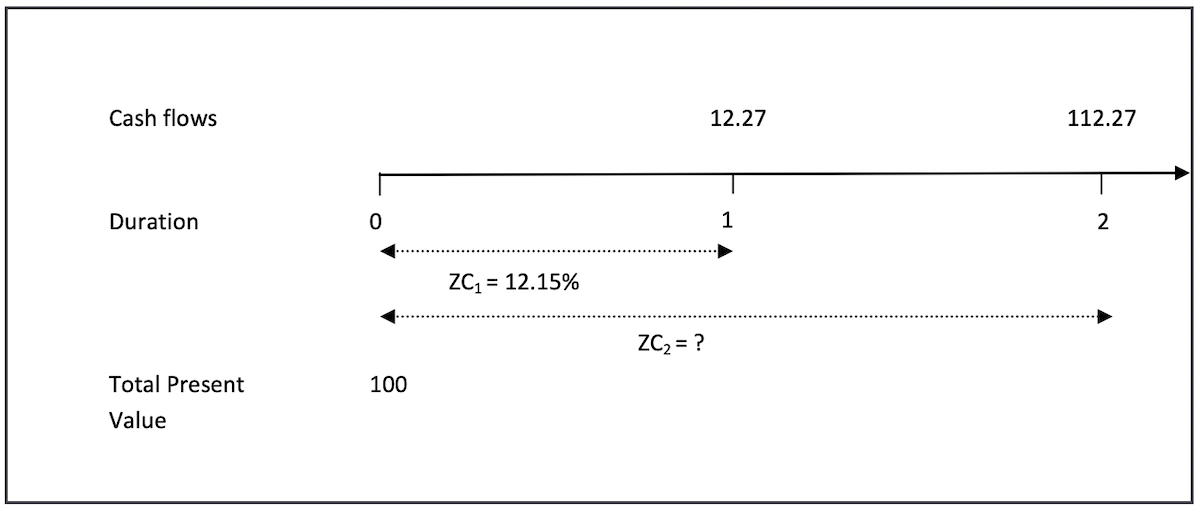

Bootstrapping Formula . Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities.

from financetrainingcourse.com

Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities.

Bootstrapping bonds to derive the zero curve

Bootstrapping Formula Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve.

From www.coursehero.com

[Solved] Standard Error from a Formula and a Bootstrap Distribution Use Bootstrapping Formula The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. Detailed step by step guide to the bootstrapping calculation process for determining. Bootstrapping Formula.

From towardsdatascience.com

An Introduction to the Bootstrap Method Towards Data Science Bootstrapping Formula Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon. Bootstrapping Formula.

From towardsdatascience.com

An Introduction to the Bootstrap Method by Lorna Yen Towards Data Bootstrapping Formula The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon. Bootstrapping Formula.

From www.slideserve.com

PPT Bond Prices and Yields PowerPoint Presentation, free download Bootstrapping Formula Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. The par curve shows the yields to maturity on government bonds with coupon payments, priced. Bootstrapping Formula.

From sheetaki.com

How to Perform Bootstrapping in Excel Sheetaki Bootstrapping Formula Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. The par curve shows the yields to maturity on government bonds with coupon payments, priced. Bootstrapping Formula.

From www.youtube.com

Bootstrap Confidence Interval for mu YouTube Bootstrapping Formula Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon. Bootstrapping Formula.

From www.youtube.com

CFA Level 1 Fixed Bootstrapping Spot & Forward Rates YouTube Bootstrapping Formula Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. The par curve shows the yields to maturity on government bonds with coupon payments, priced. Bootstrapping Formula.

From www.youtube.com

Using Bootstrapping to Calculate pvalues!!! YouTube Bootstrapping Formula The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. Detailed step by step guide to the bootstrapping calculation process for determining. Bootstrapping Formula.

From towardsdatascience.com

Tutorial for Using Confidence Intervals & Bootstrapping by Laura E Bootstrapping Formula Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. The par curve shows the yields to maturity on government bonds with coupon payments, priced. Bootstrapping Formula.

From electronics.stackexchange.com

mosfet Bootstrap capacitor calculation Which formula should I pick Bootstrapping Formula Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. The par curve shows the yields to maturity on government bonds with coupon payments, priced. Bootstrapping Formula.

From github.com

GitHub SUSE/habootstrapformula Salt formula for bootstrapping an HA Bootstrapping Formula Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. The par curve shows the yields to maturity on government bonds with coupon payments, priced. Bootstrapping Formula.

From towardsdatascience.com

Calculating Confidence Intervals with Bootstrapping by Barış Hasdemir Bootstrapping Formula Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. The par curve shows the yields to maturity on government bonds with coupon payments, priced. Bootstrapping Formula.

