Spread Duration Of A Bond Formula . one commonly used formula to calculate spread duration is: More specifically, you’ll see how to calculate. Duration measures the sensitivity of a bond to changes in interest rates. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. Calculate the price of the bond under a different credit spread scenario. spread duration is the sensitivity of a security’s price to changes in its credit spread. in this short guide, you’ll see how to calculate the bond duration. Generally, when interest rates rise,.

from analystprep.com

pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. spread duration is the sensitivity of a security’s price to changes in its credit spread. Generally, when interest rates rise,. Duration measures the sensitivity of a bond to changes in interest rates. in this short guide, you’ll see how to calculate the bond duration. More specifically, you’ll see how to calculate. Calculate the price of the bond under a different credit spread scenario. one commonly used formula to calculate spread duration is:

Exposure Measures and Their Use CFA, FRM, and Actuarial Exams Study Notes

Spread Duration Of A Bond Formula spread duration is the sensitivity of a security’s price to changes in its credit spread. More specifically, you’ll see how to calculate. spread duration is the sensitivity of a security’s price to changes in its credit spread. Duration measures the sensitivity of a bond to changes in interest rates. Calculate the price of the bond under a different credit spread scenario. Generally, when interest rates rise,. one commonly used formula to calculate spread duration is: pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. in this short guide, you’ll see how to calculate the bond duration.

From www.chegg.com

Solved Here you can upload your proof for Macaulay or Spread Duration Of A Bond Formula spread duration is the sensitivity of a security’s price to changes in its credit spread. in this short guide, you’ll see how to calculate the bond duration. one commonly used formula to calculate spread duration is: Calculate the price of the bond under a different credit spread scenario. pure, or macaulay duration, is calculated by discounting. Spread Duration Of A Bond Formula.

From www.financestrategists.com

Spread Duration Definition, Components, & Applications Spread Duration Of A Bond Formula one commonly used formula to calculate spread duration is: Generally, when interest rates rise,. spread duration is the sensitivity of a security’s price to changes in its credit spread. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. Calculate the price of the bond. Spread Duration Of A Bond Formula.

From virginiatheo.blogspot.com

Perpetual bond formula VirginiaTheo Spread Duration Of A Bond Formula in this short guide, you’ll see how to calculate the bond duration. Generally, when interest rates rise,. one commonly used formula to calculate spread duration is: Calculate the price of the bond under a different credit spread scenario. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate. Spread Duration Of A Bond Formula.

From www.youtube.com

Duration of a Bond The Calculation YouTube Spread Duration Of A Bond Formula More specifically, you’ll see how to calculate. one commonly used formula to calculate spread duration is: pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. Generally, when interest rates rise,. Calculate the price of the bond under a different credit spread scenario. spread duration. Spread Duration Of A Bond Formula.

From www.youtube.com

CFA Level 1 Fixed Reading 55 Understanding Fixed Risk Spread Duration Of A Bond Formula Calculate the price of the bond under a different credit spread scenario. one commonly used formula to calculate spread duration is: in this short guide, you’ll see how to calculate the bond duration. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. Generally, when. Spread Duration Of A Bond Formula.

From www.educba.com

Current Yield Formula Calculator (Examples with Excel Template) Spread Duration Of A Bond Formula in this short guide, you’ll see how to calculate the bond duration. More specifically, you’ll see how to calculate. Generally, when interest rates rise,. Duration measures the sensitivity of a bond to changes in interest rates. one commonly used formula to calculate spread duration is: pure, or macaulay duration, is calculated by discounting all cash flows of. Spread Duration Of A Bond Formula.

From www.educba.com

Convexity Formula Examples with Excel Template Spread Duration Of A Bond Formula Calculate the price of the bond under a different credit spread scenario. in this short guide, you’ll see how to calculate the bond duration. Generally, when interest rates rise,. Duration measures the sensitivity of a bond to changes in interest rates. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper. Spread Duration Of A Bond Formula.

From transacted.io

Spread Duration Explained Transacted Spread Duration Of A Bond Formula in this short guide, you’ll see how to calculate the bond duration. spread duration is the sensitivity of a security’s price to changes in its credit spread. More specifically, you’ll see how to calculate. Duration measures the sensitivity of a bond to changes in interest rates. Calculate the price of the bond under a different credit spread scenario.. Spread Duration Of A Bond Formula.

From studytrabeculae.z21.web.core.windows.net

How To Tell Bond Length Spread Duration Of A Bond Formula Calculate the price of the bond under a different credit spread scenario. Duration measures the sensitivity of a bond to changes in interest rates. spread duration is the sensitivity of a security’s price to changes in its credit spread. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate. Spread Duration Of A Bond Formula.

