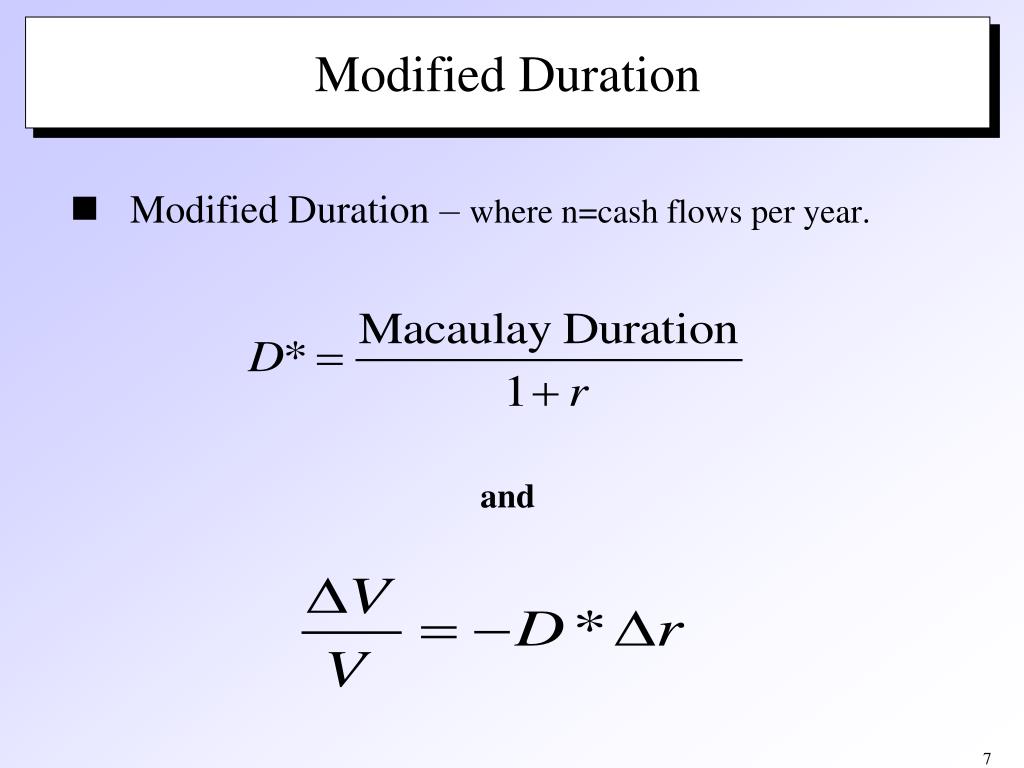

Spread Modified Duration . For risky bonds, duration is defined as. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. Sensitivity of price due to change in underlying yield. Modified duration follows the concept. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. It is an essential component in. Recall that modified duration measures the percentage. Modified duration is a measure of a bond's price sensitivity to changes in interest rates. Spread duration is a key metric that helps investors.

from www.slideserve.com

It is an essential component in. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. Spread duration is a key metric that helps investors. Sensitivity of price due to change in underlying yield. Modified duration is a measure of a bond's price sensitivity to changes in interest rates. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. For risky bonds, duration is defined as. Recall that modified duration measures the percentage. Modified duration follows the concept. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates.

PPT Bond Duration PowerPoint Presentation, free download ID5585530

Spread Modified Duration It is an essential component in. Recall that modified duration measures the percentage. It is an essential component in. Spread duration is a key metric that helps investors. Modified duration is a measure of a bond's price sensitivity to changes in interest rates. Modified duration follows the concept. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. For risky bonds, duration is defined as. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. Sensitivity of price due to change in underlying yield. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows.

From www.slideserve.com

PPT Bond Duration PowerPoint Presentation, free download ID2987215 Spread Modified Duration Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. Modified duration follows the concept. Recall that modified duration measures the percentage. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. Spread duration is a key metric that. Spread Modified Duration.

From www.slideserve.com

PPT Bond Duration PowerPoint Presentation, free download ID5585530 Spread Modified Duration Modified duration follows the concept. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. Recall that modified duration measures the percentage. Spread duration is a key metric that helps investors. It is. Spread Modified Duration.

From www.slideserve.com

PPT FINC4101 Investment Analysis PowerPoint Presentation, free Spread Modified Duration Modified duration follows the concept. Sensitivity of price due to change in underlying yield. It is an essential component in. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. For risky bonds, duration is defined as. Recall that modified duration measures the percentage. Modified duration. Spread Modified Duration.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation ID3950949 Spread Modified Duration It is an essential component in. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. Recall that modified duration measures the percentage. Spread duration is a key metric that helps investors. Modified duration follows the concept. Sensitivity of price due to change in underlying yield. Modified duration is a. Spread Modified Duration.

