What Is A Var Shock . quantitative easing and “var shocks”. A parallel shift in the japanese bond yield curve of 100bp, would cause a. the episode became known as the “var shock” of 2003. var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. a theoretical 100bp interest rate shock, i.e. Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. 1) what is var? A decade later and the threat of a “var shock” is once again.

from www.valuewalk.com

A decade later and the threat of a “var shock” is once again. the episode became known as the “var shock” of 2003. 1) what is var? A parallel shift in the japanese bond yield curve of 100bp, would cause a. a theoretical 100bp interest rate shock, i.e. value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. quantitative easing and “var shocks”. Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current.

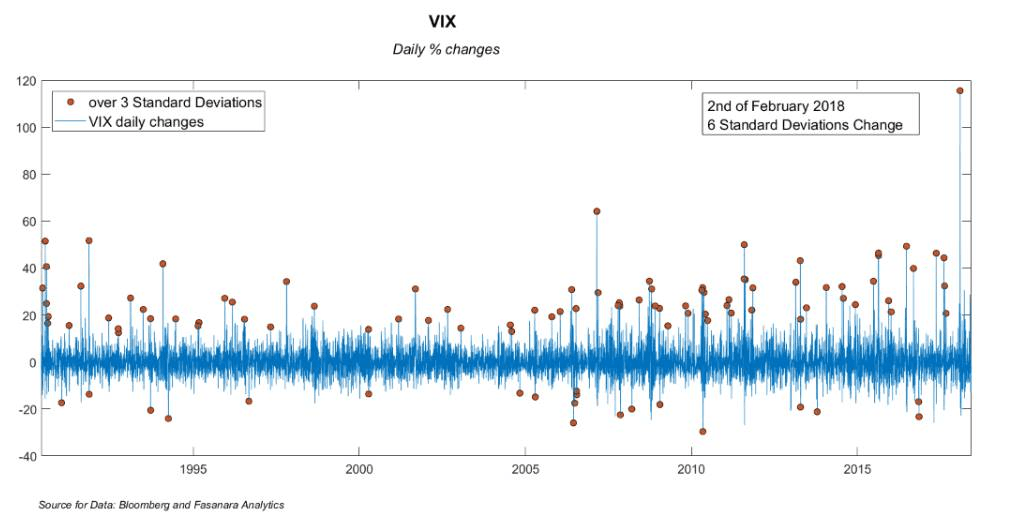

The Increasing Frequency Of VARShocks Is A Crash Hallmark

What Is A Var Shock 1) what is var? Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. quantitative easing and “var shocks”. the episode became known as the “var shock” of 2003. 1) what is var? A parallel shift in the japanese bond yield curve of 100bp, would cause a. A decade later and the threat of a “var shock” is once again. var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. a theoretical 100bp interest rate shock, i.e.

From www.medicalkidunya.com

Types of Shock Cheat Sheet medicalkidunya What Is A Var Shock A decade later and the threat of a “var shock” is once again. value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. quantitative easing and “var shocks”. a theoretical 100bp interest rate shock, i.e. the episode became known as the “var shock” of 2003. var. What Is A Var Shock.

From www.researchgate.net

Response of variables to " m2 " variable shock Download Scientific Diagram What Is A Var Shock var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. the episode became known as the “var shock” of 2003. Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market. What Is A Var Shock.

From www.charlesrcook.com

Normal Shock Ts Diagram What Is A Var Shock value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. var measures the potential maximum loss on a portfolio of investments over a given. What Is A Var Shock.

From www.osmosis.org

Shock Position What Is It, Uses, and More Osmosis What Is A Var Shock var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. the episode became known as the “var shock” of. What Is A Var Shock.

From www.fasanara.com

The Increasing Frequency of VARshocks is a Crash Hallmark Fasanara Capital What Is A Var Shock A parallel shift in the japanese bond yield curve of 100bp, would cause a. value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. the episode became known as the “var shock” of 2003. quantitative easing and “var shocks”. a theoretical 100bp interest rate shock, i.e. A. What Is A Var Shock.

From www.valuewalk.com

The Increasing Frequency Of VARShocks Is A Crash Hallmark What Is A Var Shock value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. quantitative easing and “var shocks”. var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. A decade later and the threat of a “var. What Is A Var Shock.

