Cross Currency Interest Rate Swap Hedge Accounting . Thisexample illustrates one possible method of applying the. According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short. In order to cope with this. Risk management strategy could identify changes in interest rates of loans as a risk and define a specific target range for the fixed to floating rate ratio for those loans. New ifrs 9 hedging disclosures even if ias 39 hedging is continued. If a cross currency interest rate swap is used in combination with a single currency hedged item, for which this spread is not relevant, hedge ineffectiveness could arise. Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in.

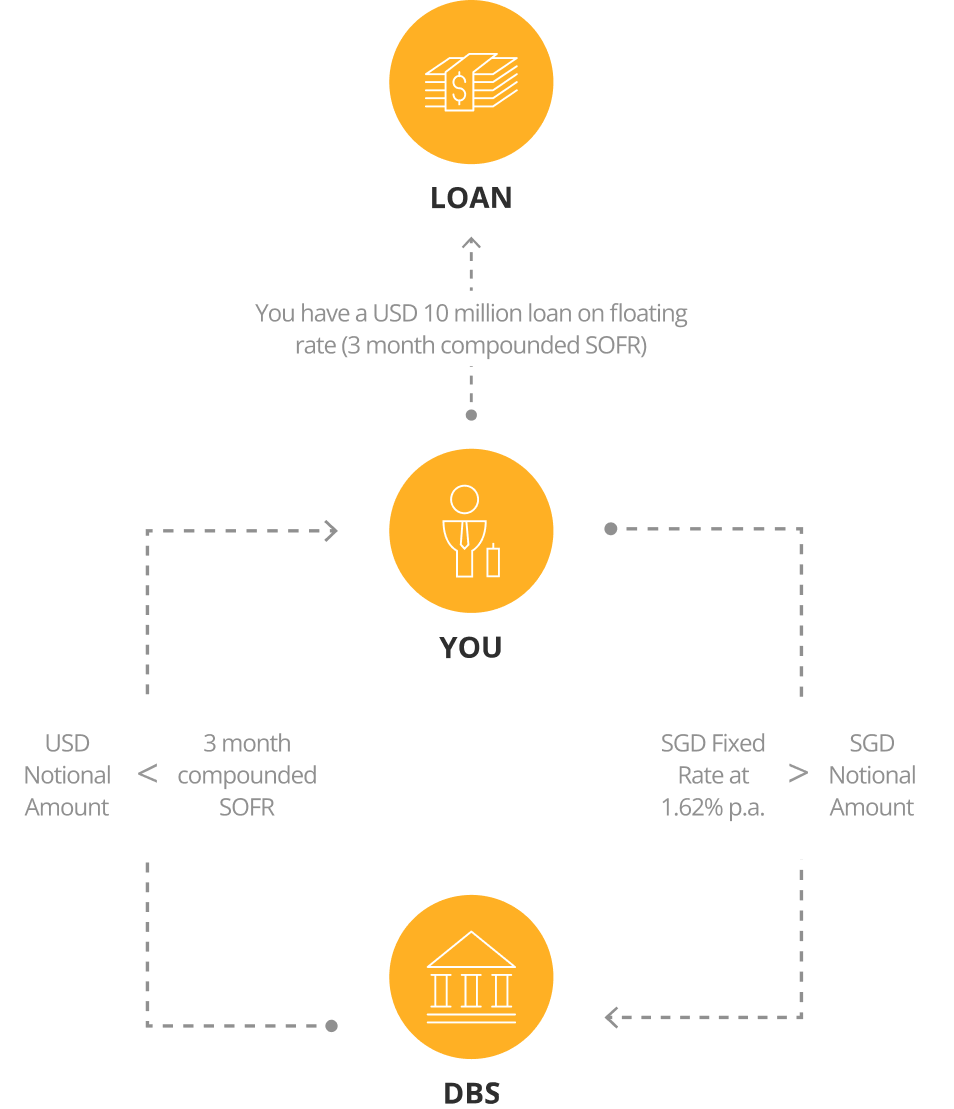

from www.dbs.com.sg

According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short. Risk management strategy could identify changes in interest rates of loans as a risk and define a specific target range for the fixed to floating rate ratio for those loans. Thisexample illustrates one possible method of applying the. If a cross currency interest rate swap is used in combination with a single currency hedged item, for which this spread is not relevant, hedge ineffectiveness could arise. In order to cope with this. New ifrs 9 hedging disclosures even if ias 39 hedging is continued. Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in.

Limit Interest Rate Exposure with Cross Currency Swaps DBS T&M

Cross Currency Interest Rate Swap Hedge Accounting Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in. Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in. Thisexample illustrates one possible method of applying the. According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short. If a cross currency interest rate swap is used in combination with a single currency hedged item, for which this spread is not relevant, hedge ineffectiveness could arise. Risk management strategy could identify changes in interest rates of loans as a risk and define a specific target range for the fixed to floating rate ratio for those loans. In order to cope with this. New ifrs 9 hedging disclosures even if ias 39 hedging is continued.

