Fixed Income Portfolio Duration . Using the weighted average of time to receipt of the aggregate. How a bond or bond portfolio’s value is. there are two methods to calculate the duration and convexity of a bond portfolio: plot the duration of your fixed income holdings using fidelity's guided portfolio summary sm (gps) to see at a glance the weighted average duration of your fixed. Most bond investors know that interest rate changes can affect the value of their fixed income holdings. duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. Pure, or macaulay duration, is. Convexity supplements duration as a measure of a. duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. It’s a simple summary statistic of the effective average maturity. These many factors are calculated into one number.

from blog.rurashfin.com

Convexity supplements duration as a measure of a. Using the weighted average of time to receipt of the aggregate. Pure, or macaulay duration, is. there are two methods to calculate the duration and convexity of a bond portfolio: duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. How a bond or bond portfolio’s value is. Most bond investors know that interest rate changes can affect the value of their fixed income holdings. plot the duration of your fixed income holdings using fidelity's guided portfolio summary sm (gps) to see at a glance the weighted average duration of your fixed. duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. It’s a simple summary statistic of the effective average maturity.

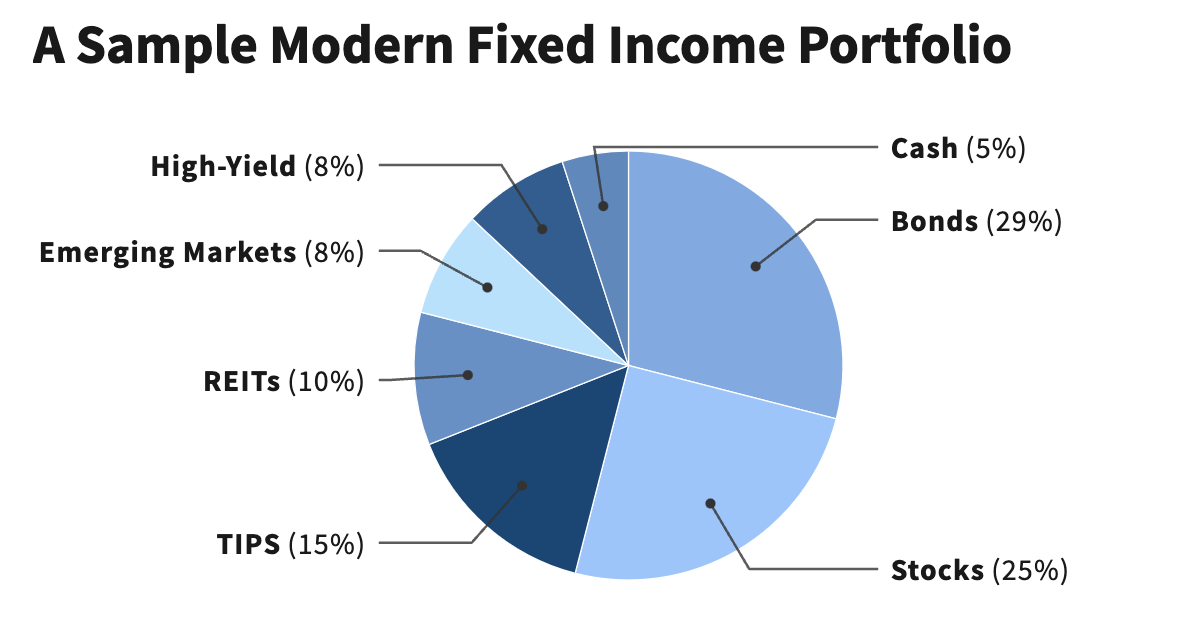

How to Create a Modern Portfolio? The Asset Allocation way

Fixed Income Portfolio Duration Most bond investors know that interest rate changes can affect the value of their fixed income holdings. duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. Using the weighted average of time to receipt of the aggregate. Most bond investors know that interest rate changes can affect the value of their fixed income holdings. duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. These many factors are calculated into one number. How a bond or bond portfolio’s value is. Pure, or macaulay duration, is. plot the duration of your fixed income holdings using fidelity's guided portfolio summary sm (gps) to see at a glance the weighted average duration of your fixed. It’s a simple summary statistic of the effective average maturity. Convexity supplements duration as a measure of a. there are two methods to calculate the duration and convexity of a bond portfolio:

From www.advisorperspectives.com

Key Takeaways From Our 2021 Advisor Fixed Portfolio Review Fixed Income Portfolio Duration How a bond or bond portfolio’s value is. plot the duration of your fixed income holdings using fidelity's guided portfolio summary sm (gps) to see at a glance the weighted average duration of your fixed. It’s a simple summary statistic of the effective average maturity. duration is a measurement of a bond’s interest rate risk that considers a. Fixed Income Portfolio Duration.

