Fixed Income Portfolio Convexity . Using the weighted averages of the durations and convexities of the individual bonds in the portfolio. The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. Application to fixed income valuation: There are two methods to calculate the duration and convexity of a bond portfolio: Duration measures the bond's sensitivity to interest rate. In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and excel solver. Convexity, a concept within fixed income markets, has gained significant attention due to its impact on portfolio optimization. 100k+ visitors in the past month For default and option free bonds, the price function is convex in the yield to maturity, a condition that easily. Using the weighted average of time to receipt of the aggregate cash flows.

from perspectives.agf.com

Using the weighted average of time to receipt of the aggregate cash flows. Convexity, a concept within fixed income markets, has gained significant attention due to its impact on portfolio optimization. In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and excel solver. For default and option free bonds, the price function is convex in the yield to maturity, a condition that easily. There are two methods to calculate the duration and convexity of a bond portfolio: The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. 100k+ visitors in the past month Duration measures the bond's sensitivity to interest rate. Using the weighted averages of the durations and convexities of the individual bonds in the portfolio. Application to fixed income valuation:

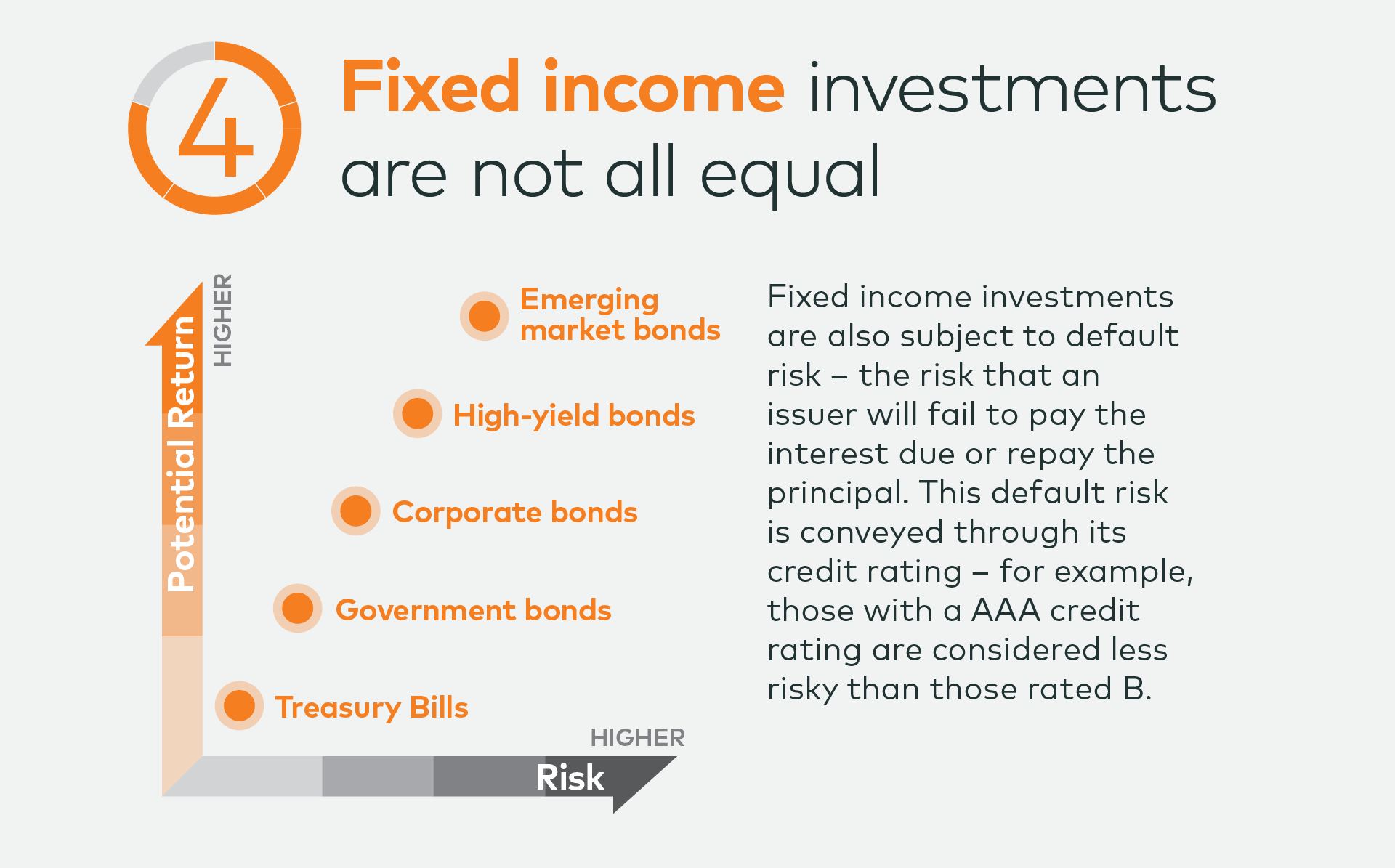

5 facts about fixed AGF Perspectives

Fixed Income Portfolio Convexity Convexity, a concept within fixed income markets, has gained significant attention due to its impact on portfolio optimization. 100k+ visitors in the past month Application to fixed income valuation: Duration measures the bond's sensitivity to interest rate. Convexity, a concept within fixed income markets, has gained significant attention due to its impact on portfolio optimization. In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and excel solver. For default and option free bonds, the price function is convex in the yield to maturity, a condition that easily. The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. There are two methods to calculate the duration and convexity of a bond portfolio: Using the weighted average of time to receipt of the aggregate cash flows. Using the weighted averages of the durations and convexities of the individual bonds in the portfolio.

From slidetodoc.com

Introduction to Fixed portfolio management Convexity strategies Fixed Income Portfolio Convexity The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. Using the weighted average of time to receipt of the aggregate cash flows. Using the weighted averages of the durations and convexities of the individual bonds in the portfolio. Application to fixed income valuation: Convexity, a. Fixed Income Portfolio Convexity.

From slidetodoc.com

Introduction to Fixed portfolio management Convexity strategies Fixed Income Portfolio Convexity Using the weighted average of time to receipt of the aggregate cash flows. Duration measures the bond's sensitivity to interest rate. In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and excel solver. Application to fixed income valuation: Convexity, a concept within fixed income markets, has gained significant. Fixed Income Portfolio Convexity.

From www.slideserve.com