From www.ejshin.org

Education Ultimate Fixed 101 What are Credit Spread, Spread Spread Modified Duration Modified duration follows the concept. Sensitivity of price due to change in underlying yield. It is an essential component in. Spread duration is a key metric that helps investors. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. Recall that modified duration measures the percentage.. Spread Modified Duration.

From giojpgkdt.blob.core.windows.net

Modified Spread Duration Formula at Suzanne Wallace blog Spread Modified Duration Sensitivity of price due to change in underlying yield. Modified duration follows the concept. Spread duration is a key metric that helps investors. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. It is an essential component in. For risky bonds, duration is defined as. Recall that modified duration. Spread Modified Duration.

From www.studocu.com

DurationModifiedDurationandConvexity 2 Duration, Modified Spread Modified Duration Spread duration is a key metric that helps investors. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. Sensitivity of price due to change in. Spread Modified Duration.

From fundsnetservices.com

Modified Duration Spread Modified Duration The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. For risky bonds, duration is defined as. Modified duration is a measure of a bond's price sensitivity to changes in interest rates. Modified. Spread Modified Duration.

From www.slideserve.com

PPT CFA REVIEW PowerPoint Presentation, free download ID5201848 Spread Modified Duration Modified duration is a measure of a bond's price sensitivity to changes in interest rates. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. It is an essential. Spread Modified Duration.

From www.slideserve.com

PPT Duration , Modified Duration, Convexity PowerPoint Presentation Spread Modified Duration For risky bonds, duration is defined as. Sensitivity of price due to change in underlying yield. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. Modified duration is a measure of a bond's price sensitivity to changes in interest rates. (roughly) the (negative of the) percentage change in a bond’s price for. Spread Modified Duration.

From www.researchgate.net

Weighted Average Real Credit Spread vs. Merton Model, Merton Modified Spread Modified Duration For risky bonds, duration is defined as. Sensitivity of price due to change in underlying yield. Spread duration is a key metric that helps investors. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. Recall that modified duration measures the percentage. The macaulay duration calculates. Spread Modified Duration.

From www.investopedia.com

Effective Duration Definition, Formula, Example Spread Modified Duration Sensitivity of price due to change in underlying yield. Modified duration follows the concept. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. It is an essential component in. Spread duration is a key metric that helps investors. Modified duration is a measure of a bond's price sensitivity to. Spread Modified Duration.

From slideplayer.com

Duration and convexity for Securities ppt download Spread Modified Duration Modified duration follows the concept. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. It is an essential component in. For risky bonds, duration is defined as. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. Sensitivity of price due to. Spread Modified Duration.

From www.slideserve.com

PPT Bond Price, Yield, Duration PowerPoint Presentation, free Spread Modified Duration Modified duration is a measure of a bond's price sensitivity to changes in interest rates. It is an essential component in. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's. Spread Modified Duration.

From www.youtube.com

CFA Level I Fixed Approximate Modified Duration and Convexity Spread Modified Duration The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. For risky bonds, duration is defined as. Modified duration follows the concept. It is an essential component in. Spread duration is a key metric that helps investors. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in. Spread Modified Duration.

From www.slideserve.com

PPT FINC4101 Investment Analysis PowerPoint Presentation, free Spread Modified Duration Modified duration is a measure of a bond's price sensitivity to changes in interest rates. Spread duration is a key metric that helps investors. Sensitivity of price due to change in underlying yield. It is an essential component in. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change. Spread Modified Duration.

From analystprep.com

Calculate and Interpret Convexity CFA Level 1 AnalystPrep Spread Modified Duration Sensitivity of price due to change in underlying yield. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. Spread duration is a key metric that helps investors. Recall that modified duration measures the percentage. Modified duration follows the concept. It is an essential component in. Modified duration is a measure of a. Spread Modified Duration.

From giogercki.blob.core.windows.net

Spread Duration Mbs at Mary Mosby blog Spread Modified Duration It is an essential component in. Spread duration is a key metric that helps investors. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. Modified duration is a measure of a bond's price sensitivity to changes in interest rates. (roughly) the (negative of the) percentage. Spread Modified Duration.

From www.britannica.com

Bond Duration Definition, Formula, & How to Calculate Britannica Money Spread Modified Duration Recall that modified duration measures the percentage. Spread duration is a key metric that helps investors. For risky bonds, duration is defined as. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. It is an essential component in. Modified duration follows the concept. Sensitivity of price due to change in underlying yield.. Spread Modified Duration.

