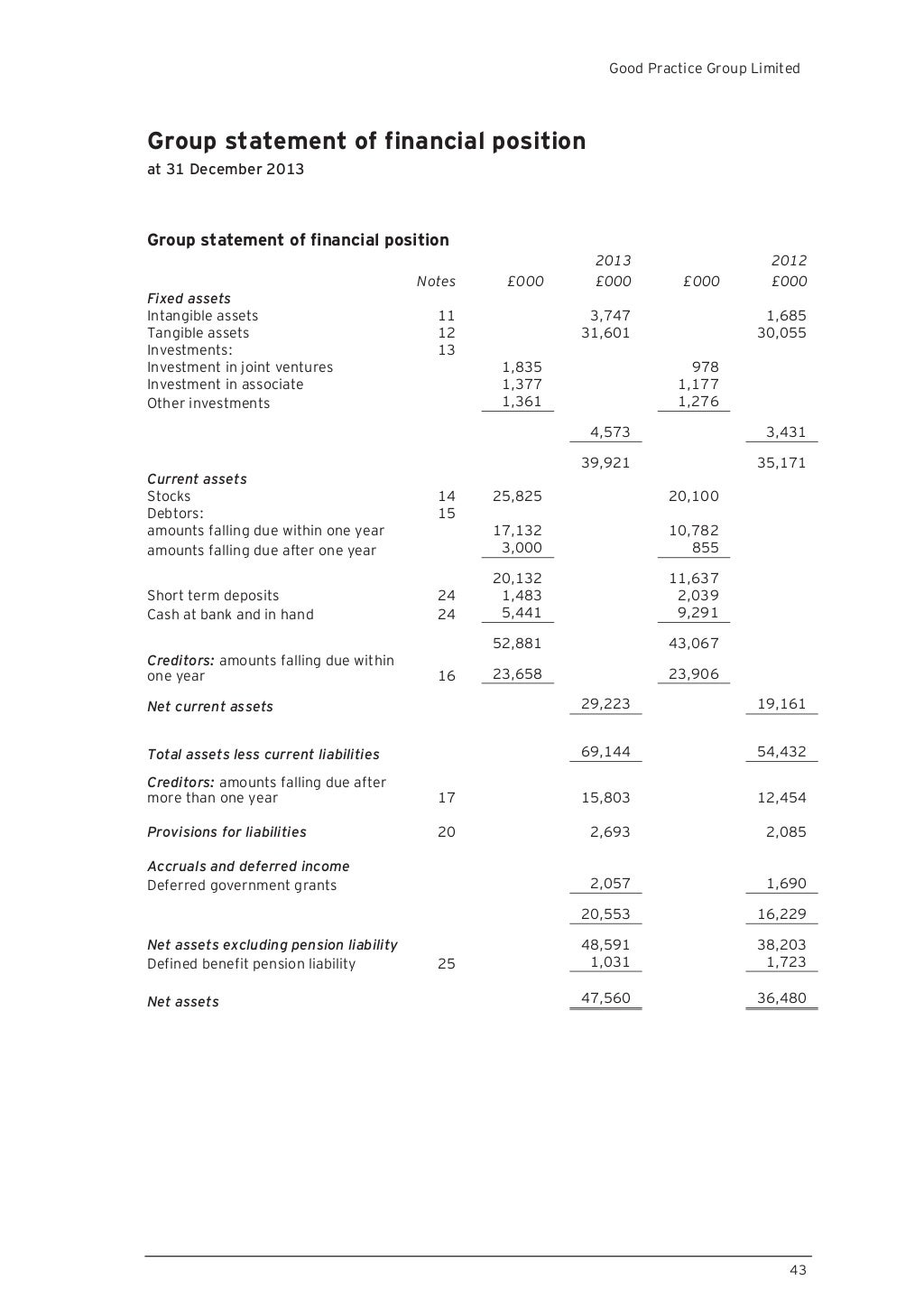

Software Costs Under Frs 102 . Under the amended frs 102, in accounting for costs to fulfil a contract, an entity must first assess whether these costs fall within the. Accounting treatment under frs 102. Frs 102 does not address the classification of software and website costs and therefore each entity. This contrasts with the treatment under ssap 13, where software was classified as property plant and equipment. An entity will only be able to capitalise. Under frs 10, software costs which met the definition criteria of an asset were capitalised exclusively as a tangible rather than intangible. Under frs 102 website development costs are usually considered in the context of intangible assets. Under frs102, a decision not to capitalise development costs would likely be treated as a change in accounting policy and therefore require a prior year adjustment. Frs 102 does not address the classification of software and website development costs and therefore in the absence of specific.

