Monte Carlo Simulation Geometric Brownian Motion Python . I will not be getting into the theoretical background of its derivation. We operate under the equivalent martingale measure. For a monte carlo simulation, one must generate random numbers representing prices according to the relative. Geometric brownian motion is a stochastic process as shown in equation below. While building the script, we also explore the intuition behind the gbm model. In this tutorial we will be simulating geometric brownian motion in python. I built a web app using python flask that allows you to simulate future stock price movements using a method called monte carlo simulations with the choice of two ‘flavours’ :. In this article, we discuss how to construct a geometric brownian motion(gbm) simulation using python. Geometric brownian motion (gbm) s is defined by s0 > 0 and the dynamics as defined in the. I am relatively new to python, and i am receiving an answer that i. How to simulate a price path using geometric brownian motion model. This article will demonstrate how to simulate brownian motion based asset paths using the python programming language and theoretical.

from nasyring.github.io

This article will demonstrate how to simulate brownian motion based asset paths using the python programming language and theoretical. Geometric brownian motion (gbm) s is defined by s0 > 0 and the dynamics as defined in the. While building the script, we also explore the intuition behind the gbm model. We operate under the equivalent martingale measure. Geometric brownian motion is a stochastic process as shown in equation below. In this article, we discuss how to construct a geometric brownian motion(gbm) simulation using python. How to simulate a price path using geometric brownian motion model. I am relatively new to python, and i am receiving an answer that i. For a monte carlo simulation, one must generate random numbers representing prices according to the relative. I will not be getting into the theoretical background of its derivation.

