Rental Property Loss Rules . It can be used to. As a result of a casualty or theft, you may have a loss related to your rental property. The rental real estate loss allowance is what the irs allows you to deduct in passive losses from real estate each year from your earned income. If you have any personal use of a dwelling unit that you rent (including a vacation home or a residence in which you rent a room),. Even though rental income or loss generally is passive, a special rule allows qualifying individuals and estates to offset up. The rental real estate loss allowance is a federal tax deduction of up to $25,000 a year for taxpayers who take a loss on rental property. Rental losses are always classified as passive losses for tax purposes. Here's the basic rule about rental losses you need to know: Rental property losses are deductible when they’re applied to passive income, and you can carry them forward from.

from www.uslegalforms.com

Rental losses are always classified as passive losses for tax purposes. The rental real estate loss allowance is what the irs allows you to deduct in passive losses from real estate each year from your earned income. Here's the basic rule about rental losses you need to know: It can be used to. The rental real estate loss allowance is a federal tax deduction of up to $25,000 a year for taxpayers who take a loss on rental property. Rental property losses are deductible when they’re applied to passive income, and you can carry them forward from. Even though rental income or loss generally is passive, a special rule allows qualifying individuals and estates to offset up. As a result of a casualty or theft, you may have a loss related to your rental property. If you have any personal use of a dwelling unit that you rent (including a vacation home or a residence in which you rent a room),.

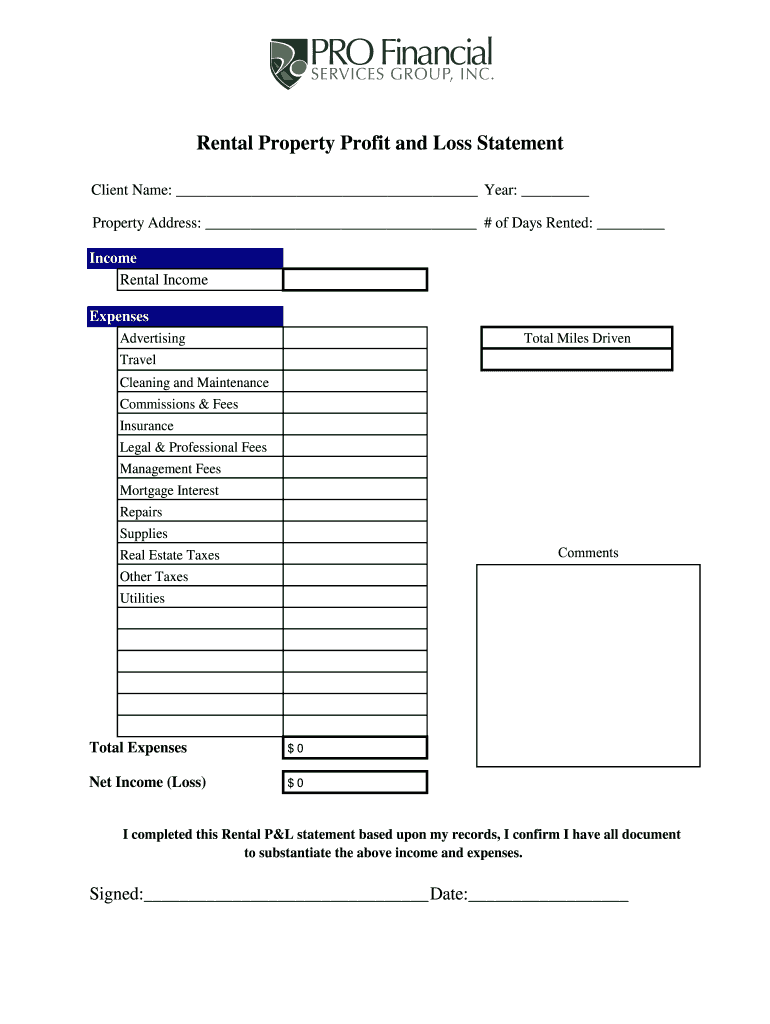

PRO Financial Rental Property Profit and Loss Statement Fill and Sign

Rental Property Loss Rules The rental real estate loss allowance is what the irs allows you to deduct in passive losses from real estate each year from your earned income. Rental property losses are deductible when they’re applied to passive income, and you can carry them forward from. Rental losses are always classified as passive losses for tax purposes. Even though rental income or loss generally is passive, a special rule allows qualifying individuals and estates to offset up. Here's the basic rule about rental losses you need to know: As a result of a casualty or theft, you may have a loss related to your rental property. The rental real estate loss allowance is what the irs allows you to deduct in passive losses from real estate each year from your earned income. It can be used to. If you have any personal use of a dwelling unit that you rent (including a vacation home or a residence in which you rent a room),. The rental real estate loss allowance is a federal tax deduction of up to $25,000 a year for taxpayers who take a loss on rental property.

