What Is Convertible Bond Delta . At its most basic essence, a. delta of a convertible. ȷ this section provides an overview of the key terms used for valuing convertible bonds such as bond floor, parity, and convexity. Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its underlying stock; The fund exploits changes in volatility, credit quality, and interest rates to make money while minimizing overall market risk. Once the delta has been. The sensitivity of a convertible ’s price to changes in parity value. to find the delta of a convertible you can apply the basic definition foe the derivative number : delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock. convertible bonds are debt securities issued by corporations that include an option for the holder to convert.

from tavaga.com

The fund exploits changes in volatility, credit quality, and interest rates to make money while minimizing overall market risk. At its most basic essence, a. Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its underlying stock; The sensitivity of a convertible ’s price to changes in parity value. delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock. Once the delta has been. ȷ this section provides an overview of the key terms used for valuing convertible bonds such as bond floor, parity, and convexity. delta of a convertible. convertible bonds are debt securities issued by corporations that include an option for the holder to convert. to find the delta of a convertible you can apply the basic definition foe the derivative number :

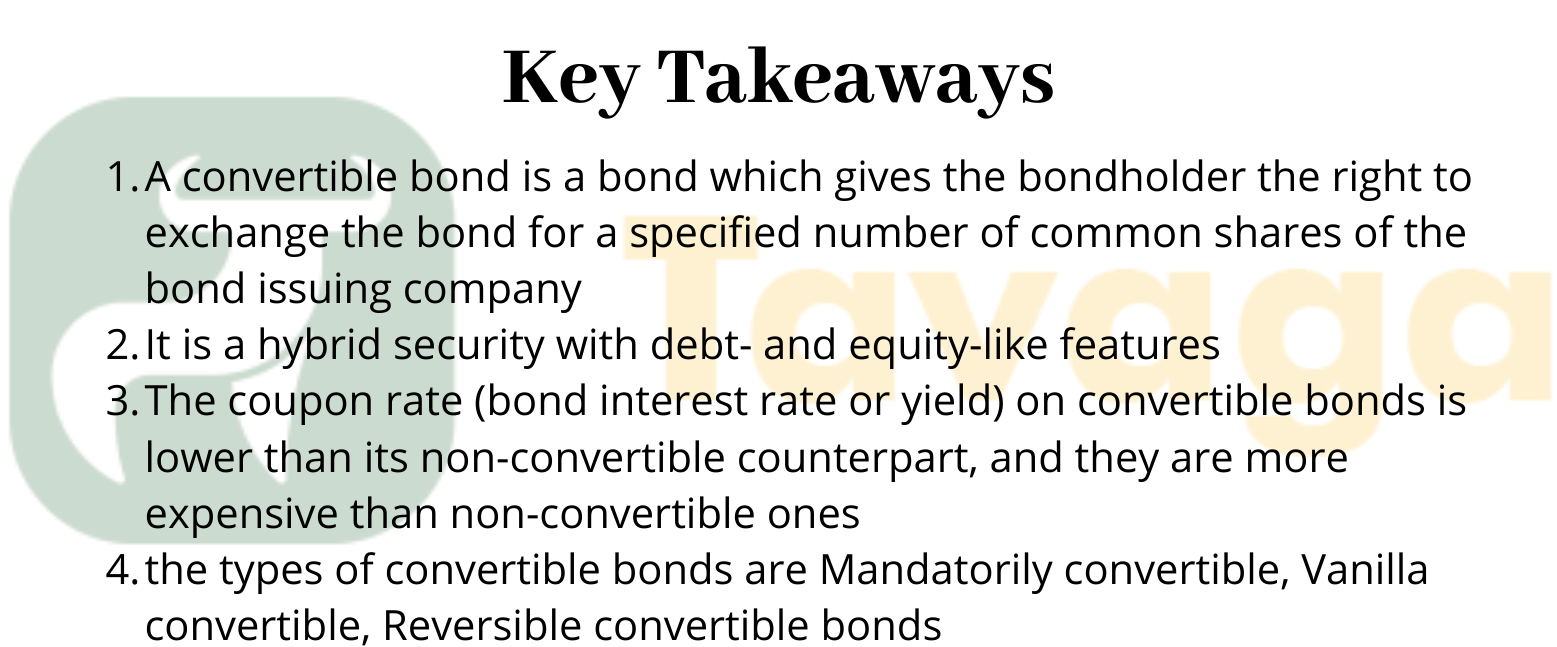

Convertible Bond And Its Types Tavaga Tavagapedia

What Is Convertible Bond Delta Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its underlying stock; delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock. convertible bonds are debt securities issued by corporations that include an option for the holder to convert. delta of a convertible. The sensitivity of a convertible ’s price to changes in parity value. Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its underlying stock; to find the delta of a convertible you can apply the basic definition foe the derivative number : ȷ this section provides an overview of the key terms used for valuing convertible bonds such as bond floor, parity, and convexity. The fund exploits changes in volatility, credit quality, and interest rates to make money while minimizing overall market risk. At its most basic essence, a. Once the delta has been.

From learn.g2.com

Cruising for Capital Your Guide to Convertible Bond Basics What Is Convertible Bond Delta delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock. convertible bonds are debt securities issued by corporations that include an option for the holder to convert. Once the delta has been. The sensitivity of a convertible ’s price to changes in parity value. to. What Is Convertible Bond Delta.

From tavaga.com

Convertible Bond And Its Types Tavaga Tavagapedia What Is Convertible Bond Delta The fund exploits changes in volatility, credit quality, and interest rates to make money while minimizing overall market risk. Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its underlying stock; to find the delta of a convertible you can apply the basic definition. What Is Convertible Bond Delta.

From www.financestrategists.com

Features of Convertible Bonds Finance Strategists What Is Convertible Bond Delta delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock. Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its underlying stock; ȷ this section provides an overview of the key. What Is Convertible Bond Delta.

