Boot Definition In Accounting . Cash boot is permitted to be a part of a. In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. The boot is the cash or other asset that is added in order to make the worth of the goods traded equal. Boot is “unlike” property received in an exchange. Boot received is the money or the fair market value of other property received by the taxpayer in an exchange. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. Cash, personal property, or a reduction in the mortgage owed.

from www.youtube.com

The boot is the cash or other asset that is added in order to make the worth of the goods traded equal. In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. Boot is “unlike” property received in an exchange. Boot received is the money or the fair market value of other property received by the taxpayer in an exchange. Cash, personal property, or a reduction in the mortgage owed. Cash boot is permitted to be a part of a.

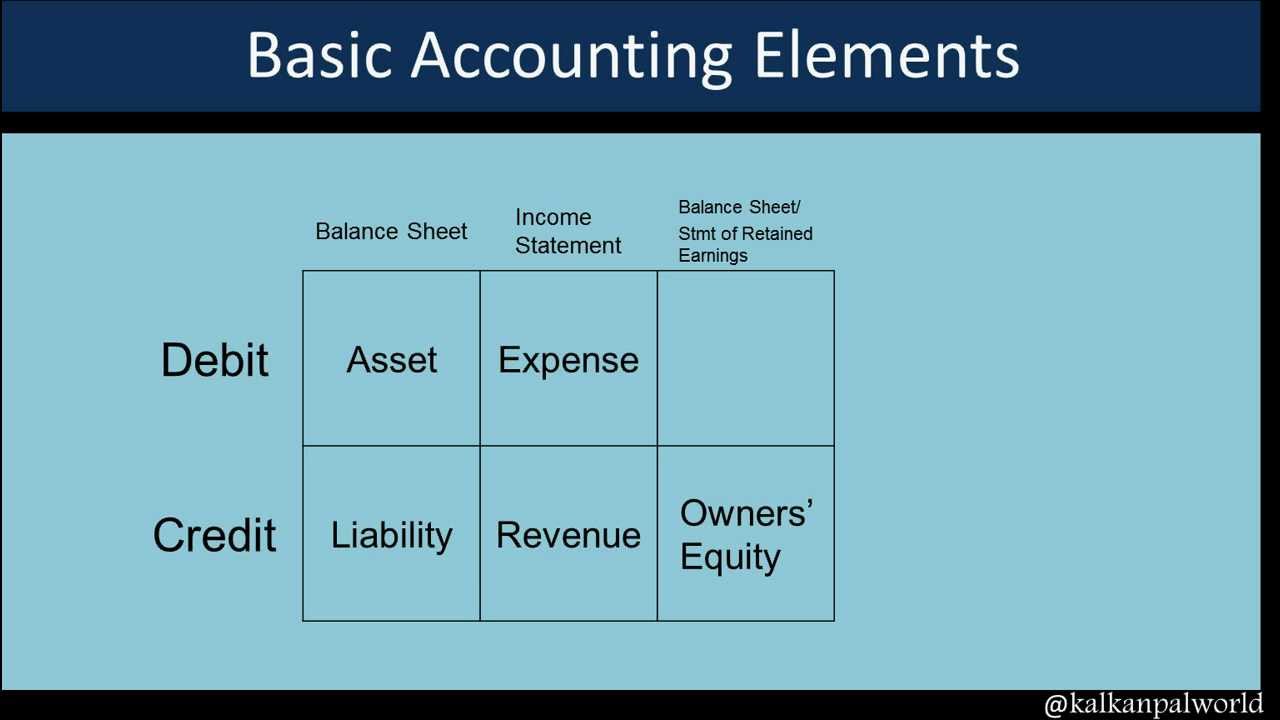

Basic Accounting Credit Debit YouTube

Boot Definition In Accounting In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. Boot is “unlike” property received in an exchange. The boot is the cash or other asset that is added in order to make the worth of the goods traded equal. Cash boot is permitted to be a part of a. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. Cash, personal property, or a reduction in the mortgage owed. Boot received is the money or the fair market value of other property received by the taxpayer in an exchange.

From pediaa.com

Difference Between UEFI and Legacy Boot Boot Definition In Accounting The boot is the cash or other asset that is added in order to make the worth of the goods traded equal. Cash, personal property, or a reduction in the mortgage owed. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. Cash. Boot Definition In Accounting.

From www.akounto.com

Assets in Accounting Definition, Types & Example Akounto Boot Definition In Accounting The boot is the cash or other asset that is added in order to make the worth of the goods traded equal. In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. Cash, personal property, or a reduction in the mortgage owed. Cash boot is permitted to be a part of. Boot Definition In Accounting.

From www.1031crowdfunding.com

Mortgage Boot 1031 Exchange Guide Debt Reduction Principle Boot Definition In Accounting In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. The boot is the cash or other asset that is added in order to. Boot Definition In Accounting.