From www.bank2home.com

Rental Property Profit And Loss Statement Template Excel Templates Rental Property Loss Rules Rental property losses are deductible when they’re applied to passive income, and you can carry them forward from. Here's the basic rule about rental losses you need to know: It can be used to. As a result of a casualty or theft, you may have a loss related to your rental property. If you have any personal use of a. Rental Property Loss Rules.

From templatelab.com

53 Profit and Loss Statement Templates & Forms [Excel, PDF] Rental Property Loss Rules Here's the basic rule about rental losses you need to know: Rental property losses are deductible when they’re applied to passive income, and you can carry them forward from. Rental losses are always classified as passive losses for tax purposes. As a result of a casualty or theft, you may have a loss related to your rental property. The rental. Rental Property Loss Rules.

From socalhomebuyers.com

Selling Your Rental Property at a Loss Rental Property Loss Rules If you have any personal use of a dwelling unit that you rent (including a vacation home or a residence in which you rent a room),. It can be used to. Rental property losses are deductible when they’re applied to passive income, and you can carry them forward from. The rental real estate loss allowance is a federal tax deduction. Rental Property Loss Rules.

From www.template.net

Rental Property Profit And Loss Template Google Sheets, Excel Rental Property Loss Rules The rental real estate loss allowance is a federal tax deduction of up to $25,000 a year for taxpayers who take a loss on rental property. If you have any personal use of a dwelling unit that you rent (including a vacation home or a residence in which you rent a room),. Rental losses are always classified as passive losses. Rental Property Loss Rules.

From lesboucans.com

Rental Property Profit And Loss Statement Template For Your Needs Rental Property Loss Rules The rental real estate loss allowance is what the irs allows you to deduct in passive losses from real estate each year from your earned income. The rental real estate loss allowance is a federal tax deduction of up to $25,000 a year for taxpayers who take a loss on rental property. Here's the basic rule about rental losses you. Rental Property Loss Rules.

From www.askspaulding.com

Why A Rental Property Loss May Not Lower Your Taxes Ask Spaulding Rental Property Loss Rules Here's the basic rule about rental losses you need to know: As a result of a casualty or theft, you may have a loss related to your rental property. Rental property losses are deductible when they’re applied to passive income, and you can carry them forward from. The rental real estate loss allowance is what the irs allows you to. Rental Property Loss Rules.

From www.wallstreetmojo.com

Casualty Loss What Is It, Explained, Examples, How To Claim? Rental Property Loss Rules It can be used to. The rental real estate loss allowance is what the irs allows you to deduct in passive losses from real estate each year from your earned income. Rental property losses are deductible when they’re applied to passive income, and you can carry them forward from. The rental real estate loss allowance is a federal tax deduction. Rental Property Loss Rules.

From www.slideserve.com

PPT CHAPTER 3 PowerPoint Presentation, free download ID771551 Rental Property Loss Rules As a result of a casualty or theft, you may have a loss related to your rental property. The rental real estate loss allowance is what the irs allows you to deduct in passive losses from real estate each year from your earned income. Here's the basic rule about rental losses you need to know: It can be used to.. Rental Property Loss Rules.

From www.pinterest.com

Printable Rental Property Profit And Loss Statement Template Excel Rental Property Loss Rules As a result of a casualty or theft, you may have a loss related to your rental property. Here's the basic rule about rental losses you need to know: The rental real estate loss allowance is a federal tax deduction of up to $25,000 a year for taxpayers who take a loss on rental property. If you have any personal. Rental Property Loss Rules.

From www.linkedin.com

How to carry forward rental property losses effectively MC Properties Rental Property Loss Rules The rental real estate loss allowance is what the irs allows you to deduct in passive losses from real estate each year from your earned income. It can be used to. As a result of a casualty or theft, you may have a loss related to your rental property. If you have any personal use of a dwelling unit that. Rental Property Loss Rules.

From thebottomline.com.au

Are you at a net rental loss? The Bottom Line Business Advisory Rental Property Loss Rules The rental real estate loss allowance is a federal tax deduction of up to $25,000 a year for taxpayers who take a loss on rental property. As a result of a casualty or theft, you may have a loss related to your rental property. Even though rental income or loss generally is passive, a special rule allows qualifying individuals and. Rental Property Loss Rules.

