Supplies Between Connected Parties Vat . For vat purposes, a “supply” is normally only made between separate legal entities; This book is a guide about the way that the vat rules apply to transactions between associated businesses, based on my interpretation of the legislation and hmrc guidance at the date. In general, the supply of staff is subject to vat at the standard rate. An area that often causes confusion is the recharge of staff between connected companies. The most common being sole. There are however specific time and value of supply rules. For the correct vat treatment, it is necessary to determine which of the supplies should be considered as movable (i.e. The general rule is that the value of a supply is the consideration (price) paid for. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals;

from plvat.co.uk

An area that often causes confusion is the recharge of staff between connected companies. The most common being sole. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; This book is a guide about the way that the vat rules apply to transactions between associated businesses, based on my interpretation of the legislation and hmrc guidance at the date. The general rule is that the value of a supply is the consideration (price) paid for. For the correct vat treatment, it is necessary to determine which of the supplies should be considered as movable (i.e. There are however specific time and value of supply rules. In general, the supply of staff is subject to vat at the standard rate. For vat purposes, a “supply” is normally only made between separate legal entities;

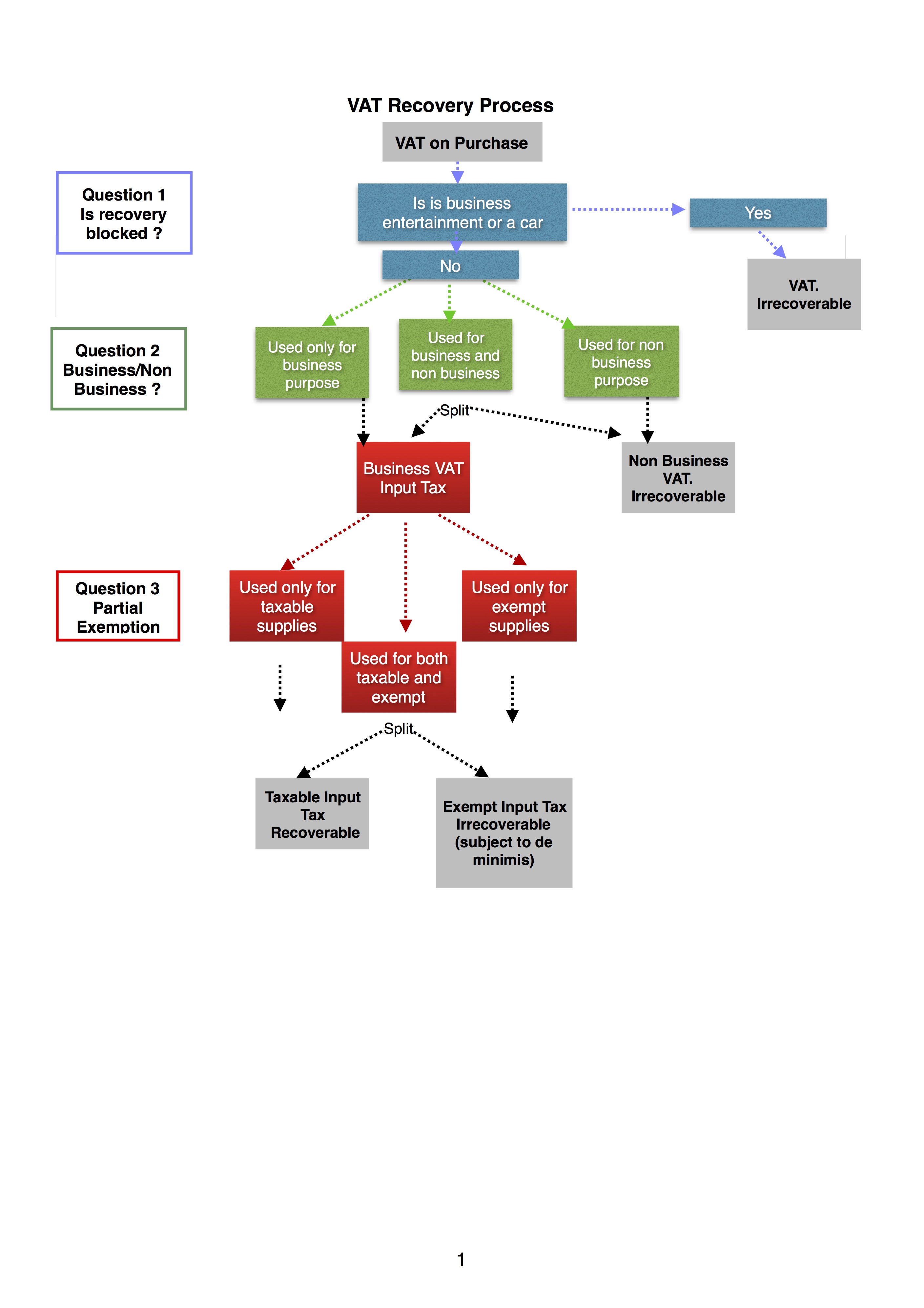

VAT recovery PLVAT

Supplies Between Connected Parties Vat In general, the supply of staff is subject to vat at the standard rate. This book is a guide about the way that the vat rules apply to transactions between associated businesses, based on my interpretation of the legislation and hmrc guidance at the date. The most common being sole. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; For vat purposes, a “supply” is normally only made between separate legal entities; In general, the supply of staff is subject to vat at the standard rate. An area that often causes confusion is the recharge of staff between connected companies. The general rule is that the value of a supply is the consideration (price) paid for. For the correct vat treatment, it is necessary to determine which of the supplies should be considered as movable (i.e. There are however specific time and value of supply rules.

From www.pwc.com

Chain transactions and VAT Supplies Between Connected Parties Vat There are however specific time and value of supply rules. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; In general, the supply of staff is subject to vat at the standard rate. For the correct vat treatment, it is necessary to determine which of the supplies. Supplies Between Connected Parties Vat.

From signalx.ai

What Is Supply Under GST? A Responsible Taxpayer SignalX AI Supplies Between Connected Parties Vat In general, the supply of staff is subject to vat at the standard rate. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; The most common being sole. For the correct vat treatment, it is necessary to determine which of the supplies should be considered as movable. Supplies Between Connected Parties Vat.

From www.webinterpret.com

