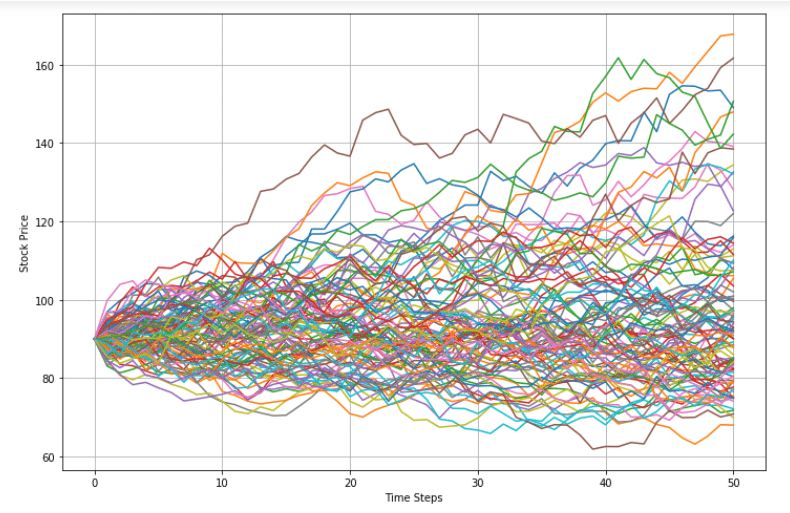

Monte Carlo Simulation Var . Thus, we simulate returns for the cac40 index using the garch (1,1) model. Value at risk (var) is a risk measure that quantifies the potential loss of a portfolio over a given time horizon at a certain. Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of a position based on the current value of a portfolio or security, the expected volatility and a time frame. Monte carlo transformation procedures employing a crude monte carlo estimator and sample size 1000 were applied to. Monte carlo var is a method for calculating value at risk (var) that uses a computational technique called monte carlo simulation to generate random scenarios based on historical data. Computing var with monte carlo simulations is very similar to historical simulations. The main difference lies in the first step of the. Figure 1 and 2 illustrate the garch simulated daily returns and volatility for the cac40 index. It is more flexible and can accommodate It is most commonly used

from ar.inspiredpencil.com

The main difference lies in the first step of the. Value at risk (var) is a risk measure that quantifies the potential loss of a portfolio over a given time horizon at a certain. Computing var with monte carlo simulations is very similar to historical simulations. Monte carlo transformation procedures employing a crude monte carlo estimator and sample size 1000 were applied to. Monte carlo var is a method for calculating value at risk (var) that uses a computational technique called monte carlo simulation to generate random scenarios based on historical data. It is most commonly used Figure 1 and 2 illustrate the garch simulated daily returns and volatility for the cac40 index. It is more flexible and can accommodate Thus, we simulate returns for the cac40 index using the garch (1,1) model. Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of a position based on the current value of a portfolio or security, the expected volatility and a time frame.

Monte Carlo Simulation Excel Template

Monte Carlo Simulation Var Monte carlo var is a method for calculating value at risk (var) that uses a computational technique called monte carlo simulation to generate random scenarios based on historical data. Value at risk (var) is a risk measure that quantifies the potential loss of a portfolio over a given time horizon at a certain. It is most commonly used It is more flexible and can accommodate Thus, we simulate returns for the cac40 index using the garch (1,1) model. The main difference lies in the first step of the. Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of a position based on the current value of a portfolio or security, the expected volatility and a time frame. Monte carlo transformation procedures employing a crude monte carlo estimator and sample size 1000 were applied to. Monte carlo var is a method for calculating value at risk (var) that uses a computational technique called monte carlo simulation to generate random scenarios based on historical data. Computing var with monte carlo simulations is very similar to historical simulations. Figure 1 and 2 illustrate the garch simulated daily returns and volatility for the cac40 index.

From getnave.com

Monte Carlo Simulation Explained How to Make Reliable Forecasts Nave Monte Carlo Simulation Var Value at risk (var) is a risk measure that quantifies the potential loss of a portfolio over a given time horizon at a certain. Monte carlo transformation procedures employing a crude monte carlo estimator and sample size 1000 were applied to. The main difference lies in the first step of the. Monte carlo var is a method for calculating value. Monte Carlo Simulation Var.

From www.slideserve.com

PPT The Role of Predictive Microbiology in Microbial Risk Assessment Monte Carlo Simulation Var Thus, we simulate returns for the cac40 index using the garch (1,1) model. Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of a position based on the current value of a portfolio or security, the expected volatility and a time frame. Value at risk (var) is a risk measure that quantifies. Monte Carlo Simulation Var.