From www.awesomefintech.com

CrossCurrency Swap and Example AwesomeFinTech Blog Cross Currency Interest Rate Swap Hedge Accounting Thisexample illustrates one possible method of applying the. New ifrs 9 hedging disclosures even if ias 39 hedging is continued. Risk management strategy could identify changes in interest rates of loans as a risk and define a specific target range for the fixed to floating rate ratio for those loans. According to ifrs 9, the net market value of the. Cross Currency Interest Rate Swap Hedge Accounting.

From corporatefinanceinstitute.com

Interest Rate Swap Learn How Interest Rate Swaps Work Cross Currency Interest Rate Swap Hedge Accounting Thisexample illustrates one possible method of applying the. Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in. Risk management strategy could identify changes in interest rates of loans as a risk and define a specific target range for the fixed to floating. Cross Currency Interest Rate Swap Hedge Accounting.

From www.slideserve.com

PPT Chapter 18 Interest Rate Swaps, Currency Swaps PowerPoint Cross Currency Interest Rate Swap Hedge Accounting In order to cope with this. Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in. Thisexample illustrates one possible method of applying the. If a cross currency interest rate swap is used in combination with a single currency hedged item, for which. Cross Currency Interest Rate Swap Hedge Accounting.

From www.slideshare.net

CCS Analytics Cross Currency Interest Rate Swap Hedge Accounting If a cross currency interest rate swap is used in combination with a single currency hedged item, for which this spread is not relevant, hedge ineffectiveness could arise. According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short. New ifrs 9 hedging disclosures even if ias 39 hedging. Cross Currency Interest Rate Swap Hedge Accounting.

From www.investopedia.com

CrossCurrency Swap Definition, How It Works, Uses, and Example Cross Currency Interest Rate Swap Hedge Accounting Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in. New ifrs 9 hedging disclosures even if ias 39 hedging is continued. In order to cope with this. If a cross currency interest rate swap is used in combination with a single currency. Cross Currency Interest Rate Swap Hedge Accounting.

From www.researchgate.net

1 Cross Currency Interest Rate Swap Download Scientific Diagram Cross Currency Interest Rate Swap Hedge Accounting Thisexample illustrates one possible method of applying the. Risk management strategy could identify changes in interest rates of loans as a risk and define a specific target range for the fixed to floating rate ratio for those loans. According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short.. Cross Currency Interest Rate Swap Hedge Accounting.

From slideplayer.com

FX Forwards vs. CrossCurrency Swaps A Fair Comparison? ppt download Cross Currency Interest Rate Swap Hedge Accounting New ifrs 9 hedging disclosures even if ias 39 hedging is continued. If a cross currency interest rate swap is used in combination with a single currency hedged item, for which this spread is not relevant, hedge ineffectiveness could arise. According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as. Cross Currency Interest Rate Swap Hedge Accounting.

From www.awesomefintech.com

CrossCurrency Swap and Example AwesomeFinTech Blog Cross Currency Interest Rate Swap Hedge Accounting Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in. Risk management strategy could identify changes in interest rates of loans as a risk and define a specific target range for the fixed to floating rate ratio for those loans. New ifrs 9. Cross Currency Interest Rate Swap Hedge Accounting.

From nakisa.org

Cross Currency Basis Swaps Explained Ramin Nakisa Cross Currency Interest Rate Swap Hedge Accounting In order to cope with this. New ifrs 9 hedging disclosures even if ias 39 hedging is continued. If a cross currency interest rate swap is used in combination with a single currency hedged item, for which this spread is not relevant, hedge ineffectiveness could arise. According to ifrs 9, the net market value of the ccirs needs to be. Cross Currency Interest Rate Swap Hedge Accounting.

From www.oreilly.com

The Trade Life Cycle for CrossCurrency Swaps Accounting for Cross Currency Interest Rate Swap Hedge Accounting Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in. New ifrs 9 hedging disclosures even if ias 39 hedging is continued. Risk management strategy could identify changes in interest rates of loans as a risk and define a specific target range for. Cross Currency Interest Rate Swap Hedge Accounting.

From studylib.net

Managing Interest Rate Risk with Cross Currency Swaps Cross Currency Interest Rate Swap Hedge Accounting According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short. Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in. New ifrs 9 hedging disclosures even if ias 39 hedging is. Cross Currency Interest Rate Swap Hedge Accounting.

From www.youtube.com

CrossCurrency Interest Rate Swap (CCIRS) YouTube Cross Currency Interest Rate Swap Hedge Accounting Thisexample illustrates one possible method of applying the. New ifrs 9 hedging disclosures even if ias 39 hedging is continued. According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short. Risk management strategy could identify changes in interest rates of loans as a risk and define a specific. Cross Currency Interest Rate Swap Hedge Accounting.