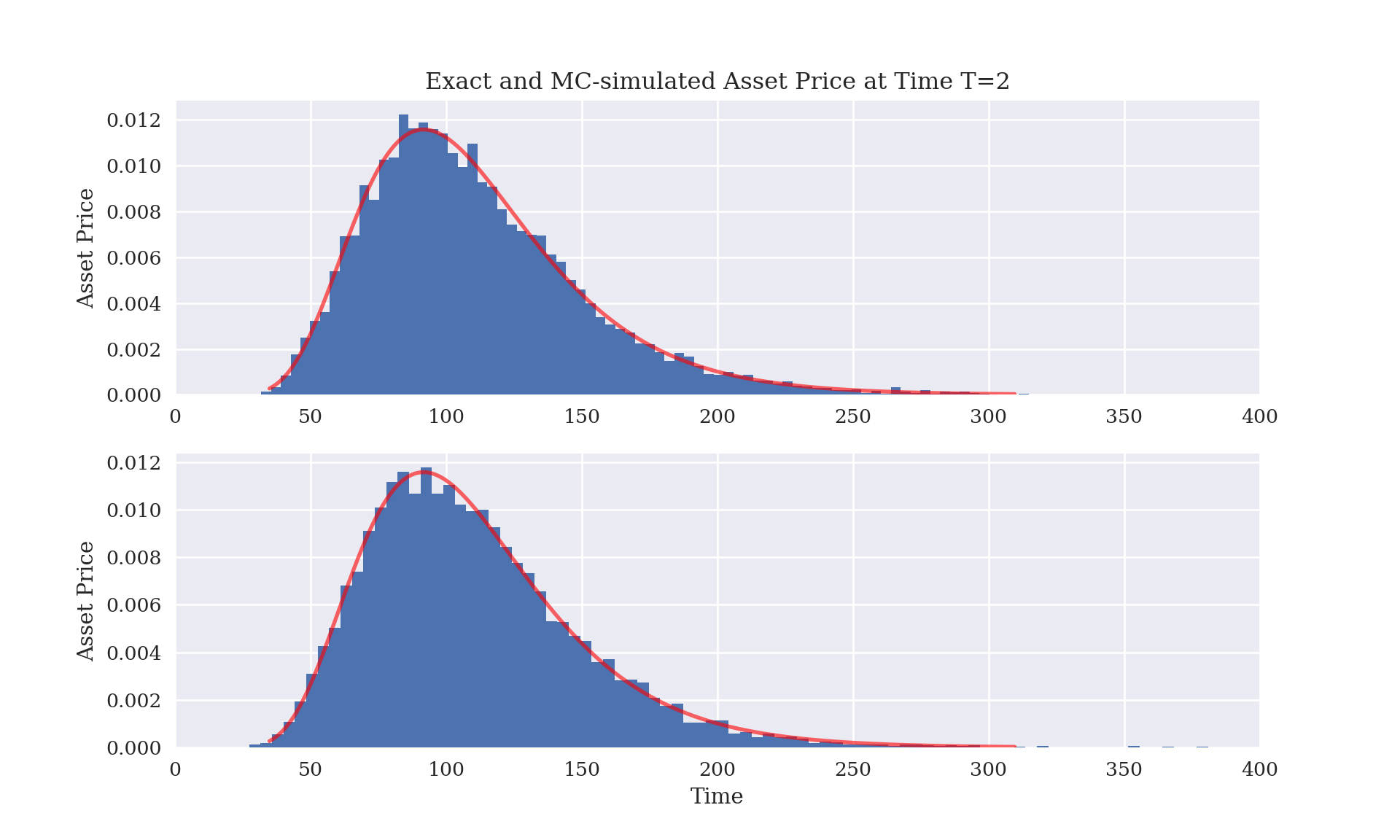

Chapter 4 The geometric Brownian motion model of asset value and Monte Carlo simulation

Monte Carlo Simulation Geometric Brownian Motion Python For a monte carlo simulation, one must generate random numbers representing prices according to the relative. Geometric brownian motion (gbm) s is defined by s0 > 0 and the dynamics as defined in the. While building the script, we also explore the intuition behind the gbm model. Geometric brownian motion is a stochastic process as shown in equation below. For a monte carlo simulation, one must generate random numbers representing prices according to the relative. How to simulate a price path using geometric brownian motion model. We operate under the equivalent martingale measure. I built a web app using python flask that allows you to simulate future stock price movements using a method called monte carlo simulations with the choice of two ‘flavours’ :. In this tutorial we will be simulating geometric brownian motion in python. I will not be getting into the theoretical background of its derivation. This article will demonstrate how to simulate brownian motion based asset paths using the python programming language and theoretical. I am relatively new to python, and i am receiving an answer that i. In this article, we discuss how to construct a geometric brownian motion(gbm) simulation using python.

From towardsdatascience.com

Stochastic Processes Simulation — Geometric Brownian Motion by Diego Barba Towards Data Science Monte Carlo Simulation Geometric Brownian Motion Python I built a web app using python flask that allows you to simulate future stock price movements using a method called monte carlo simulations with the choice of two ‘flavours’ :. For a monte carlo simulation, one must generate random numbers representing prices according to the relative. I will not be getting into the theoretical background of its derivation. In. Monte Carlo Simulation Geometric Brownian Motion Python.

From quantjourney.substack.com

Exploring Stock Market Dynamics with Geometric Brownian Motion A Python Simulation Monte Carlo Simulation Geometric Brownian Motion Python Geometric brownian motion is a stochastic process as shown in equation below. I am relatively new to python, and i am receiving an answer that i. We operate under the equivalent martingale measure. In this article, we discuss how to construct a geometric brownian motion(gbm) simulation using python. How to simulate a price path using geometric brownian motion model. I. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.youtube.com

Python code Monte Carlo Simulation (Tolerance Analysis) YouTube Monte Carlo Simulation Geometric Brownian Motion Python For a monte carlo simulation, one must generate random numbers representing prices according to the relative. I built a web app using python flask that allows you to simulate future stock price movements using a method called monte carlo simulations with the choice of two ‘flavours’ :. How to simulate a price path using geometric brownian motion model. I am. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.researchgate.net

3.4. MonteCarlo simulation of Brownian bridge pinned at (0, 0) and (1,... Download Scientific Monte Carlo Simulation Geometric Brownian Motion Python For a monte carlo simulation, one must generate random numbers representing prices according to the relative. I am relatively new to python, and i am receiving an answer that i. This article will demonstrate how to simulate brownian motion based asset paths using the python programming language and theoretical. Geometric brownian motion (gbm) s is defined by s0 > 0. Monte Carlo Simulation Geometric Brownian Motion Python.

From nasyring.github.io

Chapter 4 The geometric Brownian motion model of asset value and Monte Carlo simulation Monte Carlo Simulation Geometric Brownian Motion Python While building the script, we also explore the intuition behind the gbm model. I will not be getting into the theoretical background of its derivation. In this article, we discuss how to construct a geometric brownian motion(gbm) simulation using python. Geometric brownian motion (gbm) s is defined by s0 > 0 and the dynamics as defined in the. I built. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.youtube.com

Python code Monte Carlo Simulation (calculate pi value, 3.1415...) YouTube Monte Carlo Simulation Geometric Brownian Motion Python I built a web app using python flask that allows you to simulate future stock price movements using a method called monte carlo simulations with the choice of two ‘flavours’ :. How to simulate a price path using geometric brownian motion model. I will not be getting into the theoretical background of its derivation. Geometric brownian motion is a stochastic. Monte Carlo Simulation Geometric Brownian Motion Python.