From www.youtube.com

Bootstrapping YouTube Bootstrapping Formula Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Detailed step by step guide to the bootstrapping calculation process for determining. Bootstrapping Formula.

From www.youtube.com

Bootstrapping and confidence intervals in ttest SPSS YouTube Bootstrapping Formula Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Detailed step by step guide to the bootstrapping calculation process for determining. Bootstrapping Formula.

From www.slideserve.com

PPT Derivatives A Primer on Bonds PowerPoint Presentation, free Bootstrapping Formula Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. The par curve shows the yields to maturity on government bonds with coupon payments, priced. Bootstrapping Formula.

From www.slideserve.com

PPT Confidence Intervals Bootstrap Distribution PowerPoint Bootstrapping Formula The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon. Bootstrapping Formula.

From www.slideserve.com

PPT Interest Rates PowerPoint Presentation, free download ID2472787 Bootstrapping Formula The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon. Bootstrapping Formula.

From www.exceldemy.com

How to Calculate Bootstrapping Spot Rates in Excel (2 Examples) Bootstrapping Formula Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. The par curve shows the yields to maturity on government bonds with coupon payments, priced. Bootstrapping Formula.

From financetrainingcourse.com

Bootstrapping Zero Curve & Forward Rates Bootstrapping Formula Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. The par curve shows the yields to maturity on government bonds with coupon payments, priced. Bootstrapping Formula.

From real-statistics.com

Bootstrapping Real Statistics Using Excel Bootstrapping Formula Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Detailed step by step guide to the bootstrapping calculation process for determining. Bootstrapping Formula.

From www.youtube.com

Bootstrap prelab (formula) part 2/2 YouTube Bootstrapping Formula Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon. Bootstrapping Formula.

From www.educba.com

Bootstrapping Examples calculation of Bootstrapping with examples Bootstrapping Formula The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. Detailed step by step guide to the bootstrapping calculation process for determining. Bootstrapping Formula.

From www.slideserve.com

PPT Confidence Intervals Bootstrap Distribution 2/6/12 PowerPoint Bootstrapping Formula The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. Detailed step by step guide to the bootstrapping calculation process for determining. Bootstrapping Formula.

From aiml.com

What is bootstrapping, and why is it a useful technique? Bootstrapping Formula Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. The par curve shows the yields to maturity on government bonds with coupon payments, priced. Bootstrapping Formula.

From www.slideserve.com

PPT Duration and Yield Changes PowerPoint Presentation, free download Bootstrapping Formula The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. Detailed step by step guide to the bootstrapping calculation process for determining. Bootstrapping Formula.

From www.educba.com

Bootstrapping Examples calculation of Bootstrapping with examples Bootstrapping Formula Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. The par curve shows the yields to maturity on government bonds with coupon payments, priced. Bootstrapping Formula.

From data-flair.training

Bootstrapping in R Single guide for all concepts DataFlair Bootstrapping Formula Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. The par curve shows the yields to maturity on government bonds with coupon payments, priced. Bootstrapping Formula.

From financetrainingcourse.com

Bootstrapping bonds to derive the zero curve Bootstrapping Formula Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Detailed step by step guide to the bootstrapping calculation process for determining. Bootstrapping Formula.

From inchainsforchrist.org

Bootstrapping Finance Example Bootstrapping Formula Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. The par curve shows the yields to maturity on government bonds with coupon payments, priced. Bootstrapping Formula.

From www.slideserve.com

PPT Derivatives A Primer on Bonds PowerPoint Presentation, free Bootstrapping Formula The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. Detailed step by step guide to the bootstrapping calculation process for determining. Bootstrapping Formula.

From sheetaki.com

How to Perform Bootstrapping in Excel Sheetaki Bootstrapping Formula Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Detailed step by step guide to the bootstrapping calculation process for determining. Bootstrapping Formula.

From www.pyme.es

Conoce la fórmula bootstrapping. Aprenden de financiamiento Bootstrapping Formula The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon. Bootstrapping Formula.

From www.statology.org

How to Perform Bootstrapping in R (With Examples) Bootstrapping Formula The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon. Bootstrapping Formula.

From www.youtube.com

Bootstrapping and Resampling in Statistics with Example Statistics Bootstrapping Formula The par curve shows the yields to maturity on government bonds with coupon payments, priced at par, over a range of maturities. Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. Detailed step by step guide to the bootstrapping calculation process for determining. Bootstrapping Formula.

From www.statology.org

How to Perform Bootstrapping in Excel (With Example) Bootstrapping Formula Bootstrapping spot rates using the par curve is a very important method that allows investors to derive zero coupon interest rates from the par rate curve. Detailed step by step guide to the bootstrapping calculation process for determining zero and forward rate term structures for. The par curve shows the yields to maturity on government bonds with coupon payments, priced. Bootstrapping Formula.