PPT Fixed Portfolio Management PowerPoint Presentation, free Fixed Income Portfolio Convexity The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. There are two methods to calculate the duration and convexity of a bond portfolio: Duration measures the bond's sensitivity to interest rate. In this post, we model a fixed income portfolio by optimizing the allocation across. Fixed Income Portfolio Convexity.

From www.slideserve.com

PPT Chapter 16 Revision of the Portfolio PowerPoint Fixed Income Portfolio Convexity Using the weighted averages of the durations and convexities of the individual bonds in the portfolio. There are two methods to calculate the duration and convexity of a bond portfolio: 100k+ visitors in the past month Convexity, a concept within fixed income markets, has gained significant attention due to its impact on portfolio optimization. Application to fixed income valuation: The. Fixed Income Portfolio Convexity.

From www.slideserve.com

PPT Portfolio Management PowerPoint Presentation, free Fixed Income Portfolio Convexity Using the weighted average of time to receipt of the aggregate cash flows. Convexity, a concept within fixed income markets, has gained significant attention due to its impact on portfolio optimization. For default and option free bonds, the price function is convex in the yield to maturity, a condition that easily. Using the weighted averages of the durations and convexities. Fixed Income Portfolio Convexity.

From rurashfin.com

How to Create a Modern Portfolio? The Asset Allocation way Fixed Income Portfolio Convexity Duration measures the bond's sensitivity to interest rate. 100k+ visitors in the past month Using the weighted averages of the durations and convexities of the individual bonds in the portfolio. Using the weighted average of time to receipt of the aggregate cash flows. The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of. Fixed Income Portfolio Convexity.

From www.slideserve.com

PPT Introduction to Fixed portfolio management Convexity Fixed Income Portfolio Convexity Using the weighted average of time to receipt of the aggregate cash flows. 100k+ visitors in the past month Using the weighted averages of the durations and convexities of the individual bonds in the portfolio. In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and excel solver. Convexity,. Fixed Income Portfolio Convexity.

From financetrainingcourse.com

Model Fixed Portfolio Case Study Fixed Income Portfolio Convexity The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. There are two methods to calculate the duration and convexity of a bond portfolio: Using the weighted averages of the durations and convexities of the individual bonds in the portfolio. In this post, we model a. Fixed Income Portfolio Convexity.

From giohkxlsl.blob.core.windows.net

Fixed Portfolio Duration at Deborah McAndrews blog Fixed Income Portfolio Convexity For default and option free bonds, the price function is convex in the yield to maturity, a condition that easily. Application to fixed income valuation: In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and excel solver. Using the weighted average of time to receipt of the aggregate. Fixed Income Portfolio Convexity.

From slideplayer.com

Chapter 16 Revision of the Portfolio ppt download Fixed Income Portfolio Convexity The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. Using the weighted averages of the durations and convexities of the individual bonds in the portfolio. In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration,. Fixed Income Portfolio Convexity.

