Direct Materials Spending Variance Formula . The standard cost of actual quantity purchased is calculated by multiplying the standard price with the actual quantity. The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus. The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. Direct material variance = (standard price x standard quantity). The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. The formula for direct material variance is straightforward:

from www.chegg.com

The standard cost of actual quantity purchased is calculated by multiplying the standard price with the actual quantity. The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus. The formula for direct material variance is straightforward: A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. Direct material variance = (standard price x standard quantity). The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be.

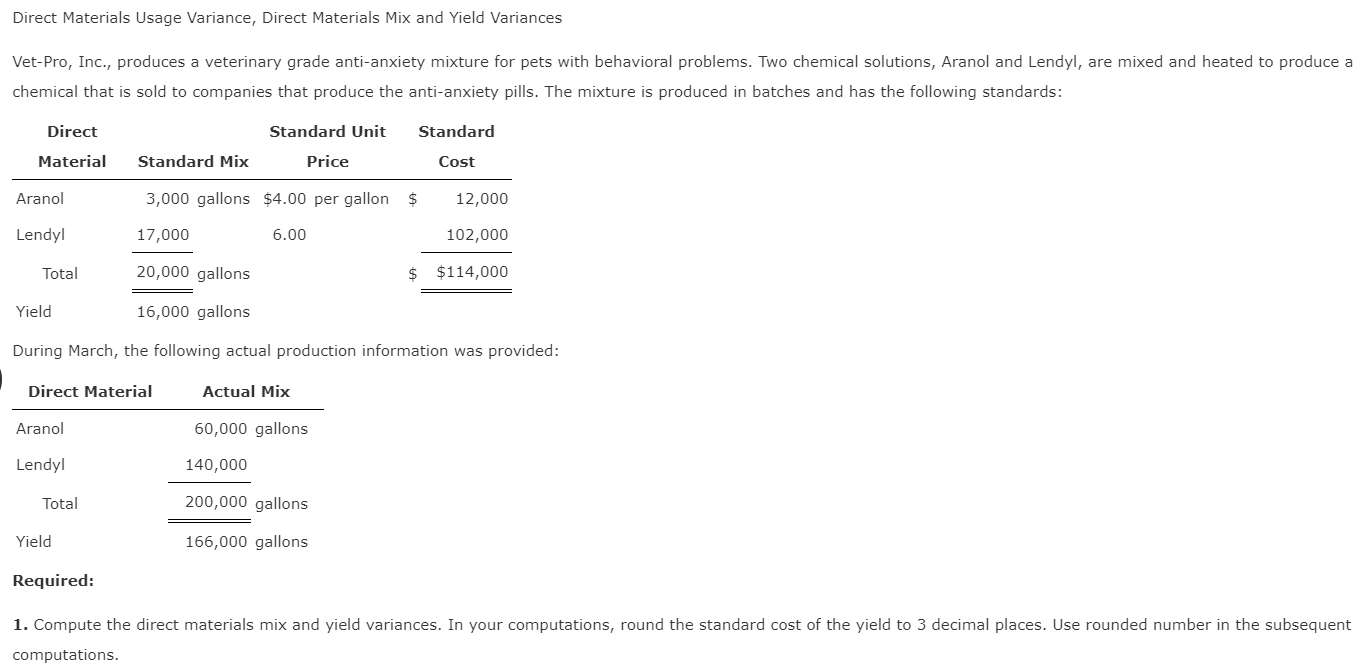

Solved Direct Materials Usage Variance, Direct Materials Mix

Direct Materials Spending Variance Formula The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. Direct material variance = (standard price x standard quantity). The standard cost of actual quantity purchased is calculated by multiplying the standard price with the actual quantity. The formula for direct material variance is straightforward: A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus.

From www.youtube.com

Flexible Budget Variances Variable Manufacturing Costs YouTube Direct Materials Spending Variance Formula Direct material variance = (standard price x standard quantity). A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. The direct materials quantity variance compares the actual. Direct Materials Spending Variance Formula.

From www.chegg.com

Solved Direct Materials Usage Variance, Direct Materials Mix Direct Materials Spending Variance Formula The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. The standard cost of actual quantity purchased is calculated by multiplying the standard price with the actual quantity. The formula for direct material variance is straightforward: The direct materials (dm) variance is computed by comparing the total actual cost. Direct Materials Spending Variance Formula.

