Define Fixed Cost In Economic Terms . Fixed costs are independent expenses that companies must pay, regardless of what their business does. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. That is to say, fixed costs remain constant for a given period despite. Whatever the output fixed costs (fc). What is a fixed cost? Fixed costs refer to the business expenses that remain constant regardless of the level of production or. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. A fixed cost is a business cost that is unrelated to output. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. They can also be referred to as ‘indirect costs’.

from efinancemanagement.com

That is to say, fixed costs remain constant for a given period despite. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Fixed costs refer to the business expenses that remain constant regardless of the level of production or. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs are independent expenses that companies must pay, regardless of what their business does. Whatever the output fixed costs (fc). They can also be referred to as ‘indirect costs’. What is a fixed cost? Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. A fixed cost is a business cost that is unrelated to output.

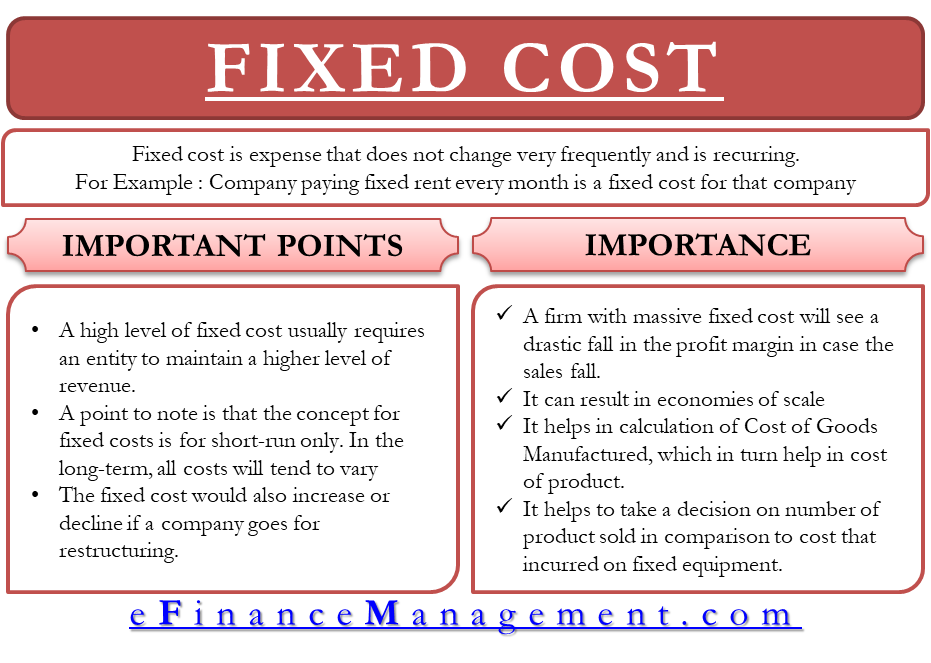

Fixed Cost What It Is And What's Its Importance?

Define Fixed Cost In Economic Terms Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs refer to the business expenses that remain constant regardless of the level of production or. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. That is to say, fixed costs remain constant for a given period despite. A fixed cost is a business cost that is unrelated to output. What is a fixed cost? Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs are independent expenses that companies must pay, regardless of what their business does. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Whatever the output fixed costs (fc). They can also be referred to as ‘indirect costs’.

From tutorstips.com

Difference between Fixed Cost and Variable Cost Tutor's Tips Define Fixed Cost In Economic Terms They can also be referred to as ‘indirect costs’. Fixed costs are independent expenses that companies must pay, regardless of what their business does. Fixed costs refer to the business expenses that remain constant regardless of the level of production or. What is a fixed cost? Whatever the output fixed costs (fc). A fixed cost is a business cost that. Define Fixed Cost In Economic Terms.

From en.ppt-online.org

This course is concerned with making good economic decisions in Define Fixed Cost In Economic Terms That is to say, fixed costs remain constant for a given period despite. Whatever the output fixed costs (fc). Fixed costs refer to the business expenses that remain constant regardless of the level of production or. What is a fixed cost? Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the. Define Fixed Cost In Economic Terms.

From www.akounto.com

Fixed Cost Definition, Calculation & Examples Akounto Define Fixed Cost In Economic Terms Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. What is a fixed cost? That is to say, fixed costs remain constant for a given period despite. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or. Define Fixed Cost In Economic Terms.

From www.educba.com

Fixed Cost Formula Calculator (Examples with Excel Template) Define Fixed Cost In Economic Terms Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Whatever the output fixed costs (fc). That is to say, fixed costs remain constant for a given period despite. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or. Define Fixed Cost In Economic Terms.

From www.slideserve.com

PPT Chapter 10Continued PowerPoint Presentation, free download ID Define Fixed Cost In Economic Terms What is a fixed cost? They can also be referred to as ‘indirect costs’. Whatever the output fixed costs (fc). Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. That is to say, fixed costs remain constant for a given period despite. Fixed costs. Define Fixed Cost In Economic Terms.

From www.marketing91.com

Average Fixed Cost Definition, Formula and Examples Marketing91 Define Fixed Cost In Economic Terms Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Fixed costs refer to the business expenses that remain constant regardless of the level of production or. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed costs are independent expenses that. Define Fixed Cost In Economic Terms.

