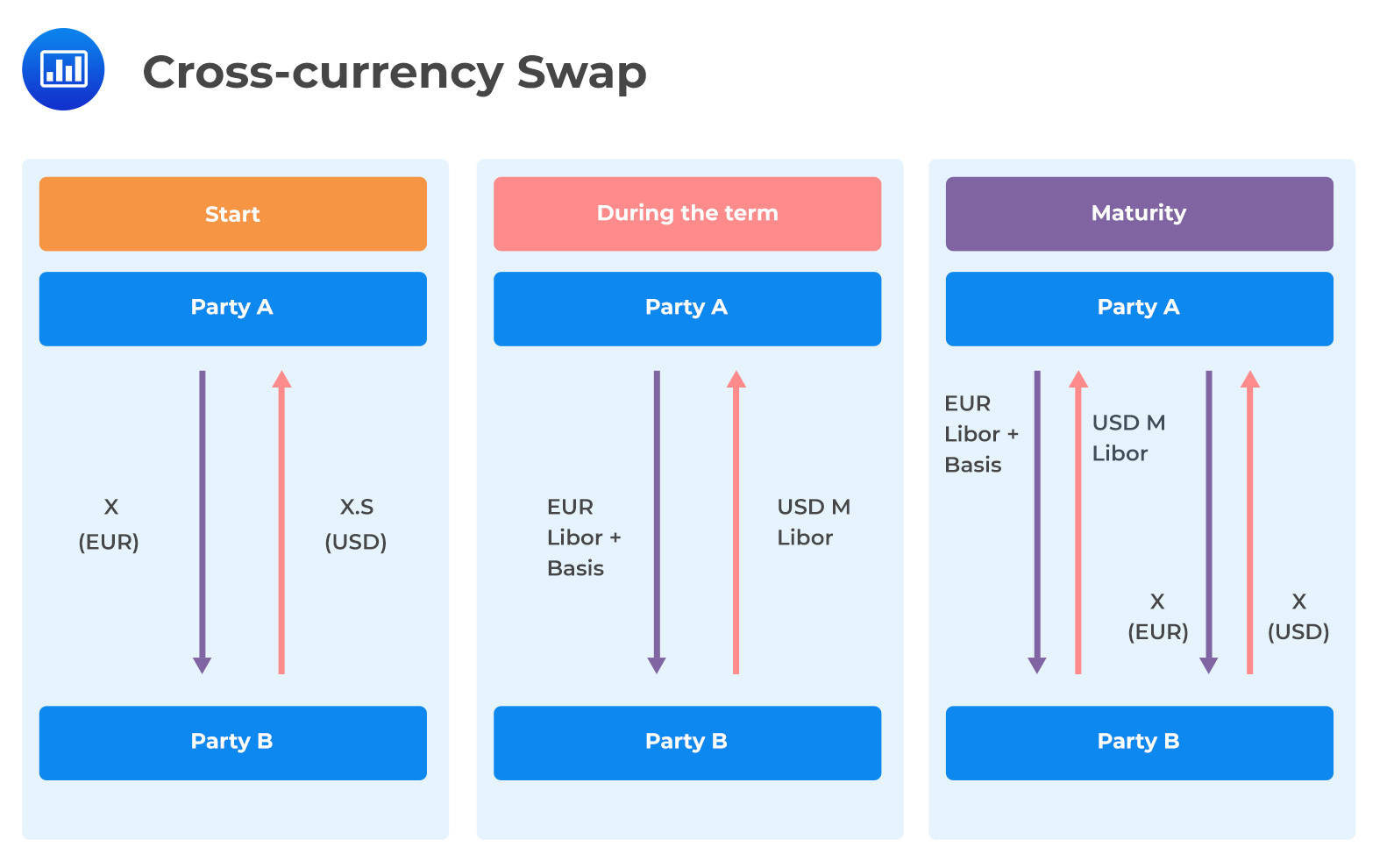

Cross Currency Discount Curve . E.g, you pay 3m usd libor and receive 3m euribor. So that you can build a new eur discount curve that allows you to retrieve cross currency swaps atm quotes. The general way to do this is first take observed market spreads for various tenors, then calibrate a discount curve such that the foreign leg plus the spread at each tenor. It provides the description in the order of the. One possible methodology is to focus on the entity’s functional currency and apply the ccb to the foreign currency’s discount curve. A cross currency swap (ccs) is a financial instrument that allows investors to exchange a set of cashflow. I heard there are two approaches: 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur vs gbp spread. It is a straightforward way to keep. I have made a few tests to. This chapter presents an overview of the construction of the discount curve.

from analystprep.com

One possible methodology is to focus on the entity’s functional currency and apply the ccb to the foreign currency’s discount curve. 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur vs gbp spread. A cross currency swap (ccs) is a financial instrument that allows investors to exchange a set of cashflow. It provides the description in the order of the. The general way to do this is first take observed market spreads for various tenors, then calibrate a discount curve such that the foreign leg plus the spread at each tenor. I heard there are two approaches: This chapter presents an overview of the construction of the discount curve. I have made a few tests to. E.g, you pay 3m usd libor and receive 3m euribor. It is a straightforward way to keep.

Covered Interest Rate Parity Lost Understanding the CrossCurrency

Cross Currency Discount Curve E.g, you pay 3m usd libor and receive 3m euribor. This chapter presents an overview of the construction of the discount curve. E.g, you pay 3m usd libor and receive 3m euribor. One possible methodology is to focus on the entity’s functional currency and apply the ccb to the foreign currency’s discount curve. I have made a few tests to. It is a straightforward way to keep. I heard there are two approaches: The general way to do this is first take observed market spreads for various tenors, then calibrate a discount curve such that the foreign leg plus the spread at each tenor. So that you can build a new eur discount curve that allows you to retrieve cross currency swaps atm quotes. 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur vs gbp spread. It provides the description in the order of the. A cross currency swap (ccs) is a financial instrument that allows investors to exchange a set of cashflow.

