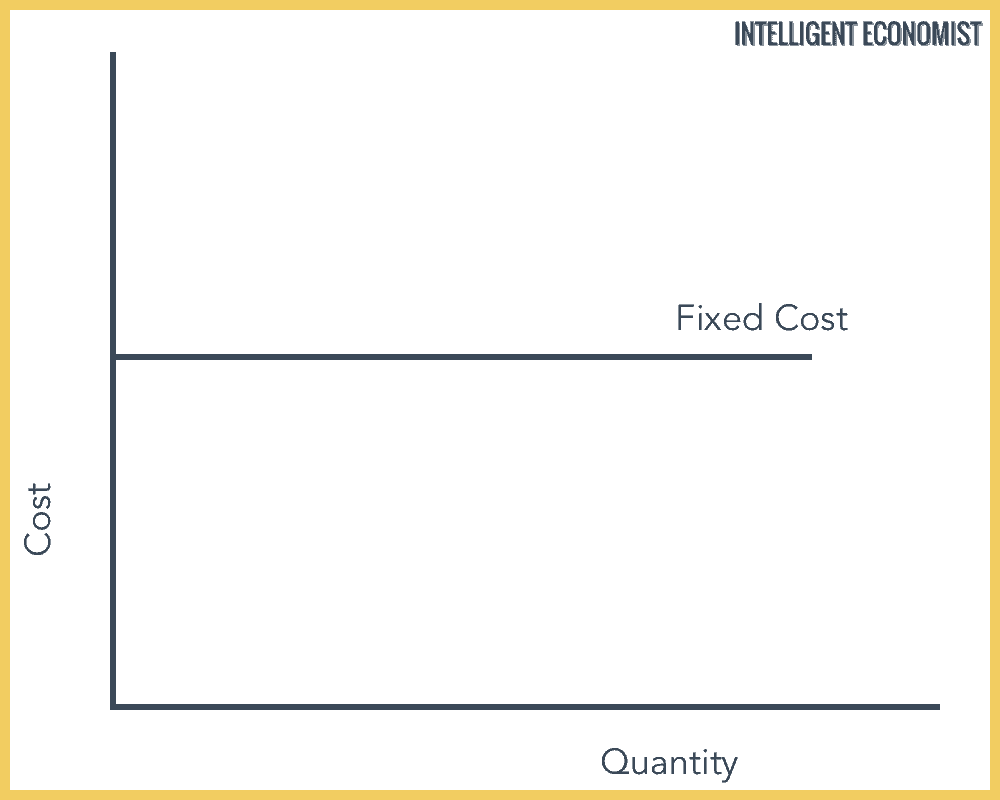

Fixed And Variable Costs Remain Constant In The Short Run . Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average fixed cost,. Understand that every factor of production has a corresponding factor price. Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Examples of fixed costs include rent on. Fixed costs remain constant regardless of output. Describe the relationship between production and costs, including average and marginal costs; Fixed costs remain constant in the short run because the firm cannot change its fixed inputs.

from www.intelligenteconomist.com

Fixed costs remain constant regardless of output. Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Describe the relationship between production and costs, including average and marginal costs; Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average fixed cost,. Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Understand that every factor of production has a corresponding factor price. Examples of fixed costs include rent on.

Theory Of Production Cost Theory Intelligent Economist

Fixed And Variable Costs Remain Constant In The Short Run Understand that every factor of production has a corresponding factor price. Understand that every factor of production has a corresponding factor price. Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average fixed cost,. Fixed costs remain constant regardless of output. Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Describe the relationship between production and costs, including average and marginal costs; Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Examples of fixed costs include rent on.

From www.numerade.com

SOLVEDIf a product's fixed costs increase and its selling price and variable costs remain Fixed And Variable Costs Remain Constant In The Short Run Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average fixed. Fixed And Variable Costs Remain Constant In The Short Run.

From agiled.app

Differences Between Fixed Cost and Variable Cost Fixed And Variable Costs Remain Constant In The Short Run Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Understand that every factor of production has a corresponding factor price. Fixed costs remain constant regardless of output. Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Understand the terms. Fixed And Variable Costs Remain Constant In The Short Run.

From www.intelligenteconomist.com

Theory Of Production Cost Theory Intelligent Economist Fixed And Variable Costs Remain Constant In The Short Run Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Examples of fixed costs include rent on. Describe the relationship between production and costs, including average and marginal costs; Understand that every. Fixed And Variable Costs Remain Constant In The Short Run.

From www.slideserve.com

PPT Cost of Production PowerPoint Presentation, free download ID6696923 Fixed And Variable Costs Remain Constant In The Short Run Understand that every factor of production has a corresponding factor price. Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Describe the relationship between production and costs, including average and marginal. Fixed And Variable Costs Remain Constant In The Short Run.

