Stock Beta Linear Regression . Beta is calculated using regression analysis. Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. Beta of a publicly traded company can be calculated using the market model regression (slope). Beta, as we noted above, is the beta coefficient of an asset that. These are a few ways you can find the alpha and beta of a stock or portfolio given their return series. Numerically, it represents the tendency for a stock’s returns to respond to the volatility of the market. We are going to focus on one particular aspect of capm: Beta formula interpretation of a beta result. Nasdaq index ) one indicates a stock. In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Slope() and intercept() are the simplest way. A stock with a beta of: In this method, we regress the company’s stock returns (ri) against the market’s returns. Zero indicates no correlation with the chosen benchmark (e.g.

from www.simtrade.fr

Zero indicates no correlation with the chosen benchmark (e.g. Beta formula interpretation of a beta result. Beta is calculated using regression analysis. Numerically, it represents the tendency for a stock’s returns to respond to the volatility of the market. Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. A stock with a beta of: We are going to focus on one particular aspect of capm: Slope() and intercept() are the simplest way. These are a few ways you can find the alpha and beta of a stock or portfolio given their return series. Beta of a publicly traded company can be calculated using the market model regression (slope).

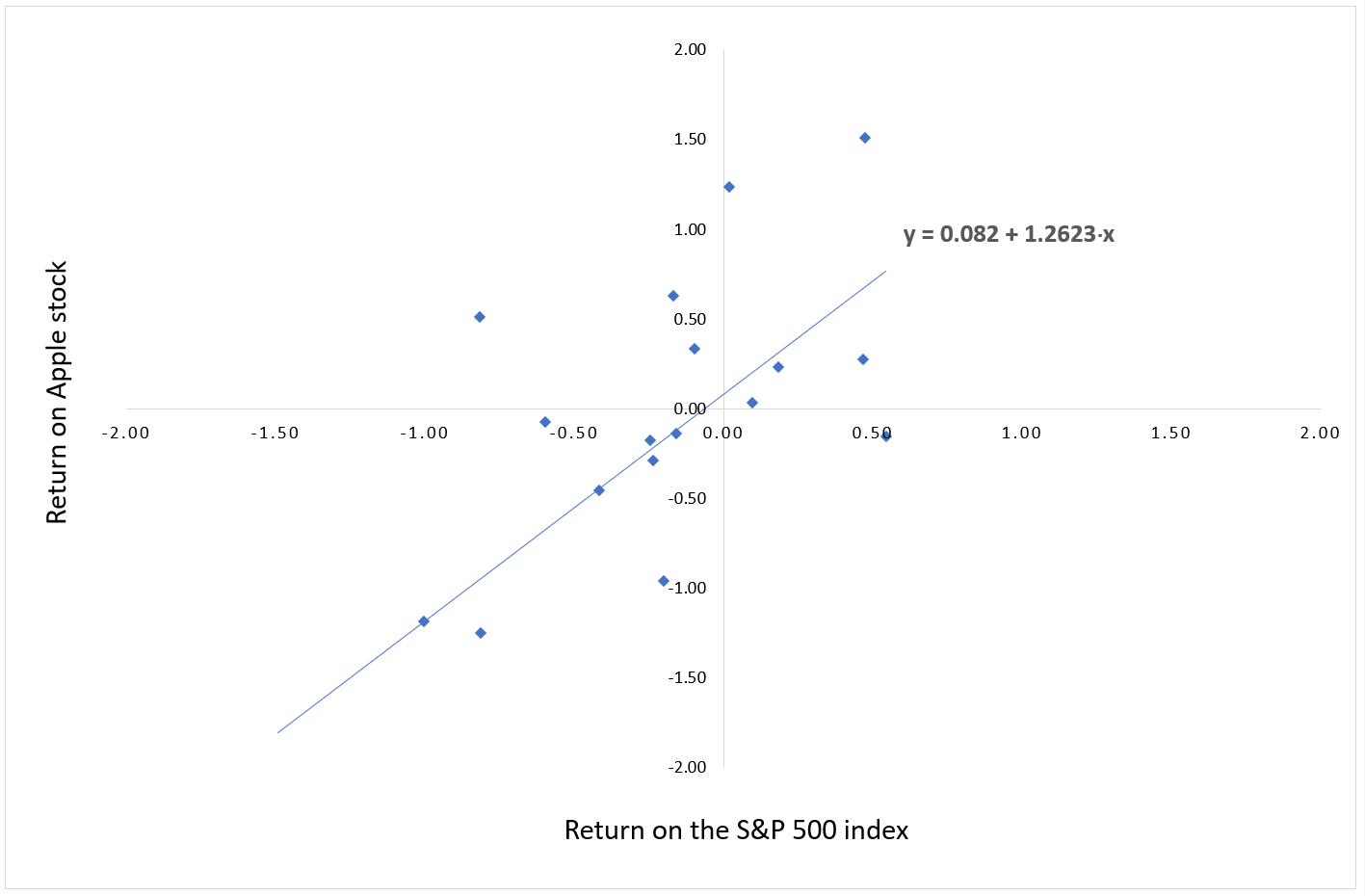

Linear Regression SimTrade blogSimTrade blog

Stock Beta Linear Regression Beta of a publicly traded company can be calculated using the market model regression (slope). In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). We are going to focus on one particular aspect of capm: In this method, we regress the company’s stock returns (ri) against the market’s returns. Beta, as we noted above, is the beta coefficient of an asset that. Beta formula interpretation of a beta result. Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. A stock with a beta of: Beta is calculated using regression analysis. Numerically, it represents the tendency for a stock’s returns to respond to the volatility of the market. These are a few ways you can find the alpha and beta of a stock or portfolio given their return series. Nasdaq index ) one indicates a stock. Slope() and intercept() are the simplest way. Beta of a publicly traded company can be calculated using the market model regression (slope). Zero indicates no correlation with the chosen benchmark (e.g.

From worksheetclouring.z14.web.core.windows.net

How To Work Out Linear Regression Stock Beta Linear Regression Numerically, it represents the tendency for a stock’s returns to respond to the volatility of the market. Beta of a publicly traded company can be calculated using the market model regression (slope). Zero indicates no correlation with the chosen benchmark (e.g. Nasdaq index ) one indicates a stock. In this method, we regress the company’s stock returns (ri) against the. Stock Beta Linear Regression.

From www.youtube.com