The comprehensive guide to VAT in Europe for sellers Supplies Between Connected Parties Vat There are however specific time and value of supply rules. For the correct vat treatment, it is necessary to determine which of the supplies should be considered as movable (i.e. In general, the supply of staff is subject to vat at the standard rate. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are. Supplies Between Connected Parties Vat.

From www.mercuriusit.com

Explaining the Strategic Tax Change for Construction Businesses Supplies Between Connected Parties Vat There are however specific time and value of supply rules. This book is a guide about the way that the vat rules apply to transactions between associated businesses, based on my interpretation of the legislation and hmrc guidance at the date. The most common being sole. The general rule is that the value of a supply is the consideration (price). Supplies Between Connected Parties Vat.

From www.indigogroupservices.com

A Guide to the VAT Domestic Reverse Charge in the Construction Industry Supplies Between Connected Parties Vat For vat purposes, a “supply” is normally only made between separate legal entities; In general, the supply of staff is subject to vat at the standard rate. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; An area that often causes confusion is the recharge of staff. Supplies Between Connected Parties Vat.

From www.detailsolicitors.com

THE IMPACT OF THE VALUE ADDED TAX (MODIFICATION ORDER) 2020 ON Supplies Between Connected Parties Vat The most common being sole. There are however specific time and value of supply rules. In general, the supply of staff is subject to vat at the standard rate. An area that often causes confusion is the recharge of staff between connected companies. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat. Supplies Between Connected Parties Vat.

From tallysolutions.com

Export of goods to GCC VAT implementing States Tally.ERP 9 Supplies Between Connected Parties Vat The most common being sole. The general rule is that the value of a supply is the consideration (price) paid for. There are however specific time and value of supply rules. This book is a guide about the way that the vat rules apply to transactions between associated businesses, based on my interpretation of the legislation and hmrc guidance at. Supplies Between Connected Parties Vat.

From www.digilaw.in

Related Party Transactions Statutory Compliances and Disclosures Supplies Between Connected Parties Vat A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; In general, the supply of staff is subject to vat at the standard rate. For vat purposes, a “supply” is normally only made between separate legal entities; The most common being sole. There are however specific time and. Supplies Between Connected Parties Vat.

From plvat.co.uk

VAT recovery PLVAT Supplies Between Connected Parties Vat In general, the supply of staff is subject to vat at the standard rate. There are however specific time and value of supply rules. For vat purposes, a “supply” is normally only made between separate legal entities; A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; For. Supplies Between Connected Parties Vat.

From thevatconsultant.com

VAT Registration UAE , VAT Registration Dubai, UAE VAT Registration Supplies Between Connected Parties Vat In general, the supply of staff is subject to vat at the standard rate. For vat purposes, a “supply” is normally only made between separate legal entities; The most common being sole. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; An area that often causes confusion. Supplies Between Connected Parties Vat.

