What Happens To Variable Cost When Production Increases . As production increases, these costs. variable costs are costs that vary with the level of output. fixed costs have no impact of short run costs, only variable costs and revenues affect the short run production. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. a variable cost is any corporate expense that changes along with changes in production volume. if variable costs decrease, net income will increase, assuming revenue and fixed costs stay constant. understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable. In the above diagram, the variable cost curve starts from zero. fixed costs and variable costs affect the marginal cost of production only if variable costs exist.

from saylordotorg.github.io

understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable. variable costs are costs that vary with the level of output. In the above diagram, the variable cost curve starts from zero. if variable costs decrease, net income will increase, assuming revenue and fixed costs stay constant. a variable cost is any corporate expense that changes along with changes in production volume. fixed costs and variable costs affect the marginal cost of production only if variable costs exist. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. As production increases, these costs. fixed costs have no impact of short run costs, only variable costs and revenues affect the short run production.

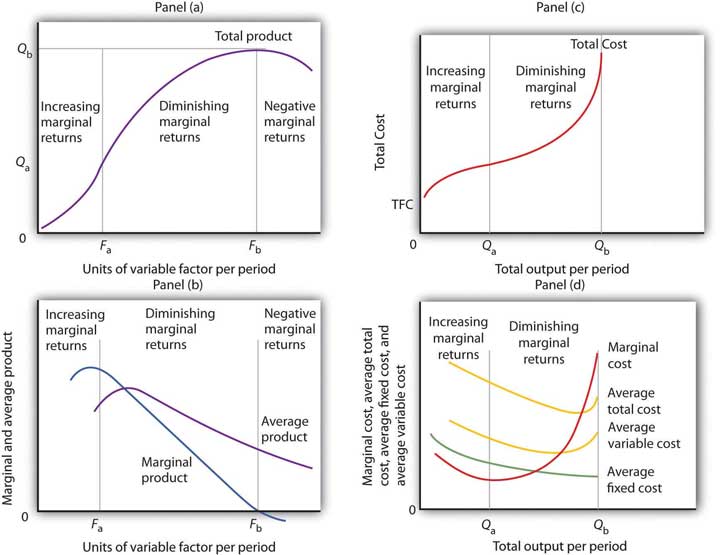

Production and Cost

What Happens To Variable Cost When Production Increases variable costs are costs that vary with the level of output. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. In the above diagram, the variable cost curve starts from zero. fixed costs and variable costs affect the marginal cost of production only if variable costs exist. variable costs are costs that vary with the level of output. a variable cost is any corporate expense that changes along with changes in production volume. if variable costs decrease, net income will increase, assuming revenue and fixed costs stay constant. As production increases, these costs. fixed costs have no impact of short run costs, only variable costs and revenues affect the short run production. understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable.

From www.intelligenteconomist.com

Theory Of Production Cost Theory Intelligent Economist What Happens To Variable Cost When Production Increases fixed costs and variable costs affect the marginal cost of production only if variable costs exist. understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output. What Happens To Variable Cost When Production Increases.

From saylordotorg.github.io

Production and Cost What Happens To Variable Cost When Production Increases As production increases, these costs. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. In the above diagram, the variable cost curve starts from zero. fixed costs have no impact of short run costs, only variable costs and revenues affect the short run. What Happens To Variable Cost When Production Increases.

From www.economicshelp.org

Diagrams of Cost Curves Economics Help What Happens To Variable Cost When Production Increases In the above diagram, the variable cost curve starts from zero. understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. a variable cost. What Happens To Variable Cost When Production Increases.

From uw.pressbooks.pub

Production Choices and Costs The Short Run Microeconomics for Managers What Happens To Variable Cost When Production Increases if variable costs decrease, net income will increase, assuming revenue and fixed costs stay constant. understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable. variable costs are costs that vary with the level of output. fixed costs have no impact of short run costs, only variable. What Happens To Variable Cost When Production Increases.

From ar.inspiredpencil.com

Total Variable Cost Graph What Happens To Variable Cost When Production Increases As production increases, these costs. fixed costs have no impact of short run costs, only variable costs and revenues affect the short run production. fixed costs and variable costs affect the marginal cost of production only if variable costs exist. variable costs are costs that vary with the level of output. In the above diagram, the variable. What Happens To Variable Cost When Production Increases.

From www.youtube.com

How to calculate Total Variable Cost Microeconomics (Cost of What Happens To Variable Cost When Production Increases a variable cost is any corporate expense that changes along with changes in production volume. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. fixed costs have no impact of short run costs, only variable costs and revenues affect the short run. What Happens To Variable Cost When Production Increases.

From ecoarun.blogspot.com

Easy Economics for Class XII 4. Diffrent total curvesTotal Utility What Happens To Variable Cost When Production Increases fixed costs and variable costs affect the marginal cost of production only if variable costs exist. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost,. What Happens To Variable Cost When Production Increases.

