Portfolio With Highest Sharpe Ratio . What is the sharpe ratio? The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. The sharpe ratio can be used. Calculating the sharpe ratio involves three key components: Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period.

from www.chegg.com

Calculating the sharpe ratio involves three key components: What is the sharpe ratio? The sharpe ratio can be used. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in.

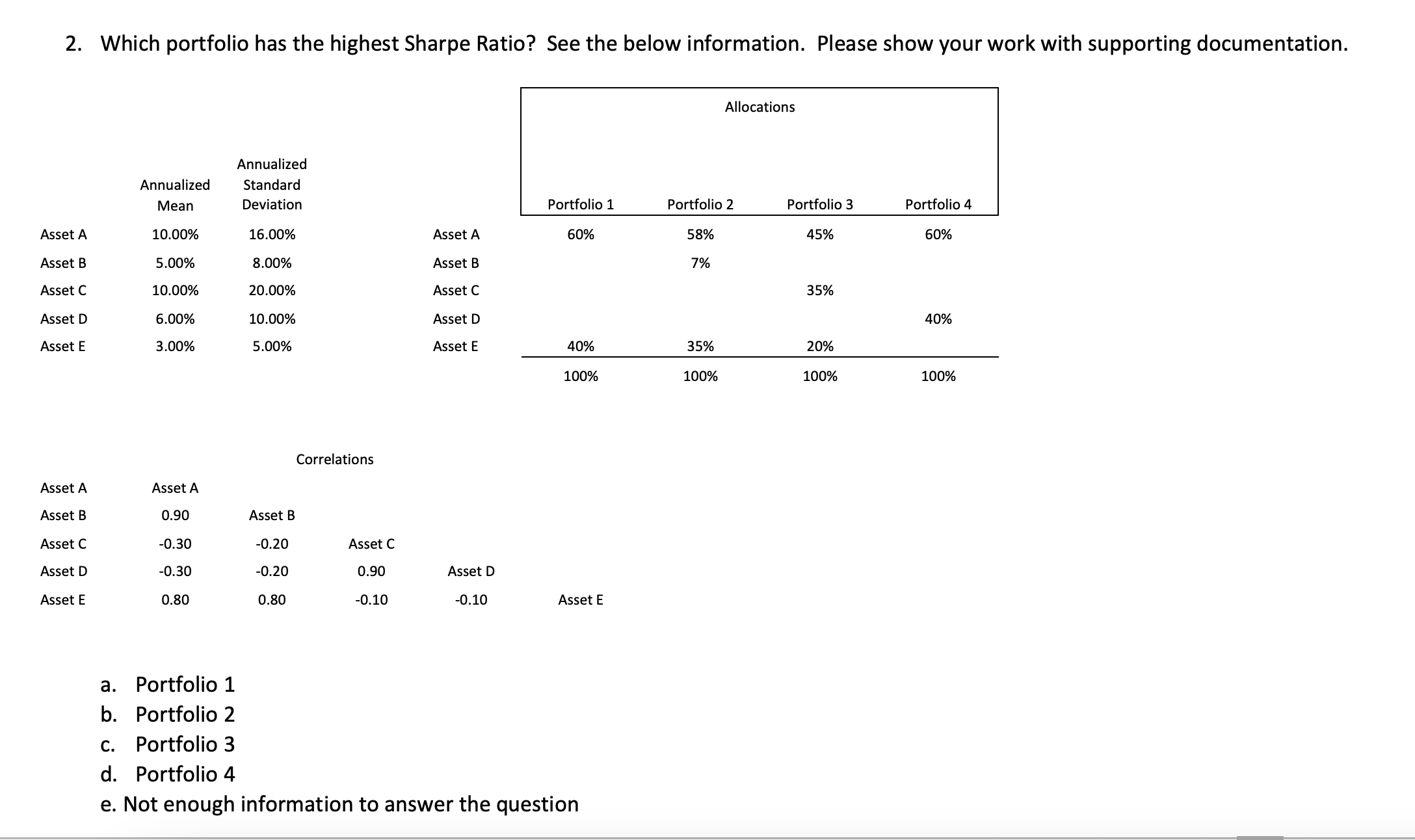

Solved Which portfolio has the highest Sharpe Ratio? See the

Portfolio With Highest Sharpe Ratio Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. The sharpe ratio can be used. What is the sharpe ratio? Calculating the sharpe ratio involves three key components: Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in.

From www.researchgate.net

Positions on Carbon Credits that provide portfolios with the Highest Portfolio With Highest Sharpe Ratio Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. Calculating the sharpe ratio involves three key components: What is the sharpe ratio? The sharpe ratio can be used. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is. Portfolio With Highest Sharpe Ratio.

From www.researchgate.net

The highest average Sharpe ratio attained by the equalweight portfolio Portfolio With Highest Sharpe Ratio Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. What is the sharpe ratio? Calculating the sharpe ratio involves three key components: The sharpe ratio can be used. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is. Portfolio With Highest Sharpe Ratio.

