Fixed Cost Definition Economics Quizlet . In accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the level of goods or services produced by. A fixed cost is a business cost that is unrelated to output. They can also be referred to as ‘indirect costs’. A fixed cost is a business expense that normally doesn’t change with an increase or decrease in the number of goods and services produced or sold by the business. They are incurred regardless of how much a business. What is a fixed cost? A cost that does not change of goods is produced. Fixed costs are expenses that do not change with the level of production or output. Whatever the output fixed costs (fc) remains constant at £300. Fixed costs are costs independent of the size of production. Cost that rises or falls depending on the quantity produced. They remain constant and fixed whether or not.

from boycewire.com

What is a fixed cost? Cost that rises or falls depending on the quantity produced. Fixed costs are expenses that do not change with the level of production or output. In accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the level of goods or services produced by. Fixed costs are costs independent of the size of production. Whatever the output fixed costs (fc) remains constant at £300. A cost that does not change of goods is produced. A fixed cost is a business expense that normally doesn’t change with an increase or decrease in the number of goods and services produced or sold by the business. They are incurred regardless of how much a business. They can also be referred to as ‘indirect costs’.

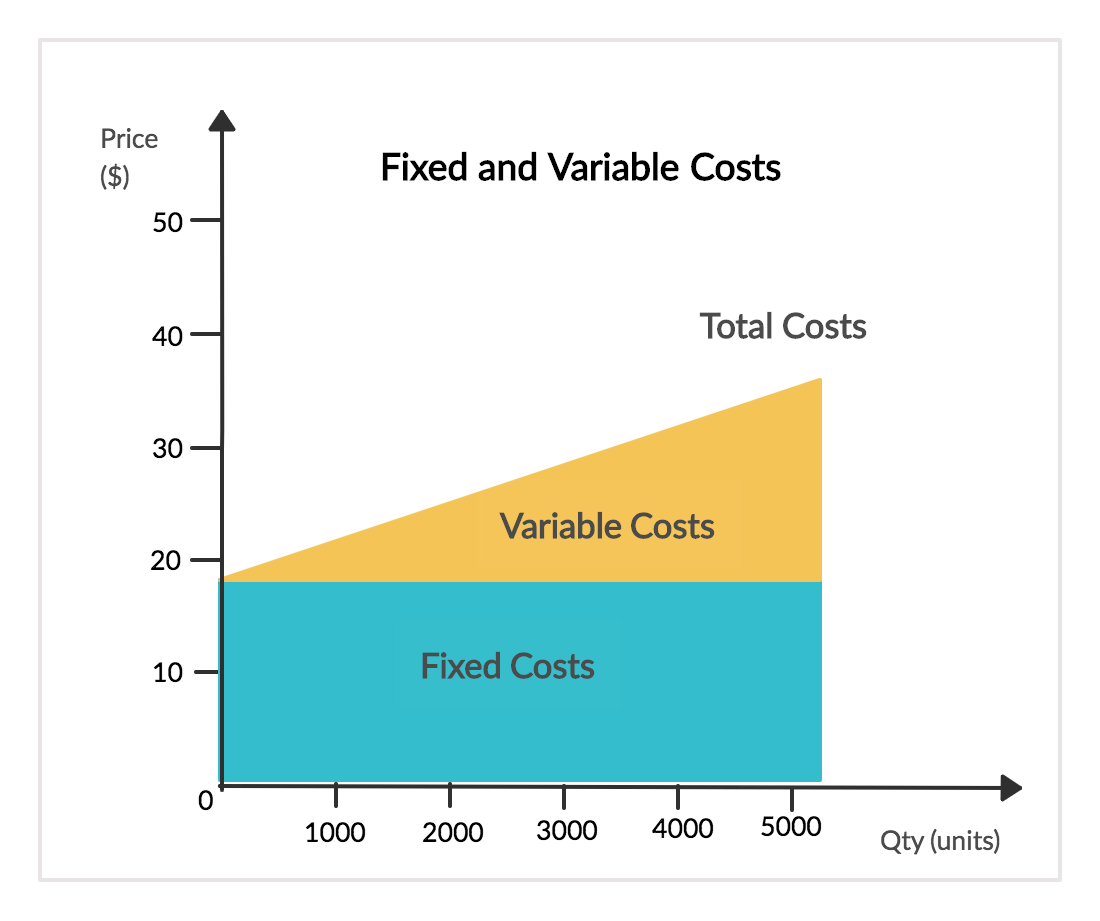

Fixed Costs Definition

Fixed Cost Definition Economics Quizlet Whatever the output fixed costs (fc) remains constant at £300. Whatever the output fixed costs (fc) remains constant at £300. A cost that does not change of goods is produced. In accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the level of goods or services produced by. A fixed cost is a business cost that is unrelated to output. Fixed costs are costs independent of the size of production. A fixed cost is a business expense that normally doesn’t change with an increase or decrease in the number of goods and services produced or sold by the business. They are incurred regardless of how much a business. They can also be referred to as ‘indirect costs’. Cost that rises or falls depending on the quantity produced. Fixed costs are expenses that do not change with the level of production or output. They remain constant and fixed whether or not. What is a fixed cost?