From mylibrary24.com

Describe the demand and supply function. My Library 24 What Happens To Variable Cost When Production Increases In the above diagram, the variable cost curve starts from zero. variable costs are costs that vary with the level of output. if variable costs decrease, net income will increase, assuming revenue and fixed costs stay constant. fixed costs have no impact of short run costs, only variable costs and revenues affect the short run production. . What Happens To Variable Cost When Production Increases.

From www.slideserve.com

PPT THEORY OF PRODUCTION AND COST PowerPoint Presentation, free What Happens To Variable Cost When Production Increases As production increases, these costs. In the above diagram, the variable cost curve starts from zero. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. fixed costs have no impact of short run costs, only variable costs and revenues affect the short run. What Happens To Variable Cost When Production Increases.

From oer.pressbooks.pub

Understanding the cost equation Accounting and Accountability What Happens To Variable Cost When Production Increases a variable cost is any corporate expense that changes along with changes in production volume. variable costs are costs that vary with the level of output. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. As production increases, these costs. fixed. What Happens To Variable Cost When Production Increases.

From www.52coding.com.cn

Microeconomics The Costs of Production NIUHE What Happens To Variable Cost When Production Increases variable costs are costs that vary with the level of output. understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable. a variable cost is any corporate expense that changes along with changes in production volume. As production increases, these costs. fixed costs and variable costs affect. What Happens To Variable Cost When Production Increases.

From courses.lumenlearning.com

Factors Affecting Supply Introduction to Business What Happens To Variable Cost When Production Increases fixed costs have no impact of short run costs, only variable costs and revenues affect the short run production. if variable costs decrease, net income will increase, assuming revenue and fixed costs stay constant. variable costs are costs that vary with the level of output. total cost, fixed cost, and variable cost each reflect different aspects. What Happens To Variable Cost When Production Increases.

From www.slideserve.com

PPT The Costs of Production PowerPoint Presentation, free download What Happens To Variable Cost When Production Increases if variable costs decrease, net income will increase, assuming revenue and fixed costs stay constant. understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable. fixed costs have no impact of short run costs, only variable costs and revenues affect the short run production. In the above diagram,. What Happens To Variable Cost When Production Increases.

From www.investopedia.com

Variable Cost What It Is and How to Calculate It What Happens To Variable Cost When Production Increases if variable costs decrease, net income will increase, assuming revenue and fixed costs stay constant. variable costs are costs that vary with the level of output. a variable cost is any corporate expense that changes along with changes in production volume. As production increases, these costs. total cost, fixed cost, and variable cost each reflect different. What Happens To Variable Cost When Production Increases.

From saylordotorg.github.io

Production and Cost What Happens To Variable Cost When Production Increases fixed costs and variable costs affect the marginal cost of production only if variable costs exist. In the above diagram, the variable cost curve starts from zero. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. As production increases, these costs. understand. What Happens To Variable Cost When Production Increases.

From saylordotorg.github.io

Production and Cost What Happens To Variable Cost When Production Increases As production increases, these costs. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. variable costs are costs that vary with the level of output. if variable costs decrease, net income will increase, assuming revenue and fixed costs stay constant. a. What Happens To Variable Cost When Production Increases.

From fyoackyhp.blob.core.windows.net

Variable Cost Marketing Definition at Albert Phillip blog What Happens To Variable Cost When Production Increases fixed costs have no impact of short run costs, only variable costs and revenues affect the short run production. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. understand the terms associated with costs in the short run—total variable cost, total fixed. What Happens To Variable Cost When Production Increases.

From ranyawang.blogspot.com

Increasing Returns To Scale Increasing returns to scale. Decreasing What Happens To Variable Cost When Production Increases understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable. variable costs are costs that vary with the level of output. As production increases, these costs. fixed costs and variable costs affect the marginal cost of production only if variable costs exist. a variable cost is any. What Happens To Variable Cost When Production Increases.

From www.youtube.com

How to derive average variable cost from production function YouTube What Happens To Variable Cost When Production Increases a variable cost is any corporate expense that changes along with changes in production volume. if variable costs decrease, net income will increase, assuming revenue and fixed costs stay constant. fixed costs have no impact of short run costs, only variable costs and revenues affect the short run production. In the above diagram, the variable cost curve. What Happens To Variable Cost When Production Increases.

From fyoqypdkr.blob.core.windows.net

Variable Cost Ratio Formula at Grace Waites blog What Happens To Variable Cost When Production Increases variable costs are costs that vary with the level of output. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. As production increases, these costs. understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost,. What Happens To Variable Cost When Production Increases.

From stock.adobe.com

variable cost concept illustration with graph and chart with blackboard What Happens To Variable Cost When Production Increases As production increases, these costs. fixed costs and variable costs affect the marginal cost of production only if variable costs exist. understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable. fixed costs have no impact of short run costs, only variable costs and revenues affect the short. What Happens To Variable Cost When Production Increases.