From deerpointmacro.substack.com

What the Hell Is A CrossCurrency Basis Swap, And Why Do They Matter? Cross Currency Discount Curve This chapter presents an overview of the construction of the discount curve. E.g, you pay 3m usd libor and receive 3m euribor. I have made a few tests to. One possible methodology is to focus on the entity’s functional currency and apply the ccb to the foreign currency’s discount curve. I heard there are two approaches: A cross currency swap. Cross Currency Discount Curve.

From www.chegg.com

Solved MedStat Unwinds its CrossCurrency Swap. In Cross Currency Discount Curve This chapter presents an overview of the construction of the discount curve. It provides the description in the order of the. I have made a few tests to. 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur vs gbp spread. The general way to do this is first take observed market spreads for. Cross Currency Discount Curve.

From analystprep.com

Covered Interest Rate Parity Lost Understanding the CrossCurrency Cross Currency Discount Curve E.g, you pay 3m usd libor and receive 3m euribor. I heard there are two approaches: A cross currency swap (ccs) is a financial instrument that allows investors to exchange a set of cashflow. One possible methodology is to focus on the entity’s functional currency and apply the ccb to the foreign currency’s discount curve. It provides the description in. Cross Currency Discount Curve.

From open.lib.umn.edu

25.2 Demand, Supply, and Equilibrium in the Money Market Principles Cross Currency Discount Curve A cross currency swap (ccs) is a financial instrument that allows investors to exchange a set of cashflow. It is a straightforward way to keep. 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur vs gbp spread. This chapter presents an overview of the construction of the discount curve. One possible methodology is. Cross Currency Discount Curve.

From efinancemanagement.com

Cross Currency Rate Meaning, Importance, Calculation Cross Currency Discount Curve The general way to do this is first take observed market spreads for various tenors, then calibrate a discount curve such that the foreign leg plus the spread at each tenor. E.g, you pay 3m usd libor and receive 3m euribor. 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur vs gbp spread.. Cross Currency Discount Curve.