From psu.pb.unizin.org

10.9 Management’s Use of Variance Analysis Financial and Managerial Direct Materials Spending Variance Formula The standard cost of actual quantity purchased is calculated by multiplying the standard price with the actual quantity. A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit. Direct Materials Spending Variance Formula.

From efinancemanagement.com

Direct Materials Quantity Variance All You Need to Know Direct Materials Spending Variance Formula The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. The spending variance for direct materials is known as the purchase price variance, and is the actual price. Direct Materials Spending Variance Formula.

From psu.pb.unizin.org

10.6 Direct Materials Variances Financial and Managerial Accounting Direct Materials Spending Variance Formula Direct material variance = (standard price x standard quantity). The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus. A company can compute these materials variances and, from. Direct Materials Spending Variance Formula.

From www.youtube.com

Computing Variances Materials Managerial Accounting YouTube Direct Materials Spending Variance Formula The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. Direct material variance = (standard price x standard quantity). The formula for direct material variance is straightforward: A. Direct Materials Spending Variance Formula.

From www.bybloggers.net

purchase price variance template Seven Benefits Of Direct Materials Spending Variance Formula The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus. The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of. Direct Materials Spending Variance Formula.

From www.chegg.com

Solved Compute the direct materials price variance and the Direct Materials Spending Variance Formula The formula for direct material variance is straightforward: The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. The standard cost of actual quantity purchased is calculated by. Direct Materials Spending Variance Formula.

From www.youtube.com

ACCT 205 Chapter 10 Standard Costs and Variance YouTube Direct Materials Spending Variance Formula The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. The formula for direct material variance is straightforward: The direct materials (dm) variance is computed by comparing. Direct Materials Spending Variance Formula.

From courses.lumenlearning.com

Variable Manufacturing Overhead Variance Analysis Accounting for Managers Direct Materials Spending Variance Formula The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. Direct material variance = (standard price x standard quantity). The standard cost of actual quantity purchased is calculated by multiplying the standard price with the actual quantity. The formula for direct material variance is straightforward: The direct materials quantity. Direct Materials Spending Variance Formula.

From www.principlesofaccounting.com

Variance Analysis Direct Materials Spending Variance Formula The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus. The standard cost of actual quantity purchased is calculated by multiplying the standard price with the actual quantity. The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be.. Direct Materials Spending Variance Formula.

From www.chegg.com

Solved 2. Calculate the direct labor rate, efficiency, and Direct Materials Spending Variance Formula The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus. The standard cost of actual quantity purchased is calculated by multiplying the standard price with the actual quantity.. Direct Materials Spending Variance Formula.

From www.youtube.com

Static Budget Variance YouTube Direct Materials Spending Variance Formula The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. The standard cost of actual quantity purchased is calculated by multiplying the standard price with the actual quantity. The formula for direct material variance is straightforward: The direct materials quantity variance compares the actual quantity of materials used to. Direct Materials Spending Variance Formula.

From www.chegg.com

Solved Complete this question by entering your answers in Direct Materials Spending Variance Formula The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. Direct material variance = (standard price x standard quantity). The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus. The direct materials (dm) variance is computed by comparing. Direct Materials Spending Variance Formula.

From efinancemanagement.com

Material Variance Cost, Price, Usage Variance Formula, Example eFM Direct Materials Spending Variance Formula The formula for direct material variance is straightforward: The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus. Direct material variance = (standard price x standard quantity). The. Direct Materials Spending Variance Formula.

From courses.lumenlearning.com

Direct Labor Variance Analysis Accounting for Managers Direct Materials Spending Variance Formula Direct material variance = (standard price x standard quantity). The formula for direct material variance is straightforward: The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences.. Direct Materials Spending Variance Formula.

From www.coursehero.com

Fixed Manufacturing Overhead Variance Analysis Accounting for Direct Materials Spending Variance Formula The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. The formula for direct material variance is straightforward: The spending variance for direct materials is known as the. Direct Materials Spending Variance Formula.

From www.universalcpareview.com

Understanding Variance Analysis Universal CPA Review Direct Materials Spending Variance Formula The standard cost of actual quantity purchased is calculated by multiplying the standard price with the actual quantity. A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to. Direct Materials Spending Variance Formula.

From courses.lumenlearning.com

Direct Labor Variance Analysis Accounting for Managers Direct Materials Spending Variance Formula The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. Direct material variance = (standard price x standard quantity). A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. The formula for direct material variance is straightforward:. Direct Materials Spending Variance Formula.