From tactical-medicine.com

Critical Care Fundamentals The Basics of Shock MEDTAC International Corp. What Is A Var Shock quantitative easing and “var shocks”. Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. A parallel shift in the japanese bond yield curve. What Is A Var Shock.

From www.researchgate.net

Aggregate Demand Shock in the Integrated VAR Download Scientific Diagram What Is A Var Shock the episode became known as the “var shock” of 2003. var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. a theoretical 100bp interest rate shock, i.e. value at risk (var) is a way for companies to assess their risk exposure by. What Is A Var Shock.

From www.slideserve.com

PPT Identifying Government Spending Shocks It’s all in the timing PowerPoint Presentation What Is A Var Shock a theoretical 100bp interest rate shock, i.e. 1) what is var? A parallel shift in the japanese bond yield curve of 100bp, would cause a. var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. the episode became known as the “var. What Is A Var Shock.

From www.researchgate.net

Impulse response of dependent to variable shocks. Download Scientific Diagram What Is A Var Shock A decade later and the threat of a “var shock” is once again. A parallel shift in the japanese bond yield curve of 100bp, would cause a. a theoretical 100bp interest rate shock, i.e. the episode became known as the “var shock” of 2003. value at risk (var) is a way for companies to assess their risk. What Is A Var Shock.

From www.valuewalk.com

The Increasing Frequency Of VARShocks Is A Crash Hallmark What Is A Var Shock the episode became known as the “var shock” of 2003. value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. A decade later and. What Is A Var Shock.

From www.researchgate.net

Reaction to an identified liquidity shock, monthly VAR with 12 lags Download Scientific Diagram What Is A Var Shock A parallel shift in the japanese bond yield curve of 100bp, would cause a. var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. quantitative easing and “var shocks”. the episode became known as the “var shock” of 2003. 1) what is. What Is A Var Shock.

From posts.themacrotourist.com

RIPPLING VAR SHOCKS by Kevin Muir The MacroTourist What Is A Var Shock A parallel shift in the japanese bond yield curve of 100bp, would cause a. a theoretical 100bp interest rate shock, i.e. Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. quantitative easing and “var shocks”. the episode became known as the. What Is A Var Shock.

From www.youtube.com

(Stata13) VAR and Impulse Response Functions (2) var irf impulseresponse innovations What Is A Var Shock the episode became known as the “var shock” of 2003. 1) what is var? a theoretical 100bp interest rate shock, i.e. var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. value at risk (var) is a way for companies to. What Is A Var Shock.

From www.slideserve.com

PPT Identifying Government Spending Shocks It’s all in the timing PowerPoint Presentation What Is A Var Shock 1) what is var? var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. quantitative easing and “var shocks”. A decade later and the threat of a “var shock” is once again. A parallel shift in the japanese bond yield curve of 100bp,. What Is A Var Shock.

From www.grc.nasa.gov

Normal Shock Wave Equations What Is A Var Shock A decade later and the threat of a “var shock” is once again. the episode became known as the “var shock” of 2003. Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. value at risk (var) is a way for companies to. What Is A Var Shock.

From www.semanticscholar.org

Figure 1 from An optimal replacement policy under variable shocks and selfhealing patterns What Is A Var Shock quantitative easing and “var shocks”. A decade later and the threat of a “var shock” is once again. A parallel shift in the japanese bond yield curve of 100bp, would cause a. value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. Var, i.e., value at risk, is a. What Is A Var Shock.

From www.researchgate.net

2 Response of Output Growth to Structural VAR Shocks Download Scientific Diagram What Is A Var Shock value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. A decade later and the threat of a “var shock” is once again. A parallel. What Is A Var Shock.

From www.valuewalk.com

The Increasing Frequency Of VARShocks Is A Crash Hallmark What Is A Var Shock Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. the episode became known as the “var shock” of. What Is A Var Shock.

From www.researchgate.net

Fiscal Policy Transmission According to VAR Model Effects of VAR... Download Scientific Diagram What Is A Var Shock value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. quantitative easing and “var shocks”. A parallel shift in the japanese bond yield curve. What Is A Var Shock.

From www.grc.nasa.gov

Normal Shock Wave Equations What Is A Var Shock the episode became known as the “var shock” of 2003. a theoretical 100bp interest rate shock, i.e. 1) what is var? value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. A parallel shift in the japanese bond yield curve of 100bp, would cause a. A decade. What Is A Var Shock.