From analystprep.com

Covered Interest Rate Parity Lost Understanding the CrossCurrency Cross Currency Interest Rate Swap Hedge Accounting In order to cope with this. Risk management strategy could identify changes in interest rates of loans as a risk and define a specific target range for the fixed to floating rate ratio for those loans. New ifrs 9 hedging disclosures even if ias 39 hedging is continued. If a cross currency interest rate swap is used in combination with. Cross Currency Interest Rate Swap Hedge Accounting.

From corporatefinanceinstitute.com

Currency Swap Contract Definition, How It Works, Types Cross Currency Interest Rate Swap Hedge Accounting If a cross currency interest rate swap is used in combination with a single currency hedged item, for which this spread is not relevant, hedge ineffectiveness could arise. According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short. Risk management strategy could identify changes in interest rates of. Cross Currency Interest Rate Swap Hedge Accounting.

From www.ibfundaccounting.com

Overview of Interest Rate Swaps would be important for hedge Fund Cross Currency Interest Rate Swap Hedge Accounting Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in. According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short. In order to cope with this. Thisexample illustrates one possible method. Cross Currency Interest Rate Swap Hedge Accounting.

From www.investopedia.com

Currency Swap Basics Cross Currency Interest Rate Swap Hedge Accounting In order to cope with this. Thisexample illustrates one possible method of applying the. Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in. If a cross currency interest rate swap is used in combination with a single currency hedged item, for which. Cross Currency Interest Rate Swap Hedge Accounting.

From www.researchgate.net

1 Cross Currency Interest Rate Swap Download Scientific Diagram Cross Currency Interest Rate Swap Hedge Accounting According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short. Risk management strategy could identify changes in interest rates of loans as a risk and define a specific target range for the fixed to floating rate ratio for those loans. Thisexample illustrates one possible method of applying the.. Cross Currency Interest Rate Swap Hedge Accounting.

From www.scribd.com

Cross Currency Risk PDF Interest Rate Swap Swap (Finance) Cross Currency Interest Rate Swap Hedge Accounting Thisexample illustrates one possible method of applying the. If a cross currency interest rate swap is used in combination with a single currency hedged item, for which this spread is not relevant, hedge ineffectiveness could arise. In order to cope with this. According to ifrs 9, the net market value of the ccirs needs to be booked on the balance. Cross Currency Interest Rate Swap Hedge Accounting.

From www.rba.gov.au

OTC Derivatives Reforms and the Australian Crosscurrency Swap Market RBA Cross Currency Interest Rate Swap Hedge Accounting If a cross currency interest rate swap is used in combination with a single currency hedged item, for which this spread is not relevant, hedge ineffectiveness could arise. Thisexample illustrates one possible method of applying the. Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due. Cross Currency Interest Rate Swap Hedge Accounting.

From www.slideserve.com

PPT Chapter 18 Interest Rate Swaps, Currency Swaps PowerPoint Cross Currency Interest Rate Swap Hedge Accounting Risk management strategy could identify changes in interest rates of loans as a risk and define a specific target range for the fixed to floating rate ratio for those loans. According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short. If a cross currency interest rate swap is. Cross Currency Interest Rate Swap Hedge Accounting.

From www.oreilly.com

Problem 1 Cross Currency Interest Rate Swap—USD/EUR Accounting for Cross Currency Interest Rate Swap Hedge Accounting In order to cope with this. New ifrs 9 hedging disclosures even if ias 39 hedging is continued. According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short. Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities. Cross Currency Interest Rate Swap Hedge Accounting.

From support.treasurysystems.com

Hedge accounting (Cross Currency Basis Swaps, CCIRS) Treasury Systems Cross Currency Interest Rate Swap Hedge Accounting If a cross currency interest rate swap is used in combination with a single currency hedged item, for which this spread is not relevant, hedge ineffectiveness could arise. Risk management strategy could identify changes in interest rates of loans as a risk and define a specific target range for the fixed to floating rate ratio for those loans. In order. Cross Currency Interest Rate Swap Hedge Accounting.

From www.slideserve.com

PPT Hedging Financial Market Exposure Interest Rate Swaps Cross Cross Currency Interest Rate Swap Hedge Accounting According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short. New ifrs 9 hedging disclosures even if ias 39 hedging is continued. In order to cope with this. If a cross currency interest rate swap is used in combination with a single currency hedged item, for which this. Cross Currency Interest Rate Swap Hedge Accounting.