From www.investopedia.com

Fixed Cost What It Is and How It’s Used in Business Fixed Cost Definition Economics Quizlet They remain constant and fixed whether or not. What is a fixed cost? A cost that does not change of goods is produced. A fixed cost is a business cost that is unrelated to output. A fixed cost is a business expense that normally doesn’t change with an increase or decrease in the number of goods and services produced or. Fixed Cost Definition Economics Quizlet.

From www.superfastcpa.com

What is a Fixed Cost? Fixed Cost Definition Economics Quizlet A fixed cost is a business cost that is unrelated to output. Fixed costs are expenses that do not change with the level of production or output. A fixed cost is a business expense that normally doesn’t change with an increase or decrease in the number of goods and services produced or sold by the business. Whatever the output fixed. Fixed Cost Definition Economics Quizlet.

From quickonomics.com

Average Fixed Cost Definition Quickonomics Fixed Cost Definition Economics Quizlet Whatever the output fixed costs (fc) remains constant at £300. A fixed cost is a business cost that is unrelated to output. In accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the level of goods or services produced by. Fixed costs are costs independent of the size. Fixed Cost Definition Economics Quizlet.

From napkinfinance.com

What is Fixed Cost vs. Variable Cost? Napkin Finance Fixed Cost Definition Economics Quizlet In accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the level of goods or services produced by. A fixed cost is a business expense that normally doesn’t change with an increase or decrease in the number of goods and services produced or sold by the business. A. Fixed Cost Definition Economics Quizlet.

From marketbusinessnews.com

What are fixed costs? Definition and meaning Market Business News Fixed Cost Definition Economics Quizlet They are incurred regardless of how much a business. A fixed cost is a business expense that normally doesn’t change with an increase or decrease in the number of goods and services produced or sold by the business. What is a fixed cost? They can also be referred to as ‘indirect costs’. Cost that rises or falls depending on the. Fixed Cost Definition Economics Quizlet.

From www.akounto.com

Fixed Cost Definition, Calculation & Examples Akounto Fixed Cost Definition Economics Quizlet In accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the level of goods or services produced by. They remain constant and fixed whether or not. Fixed costs are costs independent of the size of production. A cost that does not change of goods is produced. Fixed costs. Fixed Cost Definition Economics Quizlet.

From www.slideserve.com

PPT Cost Concepts in Economics PowerPoint Presentation, free download Fixed Cost Definition Economics Quizlet They are incurred regardless of how much a business. A fixed cost is a business cost that is unrelated to output. A fixed cost is a business expense that normally doesn’t change with an increase or decrease in the number of goods and services produced or sold by the business. Whatever the output fixed costs (fc) remains constant at £300.. Fixed Cost Definition Economics Quizlet.

From economicsexplainer.com

10 Different Types of Costs Explained with Examples Fixed Cost Definition Economics Quizlet What is a fixed cost? A cost that does not change of goods is produced. Cost that rises or falls depending on the quantity produced. They can also be referred to as ‘indirect costs’. Fixed costs are expenses that do not change with the level of production or output. A fixed cost is a business cost that is unrelated to. Fixed Cost Definition Economics Quizlet.

From sendpulse.ng

What is an Average Fixed Cost Basics Definition SendPulse Fixed Cost Definition Economics Quizlet They can also be referred to as ‘indirect costs’. What is a fixed cost? They remain constant and fixed whether or not. A cost that does not change of goods is produced. Cost that rises or falls depending on the quantity produced. Fixed costs are expenses that do not change with the level of production or output. Whatever the output. Fixed Cost Definition Economics Quizlet.

From quizlet.com

Average Cost Curve Diagram Quizlet Fixed Cost Definition Economics Quizlet What is a fixed cost? Fixed costs are costs independent of the size of production. In accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the level of goods or services produced by. They are incurred regardless of how much a business. A fixed cost is a business. Fixed Cost Definition Economics Quizlet.

From worldmartech.com

Fixed Cost What It Is & How to Calculate It World MarTech Fixed Cost Definition Economics Quizlet In accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the level of goods or services produced by. They remain constant and fixed whether or not. A cost that does not change of goods is produced. A fixed cost is a business expense that normally doesn’t change with. Fixed Cost Definition Economics Quizlet.

From learnbusinessconcepts.com

Fixed Cost Explanation, Formula, Calculation, and Examples Fixed Cost Definition Economics Quizlet They can also be referred to as ‘indirect costs’. Fixed costs are expenses that do not change with the level of production or output. A fixed cost is a business expense that normally doesn’t change with an increase or decrease in the number of goods and services produced or sold by the business. They are incurred regardless of how much. Fixed Cost Definition Economics Quizlet.