From www.clarusft.com

Mechanics of Cross Currency Swaps Cross Currency Discount Curve It is a straightforward way to keep. It provides the description in the order of the. A cross currency swap (ccs) is a financial instrument that allows investors to exchange a set of cashflow. 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur vs gbp spread. This chapter presents an overview of the. Cross Currency Discount Curve.

From bondvigilantes.com

Cross currency basis what is it? And what are the implications Cross Currency Discount Curve A cross currency swap (ccs) is a financial instrument that allows investors to exchange a set of cashflow. E.g, you pay 3m usd libor and receive 3m euribor. The general way to do this is first take observed market spreads for various tenors, then calibrate a discount curve such that the foreign leg plus the spread at each tenor. It. Cross Currency Discount Curve.

From www.researchgate.net

CrossCurrency Basis for Selected Economies Download Scientific Diagram Cross Currency Discount Curve This chapter presents an overview of the construction of the discount curve. The general way to do this is first take observed market spreads for various tenors, then calibrate a discount curve such that the foreign leg plus the spread at each tenor. So that you can build a new eur discount curve that allows you to retrieve cross currency. Cross Currency Discount Curve.

From www.clarusft.com

ISDA SIMM™ in Excel Cross Currency Swaps Cross Currency Discount Curve I heard there are two approaches: One possible methodology is to focus on the entity’s functional currency and apply the ccb to the foreign currency’s discount curve. A cross currency swap (ccs) is a financial instrument that allows investors to exchange a set of cashflow. I have made a few tests to. So that you can build a new eur. Cross Currency Discount Curve.

From ftalphaville.ft.com

Crosscurrency basis, RIP? FT Alphaville Cross Currency Discount Curve This chapter presents an overview of the construction of the discount curve. A cross currency swap (ccs) is a financial instrument that allows investors to exchange a set of cashflow. E.g, you pay 3m usd libor and receive 3m euribor. I have made a few tests to. It provides the description in the order of the. The general way to. Cross Currency Discount Curve.

From www.bis.org

Covered interest parity lost understanding the crosscurrency basis Cross Currency Discount Curve It is a straightforward way to keep. I heard there are two approaches: 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur vs gbp spread. E.g, you pay 3m usd libor and receive 3m euribor. I have made a few tests to. A cross currency swap (ccs) is a financial instrument that allows. Cross Currency Discount Curve.

From www.fibforex123.com

Cross Currency Pair Trading in the Forex Markets Cross Currency Discount Curve The general way to do this is first take observed market spreads for various tenors, then calibrate a discount curve such that the foreign leg plus the spread at each tenor. I heard there are two approaches: 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur vs gbp spread. One possible methodology is. Cross Currency Discount Curve.

From mikejuniperhill.blogspot.com

Path Synthetic Basis Spread Calculation for Shortterm Crosscurrency Cross Currency Discount Curve It provides the description in the order of the. The general way to do this is first take observed market spreads for various tenors, then calibrate a discount curve such that the foreign leg plus the spread at each tenor. 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur vs gbp spread. I. Cross Currency Discount Curve.

From www.optimx.io

Hidden costs in foreign currency bond issuance OptimX Cross Currency Discount Curve I heard there are two approaches: It is a straightforward way to keep. A cross currency swap (ccs) is a financial instrument that allows investors to exchange a set of cashflow. 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur vs gbp spread. So that you can build a new eur discount curve. Cross Currency Discount Curve.

From www.researchgate.net

Murabahabased CrossCurrency Swap. Download Scientific Diagram Cross Currency Discount Curve The general way to do this is first take observed market spreads for various tenors, then calibrate a discount curve such that the foreign leg plus the spread at each tenor. I have made a few tests to. It provides the description in the order of the. This chapter presents an overview of the construction of the discount curve. So. Cross Currency Discount Curve.