From 9to5answer.com

[Solved] Geometric Brownian Motion simulation in Python 9to5Answer Monte Carlo Simulation Geometric Brownian Motion Python Geometric brownian motion is a stochastic process as shown in equation below. Geometric brownian motion (gbm) s is defined by s0 > 0 and the dynamics as defined in the. While building the script, we also explore the intuition behind the gbm model. In this tutorial we will be simulating geometric brownian motion in python. I will not be getting. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.youtube.com

Simple Monte Carlo Simulation of Stock Prices with Python YouTube Monte Carlo Simulation Geometric Brownian Motion Python Geometric brownian motion is a stochastic process as shown in equation below. I am relatively new to python, and i am receiving an answer that i. We operate under the equivalent martingale measure. In this tutorial we will be simulating geometric brownian motion in python. This article will demonstrate how to simulate brownian motion based asset paths using the python. Monte Carlo Simulation Geometric Brownian Motion Python.

From towardsdatascience.com

Monte Carlo Simulation in R with focus on Option Pricing by Ojasvin Sood Towards Data Science Monte Carlo Simulation Geometric Brownian Motion Python How to simulate a price path using geometric brownian motion model. While building the script, we also explore the intuition behind the gbm model. I will not be getting into the theoretical background of its derivation. In this article, we discuss how to construct a geometric brownian motion(gbm) simulation using python. For a monte carlo simulation, one must generate random. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.youtube.com

Monte Carlo Simulation using Python (Part 3) Probability Distributions YouTube Monte Carlo Simulation Geometric Brownian Motion Python In this tutorial we will be simulating geometric brownian motion in python. In this article, we discuss how to construct a geometric brownian motion(gbm) simulation using python. I will not be getting into the theoretical background of its derivation. We operate under the equivalent martingale measure. Geometric brownian motion (gbm) s is defined by s0 > 0 and the dynamics. Monte Carlo Simulation Geometric Brownian Motion Python.

From github.com

GitHub zuccrobot/stockmarketmontecarlosimulation Analysing the stock prices using Monte Carlo Simulation Geometric Brownian Motion Python Geometric brownian motion (gbm) s is defined by s0 > 0 and the dynamics as defined in the. This article will demonstrate how to simulate brownian motion based asset paths using the python programming language and theoretical. In this tutorial we will be simulating geometric brownian motion in python. I built a web app using python flask that allows you. Monte Carlo Simulation Geometric Brownian Motion Python.

From remington-work.blogspot.com

work Simulation of a Geometric Brownian Motion in R Monte Carlo Simulation Geometric Brownian Motion Python I built a web app using python flask that allows you to simulate future stock price movements using a method called monte carlo simulations with the choice of two ‘flavours’ :. I will not be getting into the theoretical background of its derivation. We operate under the equivalent martingale measure. Geometric brownian motion (gbm) s is defined by s0 >. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.mdpi.com

Mathematics Free FullText Geometric Brownian Motion (GBM) of Stock Indexes and Financial Monte Carlo Simulation Geometric Brownian Motion Python In this tutorial we will be simulating geometric brownian motion in python. While building the script, we also explore the intuition behind the gbm model. Geometric brownian motion is a stochastic process as shown in equation below. This article will demonstrate how to simulate brownian motion based asset paths using the python programming language and theoretical. I built a web. Monte Carlo Simulation Geometric Brownian Motion Python.

From nasyring.github.io

Chapter 4 The geometric Brownian motion model of asset value and Monte Carlo simulation Monte Carlo Simulation Geometric Brownian Motion Python In this tutorial we will be simulating geometric brownian motion in python. While building the script, we also explore the intuition behind the gbm model. We operate under the equivalent martingale measure. I built a web app using python flask that allows you to simulate future stock price movements using a method called monte carlo simulations with the choice of. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.turingfinance.com

Random walks down Wall Street, Stochastic Processes in Python Monte Carlo Simulation Geometric Brownian Motion Python I built a web app using python flask that allows you to simulate future stock price movements using a method called monte carlo simulations with the choice of two ‘flavours’ :. Geometric brownian motion is a stochastic process as shown in equation below. I am relatively new to python, and i am receiving an answer that i. In this tutorial. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.researchgate.net

3.3. MonteCarlo simulation of Brownian motion starting at x = 0, with... Download Scientific Monte Carlo Simulation Geometric Brownian Motion Python This article will demonstrate how to simulate brownian motion based asset paths using the python programming language and theoretical. I will not be getting into the theoretical background of its derivation. Geometric brownian motion is a stochastic process as shown in equation below. We operate under the equivalent martingale measure. While building the script, we also explore the intuition behind. Monte Carlo Simulation Geometric Brownian Motion Python.