From www.pedigogy.com

Fixed and Variable Costs Pedigogy Fixed Cost Definition Economics Quizlet Fixed costs are expenses that do not change with the level of production or output. A cost that does not change of goods is produced. In accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the level of goods or services produced by. A fixed cost is a. Fixed Cost Definition Economics Quizlet.

From boycewire.com

Fixed Costs Definition Fixed Cost Definition Economics Quizlet In accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the level of goods or services produced by. A cost that does not change of goods is produced. They remain constant and fixed whether or not. Fixed costs are costs independent of the size of production. A fixed. Fixed Cost Definition Economics Quizlet.

From tutorstips.com

Difference between Fixed Cost and Variable Cost Tutor's Tips Fixed Cost Definition Economics Quizlet A fixed cost is a business cost that is unrelated to output. Fixed costs are expenses that do not change with the level of production or output. A cost that does not change of goods is produced. In accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. Fixed Cost Definition Economics Quizlet.

From efinancemanagement.com

Fixed Cost What It Is And What's Its Importance? Fixed Cost Definition Economics Quizlet Whatever the output fixed costs (fc) remains constant at £300. They are incurred regardless of how much a business. A fixed cost is a business cost that is unrelated to output. Cost that rises or falls depending on the quantity produced. They remain constant and fixed whether or not. Fixed costs are expenses that do not change with the level. Fixed Cost Definition Economics Quizlet.

From www.marketing91.com

Average Fixed Cost Definition, Formula and Examples Marketing91 Fixed Cost Definition Economics Quizlet A fixed cost is a business expense that normally doesn’t change with an increase or decrease in the number of goods and services produced or sold by the business. A cost that does not change of goods is produced. Fixed costs are costs independent of the size of production. They are incurred regardless of how much a business. What is. Fixed Cost Definition Economics Quizlet.

From hxefncvcp.blob.core.windows.net

Fixed And Variable Costs Quizlet at Petra Vaughn blog Fixed Cost Definition Economics Quizlet What is a fixed cost? They remain constant and fixed whether or not. A cost that does not change of goods is produced. They can also be referred to as ‘indirect costs’. A fixed cost is a business cost that is unrelated to output. Whatever the output fixed costs (fc) remains constant at £300. Fixed costs are expenses that do. Fixed Cost Definition Economics Quizlet.

From quizlet.com

In the earlier example, the fixed costs are split 4 million Quizlet Fixed Cost Definition Economics Quizlet They remain constant and fixed whether or not. They can also be referred to as ‘indirect costs’. What is a fixed cost? Whatever the output fixed costs (fc) remains constant at £300. Fixed costs are expenses that do not change with the level of production or output. They are incurred regardless of how much a business. In accounting and economics,. Fixed Cost Definition Economics Quizlet.

From quizlet.com

Business Sales, Revenue and Costs Diagram Quizlet Fixed Cost Definition Economics Quizlet A cost that does not change of goods is produced. Cost that rises or falls depending on the quantity produced. A fixed cost is a business cost that is unrelated to output. They can also be referred to as ‘indirect costs’. Whatever the output fixed costs (fc) remains constant at £300. In accounting and economics, fixed costs, also known as. Fixed Cost Definition Economics Quizlet.

From www.educba.com

Fixed Cost Vs Variable Cost Top 12 Key Differences & Examples Fixed Cost Definition Economics Quizlet Fixed costs are expenses that do not change with the level of production or output. They remain constant and fixed whether or not. A cost that does not change of goods is produced. Cost that rises or falls depending on the quantity produced. What is a fixed cost? Fixed costs are costs independent of the size of production. Whatever the. Fixed Cost Definition Economics Quizlet.

From www.youtube.com

Fixed cost — definition of FIXED COST YouTube Fixed Cost Definition Economics Quizlet What is a fixed cost? In accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the level of goods or services produced by. A fixed cost is a business cost that is unrelated to output. A cost that does not change of goods is produced. They remain constant. Fixed Cost Definition Economics Quizlet.

From hxefncvcp.blob.core.windows.net

Fixed And Variable Costs Quizlet at Petra Vaughn blog Fixed Cost Definition Economics Quizlet Cost that rises or falls depending on the quantity produced. They remain constant and fixed whether or not. They are incurred regardless of how much a business. Fixed costs are expenses that do not change with the level of production or output. Whatever the output fixed costs (fc) remains constant at £300. A cost that does not change of goods. Fixed Cost Definition Economics Quizlet.