From www.financestrategists.com

Convertible Bonds Definition, Types, Features, Pros, & Cons What Is Convertible Bond Delta Once the delta has been. At its most basic essence, a. delta of a convertible. delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock. Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s. What Is Convertible Bond Delta.

From www.angelone.in

Convertible Bond Arbitrage Details Explained Angel One What Is Convertible Bond Delta The sensitivity of a convertible ’s price to changes in parity value. to find the delta of a convertible you can apply the basic definition foe the derivative number : At its most basic essence, a. delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock.. What Is Convertible Bond Delta.

From www.indiabonds.com

Understanding Convertible Bonds Benefits and Varieties IndiaBonds. What Is Convertible Bond Delta to find the delta of a convertible you can apply the basic definition foe the derivative number : delta of a convertible. delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock. The sensitivity of a convertible ’s price to changes in parity value. At. What Is Convertible Bond Delta.

From efinancemanagement.com

Convertible Bonds Features, Types, Advantages & Disadvantages What Is Convertible Bond Delta The fund exploits changes in volatility, credit quality, and interest rates to make money while minimizing overall market risk. to find the delta of a convertible you can apply the basic definition foe the derivative number : delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying. What Is Convertible Bond Delta.

From finance.gov.capital

What is the delta of a convertible bond? Finance.Gov.Capital What Is Convertible Bond Delta The fund exploits changes in volatility, credit quality, and interest rates to make money while minimizing overall market risk. ȷ this section provides an overview of the key terms used for valuing convertible bonds such as bond floor, parity, and convexity. At its most basic essence, a. delta of a convertible. delta is defined as the sensitivity. What Is Convertible Bond Delta.

From www.go-yubi.com

Investing In Convertible Bonds? Learn About The Pros & Cons What Is Convertible Bond Delta convertible bonds are debt securities issued by corporations that include an option for the holder to convert. The sensitivity of a convertible ’s price to changes in parity value. At its most basic essence, a. The fund exploits changes in volatility, credit quality, and interest rates to make money while minimizing overall market risk. ȷ this section provides. What Is Convertible Bond Delta.

From www.financestrategists.com

Features of Convertible Bonds Finance Strategists What Is Convertible Bond Delta At its most basic essence, a. convertible bonds are debt securities issued by corporations that include an option for the holder to convert. The sensitivity of a convertible ’s price to changes in parity value. to find the delta of a convertible you can apply the basic definition foe the derivative number : Once the delta has been.. What Is Convertible Bond Delta.

From www.superfastcpa.com

What is a Convertible Bond? What Is Convertible Bond Delta Once the delta has been. delta of a convertible. Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its underlying stock; ȷ this section provides an overview of the key terms used for valuing convertible bonds such as bond floor, parity, and convexity.. What Is Convertible Bond Delta.