From www.rousepartners.co.uk

Construction VAT Reverse Charge What are the new rules? Rouse Supplies Between Connected Parties Vat For vat purposes, a “supply” is normally only made between separate legal entities; The most common being sole. For the correct vat treatment, it is necessary to determine which of the supplies should be considered as movable (i.e. An area that often causes confusion is the recharge of staff between connected companies. A cleaning company could have two divisions and. Supplies Between Connected Parties Vat.

From mpm.ph

Difference Between VAT and NonVAT Supplies Between Connected Parties Vat The general rule is that the value of a supply is the consideration (price) paid for. For vat purposes, a “supply” is normally only made between separate legal entities; There are however specific time and value of supply rules. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private. Supplies Between Connected Parties Vat.

From instafiling.com

Ultimate Guide To Reverse Charge Mechanism (RCM) in GST Supplies Between Connected Parties Vat This book is a guide about the way that the vat rules apply to transactions between associated businesses, based on my interpretation of the legislation and hmrc guidance at the date. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; An area that often causes confusion is. Supplies Between Connected Parties Vat.

From www.confiduss.com

Tax solutions VAT triangulation Confidus Solutions Supplies Between Connected Parties Vat There are however specific time and value of supply rules. The most common being sole. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; In general, the supply of staff is subject to vat at the standard rate. This book is a guide about the way that. Supplies Between Connected Parties Vat.

From www.tide.co

A guide to domestic VAT reverse charges Tide Business Supplies Between Connected Parties Vat This book is a guide about the way that the vat rules apply to transactions between associated businesses, based on my interpretation of the legislation and hmrc guidance at the date. The most common being sole. In general, the supply of staff is subject to vat at the standard rate. For the correct vat treatment, it is necessary to determine. Supplies Between Connected Parties Vat.

From www.yumpu.com

Zerorated and exempt supplies Supplies Between Connected Parties Vat The most common being sole. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; This book is a guide about the way that the vat rules apply to transactions between associated businesses, based on my interpretation of the legislation and hmrc guidance at the date. There are. Supplies Between Connected Parties Vat.

From www.vertexinc.com

Brexit’s Impact on VAT Triangulation Vertex, Inc. Supplies Between Connected Parties Vat The most common being sole. In general, the supply of staff is subject to vat at the standard rate. For the correct vat treatment, it is necessary to determine which of the supplies should be considered as movable (i.e. This book is a guide about the way that the vat rules apply to transactions between associated businesses, based on my. Supplies Between Connected Parties Vat.

From www.brightpay.co.uk

CIS VAT Domestic Reverse Charge BrightPay Documentation Supplies Between Connected Parties Vat For the correct vat treatment, it is necessary to determine which of the supplies should be considered as movable (i.e. For vat purposes, a “supply” is normally only made between separate legal entities; The general rule is that the value of a supply is the consideration (price) paid for. A cleaning company could have two divisions and supply customers accordingly,. Supplies Between Connected Parties Vat.

From connectresources.ae

VAT in UAE 2024 Federal Tax Authority Everything You Need about Supplies Between Connected Parties Vat The general rule is that the value of a supply is the consideration (price) paid for. The most common being sole. An area that often causes confusion is the recharge of staff between connected companies. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; In general, the. Supplies Between Connected Parties Vat.

From www.youtube.com

What is VAT ? Main Types Advantages and Disadvantages For Supplies Between Connected Parties Vat In general, the supply of staff is subject to vat at the standard rate. An area that often causes confusion is the recharge of staff between connected companies. This book is a guide about the way that the vat rules apply to transactions between associated businesses, based on my interpretation of the legislation and hmrc guidance at the date. The. Supplies Between Connected Parties Vat.

From cekindo.com

Indonesia VAT Everything You Need to Know Cekindo Indonesia Supplies Between Connected Parties Vat There are however specific time and value of supply rules. For the correct vat treatment, it is necessary to determine which of the supplies should be considered as movable (i.e. In general, the supply of staff is subject to vat at the standard rate. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are. Supplies Between Connected Parties Vat.

From elevateauditing.com

VAT Services in UAE vat registration services Dubai Supplies Between Connected Parties Vat There are however specific time and value of supply rules. An area that often causes confusion is the recharge of staff between connected companies. The general rule is that the value of a supply is the consideration (price) paid for. For the correct vat treatment, it is necessary to determine which of the supplies should be considered as movable (i.e.. Supplies Between Connected Parties Vat.

From ardaccounting.com

Zero rated, Exempt VAT supplies Al Ard Aljadeeda Accounting Supplies Between Connected Parties Vat An area that often causes confusion is the recharge of staff between connected companies. The general rule is that the value of a supply is the consideration (price) paid for. For vat purposes, a “supply” is normally only made between separate legal entities; A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat. Supplies Between Connected Parties Vat.

