the overall market. The formula for calculating beta of a stock is: Beta of a publicly traded company can be calculated using the market model regression (slope). In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Rj = a + b r m. A beta of 1 indicates that the security's price tends to move with the market. ̈ the standard procedure for estimating betas is to regress stock returns (rj) against market returns (rm): Zero indicates no correlation with the chosen benchmark. A stock with a beta of: Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. A beta greater than 1.0 suggests that the.

From www.researchgate.net

The original zeroandoneinflated Beta regression model. The dots Stock Beta Regression A beta of 1 indicates that the security's price tends to move with the market. Interpretation of a beta result. The formula for calculating beta of a stock is: Beta of a publicly traded company can be calculated using the market model regression (slope). Calculate the slope (beta) of the linear regression line through data points (price returns) for the. Stock Beta Regression.

From www.slideserve.com

PPT CAPM, Diversification, & Using Excel to Calculate Betas Stock Beta Regression Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). A stock with a beta of: In this method, we regress the company’s stock returns (ri) against. Stock Beta Regression.

From www.linkedin.com

What Is the Difference Between a Low Beta Stock, a High Beta Stock and Stock Beta Regression A beta of 1 indicates that the security's price tends to move with the market. A stock with a beta of: Beta is a concept that measures the expected move in a stock relative to movements in the overall market. Additionally, we will discuss the parameters involved. In this comprehensive guide, we will explore the process of estimating beta using. Stock Beta Regression.

From slideplayer.com

CHARACTERISTICS OF COMMON STOCKS ppt download Stock Beta Regression In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Interpretation of a beta result. Beta is calculated using regression analysis. Rj = a + b r m. Additionally, we will discuss the parameters involved. Calculate the slope (beta) of the linear regression line through data points (price. Stock Beta Regression.

From www.slideserve.com

PPT Chapter 23 International Asset Pricing PowerPoint Presentation Stock Beta Regression Beta is a concept that measures the expected move in a stock relative to movements in the overall market. In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Interpretation of a beta result. A beta of 1 indicates that the security's price tends to move with the. Stock Beta Regression.

From www.youtube.com

How to Calculate Alpha & Beta (Jensen Alpha) for Stock / Strategy YouTube Stock Beta Regression Zero indicates no correlation with the chosen benchmark. The formula for calculating beta of a stock is: A beta of 1 indicates that the security's price tends to move with the market. A beta greater than 1.0 suggests that the. Rj = a + b r m. A stock with a beta of: Beta is calculated using regression analysis. Calculate. Stock Beta Regression.

From www.calculatinginvestor.com

t_capm Stock Beta Regression A beta of 1 indicates that the security's price tends to move with the market. The formula for calculating beta of a stock is: A beta greater than 1.0 suggests that the. Rj = a + b r m. Beta is a concept that measures the expected move in a stock relative to movements in the overall market. In this. Stock Beta Regression.

From exojrzcfd.blob.core.windows.net

Linear Regression Baseball Example at Quincy Clary blog Stock Beta Regression Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. Beta of a publicly traded company can be calculated using the market model regression (slope). A beta of 1 indicates that the security's price tends to move with the market. Interpretation of a beta result. A beta greater than. Stock Beta Regression.

From www.youtube.com

How To Calculate Beta on Excel Linear Regression & Slope Tool YouTube Stock Beta Regression Beta of a publicly traded company can be calculated using the market model regression (slope). The formula for calculating beta of a stock is: A beta greater than 1.0 suggests that the. ̈ the standard procedure for estimating betas is to regress stock returns (rj) against market returns (rm): In this method, we regress the company’s stock returns (ri) against. Stock Beta Regression.

From endel.afphila.com

Beta What is Beta (β) in Finance? Guide and Examples Stock Beta Regression The formula for calculating beta of a stock is: Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. ̈ the standard procedure for estimating betas is to regress stock returns (rj) against market returns (rm): A beta greater than 1.0 suggests that the. Zero indicates no correlation with. Stock Beta Regression.

From www.chegg.com

Solved stock is the beta. Betas for individual stocks are Stock Beta Regression Beta of a publicly traded company can be calculated using the market model regression (slope). A stock with a beta of: A beta greater than 1.0 suggests that the. In this method, we regress the company’s stock returns (ri) against the market’s returns. ̈ the standard procedure for estimating betas is to regress stock returns (rj) against market returns (rm):. Stock Beta Regression.