From informacionpublica.svet.gob.gt

What Are Accounting Methods? Definition, Types, And Example Boot Definition In Accounting Boot received is the money or the fair market value of other property received by the taxpayer in an exchange. Cash boot is permitted to be a part of a. Cash, personal property, or a reduction in the mortgage owed. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition. Boot Definition In Accounting.

From www.slideserve.com

PPT Definitions of Accounting PowerPoint Presentation, free download Boot Definition In Accounting Boot received is the money or the fair market value of other property received by the taxpayer in an exchange. Cash, personal property, or a reduction in the mortgage owed. In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. Cash boot is permitted to be a part of a. In. Boot Definition In Accounting.

From techterms.com

Boot Sequence Definition What is a boot sequence? Boot Definition In Accounting Cash, personal property, or a reduction in the mortgage owed. Boot is “unlike” property received in an exchange. The boot is the cash or other asset that is added in order to make the worth of the goods traded equal. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition. Boot Definition In Accounting.

From tutorstips.com

Accounting Ratios Meaning and Definition Tutor's Tips Boot Definition In Accounting Cash boot is permitted to be a part of a. In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. The boot is the cash or other asset that is added in order to make the worth of the goods traded equal. In financial transactions, 'boot' refers to any form of. Boot Definition In Accounting.

From wirtschaftslexikon.gabler.de

BOOT • Definition Gabler Wirtschaftslexikon Boot Definition In Accounting In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. Boot is “unlike” property received in an exchange. Cash boot is permitted to be a part of a. In financial accounting, 'boot' refers to the additional value received in a transaction involving the. Boot Definition In Accounting.

From synder.com

What is DoubleEntry Accounting Double Entry Accounting Guide 2024 Boot Definition In Accounting Boot received is the money or the fair market value of other property received by the taxpayer in an exchange. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. The boot is the cash or other asset that is added in order. Boot Definition In Accounting.

From www.investopedia.com

Accounting Standard Definition How It Works Boot Definition In Accounting In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. Boot received is the money or the fair market value of other property received by the taxpayer in an exchange. Boot is “unlike” property received in an exchange. Cash, personal property, or a reduction in the mortgage owed. Cash boot is. Boot Definition In Accounting.

From vimeo.com

Boot Accounting.3Instructions on Importing Excel Spreadsheet Boot Definition In Accounting Cash, personal property, or a reduction in the mortgage owed. Boot is “unlike” property received in an exchange. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. In financial accounting, 'boot' refers to the additional value received in a transaction involving the. Boot Definition In Accounting.

From mi-pro.co.uk

What Are Accounting Methods? Definition, Types, and Example, true to Boot Definition In Accounting In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. Cash, personal property, or a reduction in the mortgage owed. Boot received is the money or the fair market value of other property received by the taxpayer in an exchange. The boot is the cash or other asset that is added. Boot Definition In Accounting.

From theinvestorsbook.com

What are Accounting Principles? definition, GAAP and basic accounting Boot Definition In Accounting In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. Boot is “unlike” property received in an exchange. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. Cash, personal property, or a reduction. Boot Definition In Accounting.

From www.youtube.com

Boot what is BOOT definition YouTube Boot Definition In Accounting Cash, personal property, or a reduction in the mortgage owed. In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. Cash boot is permitted to be a part of a. Boot is “unlike” property received in an exchange. The boot is the cash or other asset that is added in order. Boot Definition In Accounting.

From financialfalconet.com

Types of Adjusting Entries with Examples Financial Boot Definition In Accounting In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. Boot received is the money or the fair market value of other property received by the taxpayer in an exchange. Cash, personal property, or a reduction in the mortgage owed. Boot is “unlike”. Boot Definition In Accounting.

From edukedar.com

Basics of Accounting Definition, Objective, Scope, Process & Advantages Boot Definition In Accounting Boot is “unlike” property received in an exchange. In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. Boot received is the money or the fair market value of other property received by the taxpayer in an exchange. In financial transactions, 'boot' refers to any form of additional consideration received by. Boot Definition In Accounting.

From www.researchgate.net

Definition of the upper boot construction of the boot samples used in Boot Definition In Accounting The boot is the cash or other asset that is added in order to make the worth of the goods traded equal. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. Cash boot is permitted to be a part of a. In. Boot Definition In Accounting.

From wirtschaftslexikon.gabler.de

BOOT • Definition Gabler Wirtschaftslexikon Boot Definition In Accounting Boot received is the money or the fair market value of other property received by the taxpayer in an exchange. In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. Boot is “unlike” property received in an exchange. In financial transactions, 'boot' refers to any form of additional consideration received by. Boot Definition In Accounting.

From www.youtube.com

Basic Accounting Credit Debit YouTube Boot Definition In Accounting In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. Boot received is the money or the fair market value of other property received. Boot Definition In Accounting.