From www.youtube.com

Calculate The Macaulay Duration Of A Bond In Excel YouTube Spread Duration Of A Bond Formula in this short guide, you’ll see how to calculate the bond duration. Calculate the price of the bond under a different credit spread scenario. spread duration is the sensitivity of a security’s price to changes in its credit spread. More specifically, you’ll see how to calculate. pure, or macaulay duration, is calculated by discounting all cash flows. Spread Duration Of A Bond Formula.

From www.slideserve.com

PPT Bond Price Volatility PowerPoint Presentation, free download ID Spread Duration Of A Bond Formula pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. More specifically, you’ll see how to calculate. Duration measures the sensitivity of a bond to changes in interest rates. one commonly used formula to calculate spread duration is: Generally, when interest rates rise,. spread duration. Spread Duration Of A Bond Formula.

From study.com

How to Price Bonds Formula & Calculation Lesson Spread Duration Of A Bond Formula spread duration is the sensitivity of a security’s price to changes in its credit spread. one commonly used formula to calculate spread duration is: Duration measures the sensitivity of a bond to changes in interest rates. Generally, when interest rates rise,. Calculate the price of the bond under a different credit spread scenario. in this short guide,. Spread Duration Of A Bond Formula.

From www.thestreet.com

What Is Duration of a Bond? TheStreet Definition TheStreet Spread Duration Of A Bond Formula Generally, when interest rates rise,. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. spread duration is the sensitivity of a security’s price to changes in its credit spread. Duration measures the sensitivity of a bond to changes in interest rates. More specifically, you’ll see. Spread Duration Of A Bond Formula.

From virginiatheo.blogspot.com

Perpetual bond formula VirginiaTheo Spread Duration Of A Bond Formula pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. Generally, when interest rates rise,. one commonly used formula to calculate spread duration is: Calculate the price of the bond under a different credit spread scenario. More specifically, you’ll see how to calculate. in this. Spread Duration Of A Bond Formula.