Estimating Beta using regression YouTube Stock Beta Linear Regression A stock with a beta of: Beta is calculated using regression analysis. Slope() and intercept() are the simplest way. Beta, as we noted above, is the beta coefficient of an asset that. Zero indicates no correlation with the chosen benchmark (e.g. Beta formula interpretation of a beta result. Beta of a publicly traded company can be calculated using the market. Stock Beta Linear Regression.

From montilab.github.io

Linear Regression • BS831 Stock Beta Linear Regression Beta formula interpretation of a beta result. Beta, as we noted above, is the beta coefficient of an asset that. In this method, we regress the company’s stock returns (ri) against the market’s returns. A stock with a beta of: Nasdaq index ) one indicates a stock. Slope() and intercept() are the simplest way. Beta of a publicly traded company. Stock Beta Linear Regression.

From endel.afphila.com

Beta What is Beta (β) in Finance? Guide and Examples Stock Beta Linear Regression In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). These are a few ways you can find the alpha and beta of a stock or portfolio given their return series. Beta of a publicly traded company can be calculated using the market model regression (slope). Numerically, it. Stock Beta Linear Regression.

From www.statology.org

Introduction to Multiple Linear Regression Stock Beta Linear Regression Beta, as we noted above, is the beta coefficient of an asset that. In this method, we regress the company’s stock returns (ri) against the market’s returns. Beta of a publicly traded company can be calculated using the market model regression (slope). Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and. Stock Beta Linear Regression.

From www.chegg.com

Solved In the simple linear regression model Y_i = beta_0 + Stock Beta Linear Regression In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Numerically, it represents the tendency for a stock’s returns to respond to the volatility of the market. Beta, as we noted above, is the beta coefficient of an asset that. Zero indicates no correlation with the chosen benchmark. Stock Beta Linear Regression.

From stats.stackexchange.com

Can standardized \beta coefficients in linear regression be used to Stock Beta Linear Regression In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). We are going to focus on one particular aspect of capm: These are a few ways you can find the alpha and beta of a stock or portfolio given their return series. Beta is calculated using regression analysis.. Stock Beta Linear Regression.

From www.mdpi.com

JRFM Free FullText Refining Our Understanding of Beta through Stock Beta Linear Regression These are a few ways you can find the alpha and beta of a stock or portfolio given their return series. Slope() and intercept() are the simplest way. A stock with a beta of: Beta formula interpretation of a beta result. Zero indicates no correlation with the chosen benchmark (e.g. Beta, as we noted above, is the beta coefficient of. Stock Beta Linear Regression.

From www.lundgrensimon.com

How to Calculate Beta In Excel All 3 Methods (Regression, Slope Stock Beta Linear Regression Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. In this method, we regress the company’s stock returns (ri) against the market’s returns. Beta formula interpretation of a beta result. Slope() and intercept() are the simplest way. Beta is calculated using regression analysis. Numerically, it represents the tendency. Stock Beta Linear Regression.