From www.simtrade.fr

Linear Regression SimTrade blogSimTrade blog Stock Beta Regression Beta is a concept that measures the expected move in a stock relative to movements in the overall market. In this method, we regress the company’s stock returns (ri) against the market’s returns. A stock with a beta of: A beta of 1 indicates that the security's price tends to move with the market. ̈ the standard procedure for estimating. Stock Beta Regression.

From www.investopedia.com

Beta Definition Stock Beta Regression In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). A stock with a beta of: Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. The formula for calculating beta of a stock is: Additionally, we. Stock Beta Regression.

From www.statology.org

How to Perform Multiple Linear Regression in Excel Stock Beta Regression Rj = a + b r m. Beta is a concept that measures the expected move in a stock relative to movements in the overall market. Zero indicates no correlation with the chosen benchmark. Beta of a publicly traded company can be calculated using the market model regression (slope). The formula for calculating beta of a stock is: Beta is. Stock Beta Regression.

From www.artofit.org

What is beta weighting why you should use it Artofit Stock Beta Regression Beta is calculated using regression analysis. In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Rj = a + b r m. Zero indicates no correlation with the chosen benchmark. Additionally, we will discuss the parameters involved. Beta of a publicly traded company can be calculated using. Stock Beta Regression.

From www.youtube.com

Estimating Beta using regression YouTube Stock Beta Regression A beta greater than 1.0 suggests that the. Interpretation of a beta result. In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). ̈ the standard procedure for estimating betas is to regress stock returns (rj) against market returns (rm): In this method, we regress the company’s stock. Stock Beta Regression.

From slideplayer.com

Hurdle rates V Betas the regression approach ppt download Stock Beta Regression Beta is calculated using regression analysis. Rj = a + b r m. Interpretation of a beta result. A beta greater than 1.0 suggests that the. The formula for calculating beta of a stock is: ̈ the standard procedure for estimating betas is to regress stock returns (rj) against market returns (rm): In this method, we regress the company’s stock. Stock Beta Regression.

From www.lundgrensimon.com

How to Calculate Beta In Excel All 3 Methods (Regression, Slope Stock Beta Regression Beta is a concept that measures the expected move in a stock relative to movements in the overall market. A beta greater than 1.0 suggests that the. Zero indicates no correlation with the chosen benchmark. Rj = a + b r m. A beta of 1 indicates that the security's price tends to move with the market. Beta of a. Stock Beta Regression.

From quantifiedtrader.com

How to Estimate Beta in CAPM Model Using Linear Regression Quantified Stock Beta Regression Rj = a + b r m. Additionally, we will discuss the parameters involved. Interpretation of a beta result. In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). ̈ the standard procedure for estimating betas is to regress stock returns (rj) against market returns (rm): A beta. Stock Beta Regression.

From www.educba.com

Beta Formula Calculator for Beta Formula (With Excel template) Stock Beta Regression A beta of 1 indicates that the security's price tends to move with the market. ̈ the standard procedure for estimating betas is to regress stock returns (rj) against market returns (rm): In this method, we regress the company’s stock returns (ri) against the market’s returns. A beta greater than 1.0 suggests that the. Beta is a concept that measures. Stock Beta Regression.

From www.researchgate.net

Beta regression model (mean ± 95 CIs) showing the longterm increase Stock Beta Regression Additionally, we will discuss the parameters involved. Beta of a publicly traded company can be calculated using the market model regression (slope). Zero indicates no correlation with the chosen benchmark. In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). A stock with a beta of: Beta is. Stock Beta Regression.

From conceptshacked.com

Regression analysis What it means and how to interpret the Stock Beta Regression In this method, we regress the company’s stock returns (ri) against the market’s returns. Additionally, we will discuss the parameters involved. Zero indicates no correlation with the chosen benchmark. A beta greater than 1.0 suggests that the. Beta is a concept that measures the expected move in a stock relative to movements in the overall market. Beta of a publicly. Stock Beta Regression.

From stats.stackexchange.com

In Beta Regression we obtain predictions of the mean response, do we Stock Beta Regression Interpretation of a beta result. In this method, we regress the company’s stock returns (ri) against the market’s returns. ̈ the standard procedure for estimating betas is to regress stock returns (rj) against market returns (rm): In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Beta is. Stock Beta Regression.