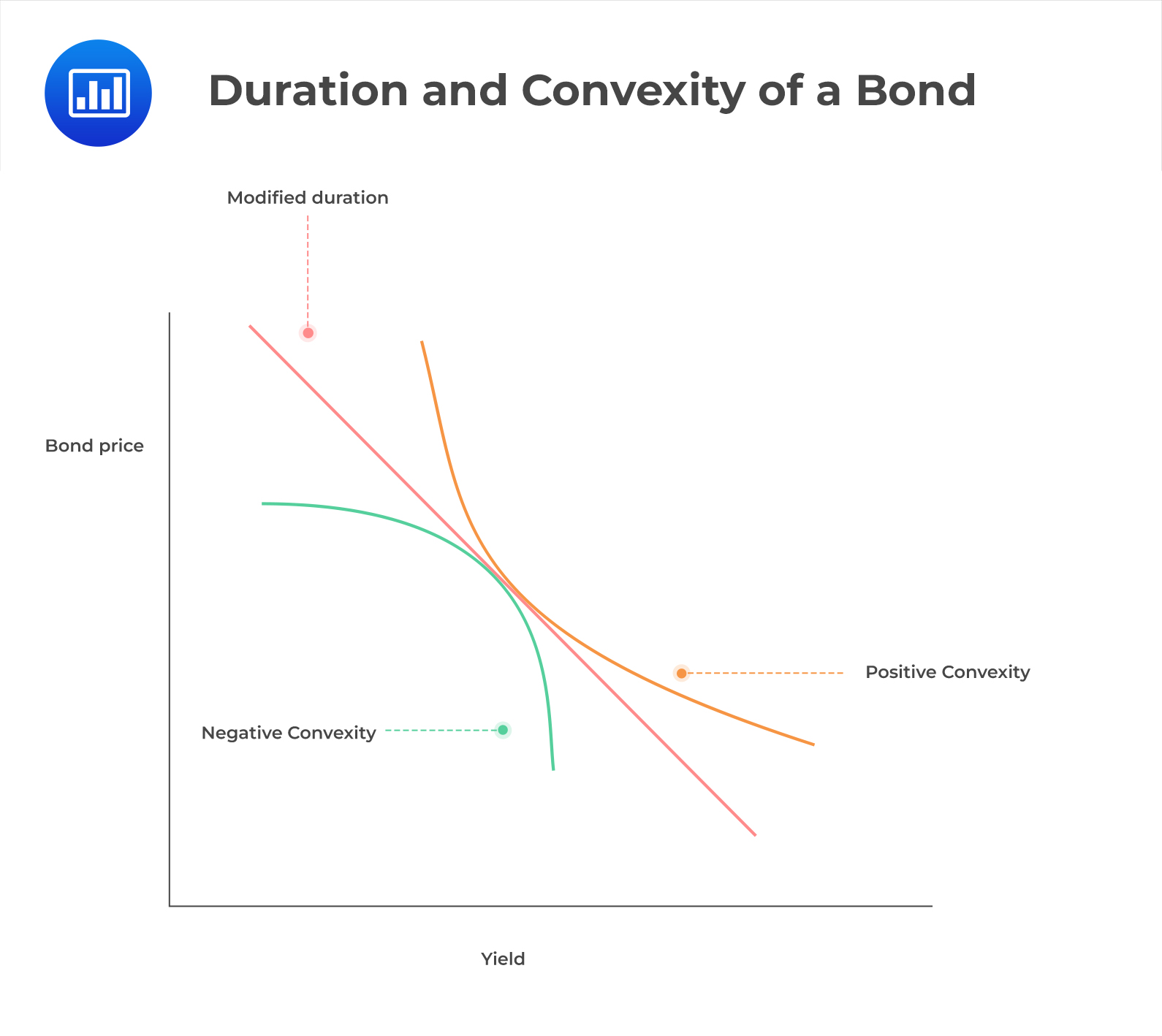

From www.researchgate.net

(PDF) Modified Duration and Convexity of a Bond Spread Duration Of A Bond Formula Generally, when interest rates rise,. Calculate the price of the bond under a different credit spread scenario. More specifically, you’ll see how to calculate. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. spread duration is the sensitivity of a security’s price to changes in. Spread Duration Of A Bond Formula.

From www.youtube.com

Bond Duration Weighted Average Macaulay Duration Duration Spread Duration Of A Bond Formula pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. in this short guide, you’ll see how to calculate the bond duration. spread duration is the sensitivity of a security’s price to changes in its credit spread. one commonly used formula to calculate spread. Spread Duration Of A Bond Formula.

From analystprep.com

Optionadjusted Spreads CFA, FRM, and Actuarial Exams Study Notes Spread Duration Of A Bond Formula one commonly used formula to calculate spread duration is: Duration measures the sensitivity of a bond to changes in interest rates. spread duration is the sensitivity of a security’s price to changes in its credit spread. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then. Spread Duration Of A Bond Formula.

From www.slideserve.com

PPT Bond Price Volatility PowerPoint Presentation ID159962 Spread Duration Of A Bond Formula in this short guide, you’ll see how to calculate the bond duration. Calculate the price of the bond under a different credit spread scenario. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. spread duration is the sensitivity of a security’s price to changes. Spread Duration Of A Bond Formula.

From analystprep.com

Exposure Measures and Their Use CFA, FRM, and Actuarial Exams Study Notes Spread Duration Of A Bond Formula More specifically, you’ll see how to calculate. Duration measures the sensitivity of a bond to changes in interest rates. in this short guide, you’ll see how to calculate the bond duration. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. Calculate the price of the. Spread Duration Of A Bond Formula.

From www.carboncollective.co

Bond Duration What It Is & How It Works, Why it Matters Spread Duration Of A Bond Formula Duration measures the sensitivity of a bond to changes in interest rates. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. More specifically, you’ll see how to calculate. in this short guide, you’ll see how to calculate the bond duration. Calculate the price of the. Spread Duration Of A Bond Formula.

From www.investopedia.com

Advanced Bond Concepts Formula Cheat Sheet Spread Duration Of A Bond Formula More specifically, you’ll see how to calculate. Duration measures the sensitivity of a bond to changes in interest rates. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. Generally, when interest rates rise,. in this short guide, you’ll see how to calculate the bond duration.. Spread Duration Of A Bond Formula.

From www.financestrategists.com

Spread Duration Definition, Components, & Applications Spread Duration Of A Bond Formula in this short guide, you’ll see how to calculate the bond duration. one commonly used formula to calculate spread duration is: pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. spread duration is the sensitivity of a security’s price to changes in its. Spread Duration Of A Bond Formula.

From www.slideserve.com

PPT Bond Duration PowerPoint Presentation, free download ID5585530 Spread Duration Of A Bond Formula Generally, when interest rates rise,. Calculate the price of the bond under a different credit spread scenario. More specifically, you’ll see how to calculate. one commonly used formula to calculate spread duration is: Duration measures the sensitivity of a bond to changes in interest rates. spread duration is the sensitivity of a security’s price to changes in its. Spread Duration Of A Bond Formula.