From www.financestrategists.com

Modified Duration Meaning, Formula, Applications, & Limitations Spread Modified Duration It is an essential component in. For risky bonds, duration is defined as. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. Recall that modified duration measures the percentage. Modified duration is a measure of a bond's price sensitivity to changes in interest rates. Spread duration is a key metric that helps. Spread Modified Duration.

From fr.thptnganamst.edu.vn

Ntroduire 52+ imagen formule de la duration fr.thptnganamst.edu.vn Spread Modified Duration The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. Recall that modified duration measures the percentage. For risky bonds, duration is defined as. It is an essential component in. Modified duration is a measure of a bond's price sensitivity to changes in interest rates. Spread duration is a key metric that helps. Spread Modified Duration.

From www.slideserve.com

PPT Duration and Yield Changes PowerPoint Presentation, free download Spread Modified Duration For risky bonds, duration is defined as. Recall that modified duration measures the percentage. Modified duration is a measure of a bond's price sensitivity to changes in interest rates. It is an essential component in. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. The macaulay duration calculates the. Spread Modified Duration.

From www.investopedia.com

Duration and Convexity to Measure Bond Risk Spread Modified Duration It is an essential component in. Recall that modified duration measures the percentage. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. Modified duration follows the concept. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. Modified duration is a measure. Spread Modified Duration.

From www.thestreet.com

What Is Duration of a Bond? TheStreet Definition TheStreet Spread Modified Duration The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. Spread duration is a key metric that helps investors. Modified duration is a measure of a bond's price sensitivity. Spread Modified Duration.

From www.pzacademy.com

spread duration有问必答品职教育 专注CFA ESG FRM CPA 考研等财经培训课程 Spread Modified Duration Modified duration follows the concept. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. Spread duration is a key metric that helps investors. Sensitivity of price due to change in underlying yield. For risky bonds, duration is defined as. The macaulay duration calculates the weighted. Spread Modified Duration.

From www.slideserve.com

PPT Chapter 10 PowerPoint Presentation, free download ID1138614 Spread Modified Duration Recall that modified duration measures the percentage. Spread duration is a key metric that helps investors. Sensitivity of price due to change in underlying yield. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. It is an essential component in. (roughly) the (negative of the). Spread Modified Duration.

From analystprep.com

Macaulay, Modified, and Effective Durations CFA Program Level 1 Spread Modified Duration (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest. Spread Modified Duration.

From www.educba.com

Macaulay Duration Formula Example with Excel Template Spread Modified Duration Sensitivity of price due to change in underlying yield. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. Modified duration follows the concept. For risky bonds, duration is defined as. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. It is. Spread Modified Duration.

From www.slideteam.net

Spread Duration Calculation In Powerpoint And Google Slides Cpb PPT Spread Modified Duration Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. For risky bonds, duration is defined as. Sensitivity of price due to change in underlying yield. Modified duration is a measure of a bond's price sensitivity to changes in interest rates. Spread duration is a key. Spread Modified Duration.

From money.stackexchange.com

bonds Difference between Macaulay duration and modified duration Spread Modified Duration Spread duration is a key metric that helps investors. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. Sensitivity of price due to change in underlying yield. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in. Spread Modified Duration.

From www.chegg.com

Solved 1. The bond's YTM is 4, coupon is 9, term is 5 Spread Modified Duration Sensitivity of price due to change in underlying yield. Spread duration is a key metric that helps investors. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. Modified duration follows the concept. Recall that modified duration measures the percentage. Modified duration is a measure of a bond's price sensitivity. Spread Modified Duration.

From www.analystforum.com

Modified Duration in SemiAnnual periods converted to Annual Periods Spread Modified Duration The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. Modified duration follows the concept. Modified duration is a measure of a bond's price sensitivity to changes in interest rates. For risky bonds,. Spread Modified Duration.

From transacted.io

Spread Duration Explained Transacted Spread Modified Duration Spread duration is a key metric that helps investors. Modified duration follows the concept. It is an essential component in. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in. Spread Modified Duration.

From www.youtube.com

Duration y Modified Duration (video 2) YouTube Spread Modified Duration Sensitivity of price due to change in underlying yield. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its spread over a. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. Modified duration is a measure of a bond's price sensitivity to changes in interest. Spread Modified Duration.

From slideplayer.com

Duration and convexity for Securities ppt download Spread Modified Duration Modified duration follows the concept. Modified duration is a measure of a bond's price sensitivity to changes in interest rates. The macaulay duration calculates the weighted average time before a bondholder would receive the bond's cash flows. It is an essential component in. (roughly) the (negative of the) percentage change in a bond’s price for a 1% change in its. Spread Modified Duration.