From www.intelligenteconomist.com

Theory Of Production Cost Theory Intelligent Economist What Happens To Variable Cost When Production Increases variable costs are costs that vary with the level of output. fixed costs have no impact of short run costs, only variable costs and revenues affect the short run production. a variable cost is any corporate expense that changes along with changes in production volume. In the above diagram, the variable cost curve starts from zero. . What Happens To Variable Cost When Production Increases.

From www.slideserve.com

PPT Chapter 2 PowerPoint Presentation ID1130963 What Happens To Variable Cost When Production Increases variable costs are costs that vary with the level of output. As production increases, these costs. fixed costs and variable costs affect the marginal cost of production only if variable costs exist. In the above diagram, the variable cost curve starts from zero. a variable cost is any corporate expense that changes along with changes in production. What Happens To Variable Cost When Production Increases.

From exyysomhs.blob.core.windows.net

Variable Cost Definition For Business at Pedro Carr blog What Happens To Variable Cost When Production Increases a variable cost is any corporate expense that changes along with changes in production volume. if variable costs decrease, net income will increase, assuming revenue and fixed costs stay constant. In the above diagram, the variable cost curve starts from zero. As production increases, these costs. fixed costs have no impact of short run costs, only variable. What Happens To Variable Cost When Production Increases.

From www.coursehero.com

[Solved] The graph illustrates an average total cost (ATC) curve (also What Happens To Variable Cost When Production Increases variable costs are costs that vary with the level of output. In the above diagram, the variable cost curve starts from zero. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. a variable cost is any corporate expense that changes along with. What Happens To Variable Cost When Production Increases.

From www.savemyexams.com

Business Costs OCR GCSE Business Revision Notes 2017 What Happens To Variable Cost When Production Increases a variable cost is any corporate expense that changes along with changes in production volume. fixed costs and variable costs affect the marginal cost of production only if variable costs exist. if variable costs decrease, net income will increase, assuming revenue and fixed costs stay constant. In the above diagram, the variable cost curve starts from zero.. What Happens To Variable Cost When Production Increases.

From hxeyjbcem.blob.core.windows.net

Explain Fixed Cost And Variable Cost With The Help Of Diagram at Susan What Happens To Variable Cost When Production Increases variable costs are costs that vary with the level of output. a variable cost is any corporate expense that changes along with changes in production volume. fixed costs have no impact of short run costs, only variable costs and revenues affect the short run production. fixed costs and variable costs affect the marginal cost of production. What Happens To Variable Cost When Production Increases.

From www.akounto.com

Variable Cost Definition, Formula & Examples Akounto What Happens To Variable Cost When Production Increases total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. In the above diagram, the variable cost curve starts from zero. fixed costs have no impact of short run costs, only variable costs and revenues affect the short run production. variable costs are. What Happens To Variable Cost When Production Increases.

From fyowwyjqa.blob.core.windows.net

Variable Cost Definition Of at Rosa Moses blog What Happens To Variable Cost When Production Increases total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. fixed costs and variable costs affect the marginal cost of production only if variable costs exist. understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost,. What Happens To Variable Cost When Production Increases.

From www.intelligenteconomist.com

Theory Of Production Cost Theory Intelligent Economist What Happens To Variable Cost When Production Increases fixed costs and variable costs affect the marginal cost of production only if variable costs exist. understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable. variable costs are costs that vary with the level of output. In the above diagram, the variable cost curve starts from zero.. What Happens To Variable Cost When Production Increases.

From penpoin.com

Total Variable Cost Examples, Curve, Importance What Happens To Variable Cost When Production Increases understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable. variable costs are costs that vary with the level of output. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. a variable. What Happens To Variable Cost When Production Increases.

From saylordotorg.github.io

Production and Cost What Happens To Variable Cost When Production Increases variable costs are costs that vary with the level of output. In the above diagram, the variable cost curve starts from zero. understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable. a variable cost is any corporate expense that changes along with changes in production volume. . What Happens To Variable Cost When Production Increases.

From www.tutor2u.net

Explaining Fixed and Variable Costs of Production tutor2u Economics What Happens To Variable Cost When Production Increases In the above diagram, the variable cost curve starts from zero. understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable. As production increases, these costs. fixed costs and variable costs affect the marginal cost of production only if variable costs exist. if variable costs decrease, net income. What Happens To Variable Cost When Production Increases.

From saylordotorg.github.io

Using the SupplyandDemand Framework What Happens To Variable Cost When Production Increases fixed costs and variable costs affect the marginal cost of production only if variable costs exist. understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable. In the above diagram, the variable cost curve starts from zero. total cost, fixed cost, and variable cost each reflect different aspects. What Happens To Variable Cost When Production Increases.

From www.akounto.com

Fixed Cost Definition, Calculation & Examples Akounto What Happens To Variable Cost When Production Increases In the above diagram, the variable cost curve starts from zero. As production increases, these costs. fixed costs and variable costs affect the marginal cost of production only if variable costs exist. a variable cost is any corporate expense that changes along with changes in production volume. if variable costs decrease, net income will increase, assuming revenue. What Happens To Variable Cost When Production Increases.