From www.vrogue.co

Difference Between Zero Rated Vat Vs Exempted Vat In vrogue.co Supplies Between Connected Parties Vat A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; For the correct vat treatment, it is necessary to determine which of the supplies should be considered as movable (i.e. In general, the supply of staff is subject to vat at the standard rate. An area that often. Supplies Between Connected Parties Vat.

From www.streetwisesubbie.com

VAT Reverse Charge For Building And Construction Services Supplies Between Connected Parties Vat There are however specific time and value of supply rules. The general rule is that the value of a supply is the consideration (price) paid for. An area that often causes confusion is the recharge of staff between connected companies. For vat purposes, a “supply” is normally only made between separate legal entities; The most common being sole. This book. Supplies Between Connected Parties Vat.

From www.goforma.com

The £85k VAT Threshold 19 Things You Need to Know about VAT Supplies Between Connected Parties Vat In general, the supply of staff is subject to vat at the standard rate. The most common being sole. The general rule is that the value of a supply is the consideration (price) paid for. For vat purposes, a “supply” is normally only made between separate legal entities; This book is a guide about the way that the vat rules. Supplies Between Connected Parties Vat.

From www.pwc.com

Chain transactions and VAT Supplies Between Connected Parties Vat The general rule is that the value of a supply is the consideration (price) paid for. There are however specific time and value of supply rules. The most common being sole. An area that often causes confusion is the recharge of staff between connected companies. This book is a guide about the way that the vat rules apply to transactions. Supplies Between Connected Parties Vat.

From www.pinterest.com

VAT Transactions Entries and Examples Accounting & Taxation Example Supplies Between Connected Parties Vat The most common being sole. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; The general rule is that the value of a supply is the consideration (price) paid for. For the correct vat treatment, it is necessary to determine which of the supplies should be considered. Supplies Between Connected Parties Vat.

From accotax.co.uk

What's the difference between exempt items & Zero Rated Vat items? Supplies Between Connected Parties Vat The general rule is that the value of a supply is the consideration (price) paid for. There are however specific time and value of supply rules. For the correct vat treatment, it is necessary to determine which of the supplies should be considered as movable (i.e. An area that often causes confusion is the recharge of staff between connected companies.. Supplies Between Connected Parties Vat.

From www.lexology.com

Brexit What is the applicable VAT regime for supplies of goods between Supplies Between Connected Parties Vat There are however specific time and value of supply rules. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; This book is a guide about the way that the vat rules apply to transactions between associated businesses, based on my interpretation of the legislation and hmrc guidance. Supplies Between Connected Parties Vat.

From www.youtube.com

Difference between Zerorated & Exempt VAT Supplies in UAE YouTube Supplies Between Connected Parties Vat In general, the supply of staff is subject to vat at the standard rate. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; The most common being sole. The general rule is that the value of a supply is the consideration (price) paid for. There are however. Supplies Between Connected Parties Vat.

From www.audiix.com

Zerorated and exempt supplies Supplies Between Connected Parties Vat This book is a guide about the way that the vat rules apply to transactions between associated businesses, based on my interpretation of the legislation and hmrc guidance at the date. The most common being sole. In general, the supply of staff is subject to vat at the standard rate. For the correct vat treatment, it is necessary to determine. Supplies Between Connected Parties Vat.

From www.pmm.co.uk

VAT Reverse Charge on building and construction supplies A handy guide Supplies Between Connected Parties Vat This book is a guide about the way that the vat rules apply to transactions between associated businesses, based on my interpretation of the legislation and hmrc guidance at the date. For vat purposes, a “supply” is normally only made between separate legal entities; The general rule is that the value of a supply is the consideration (price) paid for.. Supplies Between Connected Parties Vat.

From thevatconsultant.com

VAT Registration UAE , VAT Registration Dubai, UAE VAT Registration Supplies Between Connected Parties Vat There are however specific time and value of supply rules. In general, the supply of staff is subject to vat at the standard rate. For the correct vat treatment, it is necessary to determine which of the supplies should be considered as movable (i.e. This book is a guide about the way that the vat rules apply to transactions between. Supplies Between Connected Parties Vat.

From www.taxadvisermagazine.com

Partial exemption in VAT registered businesses Tax Adviser Supplies Between Connected Parties Vat The most common being sole. A cleaning company could have two divisions and supply customers accordingly, depending on whether they are vat registered businesses or private individuals; For the correct vat treatment, it is necessary to determine which of the supplies should be considered as movable (i.e. This book is a guide about the way that the vat rules apply. Supplies Between Connected Parties Vat.