From www.slideserve.com

PPT Chapter 7 The Valuation and Characteristics of Bonds PowerPoint What Is Convertible Bond Delta delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock. Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its underlying stock; The fund exploits changes in volatility, credit quality, and interest. What Is Convertible Bond Delta.

From www.scribd.com

Convertible Bond Asset Swaps Convertible Bond Bonds (Finance) What Is Convertible Bond Delta ȷ this section provides an overview of the key terms used for valuing convertible bonds such as bond floor, parity, and convexity. The sensitivity of a convertible ’s price to changes in parity value. At its most basic essence, a. convertible bonds are debt securities issued by corporations that include an option for the holder to convert. . What Is Convertible Bond Delta.

From moneyfortherestofus.com

Convertible Bonds Everything You Need to Know Money For The Rest of Us What Is Convertible Bond Delta Once the delta has been. delta of a convertible. The fund exploits changes in volatility, credit quality, and interest rates to make money while minimizing overall market risk. ȷ this section provides an overview of the key terms used for valuing convertible bonds such as bond floor, parity, and convexity. Convertible arbitrage is a relative value strategy in. What Is Convertible Bond Delta.

From www.wintwealth.com

Convertible Bonds Meaning, Types, Benefits & Examples Wint Wealth What Is Convertible Bond Delta Once the delta has been. to find the delta of a convertible you can apply the basic definition foe the derivative number : Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its underlying stock; The sensitivity of a convertible ’s price to changes. What Is Convertible Bond Delta.

From www.researchgate.net

Convertible bond examples Download Table What Is Convertible Bond Delta At its most basic essence, a. convertible bonds are debt securities issued by corporations that include an option for the holder to convert. delta of a convertible. Once the delta has been. to find the delta of a convertible you can apply the basic definition foe the derivative number : Convertible arbitrage is a relative value strategy. What Is Convertible Bond Delta.

From am.credit-suisse.com

Why convertible bonds are useful during market volatility Credit What Is Convertible Bond Delta The sensitivity of a convertible ’s price to changes in parity value. At its most basic essence, a. Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its underlying stock; delta of a convertible. convertible bonds are debt securities issued by corporations that. What Is Convertible Bond Delta.

From www.ssga.com

Convertible Bonds Check Your Deltas vs. the Delta Variant What Is Convertible Bond Delta Once the delta has been. ȷ this section provides an overview of the key terms used for valuing convertible bonds such as bond floor, parity, and convexity. delta of a convertible. The fund exploits changes in volatility, credit quality, and interest rates to make money while minimizing overall market risk. Convertible arbitrage is a relative value strategy in. What Is Convertible Bond Delta.

From www.ssga.com

Convertible Bonds Check Your Deltas vs. the Delta Variant What Is Convertible Bond Delta Once the delta has been. The sensitivity of a convertible ’s price to changes in parity value. convertible bonds are debt securities issued by corporations that include an option for the holder to convert. Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its. What Is Convertible Bond Delta.

From corporatefinanceinstitute.com

Convertible Bond Types & Advantages of Convertible Bonds What Is Convertible Bond Delta to find the delta of a convertible you can apply the basic definition foe the derivative number : Once the delta has been. Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its underlying stock; The sensitivity of a convertible ’s price to changes. What Is Convertible Bond Delta.

From chem.libretexts.org

3.7A Orbital Overlap Chemistry LibreTexts What Is Convertible Bond Delta ȷ this section provides an overview of the key terms used for valuing convertible bonds such as bond floor, parity, and convexity. The fund exploits changes in volatility, credit quality, and interest rates to make money while minimizing overall market risk. convertible bonds are debt securities issued by corporations that include an option for the holder to convert.. What Is Convertible Bond Delta.

From www.ssga.com

Keep a Foot in Each Camp with Convertible Bonds What Is Convertible Bond Delta The sensitivity of a convertible ’s price to changes in parity value. to find the delta of a convertible you can apply the basic definition foe the derivative number : delta of a convertible. At its most basic essence, a. Once the delta has been. ȷ this section provides an overview of the key terms used for. What Is Convertible Bond Delta.

From mergersandinquisitions.com

Convertible Arbitrage Hedge Funds Full Guide What Is Convertible Bond Delta delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock. ȷ this section provides an overview of the key terms used for valuing convertible bonds such as bond floor, parity, and convexity. to find the delta of a convertible you can apply the basic definition. What Is Convertible Bond Delta.