From www.etftrends.com

Short Duration Fixed Model Portfolio Keep the Lose the Fixed Income Portfolio Duration plot the duration of your fixed income holdings using fidelity's guided portfolio summary sm (gps) to see at a glance the weighted average duration of your fixed. there are two methods to calculate the duration and convexity of a bond portfolio: These many factors are calculated into one number. duration is a way of measuring the interest. Fixed Income Portfolio Duration.

From www.etftrends.com

Short Duration Fixed Model Portfolio Keep the Lose the Fixed Income Portfolio Duration It’s a simple summary statistic of the effective average maturity. there are two methods to calculate the duration and convexity of a bond portfolio: Convexity supplements duration as a measure of a. Using the weighted average of time to receipt of the aggregate. Most bond investors know that interest rate changes can affect the value of their fixed income. Fixed Income Portfolio Duration.

From perspectives.agf.com

5 facts about fixed AGF Perspectives Fixed Income Portfolio Duration How a bond or bond portfolio’s value is. These many factors are calculated into one number. there are two methods to calculate the duration and convexity of a bond portfolio: Using the weighted average of time to receipt of the aggregate. It’s a simple summary statistic of the effective average maturity. duration is a measurement of a bond’s. Fixed Income Portfolio Duration.

From financinglife.org

Fixed Examples Ballast to stabilize the portfolio Fixed Income Portfolio Duration duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. These many factors are calculated into one number. Pure, or macaulay duration, is. there are two methods to calculate the duration and convexity of a bond portfolio: How a bond or bond portfolio’s value is. Most bond investors know. Fixed Income Portfolio Duration.

From imgbin.com

Fixed Market Risk Portfolio Yield Curve PNG, Clipart, Area, Bond Fixed Income Portfolio Duration duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. How a bond or bond portfolio’s value is. Using the weighted average of time to receipt of the aggregate. Pure, or macaulay duration, is. there are two methods to calculate the duration and convexity of a bond portfolio: . Fixed Income Portfolio Duration.

From quantessential.blogspot.com

Duration Targeting for Fixed Portfolios Fixed Income Portfolio Duration How a bond or bond portfolio’s value is. duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. Pure, or macaulay duration, is. plot the duration of your. Fixed Income Portfolio Duration.

From www.slideserve.com

PPT Chapter 5 PowerPoint Presentation, free download ID4258851 Fixed Income Portfolio Duration Pure, or macaulay duration, is. How a bond or bond portfolio’s value is. plot the duration of your fixed income holdings using fidelity's guided portfolio summary sm (gps) to see at a glance the weighted average duration of your fixed. there are two methods to calculate the duration and convexity of a bond portfolio: Most bond investors know. Fixed Income Portfolio Duration.

From www.2020financialplanningllc.com

Examples of Fixed Portfolios Fixed Income Portfolio Duration Most bond investors know that interest rate changes can affect the value of their fixed income holdings. Pure, or macaulay duration, is. duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. It’s a simple summary statistic of the effective average maturity. duration is a measurement of a bond’s. Fixed Income Portfolio Duration.

From www.scribd.com

5.PAK QFIPME TOPIC1 MIP 6 Fixed Portfolio Management PDF Fixed Income Portfolio Duration It’s a simple summary statistic of the effective average maturity. How a bond or bond portfolio’s value is. These many factors are calculated into one number. plot the duration of your fixed income holdings using fidelity's guided portfolio summary sm (gps) to see at a glance the weighted average duration of your fixed. duration is a way of. Fixed Income Portfolio Duration.

From quantessential.blogspot.com

Duration Targeting for Fixed Portfolios Fixed Income Portfolio Duration Pure, or macaulay duration, is. duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. How a bond or bond portfolio’s value is. It’s a simple summary statistic of the effective average maturity. Most bond investors know that interest rate changes can affect the value of their fixed income holdings.. Fixed Income Portfolio Duration.