From www.studypool.com

SOLUTION Fixed costs definition and formulas for calculating them Fixed Cost Definition Economics Quizlet They are incurred regardless of how much a business. A fixed cost is a business cost that is unrelated to output. They can also be referred to as ‘indirect costs’. Cost that rises or falls depending on the quantity produced. A fixed cost is a business expense that normally doesn’t change with an increase or decrease in the number of. Fixed Cost Definition Economics Quizlet.

From www.1099cafe.com

What is a Fixed Cost Variable vs Fixed Expenses — 1099 Cafe Fixed Cost Definition Economics Quizlet Fixed costs are costs independent of the size of production. In accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the level of goods or services produced by. They remain constant and fixed whether or not. A cost that does not change of goods is produced. Cost that. Fixed Cost Definition Economics Quizlet.

From www.studypool.com

SOLUTION Fixed costs definition and formulas for calculating them Fixed Cost Definition Economics Quizlet A cost that does not change of goods is produced. In accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the level of goods or services produced by. A fixed cost is a business cost that is unrelated to output. Whatever the output fixed costs (fc) remains constant. Fixed Cost Definition Economics Quizlet.

From giollplui.blob.core.windows.net

What Are Examples Of Fixed Costs And Variable Costs For A Farm Quizlet Fixed Cost Definition Economics Quizlet A fixed cost is a business cost that is unrelated to output. In accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the level of goods or services produced by. They remain constant and fixed whether or not. A fixed cost is a business expense that normally doesn’t. Fixed Cost Definition Economics Quizlet.

From quizizz.com

Fixed and Variable costs Business Quizizz Fixed Cost Definition Economics Quizlet Fixed costs are costs independent of the size of production. They remain constant and fixed whether or not. Whatever the output fixed costs (fc) remains constant at £300. A cost that does not change of goods is produced. They are incurred regardless of how much a business. A fixed cost is a business expense that normally doesn’t change with an. Fixed Cost Definition Economics Quizlet.

From quizlet.com

Microeconomics Chapter 4, 5, 6 sample questions Diagram Quizlet Fixed Cost Definition Economics Quizlet Fixed costs are costs independent of the size of production. Cost that rises or falls depending on the quantity produced. What is a fixed cost? A fixed cost is a business expense that normally doesn’t change with an increase or decrease in the number of goods and services produced or sold by the business. They remain constant and fixed whether. Fixed Cost Definition Economics Quizlet.

From wealthnation.io

How to Balance Fixed Expenses with Variable Costs Wealth Nation Fixed Cost Definition Economics Quizlet Whatever the output fixed costs (fc) remains constant at £300. They can also be referred to as ‘indirect costs’. A fixed cost is a business cost that is unrelated to output. A cost that does not change of goods is produced. They are incurred regardless of how much a business. They remain constant and fixed whether or not. Cost that. Fixed Cost Definition Economics Quizlet.

From www.tutor2u.net

Explaining Fixed and Variable Costs of Production tutor2u Economics Fixed Cost Definition Economics Quizlet They remain constant and fixed whether or not. A cost that does not change of goods is produced. What is a fixed cost? Whatever the output fixed costs (fc) remains constant at £300. A fixed cost is a business cost that is unrelated to output. Cost that rises or falls depending on the quantity produced. Fixed costs are expenses that. Fixed Cost Definition Economics Quizlet.

From quizlet.com

Find the cost function for each marginal cost function. C'(x Quizlet Fixed Cost Definition Economics Quizlet Whatever the output fixed costs (fc) remains constant at £300. They are incurred regardless of how much a business. A fixed cost is a business expense that normally doesn’t change with an increase or decrease in the number of goods and services produced or sold by the business. Fixed costs are costs independent of the size of production. Cost that. Fixed Cost Definition Economics Quizlet.

From investinganswers.com

Fixed Costs Example & Definition InvestingAnswers Fixed Cost Definition Economics Quizlet They can also be referred to as ‘indirect costs’. They remain constant and fixed whether or not. Cost that rises or falls depending on the quantity produced. Whatever the output fixed costs (fc) remains constant at £300. A fixed cost is a business cost that is unrelated to output. Fixed costs are costs independent of the size of production. In. Fixed Cost Definition Economics Quizlet.

From agiled.app

Differences Between Fixed Cost and Variable Cost Fixed Cost Definition Economics Quizlet A fixed cost is a business expense that normally doesn’t change with an increase or decrease in the number of goods and services produced or sold by the business. Cost that rises or falls depending on the quantity produced. A fixed cost is a business cost that is unrelated to output. They remain constant and fixed whether or not. Fixed. Fixed Cost Definition Economics Quizlet.

From quizlet.com

Is it True or False? When fixed costs are positive, the ave Quizlet Fixed Cost Definition Economics Quizlet Fixed costs are expenses that do not change with the level of production or output. They remain constant and fixed whether or not. Cost that rises or falls depending on the quantity produced. A cost that does not change of goods is produced. In accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses. Fixed Cost Definition Economics Quizlet.