From www.researchgate.net

(PDF) An Algorithm for Finding a Portfolio with the Highest Sharpe Ratio Portfolio With Highest Sharpe Ratio Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. Calculating the sharpe ratio involves three key components: What is the sharpe ratio? The sharpe ratio can be used. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is. Portfolio With Highest Sharpe Ratio.

From www.researchgate.net

9 Sharpe ratio and optimal investing. Download Scientific Diagram Portfolio With Highest Sharpe Ratio Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. The sharpe ratio can be used. Calculating the sharpe ratio involves three key components: The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to. Portfolio With Highest Sharpe Ratio.

From mobi-me.net

What is the Sharpe ratio? How investors use it to analyze an asset's Portfolio With Highest Sharpe Ratio Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. What is the sharpe ratio? The sharpe ratio can be used. Calculating the sharpe ratio involves three key components: The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is. Portfolio With Highest Sharpe Ratio.

From seekingalpha.com

The Sharpe Ratio Why It's So Darn ImportantAnd How To Find It For Portfolio With Highest Sharpe Ratio Calculating the sharpe ratio involves three key components: The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. The sharpe ratio can be used. What is the sharpe ratio? Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected. Portfolio With Highest Sharpe Ratio.

From www.researchgate.net

The return performance of the highest Sharpe ratio portfolio and Portfolio With Highest Sharpe Ratio The sharpe ratio can be used. Calculating the sharpe ratio involves three key components: Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. What is the sharpe ratio? The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is. Portfolio With Highest Sharpe Ratio.

From investexcel.net

Calculating a Sharpe Optimal Portfolio with Excel Portfolio With Highest Sharpe Ratio What is the sharpe ratio? The sharpe ratio can be used. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. Calculating the sharpe ratio involves three key components: The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is. Portfolio With Highest Sharpe Ratio.

From www.researchgate.net

The highest average Sharpe ratio attained by the minimumvariance Portfolio With Highest Sharpe Ratio The sharpe ratio can be used. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. What is the. Portfolio With Highest Sharpe Ratio.

From gregorygundersen.com

The Capital Asset Pricing Model Portfolio With Highest Sharpe Ratio Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. Calculating the sharpe ratio involves three key components: The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. The. Portfolio With Highest Sharpe Ratio.

From www.linkedin.com

Calculating a Portfolio Sharpe Ratio with Python Portfolio With Highest Sharpe Ratio The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. What is the sharpe ratio? Calculating the sharpe ratio. Portfolio With Highest Sharpe Ratio.

From www.financialsamurai.com

Explaining The Sharpe Ratio In Investing Financial Samurai Portfolio With Highest Sharpe Ratio The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. Calculating the sharpe ratio involves three key components: What. Portfolio With Highest Sharpe Ratio.

From www.tickertape.in

Sharpe Ratio Meaning, Formula, Examples, and More Glossary by Portfolio With Highest Sharpe Ratio The sharpe ratio can be used. Calculating the sharpe ratio involves three key components: What is the sharpe ratio? Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is. Portfolio With Highest Sharpe Ratio.

From www.researchgate.net

The Efficient frontier and the tangent portfolio Download Scientific Portfolio With Highest Sharpe Ratio Calculating the sharpe ratio involves three key components: The sharpe ratio can be used. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. What is the sharpe ratio? The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is. Portfolio With Highest Sharpe Ratio.

From www.linkedin.com

Portfolio optimization from the highest Sharpe Ratio to minimum volatility Portfolio With Highest Sharpe Ratio The sharpe ratio can be used. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. Calculating the sharpe. Portfolio With Highest Sharpe Ratio.

From pictureperfectportfolios.com

How To Build A Maximum Sharpe Ratio Portfolio A Complete Guide Portfolio With Highest Sharpe Ratio Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. Calculating the sharpe ratio involves three key components: What is the sharpe ratio? The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the. Portfolio With Highest Sharpe Ratio.

From www.awesomefintech.com

Sharpe Ratio AwesomeFinTech Blog Portfolio With Highest Sharpe Ratio The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. What is the sharpe ratio? Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. The sharpe ratio can. Portfolio With Highest Sharpe Ratio.

From www.marottaonmoney.com

What Is The Sharpe Ratio? Marotta On Money Portfolio With Highest Sharpe Ratio Calculating the sharpe ratio involves three key components: What is the sharpe ratio? The sharpe ratio can be used. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected. Portfolio With Highest Sharpe Ratio.

From seekingalpha.com

The Sharpe Ratio Why It's So Darn ImportantAnd How To Find It For Portfolio With Highest Sharpe Ratio The sharpe ratio can be used. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. What is the sharpe ratio? Calculating the sharpe ratio involves three key components: The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is. Portfolio With Highest Sharpe Ratio.