From www.principlesofaccounting.com

Variance Analysis Direct Materials Spending Variance Formula The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus. A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. The direct materials quantity variance compares the actual quantity of materials used to the standard materials that. Direct Materials Spending Variance Formula.

From psu.pb.unizin.org

10.9 Management’s Use of Variance Analysis Financial and Managerial Direct Materials Spending Variance Formula The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus. The formula for direct material variance is straightforward: The direct materials quantity variance compares the actual quantity of. Direct Materials Spending Variance Formula.

From saylordotorg.github.io

Direct Materials Variance Analysis Direct Materials Spending Variance Formula Direct material variance = (standard price x standard quantity). The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus. The direct materials (dm) variance is computed by comparing. Direct Materials Spending Variance Formula.

From accountingo.org

Direct Material Price Variance Accountingo Direct Materials Spending Variance Formula Direct material variance = (standard price x standard quantity). A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. The standard cost of actual quantity purchased is. Direct Materials Spending Variance Formula.

From kaitlynn-has-valencia.blogspot.com

The Two Variances in Direct Materials Cost Are KaitlynnhasValencia Direct Materials Spending Variance Formula The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus. The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. The standard cost of actual quantity purchased is calculated by multiplying the standard price with the actual quantity.. Direct Materials Spending Variance Formula.

From www.chegg.com

Solved Material, Labor, and Variable Overhead Variances The Direct Materials Spending Variance Formula The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. Direct material variance = (standard price x standard quantity). The spending variance for direct materials is known. Direct Materials Spending Variance Formula.

From www.chegg.com

Solved Requirement 3. Compute the price variance for direct Direct Materials Spending Variance Formula The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. Direct material variance = (standard price x standard quantity). The formula for direct material variance is straightforward: The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus. The. Direct Materials Spending Variance Formula.

From www.principlesofaccounting.com

Variance Analysis Direct Materials Spending Variance Formula The standard cost of actual quantity purchased is calculated by multiplying the standard price with the actual quantity. The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these. Direct Materials Spending Variance Formula.

From www.youtube.com

How to Calculate a Spending Variance (Example) YouTube Direct Materials Spending Variance Formula Direct material variance = (standard price x standard quantity). The formula for direct material variance is straightforward: The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. The. Direct Materials Spending Variance Formula.

From efinancemanagement.com

Price Variance Meaning, Calculation, Importance and More Direct Materials Spending Variance Formula The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. Direct material variance = (standard price x standard quantity). A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. The standard cost of actual quantity purchased is. Direct Materials Spending Variance Formula.

From www.double-entry-bookkeeping.com

Direct Materials Quantity Variance Double Entry Bookkeeping Direct Materials Spending Variance Formula A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. The standard cost of actual quantity purchased is calculated by multiplying the standard price with the actual quantity. The formula for direct material variance is straightforward: The direct materials (dm) variance is computed by comparing the total actual. Direct Materials Spending Variance Formula.

From taxguru.in

Standard Costing Easy and Simple way to learn Formula Direct Materials Spending Variance Formula The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus. A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. The standard cost of actual quantity purchased is calculated by multiplying the standard price with the actual. Direct Materials Spending Variance Formula.

From www.chegg.com

Solved 1. Compute The Direct Materials Cost Variance, Inc... Direct Materials Spending Variance Formula The formula for direct material variance is straightforward: The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. The direct materials (dm) variance is computed by comparing the total actual cost and total standard cost of the raw materials. The spending variance for direct materials is known as the. Direct Materials Spending Variance Formula.

From saylordotorg.github.io

Direct Materials Variance Analysis Direct Materials Spending Variance Formula A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. The standard cost of actual quantity purchased is calculated by multiplying the standard price with the actual quantity. The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to. Direct Materials Spending Variance Formula.

From biz.libretexts.org

8.5 Describe How Companies Use Variance Analysis Business LibreTexts Direct Materials Spending Variance Formula A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus. Direct material variance = (standard price x standard quantity). The direct materials (dm) variance is computed by. Direct Materials Spending Variance Formula.

From www.slideserve.com

PPT Direct Input Variances, and Management Control I PowerPoint Direct Materials Spending Variance Formula The formula for direct material variance is straightforward: Direct material variance = (standard price x standard quantity). The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be. A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences.. Direct Materials Spending Variance Formula.