From www.scribd.com

Overview of Portfolio Management PDF Bond Duration Fixed Income Portfolio Duration Convexity supplements duration as a measure of a. It’s a simple summary statistic of the effective average maturity. Most bond investors know that interest rate changes can affect the value of their fixed income holdings. plot the duration of your fixed income holdings using fidelity's guided portfolio summary sm (gps) to see at a glance the weighted average duration. Fixed Income Portfolio Duration.

From www.youtube.com

Fixed 11 Portfolio Risk Management with Duration Matching YouTube Fixed Income Portfolio Duration It’s a simple summary statistic of the effective average maturity. duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. Most bond investors know that interest rate changes can affect the value of their fixed income holdings. Convexity supplements duration as a measure of a. plot the duration. Fixed Income Portfolio Duration.

From www.investopedia.com

Duration Definition and Its Use in Fixed Investing Fixed Income Portfolio Duration How a bond or bond portfolio’s value is. Pure, or macaulay duration, is. there are two methods to calculate the duration and convexity of a bond portfolio: Most bond investors know that interest rate changes can affect the value of their fixed income holdings. plot the duration of your fixed income holdings using fidelity's guided portfolio summary sm. Fixed Income Portfolio Duration.

From www.scribd.com

14 Fixed Portfolio Management PDF Bond Duration Bonds Fixed Income Portfolio Duration How a bond or bond portfolio’s value is. plot the duration of your fixed income holdings using fidelity's guided portfolio summary sm (gps) to see at a glance the weighted average duration of your fixed. duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. Convexity supplements duration. Fixed Income Portfolio Duration.

From seekingalpha.com

How To Create A (Nearly) NoRisk Portfolio That Won't Go Fixed Income Portfolio Duration Convexity supplements duration as a measure of a. These many factors are calculated into one number. Pure, or macaulay duration, is. there are two methods to calculate the duration and convexity of a bond portfolio: It’s a simple summary statistic of the effective average maturity. Most bond investors know that interest rate changes can affect the value of their. Fixed Income Portfolio Duration.

From www.slideserve.com

PPT Chapter 16 Revision of the Portfolio PowerPoint Fixed Income Portfolio Duration duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. Convexity supplements duration as a measure of a. It’s a simple summary statistic of the effective average maturity. Using the weighted average of time to receipt of the aggregate. plot the duration of your fixed income holdings using fidelity's. Fixed Income Portfolio Duration.

From www.livewiremarkets.com

Investing An Approach to Integrating Your Australian Fixed Income Portfolio Duration duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. Most bond investors know that interest rate changes can affect the value of their fixed income holdings. Convexity supplements. Fixed Income Portfolio Duration.

From www.etftrends.com

Short Duration Fixed Model Portfolio Keep the Lose the Fixed Income Portfolio Duration Using the weighted average of time to receipt of the aggregate. duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. How a bond or bond portfolio’s value is. It’s a simple summary statistic of the effective average maturity. there are two methods to calculate the duration and convexity. Fixed Income Portfolio Duration.

From cma.wolflinecapital.com

Securing Portfolio with Bond Ladder Strategy Wolfline Fixed Income Portfolio Duration duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. Pure, or macaulay duration, is. duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. It’s a simple summary statistic of the effective average maturity. How a bond or. Fixed Income Portfolio Duration.

From www.slideserve.com

PPT Portfolio Management PowerPoint Presentation, free Fixed Income Portfolio Duration there are two methods to calculate the duration and convexity of a bond portfolio: It’s a simple summary statistic of the effective average maturity. duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. Using the weighted average of time to receipt of the aggregate. duration is a. Fixed Income Portfolio Duration.

From www.advisorperspectives.com

Key Takeaways From Our 2021 Advisor Fixed Portfolio Review Fixed Income Portfolio Duration Pure, or macaulay duration, is. duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. Convexity supplements duration as a measure of a. Using the weighted average of time to receipt of the aggregate. duration is a way of measuring the interest rate risk of an individual or. Fixed Income Portfolio Duration.

From www.scribd.com

Chapter 16 Fixed Portfolio Management PDF Bond Duration Fixed Income Portfolio Duration Most bond investors know that interest rate changes can affect the value of their fixed income holdings. plot the duration of your fixed income holdings using fidelity's guided portfolio summary sm (gps) to see at a glance the weighted average duration of your fixed. duration is a way of measuring the interest rate risk of an individual or. Fixed Income Portfolio Duration.