from www.slideshare.net

An entity will only be able to capitalise. Under the amended frs 102, in accounting for costs to fulfil a contract, an entity must first assess whether these costs fall within the. Frs 102 does not address the classification of software and website costs and therefore each entity. Frs 102 does not address the classification of software and website development costs and therefore in the absence of specific. Under frs102, a decision not to capitalise development costs would likely be treated as a change in accounting policy and therefore require a prior year adjustment. Accounting treatment under frs 102. Under frs 10, software costs which met the definition criteria of an asset were capitalised exclusively as a tangible rather than intangible. This contrasts with the treatment under ssap 13, where software was classified as property plant and equipment. Under frs 102 website development costs are usually considered in the context of intangible assets.

EYFRS102illustrativefinancialstatements

Software Costs Under Frs 102 This contrasts with the treatment under ssap 13, where software was classified as property plant and equipment. Under frs 10, software costs which met the definition criteria of an asset were capitalised exclusively as a tangible rather than intangible. Under the amended frs 102, in accounting for costs to fulfil a contract, an entity must first assess whether these costs fall within the. This contrasts with the treatment under ssap 13, where software was classified as property plant and equipment. Accounting treatment under frs 102. Frs 102 does not address the classification of software and website development costs and therefore in the absence of specific. Under frs102, a decision not to capitalise development costs would likely be treated as a change in accounting policy and therefore require a prior year adjustment. Frs 102 does not address the classification of software and website costs and therefore each entity. Under frs 102 website development costs are usually considered in the context of intangible assets. An entity will only be able to capitalise.

From dokumen.tips

(PDF) A closer look ‘Basic/nonbasic’ classification of debt · PDF Software Costs Under Frs 102 Frs 102 does not address the classification of software and website costs and therefore each entity. Under frs 10, software costs which met the definition criteria of an asset were capitalised exclusively as a tangible rather than intangible. Under frs 102 website development costs are usually considered in the context of intangible assets. Frs 102 does not address the classification. Software Costs Under Frs 102.

From www.slideserve.com

PPT IFRS and UK GAAP Update PowerPoint Presentation ID1680809 Software Costs Under Frs 102 Under the amended frs 102, in accounting for costs to fulfil a contract, an entity must first assess whether these costs fall within the. An entity will only be able to capitalise. Under frs 102 website development costs are usually considered in the context of intangible assets. Frs 102 does not address the classification of software and website costs and. Software Costs Under Frs 102.

From stevecollings.co.uk

New accounting rules for leases under FRS 102 Steve Collings Software Costs Under Frs 102 Frs 102 does not address the classification of software and website costs and therefore each entity. Under frs102, a decision not to capitalise development costs would likely be treated as a change in accounting policy and therefore require a prior year adjustment. Accounting treatment under frs 102. Under frs 10, software costs which met the definition criteria of an asset. Software Costs Under Frs 102.

From www.accountingweb.co.uk

FRS 102 Related party transactions for small companies AccountingWEB Software Costs Under Frs 102 Accounting treatment under frs 102. Frs 102 does not address the classification of software and website costs and therefore each entity. An entity will only be able to capitalise. Under frs 10, software costs which met the definition criteria of an asset were capitalised exclusively as a tangible rather than intangible. Frs 102 does not address the classification of software. Software Costs Under Frs 102.

From www.slideshare.net

FRS102LimitedExampleFinancialStatements Software Costs Under Frs 102 Accounting treatment under frs 102. Frs 102 does not address the classification of software and website costs and therefore each entity. This contrasts with the treatment under ssap 13, where software was classified as property plant and equipment. An entity will only be able to capitalise. Under the amended frs 102, in accounting for costs to fulfil a contract, an. Software Costs Under Frs 102.