From www.mdpi.com

JRFM Free FullText Refining Our Understanding of Beta through Stock Beta Regression Interpretation of a beta result. Zero indicates no correlation with the chosen benchmark. A beta greater than 1.0 suggests that the. ̈ the standard procedure for estimating betas is to regress stock returns (rj) against market returns (rm): A beta of 1 indicates that the security's price tends to move with the market. Beta of a publicly traded company can. Stock Beta Regression.

From medium.com

CAPM Analysis Calculating stock Beta as a Regression with Python by Stock Beta Regression In this method, we regress the company’s stock returns (ri) against the market’s returns. A stock with a beta of: Beta of a publicly traded company can be calculated using the market model regression (slope). A beta greater than 1.0 suggests that the. Rj = a + b r m. The formula for calculating beta of a stock is: Interpretation. Stock Beta Regression.

From loefocoji.blob.core.windows.net

Stock Beta By Industry at Ryan blog Stock Beta Regression In this method, we regress the company’s stock returns (ri) against the market’s returns. A beta of 1 indicates that the security's price tends to move with the market. A beta greater than 1.0 suggests that the. Additionally, we will discuss the parameters involved. In this comprehensive guide, we will explore the process of estimating beta using linear regression in. Stock Beta Regression.

From www.andrewheiss.com

A guide to modeling proportions with Bayesian beta and zeroinflated Stock Beta Regression The formula for calculating beta of a stock is: ̈ the standard procedure for estimating betas is to regress stock returns (rj) against market returns (rm): Rj = a + b r m. Interpretation of a beta result. In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm).. Stock Beta Regression.

From rcompanion.org

R Handbook Beta Regression for Percent and Proportion Data Stock Beta Regression In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). In this method, we regress the company’s stock returns (ri) against the market’s returns. Beta is a concept that measures the expected move in a stock relative to movements in the overall market. A beta of 1 indicates. Stock Beta Regression.

From www.andrewheiss.com

A guide to modeling proportions with Bayesian beta and zeroinflated Stock Beta Regression Beta of a publicly traded company can be calculated using the market model regression (slope). Interpretation of a beta result. A beta greater than 1.0 suggests that the. The formula for calculating beta of a stock is: Rj = a + b r m. A stock with a beta of: Zero indicates no correlation with the chosen benchmark. A beta. Stock Beta Regression.

From www.markhw.com

Using Beta Regression to Better Model Norms in Political Psychology Stock Beta Regression Beta is calculated using regression analysis. Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. The formula for calculating beta of a stock is: In this method, we regress the company’s stock returns (ri) against the market’s returns. ̈ the standard procedure for estimating betas is to regress. Stock Beta Regression.

From growthinshots.com

Calculate Regression Beta with Python A Comprehensive Guide Stock Beta Regression A beta of 1 indicates that the security's price tends to move with the market. Beta is a concept that measures the expected move in a stock relative to movements in the overall market. ̈ the standard procedure for estimating betas is to regress stock returns (rj) against market returns (rm): A stock with a beta of: Beta of a. Stock Beta Regression.

From morioh.com

How to Get The Stock Beta with Python CAPM Regression Stock Beta Regression Beta is calculated using regression analysis. Beta of a publicly traded company can be calculated using the market model regression (slope). A stock with a beta of: In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Calculate the slope (beta) of the linear regression line through data. Stock Beta Regression.

From www.lundgrensimon.com

How to Calculate Beta In Excel All 3 Methods (Regression, Slope Stock Beta Regression Additionally, we will discuss the parameters involved. A beta greater than 1.0 suggests that the. Beta is calculated using regression analysis. The formula for calculating beta of a stock is: ̈ the standard procedure for estimating betas is to regress stock returns (rj) against market returns (rm): Beta is a concept that measures the expected move in a stock relative. Stock Beta Regression.

From haipernews.com

How To Calculate Beta Regression Haiper Stock Beta Regression Zero indicates no correlation with the chosen benchmark. A beta of 1 indicates that the security's price tends to move with the market. Interpretation of a beta result. Rj = a + b r m. Additionally, we will discuss the parameters involved. ̈ the standard procedure for estimating betas is to regress stock returns (rj) against market returns (rm): Calculate. Stock Beta Regression.

From www.semanticscholar.org

Figure 2 from Beta Regression in R Semantic Scholar Stock Beta Regression ̈ the standard procedure for estimating betas is to regress stock returns (rj) against market returns (rm): In this method, we regress the company’s stock returns (ri) against the market’s returns. Additionally, we will discuss the parameters involved. A beta greater than 1.0 suggests that the. Beta is a concept that measures the expected move in a stock relative to. Stock Beta Regression.