From efinancemanagement.com

What is Sharpe Ratio Formula, Example, Importance Portfolio With Highest Sharpe Ratio What is the sharpe ratio? The sharpe ratio can be used. Calculating the sharpe ratio involves three key components: The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected. Portfolio With Highest Sharpe Ratio.

From www.hivelr.com

Sharpe Ratio How to Identify Winning Investments Hivelr Portfolio With Highest Sharpe Ratio Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. The sharpe ratio can be used. What is the sharpe ratio? Calculating the sharpe ratio involves three key components: The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is. Portfolio With Highest Sharpe Ratio.

From www.youtube.com

Tangency Portfolio,The Efficient Frontier, Capital Market Line, Sharpe Portfolio With Highest Sharpe Ratio Calculating the sharpe ratio involves three key components: The sharpe ratio can be used. What is the sharpe ratio? The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected. Portfolio With Highest Sharpe Ratio.

From spreadcheaters.com

How To Calculate The Sharpe Ratio In Excel SpreadCheaters Portfolio With Highest Sharpe Ratio The sharpe ratio can be used. Calculating the sharpe ratio involves three key components: What is the sharpe ratio? The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected. Portfolio With Highest Sharpe Ratio.

From marketxls.com

Sharpe Ratio of Portfolio (with MarketXLS Formulas) Portfolio With Highest Sharpe Ratio Calculating the sharpe ratio involves three key components: Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. The sharpe ratio can be used. What is the sharpe ratio? The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is. Portfolio With Highest Sharpe Ratio.

From www.chegg.com

Solved Which portfolio has the highest Sharpe Ratio? See the Portfolio With Highest Sharpe Ratio The sharpe ratio can be used. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. Calculating the sharpe ratio involves three key components: What is the sharpe ratio? Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected. Portfolio With Highest Sharpe Ratio.

From www.scribd.com

Sharpe Ratio Optimal Portfolio Portfolio With Highest Sharpe Ratio What is the sharpe ratio? Calculating the sharpe ratio involves three key components: The sharpe ratio can be used. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected. Portfolio With Highest Sharpe Ratio.

From www.researchgate.net

Annualized Sharpe Ratios of the bestinclass portfolios Download Portfolio With Highest Sharpe Ratio Calculating the sharpe ratio involves three key components: The sharpe ratio can be used. What is the sharpe ratio? Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is. Portfolio With Highest Sharpe Ratio.

From optionalpha.com

Portfolio Performance Metrics [Guide] Portfolio With Highest Sharpe Ratio What is the sharpe ratio? Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. The sharpe ratio can be used. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy. Portfolio With Highest Sharpe Ratio.

From caia.org

Sharpe Week The Sharpe Ratio Broke Investors’ Brains Portfolio for Portfolio With Highest Sharpe Ratio The sharpe ratio can be used. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. Calculating the sharpe ratio involves three key components: Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of. Portfolio With Highest Sharpe Ratio.

From analystprep.com

Application of the Information Ratio CFA, FRM, and Actuarial Exams Portfolio With Highest Sharpe Ratio What is the sharpe ratio? The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. The sharpe ratio can be used. Calculating the sharpe ratio involves three key components: Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected. Portfolio With Highest Sharpe Ratio.

From pictureperfectportfolios.com

How To Build A Maximum Sharpe Ratio Portfolio A Complete Guide Portfolio With Highest Sharpe Ratio What is the sharpe ratio? Calculating the sharpe ratio involves three key components: The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11%. Portfolio With Highest Sharpe Ratio.

From pictureperfectportfolios.com

How To Build A Maximum Sharpe Ratio Portfolio A Complete Guide Portfolio With Highest Sharpe Ratio What is the sharpe ratio? The sharpe ratio can be used. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the. Portfolio With Highest Sharpe Ratio.

From www.reddit.com

Introducing Sharpe Ratios Why Investing is Not Only About Returns r Portfolio With Highest Sharpe Ratio The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. The sharpe ratio can be used. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. What is the. Portfolio With Highest Sharpe Ratio.

From seekingalpha.com

The Sharpe Ratio Why It's So Darn ImportantAnd How To Find It For Portfolio With Highest Sharpe Ratio The sharpe ratio can be used. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected to deliver a return of 11% over the same period. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. What is the. Portfolio With Highest Sharpe Ratio.

From www.researchgate.net

Portfolio Sharpe and Treynor Ratios Download Table Portfolio With Highest Sharpe Ratio What is the sharpe ratio? Calculating the sharpe ratio involves three key components: The sharpe ratio can be used. The sharpe ratio over 5 years of max sharpe portfolio is 1.12, which is larger, thus better compared to the benchmark spy (0.66) in. Portfolio a is expected to return 14% over the next 12 months, while portfolio b is expected. Portfolio With Highest Sharpe Ratio.