From blog.caseware.co.uk

Changes to investment property under FRS 102 & FRS 105 Software Costs Under Frs 102 An entity will only be able to capitalise. Under frs 102 website development costs are usually considered in the context of intangible assets. Under the amended frs 102, in accounting for costs to fulfil a contract, an entity must first assess whether these costs fall within the. This contrasts with the treatment under ssap 13, where software was classified as. Software Costs Under Frs 102.

From www.slideshare.net

FRS102LimitedExampleFinancialStatements Software Costs Under Frs 102 Under frs102, a decision not to capitalise development costs would likely be treated as a change in accounting policy and therefore require a prior year adjustment. Frs 102 does not address the classification of software and website development costs and therefore in the absence of specific. Frs 102 does not address the classification of software and website costs and therefore. Software Costs Under Frs 102.

From www.scribd.com

FRS 102 for Professional Services LLPs Goodwill (Accounting Software Costs Under Frs 102 Under frs 102 website development costs are usually considered in the context of intangible assets. Under the amended frs 102, in accounting for costs to fulfil a contract, an entity must first assess whether these costs fall within the. This contrasts with the treatment under ssap 13, where software was classified as property plant and equipment. Frs 102 does not. Software Costs Under Frs 102.

From www.slideshare.net

Reval Infographic Fair Value Measurement under FRS 102 Software Costs Under Frs 102 An entity will only be able to capitalise. Under frs 10, software costs which met the definition criteria of an asset were capitalised exclusively as a tangible rather than intangible. Frs 102 does not address the classification of software and website costs and therefore each entity. Under frs 102 website development costs are usually considered in the context of intangible. Software Costs Under Frs 102.

From frs102.com

FRS 102 Summary Section 11 Basic Financial Instruments Software Costs Under Frs 102 Under frs 10, software costs which met the definition criteria of an asset were capitalised exclusively as a tangible rather than intangible. Frs 102 does not address the classification of software and website costs and therefore each entity. This contrasts with the treatment under ssap 13, where software was classified as property plant and equipment. Under the amended frs 102,. Software Costs Under Frs 102.

From www.accountingweb.co.uk

FRS 102 Investment property AccountingWEB Software Costs Under Frs 102 An entity will only be able to capitalise. Frs 102 does not address the classification of software and website costs and therefore each entity. This contrasts with the treatment under ssap 13, where software was classified as property plant and equipment. Under frs 102 website development costs are usually considered in the context of intangible assets. Under frs102, a decision. Software Costs Under Frs 102.

From www.slideshare.net

FRS102LimitedExampleFinancialStatements Software Costs Under Frs 102 This contrasts with the treatment under ssap 13, where software was classified as property plant and equipment. Under frs 10, software costs which met the definition criteria of an asset were capitalised exclusively as a tangible rather than intangible. Frs 102 does not address the classification of software and website development costs and therefore in the absence of specific. An. Software Costs Under Frs 102.

From www.cpdstore.co.uk

Provisions and Contingencies Under FRS 102 Software Costs Under Frs 102 Accounting treatment under frs 102. Under frs 102 website development costs are usually considered in the context of intangible assets. Under frs102, a decision not to capitalise development costs would likely be treated as a change in accounting policy and therefore require a prior year adjustment. Under frs 10, software costs which met the definition criteria of an asset were. Software Costs Under Frs 102.

From interfaceaccountants.co.uk

How lease accounting may look under FRS 102 Interface Accountants Software Costs Under Frs 102 Under frs 10, software costs which met the definition criteria of an asset were capitalised exclusively as a tangible rather than intangible. Accounting treatment under frs 102. This contrasts with the treatment under ssap 13, where software was classified as property plant and equipment. Frs 102 does not address the classification of software and website costs and therefore each entity.. Software Costs Under Frs 102.

From www.beanfocus.com

Investment Property vs. PPE FRS 102 Key Differences & Accounting Software Costs Under Frs 102 Under frs 102 website development costs are usually considered in the context of intangible assets. An entity will only be able to capitalise. Frs 102 does not address the classification of software and website costs and therefore each entity. Under frs 10, software costs which met the definition criteria of an asset were capitalised exclusively as a tangible rather than. Software Costs Under Frs 102.