From makalah31dsa.blogspot.com

Finance Charges Economics Meaning Fixed Cost Definition 6 Examples Vs Define Fixed Cost In Economic Terms A fixed cost is a business cost that is unrelated to output. Fixed costs are independent expenses that companies must pay, regardless of what their business does. Whatever the output fixed costs (fc). Fixed costs refer to the business expenses that remain constant regardless of the level of production or. They can also be referred to as ‘indirect costs’. That. Define Fixed Cost In Economic Terms.

From www.educba.com

Average Fixed Cost Formula Step by Step Solutions (Calculator) Define Fixed Cost In Economic Terms Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. What is a fixed cost? They can also be referred to as ‘indirect costs’. Fixed costs are independent expenses that companies must pay, regardless of what their business does. Whatever the output fixed costs (fc). That is to say, fixed costs remain. Define Fixed Cost In Economic Terms.

From www.intelligenteconomist.com

Theory Of Production Cost Theory Intelligent Economist Define Fixed Cost In Economic Terms Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Whatever the output fixed costs (fc). Fixed costs are independent expenses that companies must pay, regardless of what their business does. A fixed cost is a business cost that is unrelated to output. Fixed costs are expenses that do not change with. Define Fixed Cost In Economic Terms.

From blog.hubspot.com

Fixed Cost What It Is & How to Calculate It Define Fixed Cost In Economic Terms What is a fixed cost? Fixed costs are independent expenses that companies must pay, regardless of what their business does. Fixed costs refer to the business expenses that remain constant regardless of the level of production or. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed costs are expenses that. Define Fixed Cost In Economic Terms.

From www.tutor2u.net

Explaining Fixed and Variable Costs of… Economics tutor2u Define Fixed Cost In Economic Terms Whatever the output fixed costs (fc). They can also be referred to as ‘indirect costs’. Fixed costs are independent expenses that companies must pay, regardless of what their business does. That is to say, fixed costs remain constant for a given period despite. A fixed cost is a business cost that is unrelated to output. What is a fixed cost?. Define Fixed Cost In Economic Terms.

From quickbooks.intuit.com

Operating Costs Definition, Formula & Examples QuickBooks Define Fixed Cost In Economic Terms Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed costs are independent expenses that companies must pay, regardless of what their business does. Whatever the output fixed costs (fc). What is a fixed cost? Fixed costs are expenses that do not change with increases or decreases in a company’s production. Define Fixed Cost In Economic Terms.

From efinancemanagement.com

Variable Costs and Fixed Costs Define Fixed Cost In Economic Terms That is to say, fixed costs remain constant for a given period despite. They can also be referred to as ‘indirect costs’. A fixed cost is a business cost that is unrelated to output. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. What. Define Fixed Cost In Economic Terms.

From www.cheggindia.com

Fixed Cost and Variable Cost Comprehensive Guide for 2024 Define Fixed Cost In Economic Terms What is a fixed cost? A fixed cost is a business cost that is unrelated to output. Fixed costs refer to the business expenses that remain constant regardless of the level of production or. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. They. Define Fixed Cost In Economic Terms.

From ar.inspiredpencil.com

Fixed Cost Define Fixed Cost In Economic Terms A fixed cost is a business cost that is unrelated to output. Fixed costs are independent expenses that companies must pay, regardless of what their business does. That is to say, fixed costs remain constant for a given period despite. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume. Define Fixed Cost In Economic Terms.

From sendpulse.com

What is an Average Fixed Cost Basics SendPulse Define Fixed Cost In Economic Terms Fixed costs are independent expenses that companies must pay, regardless of what their business does. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. What is a fixed cost? They can also be referred to as ‘indirect costs’. Fixed costs are expenses that do not change with increases or decreases in. Define Fixed Cost In Economic Terms.

From www.1099cafe.com

What is a Fixed Cost Variable vs Fixed Expenses — 1099 Cafe Define Fixed Cost In Economic Terms Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs refer to the business expenses that remain constant regardless of the level of production or. A fixed cost is a business cost that is unrelated to output. Whatever the output fixed costs (fc).. Define Fixed Cost In Economic Terms.

From www.youtube.com

define fixed cost define variable cost fixed cost vs variable cost Define Fixed Cost In Economic Terms That is to say, fixed costs remain constant for a given period despite. Fixed costs refer to the business expenses that remain constant regardless of the level of production or. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Whatever the output fixed costs (fc). Fixed costs are independent expenses. Define Fixed Cost In Economic Terms.

From efinancemanagement.com

Types of Costs Direct & Indirect Costs Fixed & Variable Costs eFM Define Fixed Cost In Economic Terms Fixed costs are independent expenses that companies must pay, regardless of what their business does. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. A fixed cost is a business cost that is unrelated to output. What is a fixed cost? Fixed costs are expenses that do not change with increases. Define Fixed Cost In Economic Terms.