From www.gbu-presnenskij.ru

What Are Accounting Methods? Definition, Types, And Example, 40 OFF Boot Definition In Accounting The boot is the cash or other asset that is added in order to make the worth of the goods traded equal. Cash, personal property, or a reduction in the mortgage owed. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. Boot. Boot Definition In Accounting.

From www.youtube.com

Pronunciation of Boot Definition of Boot YouTube Boot Definition In Accounting Cash, personal property, or a reduction in the mortgage owed. In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. Boot is “unlike” property received in an exchange. Boot received is the money or the fair market value of other property received by the taxpayer in an exchange. In financial transactions,. Boot Definition In Accounting.

From wirtschaftslexikon.gabler.de

BOOT • Definition Gabler Wirtschaftslexikon Boot Definition In Accounting In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. Boot is “unlike” property received in an exchange. Boot received is the money or the fair market value of other property received by the taxpayer in an exchange. Cash boot is permitted to be a part of a. Cash, personal property,. Boot Definition In Accounting.

From www.scribd.com

Accounting Terms Basic Definitions Debits And Credits Expense Boot Definition In Accounting Cash boot is permitted to be a part of a. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. Boot is “unlike” property received in an exchange. In financial accounting, 'boot' refers to the additional value received in a transaction involving the. Boot Definition In Accounting.

From www.vrogue.co

What Is Financial Accounting Definition Principles Ex vrogue.co Boot Definition In Accounting Cash, personal property, or a reduction in the mortgage owed. The boot is the cash or other asset that is added in order to make the worth of the goods traded equal. Cash boot is permitted to be a part of a. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger. Boot Definition In Accounting.

From www.investopedia.com

Boot What it is, How it Works in Accounting Boot Definition In Accounting Boot is “unlike” property received in an exchange. Cash, personal property, or a reduction in the mortgage owed. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. Boot received is the money or the fair market value of other property received by. Boot Definition In Accounting.

From www.studocu.com

BCA UNIT II Text boot .UNIT II Accounting Cycle The accounting Boot Definition In Accounting In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. Boot received is the money or the fair market value of other property received. Boot Definition In Accounting.

From quickbooks.intuit.com

What is accounting Types, definition, and FAQs QuickBooks Boot Definition In Accounting The boot is the cash or other asset that is added in order to make the worth of the goods traded equal. Boot is “unlike” property received in an exchange. In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. In financial transactions, 'boot' refers to any form of additional consideration. Boot Definition In Accounting.

From www.investopedia.com

Accounting Entity Definition, Types, and Examples Boot Definition In Accounting The boot is the cash or other asset that is added in order to make the worth of the goods traded equal. Cash boot is permitted to be a part of a. Cash, personal property, or a reduction in the mortgage owed. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger. Boot Definition In Accounting.

From www.freshbooks.com

What Is The Accounting Cycle? Definition, Steps & Example Guide Boot Definition In Accounting In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. Boot received is the money or the fair market value of other property received. Boot Definition In Accounting.

From wordstodescribesomeone.com

Boot definition Boot meaning words to describe someone Boot Definition In Accounting Boot is “unlike” property received in an exchange. In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. Cash, personal property, or a reduction in the mortgage owed. The boot is the cash or other asset that is added in order to make the worth of the goods traded equal. In. Boot Definition In Accounting.

From info-savvy.com

What is the Booting Process? Infosavvy Security and IT Management Boot Definition In Accounting Cash, personal property, or a reduction in the mortgage owed. Cash boot is permitted to be a part of a. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. Boot is “unlike” property received in an exchange. Boot received is the money. Boot Definition In Accounting.

From quickbooks.intuit.com

Accounting definition How to master the basics + 3 (free) spreadsheets Boot Definition In Accounting In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. Boot received is the money or the fair market value of other property received by the taxpayer in an exchange. Cash, personal property, or a reduction in the mortgage owed. Cash boot is permitted to be a part of a. In. Boot Definition In Accounting.

From www.youtube.com

The boot • definition of THE BOOT YouTube Boot Definition In Accounting Cash boot is permitted to be a part of a. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. Boot is “unlike” property received in an exchange. The boot is the cash or other asset that is added in order to make. Boot Definition In Accounting.

From www.youtube.com

What is Spring Boot? Definition and basic thoughts YouTube Boot Definition In Accounting Cash, personal property, or a reduction in the mortgage owed. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that is not in the form of. Boot is “unlike” property received in an exchange. Cash boot is permitted to be a part of a. Boot received is the money. Boot Definition In Accounting.

From www.lifewire.com

What Is Boot Sequence? (Boot Sequence/Order Definition) Boot Definition In Accounting Cash, personal property, or a reduction in the mortgage owed. Cash boot is permitted to be a part of a. In financial accounting, 'boot' refers to the additional value received in a transaction involving the exchange of assets, typically. In financial transactions, 'boot' refers to any form of additional consideration received by a party in a merger or acquisition that. Boot Definition In Accounting.