From rcompanion.org

R Handbook Beta Regression for Percent and Proportion Data Stock Beta Linear Regression Beta is calculated using regression analysis. These are a few ways you can find the alpha and beta of a stock or portfolio given their return series. Zero indicates no correlation with the chosen benchmark (e.g. Slope() and intercept() are the simplest way. Beta, as we noted above, is the beta coefficient of an asset that. In this method, we. Stock Beta Linear Regression.

From stats4stem.weebly.com

Confidence Interval for Beta Linear Regression STATS4STEM2 Stock Beta Linear Regression Slope() and intercept() are the simplest way. A stock with a beta of: Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Zero indicates no correlation. Stock Beta Linear Regression.

From www.chegg.com

Solved stock is the beta. Betas for individual stocks are Stock Beta Linear Regression Beta formula interpretation of a beta result. A stock with a beta of: Zero indicates no correlation with the chosen benchmark (e.g. In this method, we regress the company’s stock returns (ri) against the market’s returns. Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. Beta, as we. Stock Beta Linear Regression.

From www.youtube.com

What is Beta? YouTube Stock Beta Linear Regression Slope() and intercept() are the simplest way. Zero indicates no correlation with the chosen benchmark (e.g. In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. In. Stock Beta Linear Regression.

From slideplayer.com

Session 5 Relative Risk ppt download Stock Beta Linear Regression Numerically, it represents the tendency for a stock’s returns to respond to the volatility of the market. Slope() and intercept() are the simplest way. Beta is calculated using regression analysis. Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. We are going to focus on one particular aspect. Stock Beta Linear Regression.

From www.youtube.com

How To Calculate Beta on Excel Linear Regression & Slope Tool YouTube Stock Beta Linear Regression Beta is calculated using regression analysis. Nasdaq index ) one indicates a stock. Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. We are going to focus on one particular aspect of capm: Slope() and intercept() are the simplest way. These are a few ways you can find. Stock Beta Linear Regression.

From www.markhw.com

Using Beta Regression to Better Model Norms in Political Psychology Stock Beta Linear Regression Nasdaq index ) one indicates a stock. Zero indicates no correlation with the chosen benchmark (e.g. Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. Beta of a publicly traded company can be calculated using the market model regression (slope). We are going to focus on one particular. Stock Beta Linear Regression.

From stats4stem.weebly.com

Confidence Interval for Beta Linear Regression STATS4STEM2 Stock Beta Linear Regression Beta formula interpretation of a beta result. These are a few ways you can find the alpha and beta of a stock or portfolio given their return series. Nasdaq index ) one indicates a stock. A stock with a beta of: In this method, we regress the company’s stock returns (ri) against the market’s returns. Calculate the slope (beta) of. Stock Beta Linear Regression.

From www.youtube.com

Estimating Beta with Regression Analysis YouTube Stock Beta Linear Regression These are a few ways you can find the alpha and beta of a stock or portfolio given their return series. Beta of a publicly traded company can be calculated using the market model regression (slope). Numerically, it represents the tendency for a stock’s returns to respond to the volatility of the market. Slope() and intercept() are the simplest way.. Stock Beta Linear Regression.

From www.hcbravo.org

28 Linear Regression Lecture Notes Introduction to Data Science Stock Beta Linear Regression These are a few ways you can find the alpha and beta of a stock or portfolio given their return series. Beta is calculated using regression analysis. In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Beta of a publicly traded company can be calculated using the. Stock Beta Linear Regression.

From www.pushandprofit.com

Using Linear Regression Channels For Trading Stock Beta Linear Regression Numerically, it represents the tendency for a stock’s returns to respond to the volatility of the market. A stock with a beta of: In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Beta of a publicly traded company can be calculated using the market model regression (slope).. Stock Beta Linear Regression.

From growthinshots.com

Calculate Regression Beta with Python A Comprehensive Guide Stock Beta Linear Regression Nasdaq index ) one indicates a stock. In this method, we regress the company’s stock returns (ri) against the market’s returns. Beta of a publicly traded company can be calculated using the market model regression (slope). Slope() and intercept() are the simplest way. These are a few ways you can find the alpha and beta of a stock or portfolio. Stock Beta Linear Regression.

From loefocoji.blob.core.windows.net

Stock Beta By Industry at Ryan blog Stock Beta Linear Regression Nasdaq index ) one indicates a stock. In this method, we regress the company’s stock returns (ri) against the market’s returns. Beta formula interpretation of a beta result. Beta, as we noted above, is the beta coefficient of an asset that. Numerically, it represents the tendency for a stock’s returns to respond to the volatility of the market. These are. Stock Beta Linear Regression.

From www.researchgate.net

Betas from linear regressions modeled for each classifier parameter Stock Beta Linear Regression Zero indicates no correlation with the chosen benchmark (e.g. Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. Slope() and intercept() are the simplest way. Numerically, it represents the tendency for a stock’s returns to respond to the volatility of the market. Beta, as we noted above, is. Stock Beta Linear Regression.

