In Economics What Is Cost . This concept encompasses not only the direct financial costs. In other words, it is the sum of accounting cost and opportunity cost. Economic cost is greater than accounting cost because of the. Economic cost refers to the total cost of choosing one action over another. For example, a consumer typically equates cost with. Economic cost is the sum of explicit cost and implicit cost. The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce goods and services. Cost is the monetary value of goods and services purchased by producers and consumers. An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a.

from webapi.bu.edu

This concept encompasses not only the direct financial costs. Cost is the monetary value of goods and services purchased by producers and consumers. An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a. Economic cost refers to the total cost of choosing one action over another. Economic cost is greater than accounting cost because of the. In other words, it is the sum of accounting cost and opportunity cost. The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce goods and services. For example, a consumer typically equates cost with. Economic cost is the sum of explicit cost and implicit cost.

🌱 Why are costs important in economics. Why is opportunity cost so

In Economics What Is Cost An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a. Economic cost is the sum of explicit cost and implicit cost. This concept encompasses not only the direct financial costs. For example, a consumer typically equates cost with. Cost is the monetary value of goods and services purchased by producers and consumers. Economic cost refers to the total cost of choosing one action over another. An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a. The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce goods and services. Economic cost is greater than accounting cost because of the. In other words, it is the sum of accounting cost and opportunity cost.

From www.economicshelp.org

Diagrams of Cost Curves Economics Help In Economics What Is Cost In other words, it is the sum of accounting cost and opportunity cost. The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce goods and services. Economic cost is greater than accounting cost because of the. Cost is the monetary value of goods and services purchased by producers and consumers.. In Economics What Is Cost.

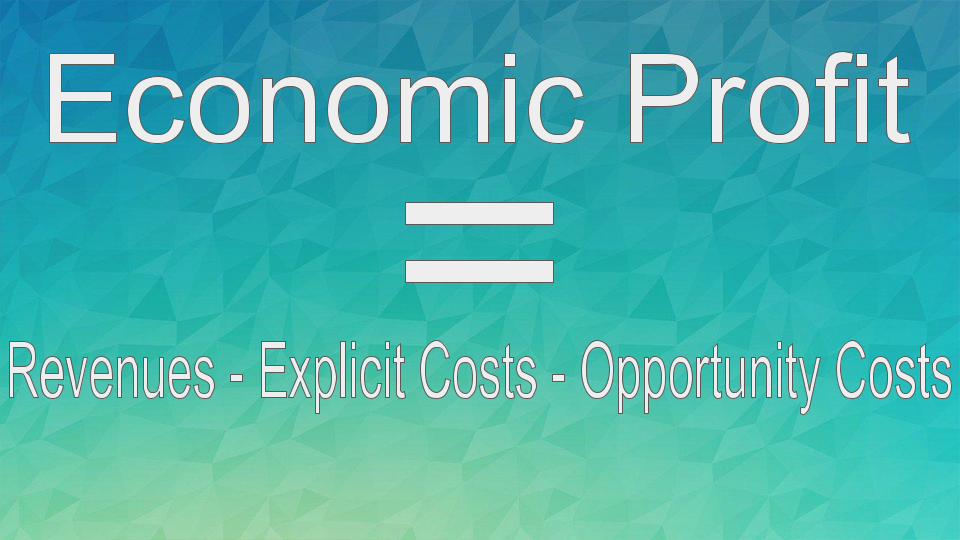

From www.slideserve.com

PPT Cost Concepts in Economics PowerPoint Presentation, free download In Economics What Is Cost Economic cost is the sum of explicit cost and implicit cost. The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce goods and services. This concept encompasses not only the direct financial costs. Economic cost is greater than accounting cost because of the. In other words, it is the sum. In Economics What Is Cost.

From www.geektonight.com

10 Types Of Costs Production Economics In Economics What Is Cost Economic cost is greater than accounting cost because of the. An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a. Economic cost is the sum of explicit cost and implicit cost. Cost is the monetary value of goods and services purchased. In Economics What Is Cost.

From www.slideserve.com

PPT Cost Concepts in Economics PowerPoint Presentation, free download In Economics What Is Cost For example, a consumer typically equates cost with. Economic cost is greater than accounting cost because of the. Economic cost refers to the total cost of choosing one action over another. An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a.. In Economics What Is Cost.

From majorstudy.blogspot.com

Cost Terminology Elements of costs, Different types of costs and Cost In Economics What Is Cost For example, a consumer typically equates cost with. Cost is the monetary value of goods and services purchased by producers and consumers. An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a. This concept encompasses not only the direct financial costs.. In Economics What Is Cost.

From helpfulprofessor.com

10 Implicit Costs Examples (2024) In Economics What Is Cost In other words, it is the sum of accounting cost and opportunity cost. Economic cost is greater than accounting cost because of the. This concept encompasses not only the direct financial costs. The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce goods and services. Cost is the monetary value. In Economics What Is Cost.

