Fixed Costs Definition Economics Quizlet . Whether you produce a lot. study with quizlet and memorize flashcards containing terms like fixed cost, variable costs, total cost and more. Cost that rises or falls depending on the quantity. A cost that does not change of goods is produced. explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of. fixed costs are costs independent of the size of production. fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. They remain constant and fixed whether or not anything is produced.

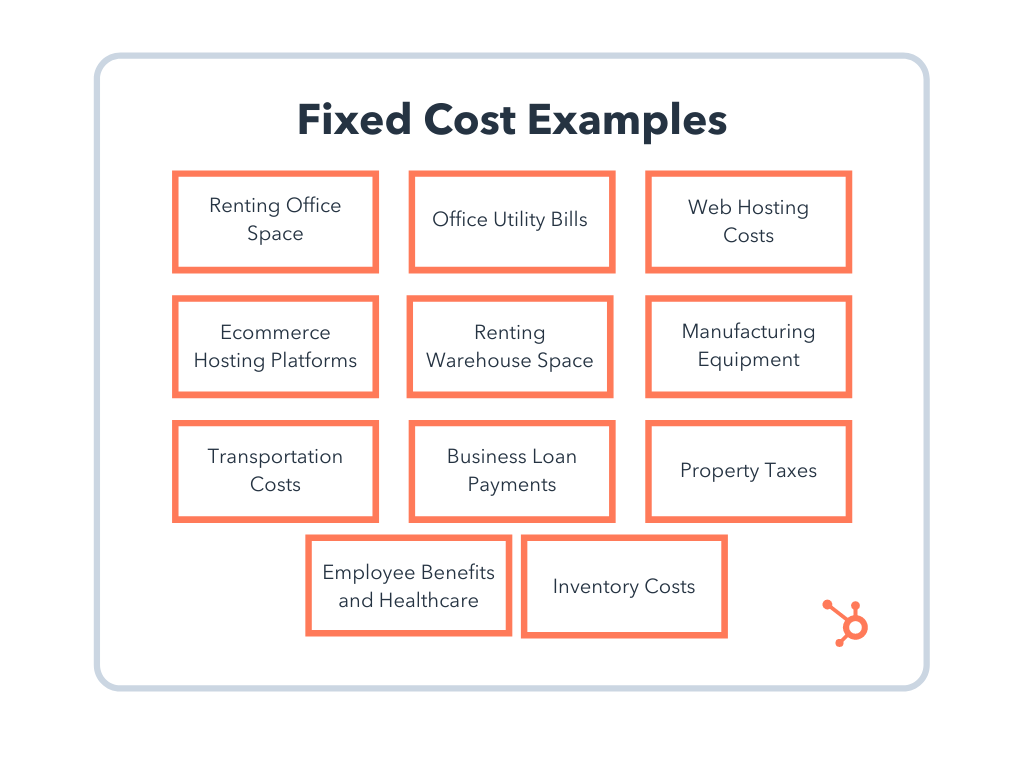

from blog.hubspot.com

fixed costs are costs independent of the size of production. They remain constant and fixed whether or not anything is produced. fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of. Whether you produce a lot. A cost that does not change of goods is produced. study with quizlet and memorize flashcards containing terms like fixed cost, variable costs, total cost and more. Cost that rises or falls depending on the quantity. explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production.

Fixed Cost What It Is & How to Calculate It

Fixed Costs Definition Economics Quizlet Cost that rises or falls depending on the quantity. A cost that does not change of goods is produced. fixed costs are costs independent of the size of production. They remain constant and fixed whether or not anything is produced. Whether you produce a lot. Cost that rises or falls depending on the quantity. explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of. study with quizlet and memorize flashcards containing terms like fixed cost, variable costs, total cost and more. fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the.

From makalah31dsa.blogspot.com

Finance Charges Economics Meaning Fixed Cost Definition 6 Examples Vs Fixed Costs Definition Economics Quizlet in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. They remain constant and fixed whether or not anything is produced. fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. Cost that rises. Fixed Costs Definition Economics Quizlet.

From quizizz.com

Fixed and Variable costs Business Quizizz Fixed Costs Definition Economics Quizlet explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. Whether you produce a lot. Cost that rises or falls depending on the quantity. in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. . Fixed Costs Definition Economics Quizlet.

From www.tutor2u.net

Explaining Fixed and Variable Costs of… Economics tutor2u Fixed Costs Definition Economics Quizlet Cost that rises or falls depending on the quantity. They remain constant and fixed whether or not anything is produced. explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. A cost that does not change of goods is produced. Whether you produce a lot. fixed costs are. Fixed Costs Definition Economics Quizlet.

From giollplui.blob.core.windows.net

What Are Examples Of Fixed Costs And Variable Costs For A Farm Quizlet Fixed Costs Definition Economics Quizlet explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. Whether you produce a lot. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of. Cost that rises or falls depending on the quantity. fixed costs. Fixed Costs Definition Economics Quizlet.