From russellinvestments.com

Crosscurrency basis An eventful year, but yearend should be quieter Cross Currency Discount Curve 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur vs gbp spread. It provides the description in the order of the. So that you can build a new eur discount curve that allows you to retrieve cross currency swaps atm quotes. E.g, you pay 3m usd libor and receive 3m euribor. The general. Cross Currency Discount Curve.

From www.fortrade.com

Fortrade Cross Currency Discount Curve A cross currency swap (ccs) is a financial instrument that allows investors to exchange a set of cashflow. This chapter presents an overview of the construction of the discount curve. So that you can build a new eur discount curve that allows you to retrieve cross currency swaps atm quotes. One possible methodology is to focus on the entity’s functional. Cross Currency Discount Curve.

From analystprep.com

Spot Rates and Forward Rates CFA, FRM, and Actuarial Exams Study Notes Cross Currency Discount Curve It is a straightforward way to keep. So that you can build a new eur discount curve that allows you to retrieve cross currency swaps atm quotes. I heard there are two approaches: It provides the description in the order of the. E.g, you pay 3m usd libor and receive 3m euribor. 3m euribor as forward curve, and the discount. Cross Currency Discount Curve.

From www.artedelcambio.com

Arte del Cambio QE and Cross Currency Basis Swaps Cross Currency Discount Curve It provides the description in the order of the. A cross currency swap (ccs) is a financial instrument that allows investors to exchange a set of cashflow. This chapter presents an overview of the construction of the discount curve. So that you can build a new eur discount curve that allows you to retrieve cross currency swaps atm quotes. It. Cross Currency Discount Curve.

From blog.deriscope.com

Currency Swaps and Basis Curves in Excel Resources Cross Currency Discount Curve I have made a few tests to. So that you can build a new eur discount curve that allows you to retrieve cross currency swaps atm quotes. One possible methodology is to focus on the entity’s functional currency and apply the ccb to the foreign currency’s discount curve. It is a straightforward way to keep. The general way to do. Cross Currency Discount Curve.

From nakisa.org

Cross Currency Basis Swaps Explained Ramin Nakisa Cross Currency Discount Curve The general way to do this is first take observed market spreads for various tenors, then calibrate a discount curve such that the foreign leg plus the spread at each tenor. I have made a few tests to. It provides the description in the order of the. 3m euribor as forward curve, and the discount curve should be eur ios. Cross Currency Discount Curve.

From www.daytrading.com

Cross Currency Basis Swaps Hedging FX in a Global Portfolio Cross Currency Discount Curve E.g, you pay 3m usd libor and receive 3m euribor. It is a straightforward way to keep. The general way to do this is first take observed market spreads for various tenors, then calibrate a discount curve such that the foreign leg plus the spread at each tenor. So that you can build a new eur discount curve that allows. Cross Currency Discount Curve.

From www.stockgro.club

Understanding cross currency swap with an example Cross Currency Discount Curve A cross currency swap (ccs) is a financial instrument that allows investors to exchange a set of cashflow. E.g, you pay 3m usd libor and receive 3m euribor. I heard there are two approaches: 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur vs gbp spread. This chapter presents an overview of the. Cross Currency Discount Curve.

From www.forexlive.com

It's all about the crosscurrency basis today Cross Currency Discount Curve A cross currency swap (ccs) is a financial instrument that allows investors to exchange a set of cashflow. This chapter presents an overview of the construction of the discount curve. I have made a few tests to. One possible methodology is to focus on the entity’s functional currency and apply the ccb to the foreign currency’s discount curve. 3m euribor. Cross Currency Discount Curve.

From blog.deriscope.com

Yield Curve Resources Cross Currency Discount Curve It provides the description in the order of the. One possible methodology is to focus on the entity’s functional currency and apply the ccb to the foreign currency’s discount curve. So that you can build a new eur discount curve that allows you to retrieve cross currency swaps atm quotes. 3m euribor as forward curve, and the discount curve should. Cross Currency Discount Curve.