From quantjourney.substack.com

Exploring Stock Market Dynamics with Geometric Brownian Motion A Python Simulation Monte Carlo Simulation Geometric Brownian Motion Python I will not be getting into the theoretical background of its derivation. How to simulate a price path using geometric brownian motion model. For a monte carlo simulation, one must generate random numbers representing prices according to the relative. Geometric brownian motion is a stochastic process as shown in equation below. While building the script, we also explore the intuition. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.youtube.com

Geometric Brownian Motion SDE Monte Carlo Simulation Python YouTube Monte Carlo Simulation Geometric Brownian Motion Python In this tutorial we will be simulating geometric brownian motion in python. Geometric brownian motion is a stochastic process as shown in equation below. This article will demonstrate how to simulate brownian motion based asset paths using the python programming language and theoretical. How to simulate a price path using geometric brownian motion model. I am relatively new to python,. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.researchgate.net

Monte Carlo simulations for the geometric Brownian motion (3) for λ =... Download Scientific Monte Carlo Simulation Geometric Brownian Motion Python We operate under the equivalent martingale measure. I will not be getting into the theoretical background of its derivation. I am relatively new to python, and i am receiving an answer that i. In this tutorial we will be simulating geometric brownian motion in python. While building the script, we also explore the intuition behind the gbm model. Geometric brownian. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.researchgate.net

Brownian motion movement of 256 particles for t = 1 s. (a) Surface plot... Download Scientific Monte Carlo Simulation Geometric Brownian Motion Python In this tutorial we will be simulating geometric brownian motion in python. In this article, we discuss how to construct a geometric brownian motion(gbm) simulation using python. I am relatively new to python, and i am receiving an answer that i. I built a web app using python flask that allows you to simulate future stock price movements using a. Monte Carlo Simulation Geometric Brownian Motion Python.

From medium.com

Measuring Portfolio risk using Monte Carlo simulation in python — Part 1 by Abdalla A. Mahgoub Monte Carlo Simulation Geometric Brownian Motion Python I will not be getting into the theoretical background of its derivation. Geometric brownian motion (gbm) s is defined by s0 > 0 and the dynamics as defined in the. How to simulate a price path using geometric brownian motion model. I built a web app using python flask that allows you to simulate future stock price movements using a. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.researchgate.net

Monte Carlo simulations for the geometric Brownian motion (3) for λ =... Download Scientific Monte Carlo Simulation Geometric Brownian Motion Python Geometric brownian motion is a stochastic process as shown in equation below. I will not be getting into the theoretical background of its derivation. In this article, we discuss how to construct a geometric brownian motion(gbm) simulation using python. In this tutorial we will be simulating geometric brownian motion in python. Geometric brownian motion (gbm) s is defined by s0. Monte Carlo Simulation Geometric Brownian Motion Python.

From pythonprogramming.net

Python Programming Tutorials Monte Carlo Simulation Geometric Brownian Motion Python Geometric brownian motion (gbm) s is defined by s0 > 0 and the dynamics as defined in the. How to simulate a price path using geometric brownian motion model. I am relatively new to python, and i am receiving an answer that i. This article will demonstrate how to simulate brownian motion based asset paths using the python programming language. Monte Carlo Simulation Geometric Brownian Motion Python.

From github.com

GitHub rbhatia46/OptionsPricingMonteCarlo A monte Carlo simulation for Options Pricing Monte Carlo Simulation Geometric Brownian Motion Python Geometric brownian motion (gbm) s is defined by s0 > 0 and the dynamics as defined in the. In this tutorial we will be simulating geometric brownian motion in python. We operate under the equivalent martingale measure. I built a web app using python flask that allows you to simulate future stock price movements using a method called monte carlo. Monte Carlo Simulation Geometric Brownian Motion Python.

From quant-trading.co

Montecarlo simulation for Geometric Brownian Motion Quant Trading Monte Carlo Simulation Geometric Brownian Motion Python How to simulate a price path using geometric brownian motion model. While building the script, we also explore the intuition behind the gbm model. I built a web app using python flask that allows you to simulate future stock price movements using a method called monte carlo simulations with the choice of two ‘flavours’ :. We operate under the equivalent. Monte Carlo Simulation Geometric Brownian Motion Python.