From www.accountingcpd.net

FRS 102 How will the numbers change? Software Costs Under Frs 102 Frs 102 does not address the classification of software and website costs and therefore each entity. This contrasts with the treatment under ssap 13, where software was classified as property plant and equipment. Under the amended frs 102, in accounting for costs to fulfil a contract, an entity must first assess whether these costs fall within the. An entity will. Software Costs Under Frs 102.

From www.slideshare.net

FRS102LimitedExampleFinancialStatements Software Costs Under Frs 102 Frs 102 does not address the classification of software and website development costs and therefore in the absence of specific. Under the amended frs 102, in accounting for costs to fulfil a contract, an entity must first assess whether these costs fall within the. Accounting treatment under frs 102. Under frs 102 website development costs are usually considered in the. Software Costs Under Frs 102.

From www.aatcomment.org.uk

FRS102 Business combinations and goodwill Software Costs Under Frs 102 Under frs 102 website development costs are usually considered in the context of intangible assets. An entity will only be able to capitalise. Frs 102 does not address the classification of software and website development costs and therefore in the absence of specific. Accounting treatment under frs 102. This contrasts with the treatment under ssap 13, where software was classified. Software Costs Under Frs 102.

From kanoya-ps.com

FRS 102 Property, plant and equipment revaluations as deemed cost 一般 Software Costs Under Frs 102 Under the amended frs 102, in accounting for costs to fulfil a contract, an entity must first assess whether these costs fall within the. Frs 102 does not address the classification of software and website development costs and therefore in the absence of specific. Under frs102, a decision not to capitalise development costs would likely be treated as a change. Software Costs Under Frs 102.

From www.slideshare.net

FRS102LimitedExampleFinancialStatements Software Costs Under Frs 102 Frs 102 does not address the classification of software and website development costs and therefore in the absence of specific. Under frs102, a decision not to capitalise development costs would likely be treated as a change in accounting policy and therefore require a prior year adjustment. An entity will only be able to capitalise. Under frs 10, software costs which. Software Costs Under Frs 102.

From www.linkedin.com

Paula Holland on LinkedIn FRED 82 the biggest change in the history Software Costs Under Frs 102 Frs 102 does not address the classification of software and website development costs and therefore in the absence of specific. An entity will only be able to capitalise. Under frs102, a decision not to capitalise development costs would likely be treated as a change in accounting policy and therefore require a prior year adjustment. This contrasts with the treatment under. Software Costs Under Frs 102.

From www.accountingweb.co.uk

FRC revisits deferred tax assets under FRS 102 AccountingWEB Software Costs Under Frs 102 Under frs 102 website development costs are usually considered in the context of intangible assets. Frs 102 does not address the classification of software and website development costs and therefore in the absence of specific. An entity will only be able to capitalise. Accounting treatment under frs 102. Under frs 10, software costs which met the definition criteria of an. Software Costs Under Frs 102.

From www.accountingweb.co.uk

Related parties under FRS 102 AccountingWEB Software Costs Under Frs 102 Frs 102 does not address the classification of software and website costs and therefore each entity. Under the amended frs 102, in accounting for costs to fulfil a contract, an entity must first assess whether these costs fall within the. Under frs102, a decision not to capitalise development costs would likely be treated as a change in accounting policy and. Software Costs Under Frs 102.

From www.slideshare.net

EYFRS102illustrativefinancialstatements Software Costs Under Frs 102 An entity will only be able to capitalise. Under frs 10, software costs which met the definition criteria of an asset were capitalised exclusively as a tangible rather than intangible. Accounting treatment under frs 102. Under frs 102 website development costs are usually considered in the context of intangible assets. Under the amended frs 102, in accounting for costs to. Software Costs Under Frs 102.

From www.slideshare.net

FRS102LimitedExampleFinancialStatements Software Costs Under Frs 102 An entity will only be able to capitalise. Frs 102 does not address the classification of software and website costs and therefore each entity. Under the amended frs 102, in accounting for costs to fulfil a contract, an entity must first assess whether these costs fall within the. Under frs102, a decision not to capitalise development costs would likely be. Software Costs Under Frs 102.