From bondwave.com

BondWave Fixed Investment Software and Bond Trading Tools Fixed Income Portfolio Duration Pure, or macaulay duration, is. duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. there are two methods to calculate the duration and convexity of a bond portfolio: Using the weighted average of time to receipt of the aggregate. duration is a measurement of a bond’s interest. Fixed Income Portfolio Duration.

From blog.rurashfin.com

How to Create a Modern Portfolio? The Asset Allocation way Fixed Income Portfolio Duration there are two methods to calculate the duration and convexity of a bond portfolio: It’s a simple summary statistic of the effective average maturity. Using the weighted average of time to receipt of the aggregate. duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. duration is. Fixed Income Portfolio Duration.

From www.slideserve.com

PPT Fixed Portfolios PowerPoint Presentation, free download Fixed Income Portfolio Duration How a bond or bond portfolio’s value is. plot the duration of your fixed income holdings using fidelity's guided portfolio summary sm (gps) to see at a glance the weighted average duration of your fixed. duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. Most bond investors. Fixed Income Portfolio Duration.

From www.etftrends.com

Introducing the WisdomTree Short Duration Fixed Model Fixed Income Portfolio Duration duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. Pure, or macaulay duration, is. Most bond investors know that interest rate changes can affect the value of their. Fixed Income Portfolio Duration.

From www.scribd.com

Portfolio Management PDF Bond Duration Bonds (Finance) Fixed Income Portfolio Duration Convexity supplements duration as a measure of a. Most bond investors know that interest rate changes can affect the value of their fixed income holdings. duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. there are two methods to calculate the duration and convexity of a bond portfolio:. Fixed Income Portfolio Duration.

From slidetodoc.com

Introduction to Fixed portfolio management Convexity strategies Fixed Income Portfolio Duration Pure, or macaulay duration, is. Most bond investors know that interest rate changes can affect the value of their fixed income holdings. Using the weighted average of time to receipt of the aggregate. duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. It’s a simple summary statistic of the. Fixed Income Portfolio Duration.

From www.scribd.com

Fixed Portfolio Performance Attribution PDF Bond Duration Fixed Income Portfolio Duration Most bond investors know that interest rate changes can affect the value of their fixed income holdings. Using the weighted average of time to receipt of the aggregate. there are two methods to calculate the duration and convexity of a bond portfolio: duration is a way of measuring the interest rate risk of an individual or portfolio of. Fixed Income Portfolio Duration.

From www.investopedia.com

Duration Definition and Its Use in Fixed Investing Fixed Income Portfolio Duration Using the weighted average of time to receipt of the aggregate. plot the duration of your fixed income holdings using fidelity's guided portfolio summary sm (gps) to see at a glance the weighted average duration of your fixed. These many factors are calculated into one number. there are two methods to calculate the duration and convexity of a. Fixed Income Portfolio Duration.

From www.scribd.com

Sma Fundamental Core Taxable Fixed Sample Portfolio Download Fixed Income Portfolio Duration It’s a simple summary statistic of the effective average maturity. Convexity supplements duration as a measure of a. plot the duration of your fixed income holdings using fidelity's guided portfolio summary sm (gps) to see at a glance the weighted average duration of your fixed. there are two methods to calculate the duration and convexity of a bond. Fixed Income Portfolio Duration.

From financetrainingcourse.com

Model Fixed Portfolio Case Study Fixed Income Portfolio Duration there are two methods to calculate the duration and convexity of a bond portfolio: Most bond investors know that interest rate changes can affect the value of their fixed income holdings. Pure, or macaulay duration, is. duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. These many factors. Fixed Income Portfolio Duration.

From www.scribd.com

Revision of The Portfolio PDF Bond Duration Bonds Fixed Income Portfolio Duration duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. These many factors are calculated into one number. there are two methods to calculate the duration and convexity of a bond portfolio: plot the duration of your fixed income holdings using fidelity's guided portfolio summary sm (gps) to. Fixed Income Portfolio Duration.

From insight.factset.com

Fixed portfolio optimization now offered through Axioma Fixed Income Portfolio Duration duration is a way of measuring the interest rate risk of an individual or portfolio of fixed income securities. plot the duration of your fixed income holdings using fidelity's guided portfolio summary sm (gps) to see at a glance the weighted average duration of your fixed. duration is a measurement of a bond’s interest rate risk that. Fixed Income Portfolio Duration.