From giownspwj.blob.core.windows.net

What Is The Definition Of A Fixed Expense Quizlet at Chris Simons blog Fixed Costs Definition Economics Quizlet fixed costs are costs independent of the size of production. Whether you produce a lot. A cost that does not change of goods is produced. study with quizlet and memorize flashcards containing terms like fixed cost, variable costs, total cost and more. fixed costs are expenditures that do not change regardless of the level of production, at. Fixed Costs Definition Economics Quizlet.

From exyulavkl.blob.core.windows.net

Fixed Costs Are Associated With at Arthur Reynolds blog Fixed Costs Definition Economics Quizlet A cost that does not change of goods is produced. explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. Whether you produce a lot. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of. study. Fixed Costs Definition Economics Quizlet.

From www.akounto.com

Fixed Cost Definition, Calculation & Examples Akounto Fixed Costs Definition Economics Quizlet explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. A cost that does not change of goods is produced. fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. fixed costs are costs independent of. Fixed Costs Definition Economics Quizlet.

From giownspwj.blob.core.windows.net

What Is The Definition Of A Fixed Expense Quizlet at Chris Simons blog Fixed Costs Definition Economics Quizlet total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of. A cost that does not change of goods is produced. Whether you produce a lot. explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. They remain. Fixed Costs Definition Economics Quizlet.

From learnbusinessconcepts.com

Fixed Cost Explanation, Formula, Calculation, and Examples Fixed Costs Definition Economics Quizlet study with quizlet and memorize flashcards containing terms like fixed cost, variable costs, total cost and more. A cost that does not change of goods is produced. Whether you produce a lot. in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. fixed costs. Fixed Costs Definition Economics Quizlet.

From quizlet.com

In the earlier example, the fixed costs are split 4 million Quizlet Fixed Costs Definition Economics Quizlet Whether you produce a lot. Cost that rises or falls depending on the quantity. study with quizlet and memorize flashcards containing terms like fixed cost, variable costs, total cost and more. fixed costs are costs independent of the size of production. explore how to think about average fixed, variable, and marginal costs, and how to calculate them,. Fixed Costs Definition Economics Quizlet.

From www.toolazytostudy.com

Fixed costs and variable costs economics notes explained with diagrams Fixed Costs Definition Economics Quizlet explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. study with quizlet and memorize flashcards containing terms like fixed cost, variable costs, total. Fixed Costs Definition Economics Quizlet.

From giollplui.blob.core.windows.net

What Are Examples Of Fixed Costs And Variable Costs For A Farm Quizlet Fixed Costs Definition Economics Quizlet study with quizlet and memorize flashcards containing terms like fixed cost, variable costs, total cost and more. fixed costs are costs independent of the size of production. fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. explore how to think about average fixed, variable,. Fixed Costs Definition Economics Quizlet.

From www.marketing91.com

Average Fixed Cost Definition, Formula and Examples Marketing91 Fixed Costs Definition Economics Quizlet A cost that does not change of goods is produced. explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. in accounting and economics, fixed costs,. Fixed Costs Definition Economics Quizlet.

From www.youtube.com

Fixed cost — definition of FIXED COST YouTube Fixed Costs Definition Economics Quizlet in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. fixed costs are costs independent of the size of production. A cost that does not change of goods is produced. explore how to think about average fixed, variable, and marginal costs, and how to. Fixed Costs Definition Economics Quizlet.

From boycewire.com

Fixed Costs Definition Fixed Costs Definition Economics Quizlet fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. study with quizlet and memorize flashcards containing terms like fixed cost, variable costs,. Fixed Costs Definition Economics Quizlet.

From www.superfastcpa.com

What is a Fixed Cost? Fixed Costs Definition Economics Quizlet A cost that does not change of goods is produced. in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. They remain constant and fixed whether or not anything is produced. Whether you produce a lot. fixed costs are costs independent of the size of. Fixed Costs Definition Economics Quizlet.

From education-portal.com

Fixed Costs Definition, Formula & Examples Video & Lesson Transcript Fixed Costs Definition Economics Quizlet Whether you produce a lot. explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. A cost that does not change of goods is produced. fixed costs are costs independent of the size of production. They remain constant and fixed whether or not anything is produced. in. Fixed Costs Definition Economics Quizlet.

From tutorstips.com

Difference between Fixed Cost and Variable Cost Tutor's Tips Fixed Costs Definition Economics Quizlet A cost that does not change of goods is produced. in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. Cost that rises or falls depending on the quantity. fixed costs are expenditures that do not change regardless of the level of production, at least. Fixed Costs Definition Economics Quizlet.

From efinancemanagement.com

Fixed Cost What It Is And What's Its Importance? Fixed Costs Definition Economics Quizlet in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. study with quizlet and memorize flashcards containing terms like fixed cost, variable costs, total. Fixed Costs Definition Economics Quizlet.

From blog.hubspot.com

Fixed Cost What It Is & How to Calculate It Fixed Costs Definition Economics Quizlet explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. Cost that rises or falls depending on the quantity. They remain constant and fixed whether or not anything is produced. Whether you produce a lot. A cost that does not change of goods is produced. fixed costs are. Fixed Costs Definition Economics Quizlet.