From slidetodoc.com

Introduction to Fixed portfolio management Convexity strategies Fixed Income Portfolio Convexity Convexity, a concept within fixed income markets, has gained significant attention due to its impact on portfolio optimization. Duration measures the bond's sensitivity to interest rate. There are two methods to calculate the duration and convexity of a bond portfolio: Application to fixed income valuation: The effective convexity of a bond is a curve convexity statistic that measures the secondary. Fixed Income Portfolio Convexity.

From www.slideserve.com

PPT Fixed Portfolio Management PowerPoint Presentation, free Fixed Income Portfolio Convexity For default and option free bonds, the price function is convex in the yield to maturity, a condition that easily. 100k+ visitors in the past month The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. Convexity, a concept within fixed income markets, has gained significant. Fixed Income Portfolio Convexity.

From www.slideserve.com

PPT Chapter 16 Revision of the Portfolio PowerPoint Fixed Income Portfolio Convexity Using the weighted average of time to receipt of the aggregate cash flows. 100k+ visitors in the past month Duration measures the bond's sensitivity to interest rate. The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. Application to fixed income valuation: Convexity, a concept within. Fixed Income Portfolio Convexity.

From slideplayer.com

Chapter 16 Revision of the Portfolio ppt download Fixed Income Portfolio Convexity Using the weighted average of time to receipt of the aggregate cash flows. For default and option free bonds, the price function is convex in the yield to maturity, a condition that easily. Convexity, a concept within fixed income markets, has gained significant attention due to its impact on portfolio optimization. In this post, we model a fixed income portfolio. Fixed Income Portfolio Convexity.

From www.investopedia.com

Duration and Convexity to Measure Bond Risk Fixed Income Portfolio Convexity The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. Using the weighted averages of the durations and convexities of the individual bonds in the portfolio. Application to fixed income valuation: There are two methods to calculate the duration and convexity of a bond portfolio: Using. Fixed Income Portfolio Convexity.

From www.slideserve.com

PPT Fixed Portfolio Management PowerPoint Presentation, free Fixed Income Portfolio Convexity 100k+ visitors in the past month Duration measures the bond's sensitivity to interest rate. For default and option free bonds, the price function is convex in the yield to maturity, a condition that easily. In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and excel solver. Convexity, a. Fixed Income Portfolio Convexity.

From www.slideserve.com

PPT Chapter 16 Revision of the Portfolio PowerPoint Fixed Income Portfolio Convexity Duration measures the bond's sensitivity to interest rate. For default and option free bonds, the price function is convex in the yield to maturity, a condition that easily. Using the weighted averages of the durations and convexities of the individual bonds in the portfolio. There are two methods to calculate the duration and convexity of a bond portfolio: The effective. Fixed Income Portfolio Convexity.

From www.slideserve.com

PPT Chapter 16 Revision of the Portfolio PowerPoint Fixed Income Portfolio Convexity Duration measures the bond's sensitivity to interest rate. In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and excel solver. The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. Convexity, a concept within. Fixed Income Portfolio Convexity.

From www.slideserve.com

PPT Introduction to Fixed portfolio management Convexity Fixed Income Portfolio Convexity Convexity, a concept within fixed income markets, has gained significant attention due to its impact on portfolio optimization. For default and option free bonds, the price function is convex in the yield to maturity, a condition that easily. Using the weighted averages of the durations and convexities of the individual bonds in the portfolio. In this post, we model a. Fixed Income Portfolio Convexity.

From www.slideserve.com

PPT Chapter 16 Revision of the Portfolio PowerPoint Fixed Income Portfolio Convexity 100k+ visitors in the past month In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and excel solver. Using the weighted average of time to receipt of the aggregate cash flows. Application to fixed income valuation: Using the weighted averages of the durations and convexities of the individual. Fixed Income Portfolio Convexity.

From www.slideserve.com

PPT Fixed Portfolio Management PowerPoint Presentation, free Fixed Income Portfolio Convexity Application to fixed income valuation: Using the weighted average of time to receipt of the aggregate cash flows. Duration measures the bond's sensitivity to interest rate. In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and excel solver. Convexity, a concept within fixed income markets, has gained significant. Fixed Income Portfolio Convexity.

From slidetodoc.com

Introduction to Fixed portfolio management Convexity strategies Fixed Income Portfolio Convexity Duration measures the bond's sensitivity to interest rate. Using the weighted averages of the durations and convexities of the individual bonds in the portfolio. The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. Application to fixed income valuation: In this post, we model a fixed. Fixed Income Portfolio Convexity.