From ar.inspiredpencil.com

Monte Carlo Simulation Excel Template Monte Carlo Simulation Var Figure 1 and 2 illustrate the garch simulated daily returns and volatility for the cac40 index. It is most commonly used The main difference lies in the first step of the. Value at risk (var) is a risk measure that quantifies the potential loss of a portfolio over a given time horizon at a certain. Monte carlo var is a. Monte Carlo Simulation Var.

From www.investopedia.com

Monte Carlo Simulation What It Is, How It Works, History, 4 Key Steps Monte Carlo Simulation Var Computing var with monte carlo simulations is very similar to historical simulations. Value at risk (var) is a risk measure that quantifies the potential loss of a portfolio over a given time horizon at a certain. Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of a position based on the current. Monte Carlo Simulation Var.

From howtomakechocolatemugcake.blogspot.com

Montecarlo Simulation Monte Carlo Simulation Tips and Tricks / The Monte Carlo Simulation Var Monte carlo var is a method for calculating value at risk (var) that uses a computational technique called monte carlo simulation to generate random scenarios based on historical data. Figure 1 and 2 illustrate the garch simulated daily returns and volatility for the cac40 index. It is more flexible and can accommodate Computing var with monte carlo simulations is very. Monte Carlo Simulation Var.

From dokumen.tips

(PPTX) MONTE CARLO SIMULATION. Topics History of Monte Carlo Simulation Monte Carlo Simulation Var The main difference lies in the first step of the. It is more flexible and can accommodate Figure 1 and 2 illustrate the garch simulated daily returns and volatility for the cac40 index. Computing var with monte carlo simulations is very similar to historical simulations. Value at risk (var) is a risk measure that quantifies the potential loss of a. Monte Carlo Simulation Var.

From www.investopedia.com

Value at Risk (VaR) Definition Monte Carlo Simulation Var It is most commonly used Figure 1 and 2 illustrate the garch simulated daily returns and volatility for the cac40 index. Thus, we simulate returns for the cac40 index using the garch (1,1) model. The main difference lies in the first step of the. It is more flexible and can accommodate Value at risk (var) is a risk measure that. Monte Carlo Simulation Var.

From www.solver.com

Monte Carlo Simulation Tutorial Statistics and Percentiles solver Monte Carlo Simulation Var It is more flexible and can accommodate Monte carlo transformation procedures employing a crude monte carlo estimator and sample size 1000 were applied to. Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of a position based on the current value of a portfolio or security, the expected volatility and a time. Monte Carlo Simulation Var.

From www.researchgate.net

Graphical depiction of the Monte Carlo simulation procedure. Download Monte Carlo Simulation Var Monte carlo transformation procedures employing a crude monte carlo estimator and sample size 1000 were applied to. Value at risk (var) is a risk measure that quantifies the potential loss of a portfolio over a given time horizon at a certain. It is most commonly used Thus, we simulate returns for the cac40 index using the garch (1,1) model. Figure. Monte Carlo Simulation Var.

From excel.tv

Monte Carlo Simulation Formula in Excel Tutorial and Download Excel TV Monte Carlo Simulation Var The main difference lies in the first step of the. It is most commonly used Monte carlo var is a method for calculating value at risk (var) that uses a computational technique called monte carlo simulation to generate random scenarios based on historical data. Monte carlo transformation procedures employing a crude monte carlo estimator and sample size 1000 were applied. Monte Carlo Simulation Var.

From www.vrogue.co

Monte Carlo Simulation Perform Monte Carlo Simulation vrogue.co Monte Carlo Simulation Var Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of a position based on the current value of a portfolio or security, the expected volatility and a time frame. Figure 1 and 2 illustrate the garch simulated daily returns and volatility for the cac40 index. The main difference lies in the first. Monte Carlo Simulation Var.

From www.youtube.com

[Arabic] Monte Carlo Simulation using R YouTube Monte Carlo Simulation Var Monte carlo var is a method for calculating value at risk (var) that uses a computational technique called monte carlo simulation to generate random scenarios based on historical data. Figure 1 and 2 illustrate the garch simulated daily returns and volatility for the cac40 index. Thus, we simulate returns for the cac40 index using the garch (1,1) model. Value at. Monte Carlo Simulation Var.

From www.youtube.com

Monte Carlo Simulation In Trading YouTube Monte Carlo Simulation Var The main difference lies in the first step of the. Figure 1 and 2 illustrate the garch simulated daily returns and volatility for the cac40 index. Monte carlo var is a method for calculating value at risk (var) that uses a computational technique called monte carlo simulation to generate random scenarios based on historical data. Monte carlo transformation procedures employing. Monte Carlo Simulation Var.