From www.youtube.com

(EViews10) VAR and Impulse Response Functions (1)var irf impulseresponse innovations What Is A Var Shock the episode became known as the “var shock” of 2003. quantitative easing and “var shocks”. Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. A parallel shift in the japanese bond yield curve of 100bp, would cause a. value at risk. What Is A Var Shock.

From www.valuewalk.com

The Increasing Frequency Of VARShocks Is A Crash Hallmark What Is A Var Shock var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. a theoretical 100bp interest rate shock, i.e. Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. A parallel. What Is A Var Shock.

From present5.com

ABCs of Shock Pediatric Critical Care Medicine Emory What Is A Var Shock a theoretical 100bp interest rate shock, i.e. Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. 1) what is var? A decade later and the threat of a “var shock” is once again. A parallel shift in the japanese bond yield curve. What Is A Var Shock.

From www.researchgate.net

Impulse Responses to Uncertainty Shock in the VAR Model. Notes Shaded... Download Scientific What Is A Var Shock A decade later and the threat of a “var shock” is once again. quantitative easing and “var shocks”. Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. A parallel shift in the japanese bond yield curve of 100bp, would cause a. 1). What Is A Var Shock.

From www.researchgate.net

IRFs in VAR, DVAR, and SVAR Shock to Domestic Consumption (QHM). Download Scientific Diagram What Is A Var Shock Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. A parallel shift in the japanese bond yield curve of 100bp, would cause a. the episode became known as the “var shock” of 2003. quantitative easing and “var shocks”. var measures the. What Is A Var Shock.

From www.slideserve.com

PPT Physiology of shock PowerPoint Presentation, free download ID515401 What Is A Var Shock a theoretical 100bp interest rate shock, i.e. A parallel shift in the japanese bond yield curve of 100bp, would cause a. 1) what is var? value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. the episode became known as the “var shock” of 2003. var. What Is A Var Shock.

From www.researchgate.net

Structural Shocks from a VAR with Excess Stock Returns —Fiscal and and... Download Scientific What Is A Var Shock var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. the episode became known as the “var shock” of 2003. a theoretical 100bp interest rate shock, i.e. 1) what is var? A decade later and the threat of a “var shock” is. What Is A Var Shock.

From www.osmosis.org

Approach to shock Clinical sciences Osmosis Video Library What Is A Var Shock Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. the episode became known as the “var shock” of 2003. A decade later and the threat of a “var shock” is once again. 1) what is var? A parallel shift in the japanese. What Is A Var Shock.

From www.youtube.com

(EViews10) VAR and Impulse Response Functions (2) var irf impulseresponse innovations What Is A Var Shock value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. A parallel shift in the japanese bond yield curve of 100bp, would cause a. . What Is A Var Shock.

From www.slideserve.com

PPT Technical tips on time series with Stata PowerPoint Presentation ID1081243 What Is A Var Shock value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. a theoretical 100bp interest rate shock, i.e. var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. quantitative easing and “var shocks”. . What Is A Var Shock.

From www.researchgate.net

VAR and Model Impulse Responses to a Technology Shock Download Scientific Diagram What Is A Var Shock var measures the potential maximum loss on a portfolio of investments over a given period of time, and is calculated using historical returns, current. Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. a theoretical 100bp interest rate shock, i.e. quantitative. What Is A Var Shock.

From www.aptech.com

Introduction to the Fundamentals of Vector Autoregressive Models Aptech What Is A Var Shock the episode became known as the “var shock” of 2003. quantitative easing and “var shocks”. Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. a theoretical 100bp interest rate shock, i.e. A parallel shift in the japanese bond yield curve of. What Is A Var Shock.

From www.r-econometrics.com

An Introduction to Impulse Response Analysis of VAR Models · reconometrics What Is A Var Shock A parallel shift in the japanese bond yield curve of 100bp, would cause a. A decade later and the threat of a “var shock” is once again. Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. value at risk (var) is a way. What Is A Var Shock.

From www.researchgate.net

VAR specification sensitivity Neutral technology shock. Download Scientific Diagram What Is A Var Shock Var, i.e., value at risk, is a measure of how much money you might lose ‘worst case’ based on your current positions (i.e., market risk. value at risk (var) is a way for companies to assess their risk exposure by quantifying the maximum possible. a theoretical 100bp interest rate shock, i.e. quantitative easing and “var shocks”. . What Is A Var Shock.