From accidentalrental.com

15 Ways You Can Grow Rental Profits Today Accidental Rental Rental Property Loss Rules Here's the basic rule about rental losses you need to know: If you have any personal use of a dwelling unit that you rent (including a vacation home or a residence in which you rent a room),. Even though rental income or loss generally is passive, a special rule allows qualifying individuals and estates to offset up. The rental real. Rental Property Loss Rules.

From www.linkedin.com

Three Methods to Generate From Your Rental Property Tax Losses Rental Property Loss Rules Here's the basic rule about rental losses you need to know: Even though rental income or loss generally is passive, a special rule allows qualifying individuals and estates to offset up. Rental losses are always classified as passive losses for tax purposes. If you have any personal use of a dwelling unit that you rent (including a vacation home or. Rental Property Loss Rules.

From illuminationwealth.com

Illumination Wealth ManagementUnderstanding Passive Loss Rules for Rental Property Loss Rules The rental real estate loss allowance is what the irs allows you to deduct in passive losses from real estate each year from your earned income. Even though rental income or loss generally is passive, a special rule allows qualifying individuals and estates to offset up. The rental real estate loss allowance is a federal tax deduction of up to. Rental Property Loss Rules.

From www.pinterest.com

The Ultimate 5 Property Rental Real Estate Template excel Etsy Rental Property Loss Rules Rental property losses are deductible when they’re applied to passive income, and you can carry them forward from. If you have any personal use of a dwelling unit that you rent (including a vacation home or a residence in which you rent a room),. It can be used to. As a result of a casualty or theft, you may have. Rental Property Loss Rules.

From www.etsy.com

Rental Property Profit and Loss Statement Template Excel Profit and Rental Property Loss Rules Here's the basic rule about rental losses you need to know: As a result of a casualty or theft, you may have a loss related to your rental property. The rental real estate loss allowance is a federal tax deduction of up to $25,000 a year for taxpayers who take a loss on rental property. It can be used to.. Rental Property Loss Rules.

From www.nuventurecpa.com

Rental Property Profit & Loss Statement for Clients — Nuventure CPA LLC Rental Property Loss Rules It can be used to. The rental real estate loss allowance is a federal tax deduction of up to $25,000 a year for taxpayers who take a loss on rental property. If you have any personal use of a dwelling unit that you rent (including a vacation home or a residence in which you rent a room),. As a result. Rental Property Loss Rules.

From irstaxtrouble.com

Rental Losses for Real Estate Agents Passive Activity Loss Rules Rental Property Loss Rules Rental property losses are deductible when they’re applied to passive income, and you can carry them forward from. The rental real estate loss allowance is what the irs allows you to deduct in passive losses from real estate each year from your earned income. As a result of a casualty or theft, you may have a loss related to your. Rental Property Loss Rules.

From housing.com

Loss from House Property All you Need to Know Rental Property Loss Rules Rental losses are always classified as passive losses for tax purposes. It can be used to. The rental real estate loss allowance is a federal tax deduction of up to $25,000 a year for taxpayers who take a loss on rental property. Rental property losses are deductible when they’re applied to passive income, and you can carry them forward from.. Rental Property Loss Rules.

From www.chegg.com

Solved Discussion Question 1119 (LO. 6) Complete the Rental Property Loss Rules Rental property losses are deductible when they’re applied to passive income, and you can carry them forward from. The rental real estate loss allowance is what the irs allows you to deduct in passive losses from real estate each year from your earned income. Rental losses are always classified as passive losses for tax purposes. If you have any personal. Rental Property Loss Rules.

From www.landlordstudio.com

About Your Rental Property Profit and Loss Statement Rental Property Loss Rules Even though rental income or loss generally is passive, a special rule allows qualifying individuals and estates to offset up. The rental real estate loss allowance is a federal tax deduction of up to $25,000 a year for taxpayers who take a loss on rental property. Rental property losses are deductible when they’re applied to passive income, and you can. Rental Property Loss Rules.

From htj.tax

Rental Activity Loss Rules for Real Estate HTJ Tax Rental Property Loss Rules Here's the basic rule about rental losses you need to know: The rental real estate loss allowance is what the irs allows you to deduct in passive losses from real estate each year from your earned income. As a result of a casualty or theft, you may have a loss related to your rental property. The rental real estate loss. Rental Property Loss Rules.

From old.sermitsiaq.ag

Rental Property Profit Loss Template Rental Property Loss Rules Here's the basic rule about rental losses you need to know: Even though rental income or loss generally is passive, a special rule allows qualifying individuals and estates to offset up. As a result of a casualty or theft, you may have a loss related to your rental property. The rental real estate loss allowance is what the irs allows. Rental Property Loss Rules.