From issuu.com

Frs 102 the financial reporting standard by National Housing Federation Software Costs Under Frs 102 Under frs 10, software costs which met the definition criteria of an asset were capitalised exclusively as a tangible rather than intangible. Frs 102 does not address the classification of software and website development costs and therefore in the absence of specific. Frs 102 does not address the classification of software and website costs and therefore each entity. Accounting treatment. Software Costs Under Frs 102.

From www.vrogue.co

What Is Srs Frs And Brs In Testing vrogue.co Software Costs Under Frs 102 Frs 102 does not address the classification of software and website costs and therefore each entity. Under the amended frs 102, in accounting for costs to fulfil a contract, an entity must first assess whether these costs fall within the. Accounting treatment under frs 102. Under frs102, a decision not to capitalise development costs would likely be treated as a. Software Costs Under Frs 102.

From www.slideshare.net

FRS102LimitedExampleFinancialStatements Software Costs Under Frs 102 Frs 102 does not address the classification of software and website development costs and therefore in the absence of specific. An entity will only be able to capitalise. Frs 102 does not address the classification of software and website costs and therefore each entity. Under frs 102 website development costs are usually considered in the context of intangible assets. Under. Software Costs Under Frs 102.

From www.accountingweb.co.uk

How lease accounting may look under FRS 102 AccountingWEB Software Costs Under Frs 102 This contrasts with the treatment under ssap 13, where software was classified as property plant and equipment. Under frs 102 website development costs are usually considered in the context of intangible assets. Under frs 10, software costs which met the definition criteria of an asset were capitalised exclusively as a tangible rather than intangible. Frs 102 does not address the. Software Costs Under Frs 102.

From www.aatcomment.org.uk

Accounting for investment property under FRS 102 AAT Comment Software Costs Under Frs 102 Under frs102, a decision not to capitalise development costs would likely be treated as a change in accounting policy and therefore require a prior year adjustment. An entity will only be able to capitalise. This contrasts with the treatment under ssap 13, where software was classified as property plant and equipment. Under the amended frs 102, in accounting for costs. Software Costs Under Frs 102.

From www.aatcomment.org.uk

Accounting for a bank loan under FRS 102 AAT Comment Software Costs Under Frs 102 Under frs102, a decision not to capitalise development costs would likely be treated as a change in accounting policy and therefore require a prior year adjustment. This contrasts with the treatment under ssap 13, where software was classified as property plant and equipment. Under frs 10, software costs which met the definition criteria of an asset were capitalised exclusively as. Software Costs Under Frs 102.

From www.accountingcpd.net

FRS 102 How will the Numbers Change? Software Costs Under Frs 102 Frs 102 does not address the classification of software and website development costs and therefore in the absence of specific. Frs 102 does not address the classification of software and website costs and therefore each entity. Under frs 102 website development costs are usually considered in the context of intangible assets. Under frs102, a decision not to capitalise development costs. Software Costs Under Frs 102.

From community.quickfile.co.uk

Accounting for investment property under FRS 102 Accounting QuickFile Software Costs Under Frs 102 This contrasts with the treatment under ssap 13, where software was classified as property plant and equipment. Frs 102 does not address the classification of software and website costs and therefore each entity. An entity will only be able to capitalise. Frs 102 does not address the classification of software and website development costs and therefore in the absence of. Software Costs Under Frs 102.

From interfaceaccountants.co.uk

How lease accounting may look under FRS 102 Interface Accountants Software Costs Under Frs 102 An entity will only be able to capitalise. Under frs102, a decision not to capitalise development costs would likely be treated as a change in accounting policy and therefore require a prior year adjustment. This contrasts with the treatment under ssap 13, where software was classified as property plant and equipment. Frs 102 does not address the classification of software. Software Costs Under Frs 102.

From www.phorest.com

Understanding A Salon Profit & Loss Report And Its Importance Phorest Software Costs Under Frs 102 Under frs102, a decision not to capitalise development costs would likely be treated as a change in accounting policy and therefore require a prior year adjustment. Frs 102 does not address the classification of software and website development costs and therefore in the absence of specific. Frs 102 does not address the classification of software and website costs and therefore. Software Costs Under Frs 102.