From www.slideserve.com

PPT Transaction Cost Economics PowerPoint Presentation, free download In Economics What Is Cost Economic cost is greater than accounting cost because of the. In other words, it is the sum of accounting cost and opportunity cost. Cost is the monetary value of goods and services purchased by producers and consumers. For example, a consumer typically equates cost with. The concept of cost in economics refers to the total expenditure a firm incurs when. In Economics What Is Cost.

From penpoin.com

Total Variable Cost Examples, Curve, Importance In Economics What Is Cost In other words, it is the sum of accounting cost and opportunity cost. For example, a consumer typically equates cost with. Economic cost is greater than accounting cost because of the. Cost is the monetary value of goods and services purchased by producers and consumers. Economic cost is the sum of explicit cost and implicit cost. An economic cost is. In Economics What Is Cost.

From www.slideserve.com

PPT TRANSACTION COST THEORY PowerPoint Presentation, free download In Economics What Is Cost Economic cost refers to the total cost of choosing one action over another. Cost is the monetary value of goods and services purchased by producers and consumers. This concept encompasses not only the direct financial costs. For example, a consumer typically equates cost with. The concept of cost in economics refers to the total expenditure a firm incurs when utilizing. In Economics What Is Cost.

From www.slideserve.com

PPT 13.1 ECONOMIC COST AND PROFIT PowerPoint Presentation, free In Economics What Is Cost An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a. For example, a consumer typically equates cost with. Economic cost refers to the total cost of choosing one action over another. Economic cost is the sum of explicit cost and implicit. In Economics What Is Cost.

From www.educba.com

Total Cost Formula Calculator (Examples with Excel Template) In Economics What Is Cost Economic cost refers to the total cost of choosing one action over another. Economic cost is greater than accounting cost because of the. The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce goods and services. For example, a consumer typically equates cost with. Economic cost is the sum of. In Economics What Is Cost.

From www.slideserve.com

PPT Costs PowerPoint Presentation, free download ID6671806 In Economics What Is Cost In other words, it is the sum of accounting cost and opportunity cost. The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce goods and services. This concept encompasses not only the direct financial costs. Economic cost is greater than accounting cost because of the. An economic cost is the. In Economics What Is Cost.

From iteducationlearning.com

What are the opportunity costs and all that you need to know about it? In Economics What Is Cost This concept encompasses not only the direct financial costs. An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a. Economic cost refers to the total cost of choosing one action over another. Economic cost is the sum of explicit cost and. In Economics What Is Cost.

From www.geektonight.com

10 Types Of Costs Production Economics In Economics What Is Cost For example, a consumer typically equates cost with. In other words, it is the sum of accounting cost and opportunity cost. An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a. Economic cost is greater than accounting cost because of the.. In Economics What Is Cost.

From educationleaves.com

What is cost and revenue in economics?, Types of cost, Revenue In Economics What Is Cost For example, a consumer typically equates cost with. Cost is the monetary value of goods and services purchased by producers and consumers. Economic cost is greater than accounting cost because of the. In other words, it is the sum of accounting cost and opportunity cost. The concept of cost in economics refers to the total expenditure a firm incurs when. In Economics What Is Cost.

From webapi.bu.edu

🌱 Why are costs important in economics. Why is opportunity cost so In Economics What Is Cost For example, a consumer typically equates cost with. Economic cost refers to the total cost of choosing one action over another. Cost is the monetary value of goods and services purchased by producers and consumers. This concept encompasses not only the direct financial costs. Economic cost is greater than accounting cost because of the. An economic cost is the value. In Economics What Is Cost.

From en.ppt-online.org

The costs of production. Chapter 8 online presentation In Economics What Is Cost Economic cost refers to the total cost of choosing one action over another. For example, a consumer typically equates cost with. This concept encompasses not only the direct financial costs. An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a. In. In Economics What Is Cost.

From www.economicshelp.org

Diagrams of Cost Curves Economics Help In Economics What Is Cost The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce goods and services. For example, a consumer typically equates cost with. Economic cost is greater than accounting cost because of the. Economic cost refers to the total cost of choosing one action over another. Economic cost is the sum of. In Economics What Is Cost.

From scoop.eduncle.com

What is economic cost? In Economics What Is Cost An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a. Economic cost is greater than accounting cost because of the. Economic cost is the sum of explicit cost and implicit cost. This concept encompasses not only the direct financial costs. The. In Economics What Is Cost.

From www.youtube.com

Economic cost calculations. For unit 5, by John In Economics What Is Cost An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a. For example, a consumer typically equates cost with. The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce goods and services.. In Economics What Is Cost.