From www.youtube.com

Monte Carlo Simulation with value at risk (VaR) and conditional value Monte Carlo Simulation Var The main difference lies in the first step of the. Monte carlo transformation procedures employing a crude monte carlo estimator and sample size 1000 were applied to. It is more flexible and can accommodate Figure 1 and 2 illustrate the garch simulated daily returns and volatility for the cac40 index. Using monte carlo to calculate value at risk (var) var. Monte Carlo Simulation Var.

From valueatrisk.weebly.com

VaR Calculation Parametric Value at Risk Monte Carlo Simulation Monte Carlo Simulation Var The main difference lies in the first step of the. Thus, we simulate returns for the cac40 index using the garch (1,1) model. It is more flexible and can accommodate Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of a position based on the current value of a portfolio or security,. Monte Carlo Simulation Var.

From projectmanagementacademy.net

Understanding the Monte Carlo Analysis in Project Management Project Monte Carlo Simulation Var The main difference lies in the first step of the. Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of a position based on the current value of a portfolio or security, the expected volatility and a time frame. Value at risk (var) is a risk measure that quantifies the potential loss. Monte Carlo Simulation Var.

From towardsai.net

GOOG 10,000 Monte Carlo, Discovering VaR (Value at Risk) Towards AI Monte Carlo Simulation Var Monte carlo var is a method for calculating value at risk (var) that uses a computational technique called monte carlo simulation to generate random scenarios based on historical data. It is most commonly used Monte carlo transformation procedures employing a crude monte carlo estimator and sample size 1000 were applied to. The main difference lies in the first step of. Monte Carlo Simulation Var.

From www.mbrm.com

UNIVVAR Universal VaR Addin "ValueatRisk" Monte Carlo Simulation Var It is most commonly used Value at risk (var) is a risk measure that quantifies the potential loss of a portfolio over a given time horizon at a certain. Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of a position based on the current value of a portfolio or security, the. Monte Carlo Simulation Var.

From www.tejwin.com

Options Pricing with Monte Carlo Simulation TEJ Monte Carlo Simulation Var It is most commonly used Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of a position based on the current value of a portfolio or security, the expected volatility and a time frame. The main difference lies in the first step of the. Figure 1 and 2 illustrate the garch simulated. Monte Carlo Simulation Var.

From www.youtube.com

VaR thru Monte carlo simulation YouTube Monte Carlo Simulation Var It is most commonly used Monte carlo transformation procedures employing a crude monte carlo estimator and sample size 1000 were applied to. Value at risk (var) is a risk measure that quantifies the potential loss of a portfolio over a given time horizon at a certain. Using monte carlo to calculate value at risk (var) var is a measurement of. Monte Carlo Simulation Var.

From www.slideshare.net

Monte carlo simulation Monte Carlo Simulation Var It is more flexible and can accommodate Figure 1 and 2 illustrate the garch simulated daily returns and volatility for the cac40 index. Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of a position based on the current value of a portfolio or security, the expected volatility and a time frame.. Monte Carlo Simulation Var.

From www.researchgate.net

Which tools are easy for monte carlo simulation analysis? ResearchGate Monte Carlo Simulation Var Thus, we simulate returns for the cac40 index using the garch (1,1) model. Monte carlo var is a method for calculating value at risk (var) that uses a computational technique called monte carlo simulation to generate random scenarios based on historical data. Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of. Monte Carlo Simulation Var.

From www.youtube.com

Monte Carlo Simulation VaR YouTube Monte Carlo Simulation Var Monte carlo var is a method for calculating value at risk (var) that uses a computational technique called monte carlo simulation to generate random scenarios based on historical data. It is most commonly used Computing var with monte carlo simulations is very similar to historical simulations. Thus, we simulate returns for the cac40 index using the garch (1,1) model. Using. Monte Carlo Simulation Var.

From www.youtube.com

Monte Carlo Simulation of Value at Risk (VaR) in Excel YouTube Monte Carlo Simulation Var Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of a position based on the current value of a portfolio or security, the expected volatility and a time frame. Thus, we simulate returns for the cac40 index using the garch (1,1) model. The main difference lies in the first step of the.. Monte Carlo Simulation Var.

From www.youtube.com

Monte Carlo Simulation NPV example YouTube Monte Carlo Simulation Var Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of a position based on the current value of a portfolio or security, the expected volatility and a time frame. Monte carlo var is a method for calculating value at risk (var) that uses a computational technique called monte carlo simulation to generate. Monte Carlo Simulation Var.