From www.slideserve.com

PPT Chapter 16 Revision of the Portfolio PowerPoint Fixed Income Portfolio Convexity Using the weighted average of time to receipt of the aggregate cash flows. 100k+ visitors in the past month Duration measures the bond's sensitivity to interest rate. In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and excel solver. Using the weighted averages of the durations and convexities. Fixed Income Portfolio Convexity.

From www.youtube.com

Fixed 10 Bond Duration and Convexity Calculations YouTube Fixed Income Portfolio Convexity Duration measures the bond's sensitivity to interest rate. 100k+ visitors in the past month Using the weighted averages of the durations and convexities of the individual bonds in the portfolio. Convexity, a concept within fixed income markets, has gained significant attention due to its impact on portfolio optimization. There are two methods to calculate the duration and convexity of a. Fixed Income Portfolio Convexity.

From www.youtube.com

CFA L1 Fixed Yield Based Bond Convexity & Portfolio Fixed Income Portfolio Convexity In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and excel solver. Duration measures the bond's sensitivity to interest rate. There are two methods to calculate the duration and convexity of a bond portfolio: Convexity, a concept within fixed income markets, has gained significant attention due to its. Fixed Income Portfolio Convexity.

From www.slideserve.com

PPT Fixed Portfolio Management PowerPoint Presentation, free Fixed Income Portfolio Convexity The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and excel solver. Using the weighted average of time to receipt of the aggregate cash. Fixed Income Portfolio Convexity.

From studylib.net

Chapter 16 Revision of the Portfolio 1 Fixed Income Portfolio Convexity In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and excel solver. Duration measures the bond's sensitivity to interest rate. Using the weighted average of time to receipt of the aggregate cash flows. Convexity, a concept within fixed income markets, has gained significant attention due to its impact. Fixed Income Portfolio Convexity.

From slideplayer.com

Chapter 16 Revision of the Portfolio ppt download Fixed Income Portfolio Convexity There are two methods to calculate the duration and convexity of a bond portfolio: For default and option free bonds, the price function is convex in the yield to maturity, a condition that easily. The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. Using the. Fixed Income Portfolio Convexity.

From www.investopedia.com

Convexity Definition Fixed Income Portfolio Convexity Convexity, a concept within fixed income markets, has gained significant attention due to its impact on portfolio optimization. Duration measures the bond's sensitivity to interest rate. 100k+ visitors in the past month Using the weighted averages of the durations and convexities of the individual bonds in the portfolio. Using the weighted average of time to receipt of the aggregate cash. Fixed Income Portfolio Convexity.

From slidetodoc.com

Introduction to Fixed portfolio management Convexity strategies Fixed Income Portfolio Convexity The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. 100k+ visitors in the past month Convexity, a concept within fixed income markets, has gained significant attention due to its impact on portfolio optimization. For default and option free bonds, the price function is convex in. Fixed Income Portfolio Convexity.

From slidetodoc.com

Introduction to Fixed portfolio management Convexity strategies Fixed Income Portfolio Convexity 100k+ visitors in the past month Application to fixed income valuation: Duration measures the bond's sensitivity to interest rate. Using the weighted average of time to receipt of the aggregate cash flows. Using the weighted averages of the durations and convexities of the individual bonds in the portfolio. In this post, we model a fixed income portfolio by optimizing the. Fixed Income Portfolio Convexity.

From slidetodoc.com

Introduction to Fixed portfolio management Convexity strategies Fixed Income Portfolio Convexity Duration measures the bond's sensitivity to interest rate. In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and excel solver. There are two methods to calculate the duration and convexity of a bond portfolio: Using the weighted averages of the durations and convexities of the individual bonds in. Fixed Income Portfolio Convexity.

From perspectives.agf.com

5 facts about fixed AGF Perspectives Fixed Income Portfolio Convexity 100k+ visitors in the past month Duration measures the bond's sensitivity to interest rate. The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. Application to fixed income valuation: Using the weighted average of time to receipt of the aggregate cash flows. For default and option. Fixed Income Portfolio Convexity.

From www.slideserve.com

PPT Chapter 13 PowerPoint Presentation, free download ID6802356 Fixed Income Portfolio Convexity Convexity, a concept within fixed income markets, has gained significant attention due to its impact on portfolio optimization. For default and option free bonds, the price function is convex in the yield to maturity, a condition that easily. In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and. Fixed Income Portfolio Convexity.

From slideplayer.com

Chapter 16 Revision of the Portfolio ppt download Fixed Income Portfolio Convexity The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. 100k+ visitors in the past month Application to fixed income valuation: In this post, we model a fixed income portfolio by optimizing the allocation across the universe of securities using duration, convexity and excel solver. Duration. Fixed Income Portfolio Convexity.