From www.investopedia.com

Fixed Cost What It Is and How It’s Used in Business Define Fixed Cost In Economic Terms A fixed cost is a business cost that is unrelated to output. That is to say, fixed costs remain constant for a given period despite. They can also be referred to as ‘indirect costs’. Fixed costs are independent expenses that companies must pay, regardless of what their business does. Fixed costs (or constant costs) are costs that are not affected. Define Fixed Cost In Economic Terms.

From definitionjull.blogspot.com

Fixed Cost Definition Economics definitionjull Define Fixed Cost In Economic Terms A fixed cost is a business cost that is unrelated to output. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. That is to say, fixed costs remain constant for a given period despite. Fixed costs are expenses that do not change with increases or decreases in a company’s production or. Define Fixed Cost In Economic Terms.

From sendpulse.com

What is an Average Fixed Cost Basics SendPulse Define Fixed Cost In Economic Terms Whatever the output fixed costs (fc). That is to say, fixed costs remain constant for a given period despite. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Fixed costs are independent. Define Fixed Cost In Economic Terms.

From gupshups.org

What is Difference between Fixed Cost and Variable Cost? Define Fixed Cost In Economic Terms They can also be referred to as ‘indirect costs’. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Whatever the output fixed costs (fc). A fixed cost is a business cost that is unrelated to output. What is a fixed cost? That is to. Define Fixed Cost In Economic Terms.

From oer.pressbooks.pub

Understanding the cost equation Accounting and Accountability Define Fixed Cost In Economic Terms Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. They can also be referred to as ‘indirect costs’. Fixed costs refer to the business expenses that. Define Fixed Cost In Economic Terms.

From www.slideserve.com

PPT Cost Concepts in Economics PowerPoint Presentation, free download Define Fixed Cost In Economic Terms Fixed costs are independent expenses that companies must pay, regardless of what their business does. Whatever the output fixed costs (fc). Fixed costs refer to the business expenses that remain constant regardless of the level of production or. A fixed cost is a business cost that is unrelated to output. Fixed costs are a type of expense or cost that. Define Fixed Cost In Economic Terms.

From www.slideshare.net

Business economics cost analysis Define Fixed Cost In Economic Terms They can also be referred to as ‘indirect costs’. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Fixed costs are independent expenses that companies. Define Fixed Cost In Economic Terms.

From efinancemanagement.com

Types and Basis of Cost Classification Nature, Functions, Behavior eFM Define Fixed Cost In Economic Terms Whatever the output fixed costs (fc). Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. What is a fixed cost? Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. A fixed cost is a business. Define Fixed Cost In Economic Terms.

From penpoin.com

Total Variable Cost Examples, Curve, Importance Define Fixed Cost In Economic Terms Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. They can also be referred to as ‘indirect costs’. A fixed cost is a business cost that. Define Fixed Cost In Economic Terms.

From learnbusinessconcepts.com

Fixed Cost Explanation, Formula, Calculation, and Examples Define Fixed Cost In Economic Terms Fixed costs refer to the business expenses that remain constant regardless of the level of production or. A fixed cost is a business cost that is unrelated to output. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. That is to say, fixed costs remain constant for a given period despite.. Define Fixed Cost In Economic Terms.

From www.youtube.com

Fixed Cost Vs Variable Cost Difference Between them with Example Define Fixed Cost In Economic Terms That is to say, fixed costs remain constant for a given period despite. A fixed cost is a business cost that is unrelated to output. They can also be referred to as ‘indirect costs’. Fixed costs are independent expenses that companies must pay, regardless of what their business does. Fixed costs (or constant costs) are costs that are not affected. Define Fixed Cost In Economic Terms.

From www.geektonight.com

10 Types Of Costs Production Economics Define Fixed Cost In Economic Terms A fixed cost is a business cost that is unrelated to output. Whatever the output fixed costs (fc). Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs are independent expenses that companies must pay, regardless of what their business does. Fixed costs. Define Fixed Cost In Economic Terms.

From efinancemanagement.com

Fixed Cost What It Is And What's Its Importance? Define Fixed Cost In Economic Terms Fixed costs refer to the business expenses that remain constant regardless of the level of production or. They can also be referred to as ‘indirect costs’. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. That is to say, fixed costs remain constant for. Define Fixed Cost In Economic Terms.

From www.superfastcpa.com

What is the Difference Between Fixed Cost and Variable Cost? Define Fixed Cost In Economic Terms A fixed cost is a business cost that is unrelated to output. What is a fixed cost? Fixed costs refer to the business expenses that remain constant regardless of the level of production or. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. That is to say, fixed costs remain. Define Fixed Cost In Economic Terms.

From avada.io

How to Calculate Fixed Cost? Formula, Guide and Examples Define Fixed Cost In Economic Terms That is to say, fixed costs remain constant for a given period despite. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs are independent expenses that companies must pay, regardless of what their business does. What is a fixed cost? Fixed costs. Define Fixed Cost In Economic Terms.

From slidemodel.com

What is Cost Structure in a Business Model and Why Does it Matter Define Fixed Cost In Economic Terms Fixed costs are independent expenses that companies must pay, regardless of what their business does. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs refer to the business expenses that remain constant regardless of the level of production or. Whatever the output. Define Fixed Cost In Economic Terms.