From www.youtube.com

Monte Carlo simulation for Conditional VaR (Excel) YouTube Monte Carlo Simulation Var Computing var with monte carlo simulations is very similar to historical simulations. Thus, we simulate returns for the cac40 index using the garch (1,1) model. Figure 1 and 2 illustrate the garch simulated daily returns and volatility for the cac40 index. Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of a. Monte Carlo Simulation Var.

From risk-engineering.org

Estimating Value at Risk using Python Measures of exposure to Monte Carlo Simulation Var Computing var with monte carlo simulations is very similar to historical simulations. It is most commonly used Figure 1 and 2 illustrate the garch simulated daily returns and volatility for the cac40 index. Monte carlo var is a method for calculating value at risk (var) that uses a computational technique called monte carlo simulation to generate random scenarios based on. Monte Carlo Simulation Var.

From corporatefinanceinstitute.com

Modeling Risk with Monte Carlo I Finance Course I CFI Monte Carlo Simulation Var Monte carlo transformation procedures employing a crude monte carlo estimator and sample size 1000 were applied to. It is more flexible and can accommodate Thus, we simulate returns for the cac40 index using the garch (1,1) model. The main difference lies in the first step of the. Computing var with monte carlo simulations is very similar to historical simulations. Monte. Monte Carlo Simulation Var.

From www.financestrategists.com

Monte Carlo VaR Definition, Calculation, & Application Monte Carlo Simulation Var It is most commonly used The main difference lies in the first step of the. Value at risk (var) is a risk measure that quantifies the potential loss of a portfolio over a given time horizon at a certain. Monte carlo transformation procedures employing a crude monte carlo estimator and sample size 1000 were applied to. Computing var with monte. Monte Carlo Simulation Var.

From pmstudycircle.com

What is a Monte Carlo Simulation? PM Study Circle Monte Carlo Simulation Var Monte carlo transformation procedures employing a crude monte carlo estimator and sample size 1000 were applied to. It is more flexible and can accommodate The main difference lies in the first step of the. Monte carlo var is a method for calculating value at risk (var) that uses a computational technique called monte carlo simulation to generate random scenarios based. Monte Carlo Simulation Var.

From towardsdatascience.com

Monte Carlo Simulation in R with focus on Option Pricing by Ojasvin Monte Carlo Simulation Var It is more flexible and can accommodate Value at risk (var) is a risk measure that quantifies the potential loss of a portfolio over a given time horizon at a certain. Thus, we simulate returns for the cac40 index using the garch (1,1) model. Computing var with monte carlo simulations is very similar to historical simulations. Using monte carlo to. Monte Carlo Simulation Var.

From aquaq.co.uk

Calculating VaR using Monte Carlo Simulation AquaQ Monte Carlo Simulation Var Computing var with monte carlo simulations is very similar to historical simulations. Monte carlo transformation procedures employing a crude monte carlo estimator and sample size 1000 were applied to. It is most commonly used It is more flexible and can accommodate Thus, we simulate returns for the cac40 index using the garch (1,1) model. The main difference lies in the. Monte Carlo Simulation Var.

From www.analyticsvidhya.com

Monte Carlo Simulation Perform Monte Carlo Simulation in R Monte Carlo Simulation Var Monte carlo transformation procedures employing a crude monte carlo estimator and sample size 1000 were applied to. Using monte carlo to calculate value at risk (var) var is a measurement of the downside risk of a position based on the current value of a portfolio or security, the expected volatility and a time frame. It is more flexible and can. Monte Carlo Simulation Var.

From www.youtube.com

VaR Monte Carlo Simulation Value at Risk through Monte Carlo Monte Carlo Simulation Var Monte carlo transformation procedures employing a crude monte carlo estimator and sample size 1000 were applied to. The main difference lies in the first step of the. Computing var with monte carlo simulations is very similar to historical simulations. Monte carlo var is a method for calculating value at risk (var) that uses a computational technique called monte carlo simulation. Monte Carlo Simulation Var.

From www.carolinalago.com

Monte Carlo Simulation carolinalago Monte Carlo Simulation Var Thus, we simulate returns for the cac40 index using the garch (1,1) model. Monte carlo var is a method for calculating value at risk (var) that uses a computational technique called monte carlo simulation to generate random scenarios based on historical data. Computing var with monte carlo simulations is very similar to historical simulations. Figure 1 and 2 illustrate the. Monte Carlo Simulation Var.