From www.youtube.com

How to Calculate Beta In Excel All 3 Methods (Regression, Slope Stock Beta Linear Regression Slope() and intercept() are the simplest way. In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. These are a few ways you can find the alpha. Stock Beta Linear Regression.

From www.researchgate.net

Linear regression standardized Beta coefficients and corresponding Stock Beta Linear Regression We are going to focus on one particular aspect of capm: Zero indicates no correlation with the chosen benchmark (e.g. These are a few ways you can find the alpha and beta of a stock or portfolio given their return series. Beta formula interpretation of a beta result. Beta is calculated using regression analysis. Nasdaq index ) one indicates a. Stock Beta Linear Regression.

From www.calculatinginvestor.com

t_capm Stock Beta Linear Regression These are a few ways you can find the alpha and beta of a stock or portfolio given their return series. Slope() and intercept() are the simplest way. In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Zero indicates no correlation with the chosen benchmark (e.g. Calculate. Stock Beta Linear Regression.

From www.andrewheiss.com

A guide to modeling proportions with Bayesian beta and zeroinflated Stock Beta Linear Regression These are a few ways you can find the alpha and beta of a stock or portfolio given their return series. A stock with a beta of: Slope() and intercept() are the simplest way. We are going to focus on one particular aspect of capm: In this method, we regress the company’s stock returns (ri) against the market’s returns. Beta,. Stock Beta Linear Regression.

From www.researchgate.net

(a) The results of a twoway beta regression model revealed differences Stock Beta Linear Regression Beta, as we noted above, is the beta coefficient of an asset that. Calculate the slope (beta) of the linear regression line through data points (price returns) for the stock and the benchmark index. A stock with a beta of: Numerically, it represents the tendency for a stock’s returns to respond to the volatility of the market. Beta formula interpretation. Stock Beta Linear Regression.

From www.simtrade.fr

Linear Regression SimTrade blogSimTrade blog Stock Beta Linear Regression Zero indicates no correlation with the chosen benchmark (e.g. Beta of a publicly traded company can be calculated using the market model regression (slope). Beta formula interpretation of a beta result. A stock with a beta of: In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Calculate. Stock Beta Linear Regression.

From www.slideserve.com

PPT Chapter 11 Simple Linear Regression Analysis ( 线性回归分析 Stock Beta Linear Regression A stock with a beta of: These are a few ways you can find the alpha and beta of a stock or portfolio given their return series. Nasdaq index ) one indicates a stock. Slope() and intercept() are the simplest way. Beta, as we noted above, is the beta coefficient of an asset that. Beta formula interpretation of a beta. Stock Beta Linear Regression.

From www.researchgate.net

Linear Regression model sample illustration Download Scientific Diagram Stock Beta Linear Regression Zero indicates no correlation with the chosen benchmark (e.g. Nasdaq index ) one indicates a stock. In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Beta of a publicly traded company can be calculated using the market model regression (slope). Slope() and intercept() are the simplest way.. Stock Beta Linear Regression.

From stats.stackexchange.com

In Beta Regression we obtain predictions of the mean response, do we Stock Beta Linear Regression A stock with a beta of: These are a few ways you can find the alpha and beta of a stock or portfolio given their return series. Beta formula interpretation of a beta result. Beta is calculated using regression analysis. Zero indicates no correlation with the chosen benchmark (e.g. Numerically, it represents the tendency for a stock’s returns to respond. Stock Beta Linear Regression.

From www.introranger.org

How ANOVA is linear regression IntroRangeR Stock Beta Linear Regression These are a few ways you can find the alpha and beta of a stock or portfolio given their return series. Beta is calculated using regression analysis. Nasdaq index ) one indicates a stock. Beta, as we noted above, is the beta coefficient of an asset that. Beta formula interpretation of a beta result. Numerically, it represents the tendency for. Stock Beta Linear Regression.

From www.lundgrensimon.com

How to Calculate Beta In Excel All 3 Methods (Regression, Slope Stock Beta Linear Regression In this comprehensive guide, we will explore the process of estimating beta using linear regression in the capital asset pricing model (capm). Numerically, it represents the tendency for a stock’s returns to respond to the volatility of the market. In this method, we regress the company’s stock returns (ri) against the market’s returns. Beta formula interpretation of a beta result.. Stock Beta Linear Regression.

From www.youtube.com

An Introduction to Linear Regression Analysis YouTube Stock Beta Linear Regression A stock with a beta of: Beta formula interpretation of a beta result. Beta of a publicly traded company can be calculated using the market model regression (slope). Nasdaq index ) one indicates a stock. We are going to focus on one particular aspect of capm: Calculate the slope (beta) of the linear regression line through data points (price returns). Stock Beta Linear Regression.