From byjus.com

Short Run Supply Curve of a Firm Cases In Short Run Supply Curve of a Firm Fixed And Variable Costs Remain Constant In The Short Run Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Describe the relationship between production and costs, including average and marginal costs; Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average fixed cost,. Examples of. Fixed And Variable Costs Remain Constant In The Short Run.

From www.tutor2u.net

Explaining Fixed and Variable Costs of Production tutor2u Economics Fixed And Variable Costs Remain Constant In The Short Run Fixed costs remain constant regardless of output. Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average fixed cost,. Examples of fixed costs include rent on. Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production.. Fixed And Variable Costs Remain Constant In The Short Run.

From riable.com

Fixed Costs Riable Fixed And Variable Costs Remain Constant In The Short Run Understand that every factor of production has a corresponding factor price. Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average fixed cost,. Fixed costs remain. Fixed And Variable Costs Remain Constant In The Short Run.

From byjus.com

Short Run Costs Definition What Is Short Run Costs Fixed And Variable Costs Remain Constant In The Short Run Understand that every factor of production has a corresponding factor price. Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Examples of fixed costs include rent on. Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Firms categorize costs into fixed costs, which remain constant regardless of. Fixed And Variable Costs Remain Constant In The Short Run.

From www.educba.com

Fixed Cost Vs Variable Cost Top 12 Key Differences & Examples Fixed And Variable Costs Remain Constant In The Short Run Examples of fixed costs include rent on. Understand that every factor of production has a corresponding factor price. Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Describe the relationship between production and costs, including average and marginal costs; Short run cost curves include total, fixed,. Fixed And Variable Costs Remain Constant In The Short Run.

From policonomics.com

Variable costs variable costs depend on the level of production, and can include things such as Fixed And Variable Costs Remain Constant In The Short Run Describe the relationship between production and costs, including average and marginal costs; Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Understand that every factor of production has a corresponding factor price. Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average. Fixed And Variable Costs Remain Constant In The Short Run.

From www.intelligenteconomist.com

Theory Of Production Cost Theory Intelligent Economist Fixed And Variable Costs Remain Constant In The Short Run Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average fixed cost,. Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Fixed costs remain constant regardless of output. Short run cost curves include total, fixed, and variable costs, as well as marginal. Fixed And Variable Costs Remain Constant In The Short Run.

From www.economicshelp.org

Diagrams of Cost Curves Economics Help Fixed And Variable Costs Remain Constant In The Short Run Fixed costs remain constant regardless of output. Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average fixed cost,. Understand that every factor of production has a corresponding factor price. Examples of fixed costs. Fixed And Variable Costs Remain Constant In The Short Run.

From boycewire.com

Fixed Cost Definition BoyceWire Fixed And Variable Costs Remain Constant In The Short Run Describe the relationship between production and costs, including average and marginal costs; Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which. Fixed And Variable Costs Remain Constant In The Short Run.

From www.economicshelp.org

Diagrams of Cost Curves Economics Help Fixed And Variable Costs Remain Constant In The Short Run Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Examples of fixed costs include rent on. Fixed costs remain constant regardless of output. Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Understand the terms associated with costs in the short run—total variable cost, total fixed cost,. Fixed And Variable Costs Remain Constant In The Short Run.

From arinjayacademy.com

Short Run Cost in Economics Class 11 Notes Microeconomics Fixed And Variable Costs Remain Constant In The Short Run Examples of fixed costs include rent on. Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Fixed costs remain constant regardless of output. Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Understand the terms associated with costs in the short run—total variable cost, total fixed cost,. Fixed And Variable Costs Remain Constant In The Short Run.

From www.coursehero.com

[Solved] On the breakeven graph, if sales price and variable cost remain... Course Hero Fixed And Variable Costs Remain Constant In The Short Run Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Understand that every factor of production has a corresponding factor price. Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change. Fixed And Variable Costs Remain Constant In The Short Run.

From www.freepik.com

Premium Vector Short Run Average Costs in economics for Average Fixed Cost Average Variable Cost Fixed And Variable Costs Remain Constant In The Short Run Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average fixed cost,. Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level. Fixed And Variable Costs Remain Constant In The Short Run.

From www.slideshare.net

ShortRun Costs and Output Decisions Fixed And Variable Costs Remain Constant In The Short Run Examples of fixed costs include rent on. Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Fixed costs remain constant regardless of output. Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Understand the terms associated with costs in the. Fixed And Variable Costs Remain Constant In The Short Run.