From blog.avada.io

How to Calculate Fixed Cost? Formula, Guide and Examples Fixed Costs Definition Economics Quizlet study with quizlet and memorize flashcards containing terms like fixed cost, variable costs, total cost and more. Cost that rises or falls depending on the quantity. explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. fixed costs are costs independent of the size of production. A. Fixed Costs Definition Economics Quizlet.

From www.educba.com

What is Fixed Cost? Formula & Examples Advantages & Disadvantages Fixed Costs Definition Economics Quizlet explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. Whether you produce a lot. in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. Cost that rises or falls depending on the quantity. . Fixed Costs Definition Economics Quizlet.

From www.investopedia.com

Fixed Cost What It Is and How It’s Used in Business Fixed Costs Definition Economics Quizlet Cost that rises or falls depending on the quantity. A cost that does not change of goods is produced. fixed costs are costs independent of the size of production. explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. in accounting and economics, fixed costs, also known. Fixed Costs Definition Economics Quizlet.

From hxeeggrze.blob.core.windows.net

Fixed Cost And Variable Cost Definition Pdf at Crystal Robertson blog Fixed Costs Definition Economics Quizlet study with quizlet and memorize flashcards containing terms like fixed cost, variable costs, total cost and more. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of. A cost that does not change of goods is produced. explore how to think about average fixed, variable, and. Fixed Costs Definition Economics Quizlet.

From www.gobankingrates.com

Fixed Expenses vs. Variable Expenses for Budgeting What's the Fixed Costs Definition Economics Quizlet Whether you produce a lot. A cost that does not change of goods is produced. in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. They remain constant and fixed whether or not anything is produced. study with quizlet and memorize flashcards containing terms like. Fixed Costs Definition Economics Quizlet.

From www.1099cafe.com

What is a Fixed Cost Variable vs Fixed Expenses — 1099 Cafe Fixed Costs Definition Economics Quizlet Cost that rises or falls depending on the quantity. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of. Whether you produce a lot. fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. A cost. Fixed Costs Definition Economics Quizlet.

From giocabmjp.blob.core.windows.net

Examples Of Common Fixed Costs at Miguel Paradise blog Fixed Costs Definition Economics Quizlet fixed costs are costs independent of the size of production. study with quizlet and memorize flashcards containing terms like fixed cost, variable costs, total cost and more. in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. Cost that rises or falls depending on. Fixed Costs Definition Economics Quizlet.

From efinancemanagement.com

Variable Costs and Fixed Costs Fixed Costs Definition Economics Quizlet total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of. Whether you produce a lot. fixed costs are costs independent of the size of production. They remain constant and fixed whether or not anything is produced. fixed costs are expenditures that do not change regardless of. Fixed Costs Definition Economics Quizlet.

From exyglzsus.blob.core.windows.net

Which Of The Following Are Examples Of Fixed Costs Quizlet at Marcie Fixed Costs Definition Economics Quizlet study with quizlet and memorize flashcards containing terms like fixed cost, variable costs, total cost and more. Cost that rises or falls depending on the quantity. A cost that does not change of goods is produced. fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. They. Fixed Costs Definition Economics Quizlet.

From www.educba.com

Fixed Cost Vs Variable Cost Top 12 Key Differences & Examples Fixed Costs Definition Economics Quizlet A cost that does not change of goods is produced. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of. Whether you produce a lot. study with quizlet and memorize flashcards containing terms like fixed cost, variable costs, total cost and more. Cost that rises or falls. Fixed Costs Definition Economics Quizlet.

From quizlet.com

Average Cost Curve Diagram Quizlet Fixed Costs Definition Economics Quizlet A cost that does not change of goods is produced. in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. fixed costs are costs independent of the size of production. They remain constant and fixed whether or not anything is produced. total cost, fixed. Fixed Costs Definition Economics Quizlet.

From www.slideserve.com

PPT Chapter 27 PowerPoint Presentation, free download ID6557622 Fixed Costs Definition Economics Quizlet total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of. A cost that does not change of goods is produced. explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. fixed costs are expenditures that do. Fixed Costs Definition Economics Quizlet.

From www.hashmicro.com

Fixed Costs and Variable Costs Definition and Examples Fixed Costs Definition Economics Quizlet total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of. A cost that does not change of goods is produced. in accounting and economics, fixed costs, also known as indirect costs or overhead costs, are business expenses that are not dependent on the. fixed costs are. Fixed Costs Definition Economics Quizlet.

From quickbooks.intuit.com

Operating Costs Definition, Formula & Examples QuickBooks Fixed Costs Definition Economics Quizlet Whether you produce a lot. explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of. Cost that rises or falls depending on the quantity. A cost that. Fixed Costs Definition Economics Quizlet.

From exyglzsus.blob.core.windows.net

Which Of The Following Are Examples Of Fixed Costs Quizlet at Marcie Fixed Costs Definition Economics Quizlet They remain constant and fixed whether or not anything is produced. explore how to think about average fixed, variable, and marginal costs, and how to calculate them, using a firm's production. A cost that does not change of goods is produced. total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over. Fixed Costs Definition Economics Quizlet.