From www.slideserve.com

PPT Hedging Financial Market Exposure Interest Rate Swaps Cross Cross Currency Interest Rate Swap Hedge Accounting If a cross currency interest rate swap is used in combination with a single currency hedged item, for which this spread is not relevant, hedge ineffectiveness could arise. Thisexample illustrates one possible method of applying the. According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short. New ifrs. Cross Currency Interest Rate Swap Hedge Accounting.

From quantrl.com

What Are Cross Currency Swaps Quant RL Cross Currency Interest Rate Swap Hedge Accounting In order to cope with this. According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short. Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in. Risk management strategy could identify. Cross Currency Interest Rate Swap Hedge Accounting.

From corporatefinanceinstitute.com

Cross Currency Swap Overview, How It Works, Benefits and Risks Cross Currency Interest Rate Swap Hedge Accounting New ifrs 9 hedging disclosures even if ias 39 hedging is continued. If a cross currency interest rate swap is used in combination with a single currency hedged item, for which this spread is not relevant, hedge ineffectiveness could arise. Thisexample illustrates one possible method of applying the. According to ifrs 9, the net market value of the ccirs needs. Cross Currency Interest Rate Swap Hedge Accounting.

From www.investopedia.com

Currency Swap vs. Interest Rate Swap Cross Currency Interest Rate Swap Hedge Accounting Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in. According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short. Risk management strategy could identify changes in interest rates of loans. Cross Currency Interest Rate Swap Hedge Accounting.

From www.slideserve.com

PPT Hedging Financial Market Exposure Interest Rate Swaps Cross Cross Currency Interest Rate Swap Hedge Accounting New ifrs 9 hedging disclosures even if ias 39 hedging is continued. Thisexample illustrates one possible method of applying the. Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in. According to ifrs 9, the net market value of the ccirs needs to. Cross Currency Interest Rate Swap Hedge Accounting.

From www.slideserve.com

PPT Managing Interest Rate Risk with Cross Currency Swaps PowerPoint Cross Currency Interest Rate Swap Hedge Accounting Thisexample illustrates one possible method of applying the. Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in. According to ifrs 9, the net market value of the ccirs needs to be booked on the balance sheet as a short. If a cross. Cross Currency Interest Rate Swap Hedge Accounting.

From mavink.com

Interest Rate Swap Cross Currency Interest Rate Swap Hedge Accounting If a cross currency interest rate swap is used in combination with a single currency hedged item, for which this spread is not relevant, hedge ineffectiveness could arise. New ifrs 9 hedging disclosures even if ias 39 hedging is continued. In order to cope with this. According to ifrs 9, the net market value of the ccirs needs to be. Cross Currency Interest Rate Swap Hedge Accounting.

From investpost.org

Currency Swap Examples Investing Post Cross Currency Interest Rate Swap Hedge Accounting Risk management strategy could identify changes in interest rates of loans as a risk and define a specific target range for the fixed to floating rate ratio for those loans. In order to cope with this. Thisexample illustrates one possible method of applying the. Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value. Cross Currency Interest Rate Swap Hedge Accounting.

From slideplayer.com

FX Forwards vs. CrossCurrency Swaps A Fair Comparison? ppt download Cross Currency Interest Rate Swap Hedge Accounting Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in. New ifrs 9 hedging disclosures even if ias 39 hedging is continued. In order to cope with this. If a cross currency interest rate swap is used in combination with a single currency. Cross Currency Interest Rate Swap Hedge Accounting.

From www.slideserve.com

PPT Hedging Financial Market Exposure Interest Rate Swaps Cross Cross Currency Interest Rate Swap Hedge Accounting If a cross currency interest rate swap is used in combination with a single currency hedged item, for which this spread is not relevant, hedge ineffectiveness could arise. In order to cope with this. Risk management strategy could identify changes in interest rates of loans as a risk and define a specific target range for the fixed to floating rate. Cross Currency Interest Rate Swap Hedge Accounting.

From www.slideserve.com

PPT Hedging Financial Market Exposure Interest Rate Swaps Cross Cross Currency Interest Rate Swap Hedge Accounting New ifrs 9 hedging disclosures even if ias 39 hedging is continued. Companies routinely utilize interest rate swaps to reduce their exposure to changes in the fair value of assets and liabilities or cash flows due to fluctuations in. Risk management strategy could identify changes in interest rates of loans as a risk and define a specific target range for. Cross Currency Interest Rate Swap Hedge Accounting.

From www.dbs.com.sg

Limit Interest Rate Exposure with Cross Currency Swaps DBS T&M Cross Currency Interest Rate Swap Hedge Accounting New ifrs 9 hedging disclosures even if ias 39 hedging is continued. In order to cope with this. If a cross currency interest rate swap is used in combination with a single currency hedged item, for which this spread is not relevant, hedge ineffectiveness could arise. Risk management strategy could identify changes in interest rates of loans as a risk. Cross Currency Interest Rate Swap Hedge Accounting.