From www.template.net

Rental Profit And Loss Template in Excel, Google Sheets Download Rental Property Loss Rules The rental real estate loss allowance is what the irs allows you to deduct in passive losses from real estate each year from your earned income. Rental property losses are deductible when they’re applied to passive income, and you can carry them forward from. It can be used to. The rental real estate loss allowance is a federal tax deduction. Rental Property Loss Rules.

From www.template.net

Rental Property Profit And Loss Template Download in Excel, Google Rental Property Loss Rules Rental property losses are deductible when they’re applied to passive income, and you can carry them forward from. The rental real estate loss allowance is what the irs allows you to deduct in passive losses from real estate each year from your earned income. Even though rental income or loss generally is passive, a special rule allows qualifying individuals and. Rental Property Loss Rules.

From ttlc.intuit.com

Solved Material Participation to Recognize Rental Property Losses Rental Property Loss Rules It can be used to. If you have any personal use of a dwelling unit that you rent (including a vacation home or a residence in which you rent a room),. The rental real estate loss allowance is a federal tax deduction of up to $25,000 a year for taxpayers who take a loss on rental property. As a result. Rental Property Loss Rules.

From www.uslegalforms.com

PRO Financial Rental Property Profit and Loss Statement Fill and Sign Rental Property Loss Rules Rental losses are always classified as passive losses for tax purposes. If you have any personal use of a dwelling unit that you rent (including a vacation home or a residence in which you rent a room),. Here's the basic rule about rental losses you need to know: Even though rental income or loss generally is passive, a special rule. Rental Property Loss Rules.

From www.templatenum.com

Profit And Loss Template For Rental Property Rental Property Loss Rules The rental real estate loss allowance is a federal tax deduction of up to $25,000 a year for taxpayers who take a loss on rental property. It can be used to. If you have any personal use of a dwelling unit that you rent (including a vacation home or a residence in which you rent a room),. Even though rental. Rental Property Loss Rules.

From www.adjustersinternational.com

Property Loss Professionals Who Are They and How Can They Help You Rental Property Loss Rules It can be used to. Rental property losses are deductible when they’re applied to passive income, and you can carry them forward from. Here's the basic rule about rental losses you need to know: Rental losses are always classified as passive losses for tax purposes. If you have any personal use of a dwelling unit that you rent (including a. Rental Property Loss Rules.

From legaltemplates.net

Free Release of Liability Form Sample Waiver Form Legal Templates Rental Property Loss Rules Here's the basic rule about rental losses you need to know: As a result of a casualty or theft, you may have a loss related to your rental property. The rental real estate loss allowance is a federal tax deduction of up to $25,000 a year for taxpayers who take a loss on rental property. Rental losses are always classified. Rental Property Loss Rules.

From lesboucans.com

Rental Property Profit And Loss Statement Template For Your Needs Rental Property Loss Rules As a result of a casualty or theft, you may have a loss related to your rental property. The rental real estate loss allowance is a federal tax deduction of up to $25,000 a year for taxpayers who take a loss on rental property. If you have any personal use of a dwelling unit that you rent (including a vacation. Rental Property Loss Rules.

From www.slideserve.com

PPT Passive Loss Rules PowerPoint Presentation, free download ID Rental Property Loss Rules The rental real estate loss allowance is a federal tax deduction of up to $25,000 a year for taxpayers who take a loss on rental property. It can be used to. The rental real estate loss allowance is what the irs allows you to deduct in passive losses from real estate each year from your earned income. Rental losses are. Rental Property Loss Rules.

From www.ssacpa.com

Converting a home to a rental Know the tax implications Rental Property Loss Rules Rental losses are always classified as passive losses for tax purposes. As a result of a casualty or theft, you may have a loss related to your rental property. Even though rental income or loss generally is passive, a special rule allows qualifying individuals and estates to offset up. If you have any personal use of a dwelling unit that. Rental Property Loss Rules.

From www.liddellcrook.nz

Rental Losses Liddell and Crook Rental Property Loss Rules Even though rental income or loss generally is passive, a special rule allows qualifying individuals and estates to offset up. Rental property losses are deductible when they’re applied to passive income, and you can carry them forward from. Here's the basic rule about rental losses you need to know: If you have any personal use of a dwelling unit that. Rental Property Loss Rules.

From www.propertyinsurancecoveragelaw.com

Property Loss Prevention and Laws Are Not New Ideas But Necessary Rental Property Loss Rules Rental losses are always classified as passive losses for tax purposes. It can be used to. Here's the basic rule about rental losses you need to know: If you have any personal use of a dwelling unit that you rent (including a vacation home or a residence in which you rent a room),. Even though rental income or loss generally. Rental Property Loss Rules.