From isquared.digital

Determinism, see Randomness in Action How to Model Stock Price iSquared Monte Carlo Simulation Geometric Brownian Motion Python How to simulate a price path using geometric brownian motion model. While building the script, we also explore the intuition behind the gbm model. This article will demonstrate how to simulate brownian motion based asset paths using the python programming language and theoretical. In this article, we discuss how to construct a geometric brownian motion(gbm) simulation using python. I will. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.reddit.com

Animated Visualization of Brownian Motion in Python r/Python Monte Carlo Simulation Geometric Brownian Motion Python In this tutorial we will be simulating geometric brownian motion in python. This article will demonstrate how to simulate brownian motion based asset paths using the python programming language and theoretical. I will not be getting into the theoretical background of its derivation. Geometric brownian motion (gbm) s is defined by s0 > 0 and the dynamics as defined in. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.youtube.com

Monte Carlo Simulation and Python 4 Plotting with Matplotlib YouTube Monte Carlo Simulation Geometric Brownian Motion Python This article will demonstrate how to simulate brownian motion based asset paths using the python programming language and theoretical. I will not be getting into the theoretical background of its derivation. I built a web app using python flask that allows you to simulate future stock price movements using a method called monte carlo simulations with the choice of two. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.youtube.com

Brownian motion simulation YouTube Monte Carlo Simulation Geometric Brownian Motion Python I am relatively new to python, and i am receiving an answer that i. In this tutorial we will be simulating geometric brownian motion in python. While building the script, we also explore the intuition behind the gbm model. In this article, we discuss how to construct a geometric brownian motion(gbm) simulation using python. I will not be getting into. Monte Carlo Simulation Geometric Brownian Motion Python.

From towardsdatascience.com

Monte Carlo Simulation in R with focus on Option Pricing by Ojasvin Sood Towards Data Science Monte Carlo Simulation Geometric Brownian Motion Python We operate under the equivalent martingale measure. I am relatively new to python, and i am receiving an answer that i. Geometric brownian motion is a stochastic process as shown in equation below. In this article, we discuss how to construct a geometric brownian motion(gbm) simulation using python. How to simulate a price path using geometric brownian motion model. For. Monte Carlo Simulation Geometric Brownian Motion Python.

From interestingfactsworld.com

3+ Legendary Brownian Motion Facts You Need to Know for School Monte Carlo Simulation Geometric Brownian Motion Python For a monte carlo simulation, one must generate random numbers representing prices according to the relative. In this article, we discuss how to construct a geometric brownian motion(gbm) simulation using python. Geometric brownian motion is a stochastic process as shown in equation below. I will not be getting into the theoretical background of its derivation. We operate under the equivalent. Monte Carlo Simulation Geometric Brownian Motion Python.

From math.stackexchange.com

probability Simulating Drifting Brownian Motion Mathematics Stack Exchange Monte Carlo Simulation Geometric Brownian Motion Python Geometric brownian motion (gbm) s is defined by s0 > 0 and the dynamics as defined in the. For a monte carlo simulation, one must generate random numbers representing prices according to the relative. We operate under the equivalent martingale measure. While building the script, we also explore the intuition behind the gbm model. Geometric brownian motion is a stochastic. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.youtube.com

Monte Carlo Simulation using Python (Part 2) Simulation, Plots, Formating YouTube Monte Carlo Simulation Geometric Brownian Motion Python Geometric brownian motion is a stochastic process as shown in equation below. For a monte carlo simulation, one must generate random numbers representing prices according to the relative. We operate under the equivalent martingale measure. Geometric brownian motion (gbm) s is defined by s0 > 0 and the dynamics as defined in the. How to simulate a price path using. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.youtube.com

Simulating Geometric Brownian Motion in Python Stochastic Calculus for Quants YouTube Monte Carlo Simulation Geometric Brownian Motion Python I built a web app using python flask that allows you to simulate future stock price movements using a method called monte carlo simulations with the choice of two ‘flavours’ :. For a monte carlo simulation, one must generate random numbers representing prices according to the relative. We operate under the equivalent martingale measure. In this article, we discuss how. Monte Carlo Simulation Geometric Brownian Motion Python.

From www.youtube.com

Monte Carlo Simulation in Python Jump Diffusion and Geometric Brownian Motion. YouTube Monte Carlo Simulation Geometric Brownian Motion Python For a monte carlo simulation, one must generate random numbers representing prices according to the relative. I am relatively new to python, and i am receiving an answer that i. How to simulate a price path using geometric brownian motion model. This article will demonstrate how to simulate brownian motion based asset paths using the python programming language and theoretical.. Monte Carlo Simulation Geometric Brownian Motion Python.