From analystprep.com

Illustration of the EE for crosscurrency swaps of different maturities Cross Currency Discount Curve The general way to do this is first take observed market spreads for various tenors, then calibrate a discount curve such that the foreign leg plus the spread at each tenor. So that you can build a new eur discount curve that allows you to retrieve cross currency swaps atm quotes. This chapter presents an overview of the construction of. Cross Currency Discount Curve.

From www.semanticscholar.org

Figure 1 from Dynamic Crosscurrency Linkages of the LIBOROIS Spreads Cross Currency Discount Curve I heard there are two approaches: E.g, you pay 3m usd libor and receive 3m euribor. One possible methodology is to focus on the entity’s functional currency and apply the ccb to the foreign currency’s discount curve. This chapter presents an overview of the construction of the discount curve. I have made a few tests to. It provides the description. Cross Currency Discount Curve.

From mfxsolutions.com

Cross Currency Swaps MFX Currency Risk Solutions Cross Currency Discount Curve This chapter presents an overview of the construction of the discount curve. One possible methodology is to focus on the entity’s functional currency and apply the ccb to the foreign currency’s discount curve. 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur vs gbp spread. I have made a few tests to. I. Cross Currency Discount Curve.

From thediversifiedtrader.com

Major Cross Currency Pairs The Diversified Trader Cross Currency Discount Curve 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur vs gbp spread. It provides the description in the order of the. The general way to do this is first take observed market spreads for various tenors, then calibrate a discount curve such that the foreign leg plus the spread at each tenor. It. Cross Currency Discount Curve.

From www.daytrading.com

Cross Currency Basis Swaps Hedging FX in a Global Portfolio Cross Currency Discount Curve One possible methodology is to focus on the entity’s functional currency and apply the ccb to the foreign currency’s discount curve. 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur vs gbp spread. I have made a few tests to. E.g, you pay 3m usd libor and receive 3m euribor. A cross currency. Cross Currency Discount Curve.

From www.artedelcambio.com

Arte del Cambio QE and Cross Currency Basis Swaps Cross Currency Discount Curve E.g, you pay 3m usd libor and receive 3m euribor. I heard there are two approaches: So that you can build a new eur discount curve that allows you to retrieve cross currency swaps atm quotes. It is a straightforward way to keep. It provides the description in the order of the. 3m euribor as forward curve, and the discount. Cross Currency Discount Curve.

From www.clarusft.com

ISDA SIMM™ in Excel Cross Currency Swaps Cross Currency Discount Curve E.g, you pay 3m usd libor and receive 3m euribor. It is a straightforward way to keep. I heard there are two approaches: One possible methodology is to focus on the entity’s functional currency and apply the ccb to the foreign currency’s discount curve. 3m euribor as forward curve, and the discount curve should be eur ios adjusted with eur. Cross Currency Discount Curve.

From www.slideshare.net

Cross currency chart Cross Currency Discount Curve One possible methodology is to focus on the entity’s functional currency and apply the ccb to the foreign currency’s discount curve. The general way to do this is first take observed market spreads for various tenors, then calibrate a discount curve such that the foreign leg plus the spread at each tenor. It is a straightforward way to keep. I. Cross Currency Discount Curve.

From www.artedelcambio.com

Arte del Cambio QE and Cross Currency Basis Swaps Cross Currency Discount Curve So that you can build a new eur discount curve that allows you to retrieve cross currency swaps atm quotes. I have made a few tests to. It provides the description in the order of the. This chapter presents an overview of the construction of the discount curve. I heard there are two approaches: One possible methodology is to focus. Cross Currency Discount Curve.

From blog.deriv.com

Understanding crosscurrency pairs Deriv Blog Cross Currency Discount Curve E.g, you pay 3m usd libor and receive 3m euribor. It is a straightforward way to keep. I have made a few tests to. I heard there are two approaches: This chapter presents an overview of the construction of the discount curve. A cross currency swap (ccs) is a financial instrument that allows investors to exchange a set of cashflow.. Cross Currency Discount Curve.