From quant.stackexchange.com

bond Duration. Floating rate note Quantitative Finance Stack Exchange Spread Duration Of A Bond Formula Generally, when interest rates rise,. spread duration is the sensitivity of a security’s price to changes in its credit spread. in this short guide, you’ll see how to calculate the bond duration. More specifically, you’ll see how to calculate. one commonly used formula to calculate spread duration is: Duration measures the sensitivity of a bond to changes. Spread Duration Of A Bond Formula.

From www.investopedia.com

Duration and Convexity to Measure Bond Risk Spread Duration Of A Bond Formula Duration measures the sensitivity of a bond to changes in interest rates. one commonly used formula to calculate spread duration is: Calculate the price of the bond under a different credit spread scenario. Generally, when interest rates rise,. spread duration is the sensitivity of a security’s price to changes in its credit spread. pure, or macaulay duration,. Spread Duration Of A Bond Formula.

From analystprep.com

Valuing Bonds with Embedded Options CFA, FRM, and Actuarial Exams Spread Duration Of A Bond Formula More specifically, you’ll see how to calculate. one commonly used formula to calculate spread duration is: pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. spread duration is the sensitivity of a security’s price to changes in its credit spread. in this short. Spread Duration Of A Bond Formula.

From www.educba.com

Modified Duration Formula Calculator (Example with Excel Template) Spread Duration Of A Bond Formula spread duration is the sensitivity of a security’s price to changes in its credit spread. in this short guide, you’ll see how to calculate the bond duration. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. Duration measures the sensitivity of a bond to. Spread Duration Of A Bond Formula.

From www.youtube.com

Puttable Bond Valuation and Risk YouTube Spread Duration Of A Bond Formula spread duration is the sensitivity of a security’s price to changes in its credit spread. in this short guide, you’ll see how to calculate the bond duration. Generally, when interest rates rise,. More specifically, you’ll see how to calculate. Calculate the price of the bond under a different credit spread scenario. one commonly used formula to calculate. Spread Duration Of A Bond Formula.

From granteshita.blogspot.com

Current bond price formula GrantEshita Spread Duration Of A Bond Formula one commonly used formula to calculate spread duration is: pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. spread duration is the sensitivity of a security’s price to changes in its credit spread. More specifically, you’ll see how to calculate. Calculate the price of. Spread Duration Of A Bond Formula.

From blog.deriscope.com

Bond Key Rate Duration (KRD) in Excel Calculating and Understanding Spread Duration Of A Bond Formula in this short guide, you’ll see how to calculate the bond duration. Generally, when interest rates rise,. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. Duration measures the sensitivity of a bond to changes in interest rates. More specifically, you’ll see how to calculate.. Spread Duration Of A Bond Formula.

From www.slideserve.com

PPT Bond Duration PowerPoint Presentation, free download ID5585530 Spread Duration Of A Bond Formula Duration measures the sensitivity of a bond to changes in interest rates. Generally, when interest rates rise,. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. More specifically, you’ll see how to calculate. in this short guide, you’ll see how to calculate the bond duration.. Spread Duration Of A Bond Formula.

From www.financestrategists.com

Convexity in Bond Definition, Formula, & Calculation Spread Duration Of A Bond Formula spread duration is the sensitivity of a security’s price to changes in its credit spread. Calculate the price of the bond under a different credit spread scenario. More specifically, you’ll see how to calculate. Generally, when interest rates rise,. in this short guide, you’ll see how to calculate the bond duration. Duration measures the sensitivity of a bond. Spread Duration Of A Bond Formula.

From www.youtube.com

Bond Convexity and Duration Convexity explained with example FINEd Spread Duration Of A Bond Formula Duration measures the sensitivity of a bond to changes in interest rates. More specifically, you’ll see how to calculate. in this short guide, you’ll see how to calculate the bond duration. pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. Generally, when interest rates rise,.. Spread Duration Of A Bond Formula.

From studylib.net

Bond Pricing BYU Marriott School Spread Duration Of A Bond Formula one commonly used formula to calculate spread duration is: pure, or macaulay duration, is calculated by discounting all cash flows of a bond using the proper interest rate and then time. in this short guide, you’ll see how to calculate the bond duration. Generally, when interest rates rise,. spread duration is the sensitivity of a security’s. Spread Duration Of A Bond Formula.

From www.educba.com

Macaulay Duration Formula Example with Excel Template Spread Duration Of A Bond Formula Generally, when interest rates rise,. one commonly used formula to calculate spread duration is: Calculate the price of the bond under a different credit spread scenario. Duration measures the sensitivity of a bond to changes in interest rates. spread duration is the sensitivity of a security’s price to changes in its credit spread. More specifically, you’ll see how. Spread Duration Of A Bond Formula.