From www.investopedia.com

Convertible Bond Definition, Example, and Benefits What Is Convertible Bond Delta At its most basic essence, a. The fund exploits changes in volatility, credit quality, and interest rates to make money while minimizing overall market risk. delta of a convertible. The sensitivity of a convertible ’s price to changes in parity value. Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy. What Is Convertible Bond Delta.

From www.youtube.com

Delta bond in metal cluster CSIR NET GATE CHEMISTRY Organometallics What Is Convertible Bond Delta delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock. The fund exploits changes in volatility, credit quality, and interest rates to make money while minimizing overall market risk. convertible bonds are debt securities issued by corporations that include an option for the holder to convert.. What Is Convertible Bond Delta.

From www.financestrategists.com

Convertible Bonds Definition, Types, Features, Pros, & Cons What Is Convertible Bond Delta Once the delta has been. ȷ this section provides an overview of the key terms used for valuing convertible bonds such as bond floor, parity, and convexity. The sensitivity of a convertible ’s price to changes in parity value. At its most basic essence, a. delta of a convertible. Convertible arbitrage is a relative value strategy in which. What Is Convertible Bond Delta.

From www.bajajfinservsecurities.in

Convertible Bond Meaning, Types, Pros, and Cons What Is Convertible Bond Delta ȷ this section provides an overview of the key terms used for valuing convertible bonds such as bond floor, parity, and convexity. convertible bonds are debt securities issued by corporations that include an option for the holder to convert. Once the delta has been. to find the delta of a convertible you can apply the basic definition. What Is Convertible Bond Delta.

From mitchellewahardy.blogspot.com

Convertible Bonds Advantages and Disadvantages MitchellewaHardy What Is Convertible Bond Delta Once the delta has been. delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock. The sensitivity of a convertible ’s price to changes in parity value. to find the delta of a convertible you can apply the basic definition foe the derivative number : At. What Is Convertible Bond Delta.

From www.researchgate.net

Delta versus spot price graph for a 7year convertible bond. Note This What Is Convertible Bond Delta delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock. Once the delta has been. delta of a convertible. Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its underlying stock;. What Is Convertible Bond Delta.

From www.investopedia.com

An Introduction to Convertible Bonds What Is Convertible Bond Delta convertible bonds are debt securities issued by corporations that include an option for the holder to convert. The sensitivity of a convertible ’s price to changes in parity value. Once the delta has been. At its most basic essence, a. to find the delta of a convertible you can apply the basic definition foe the derivative number :. What Is Convertible Bond Delta.

From moneyfortherestofus.com

Convertible Bonds Everything You Need to Know Money For The Rest of Us What Is Convertible Bond Delta delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock. convertible bonds are debt securities issued by corporations that include an option for the holder to convert. to find the delta of a convertible you can apply the basic definition foe the derivative number :. What Is Convertible Bond Delta.

From www.slideshare.net

CONVERTIBLE BOND What Is Convertible Bond Delta The sensitivity of a convertible ’s price to changes in parity value. ȷ this section provides an overview of the key terms used for valuing convertible bonds such as bond floor, parity, and convexity. delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock. Once the. What Is Convertible Bond Delta.

From financeplusinsurance.com

Convertible Bonds Meaning, Examples, Types, Benefits, Pros What Is Convertible Bond Delta The fund exploits changes in volatility, credit quality, and interest rates to make money while minimizing overall market risk. The sensitivity of a convertible ’s price to changes in parity value. delta of a convertible. delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock. . What Is Convertible Bond Delta.

From www.financestrategists.com

Features of Convertible Bonds Finance Strategists What Is Convertible Bond Delta delta is defined as the sensitivity of the price of a convertible bond to changes in the price of the underlying stock. delta of a convertible. to find the delta of a convertible you can apply the basic definition foe the derivative number : At its most basic essence, a. Once the delta has been. The sensitivity. What Is Convertible Bond Delta.

From www.financestrategists.com

Convertible Bonds Definition, Types, Features, Pros, & Cons What Is Convertible Bond Delta Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its underlying stock; to find the delta of a convertible you can apply the basic definition foe the derivative number : convertible bonds are debt securities issued by corporations that include an option for. What Is Convertible Bond Delta.