From efinancemanagement.com

Types and Basis of Cost Classification Nature, Functions, Behavior eFM In Economics What Is Cost For example, a consumer typically equates cost with. Economic cost is greater than accounting cost because of the. Economic cost refers to the total cost of choosing one action over another. An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a.. In Economics What Is Cost.

From www.wallstreetmojo.com

Factor Cost Meaning, Formula (GDP, NNP, NVA), Vs Market Price In Economics What Is Cost Economic cost refers to the total cost of choosing one action over another. The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce goods and services. In other words, it is the sum of accounting cost and opportunity cost. For example, a consumer typically equates cost with. This concept encompasses. In Economics What Is Cost.

From dxojiicsa.blob.core.windows.net

Average Cost Definition Of at Gregory Cassidy blog In Economics What Is Cost In other words, it is the sum of accounting cost and opportunity cost. An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a. Economic cost refers to the total cost of choosing one action over another. For example, a consumer typically. In Economics What Is Cost.

From www.economicshelp.org

Diagrams of Cost Curves Economics Help In Economics What Is Cost The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce goods and services. Economic cost refers to the total cost of choosing one action over another. Cost is the monetary value of goods and services purchased by producers and consumers. For example, a consumer typically equates cost with. An economic. In Economics What Is Cost.

From www.marketing91.com

Economic Cost Definition, Examples and Calculation Marketing91 In Economics What Is Cost Economic cost refers to the total cost of choosing one action over another. In other words, it is the sum of accounting cost and opportunity cost. Cost is the monetary value of goods and services purchased by producers and consumers. The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce. In Economics What Is Cost.

From learnbusinessconcepts.com

Economic Cost Definition, Explanation, with Examples In Economics What Is Cost This concept encompasses not only the direct financial costs. The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce goods and services. Economic cost refers to the total cost of choosing one action over another. An economic cost is the value you give up when you choose one economic activity. In Economics What Is Cost.

From www.youtube.com

IB Economics Economic Cost Explicit vs Implicit Cost YouTube In Economics What Is Cost In other words, it is the sum of accounting cost and opportunity cost. Economic cost is greater than accounting cost because of the. For example, a consumer typically equates cost with. This concept encompasses not only the direct financial costs. An economic cost is the value you give up when you choose one economic activity over the next best economic. In Economics What Is Cost.

From enotesworld.com

Cost of Economic Growth Development Economics In Economics What Is Cost Economic cost refers to the total cost of choosing one action over another. An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a. Cost is the monetary value of goods and services purchased by producers and consumers. The concept of cost. In Economics What Is Cost.

From loegppfac.blob.core.windows.net

What Does Cost Mean In Economics And Factors Which Affect The In Economics What Is Cost An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a. Economic cost is the sum of explicit cost and implicit cost. The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce. In Economics What Is Cost.

From www.slideserve.com

PPT Costs Curves Diminishing Returns PowerPoint Presentation, free In Economics What Is Cost For example, a consumer typically equates cost with. The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce goods and services. An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a.. In Economics What Is Cost.

From study.com

Transaction Costs in Economics Theory, Types & Examples Lesson In Economics What Is Cost For example, a consumer typically equates cost with. This concept encompasses not only the direct financial costs. Economic cost is the sum of explicit cost and implicit cost. Economic cost is greater than accounting cost because of the. In other words, it is the sum of accounting cost and opportunity cost. Cost is the monetary value of goods and services. In Economics What Is Cost.

From getuplearn.com

What is Cost Concept? All Different Types of Costs In Economics What Is Cost Economic cost is greater than accounting cost because of the. This concept encompasses not only the direct financial costs. Economic cost is the sum of explicit cost and implicit cost. Cost is the monetary value of goods and services purchased by producers and consumers. In other words, it is the sum of accounting cost and opportunity cost. The concept of. In Economics What Is Cost.

From www.youtube.com

What is Economic Cost? YouTube In Economics What Is Cost The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce goods and services. An economic cost is the value you give up when you choose one economic activity over the next best economic activity, such as buying a product or starting a. Economic cost is the sum of explicit cost. In Economics What Is Cost.

From sendpulse.ng

What is Total Cost Definitive Guide SendPulse In Economics What Is Cost Economic cost is greater than accounting cost because of the. Economic cost is the sum of explicit cost and implicit cost. For example, a consumer typically equates cost with. Economic cost refers to the total cost of choosing one action over another. This concept encompasses not only the direct financial costs. In other words, it is the sum of accounting. In Economics What Is Cost.

From joidudyzb.blob.core.windows.net

Types Of Cost Basis at Elma Alexander blog In Economics What Is Cost Economic cost is greater than accounting cost because of the. This concept encompasses not only the direct financial costs. Cost is the monetary value of goods and services purchased by producers and consumers. The concept of cost in economics refers to the total expenditure a firm incurs when utilizing economic resources to produce goods and services. In other words, it. In Economics What Is Cost.