From tutorstips.com

Short Run Costs Total Cost, Fixed Cost and Variable Cost Tutor's Tips Fixed And Variable Costs Remain Constant In The Short Run Fixed costs remain constant regardless of output. Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average fixed cost,. Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Examples of fixed costs include rent on. Describe the relationship between production and costs, including. Fixed And Variable Costs Remain Constant In The Short Run.

From www.chegg.com

Solved If a firm shuts down, its fixed costs remain Fixed And Variable Costs Remain Constant In The Short Run Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Understand that every factor of production has a corresponding factor price. Short run cost curves include total, fixed, and variable costs,. Fixed And Variable Costs Remain Constant In The Short Run.

From www.youtube.com

Short run Cost curve Total Variable Cost (With Numerical Example) YouTube Fixed And Variable Costs Remain Constant In The Short Run Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Understand that every factor of production has a corresponding factor price. Fixed costs remain constant regardless of output. Examples of fixed costs include rent on. Describe the relationship between production and costs, including average and marginal costs; Firms categorize costs into fixed costs, which. Fixed And Variable Costs Remain Constant In The Short Run.

From penpoin.com

Total Variable Cost Examples, Curve, Importance Fixed And Variable Costs Remain Constant In The Short Run Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Understand that every factor of production has a corresponding factor price. Describe the relationship between production and costs, including average and marginal. Fixed And Variable Costs Remain Constant In The Short Run.

From www.chegg.com

Solved As a firm produces more units of a good, its 50 a Fixed And Variable Costs Remain Constant In The Short Run Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Fixed costs remain constant regardless of output. Understand that every factor of production has a corresponding factor price. Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable. Fixed And Variable Costs Remain Constant In The Short Run.

From napkinfinance.com

What is Fixed Cost vs. Variable Cost? Napkin Finance Fixed And Variable Costs Remain Constant In The Short Run Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Fixed costs remain constant regardless of output. Examples of fixed costs include rent on. Describe the relationship between production and costs, including. Fixed And Variable Costs Remain Constant In The Short Run.

From open.oregonstate.education

Module 8 Cost Curves Intermediate Microeconomics Fixed And Variable Costs Remain Constant In The Short Run Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Examples of fixed costs include rent on. Describe the relationship between production and costs, including average and marginal costs; Short run. Fixed And Variable Costs Remain Constant In The Short Run.

From readingandwritingprojectcom.web.fc2.com

fixed costs of production in the short run quizlet Fixed And Variable Costs Remain Constant In The Short Run Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Understand that every factor of production has a corresponding factor price. Describe the relationship between production and costs, including average and marginal costs; Examples of fixed costs include rent on. Firms categorize costs into fixed costs, which remain constant regardless of output level, and. Fixed And Variable Costs Remain Constant In The Short Run.

From napkinfinance.com

What is Fixed Cost vs. Variable Cost? Napkin Finance Fixed And Variable Costs Remain Constant In The Short Run Understand that every factor of production has a corresponding factor price. Describe the relationship between production and costs, including average and marginal costs; Fixed costs remain constant regardless of output. Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Understand the terms associated with costs in the short run—total variable cost, total fixed cost,. Fixed And Variable Costs Remain Constant In The Short Run.

From www.freepik.com

Premium Vector Production Costs in the Short Run for Total Cost Curves Total Variable Cost Fixed And Variable Costs Remain Constant In The Short Run Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average fixed cost,. Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Examples of fixed costs include rent on. Firms categorize costs into fixed costs, which remain constant regardless of output level, and. Fixed And Variable Costs Remain Constant In The Short Run.

From www.1099cafe.com

What is a Fixed Cost Variable vs Fixed Expenses — 1099 Cafe Fixed And Variable Costs Remain Constant In The Short Run Examples of fixed costs include rent on. Understand that every factor of production has a corresponding factor price. Describe the relationship between production and costs, including average and marginal costs; Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average fixed cost,. Firms categorize costs into fixed costs, which. Fixed And Variable Costs Remain Constant In The Short Run.

From open.lib.umn.edu

8.1 Production Choices and Costs The Short Run Principles of Economics Fixed And Variable Costs Remain Constant In The Short Run Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average fixed cost,. Understand that every factor of production. Fixed And Variable Costs Remain Constant In The Short Run.

From www.slideserve.com

PPT Cost PowerPoint Presentation, free download ID5717240 Fixed And Variable Costs Remain Constant In The Short Run Describe the relationship between production and costs, including average and marginal costs; Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Fixed costs remain constant regardless of output. Examples of fixed. Fixed And Variable Costs Remain Constant In The Short Run.

From evieyouthsantiago.blogspot.com

The Equation That Best Describes a Mixed Cost Is Fixed And Variable Costs Remain Constant In The Short Run Examples of fixed costs include rent on. Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average fixed cost,. Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Describe the relationship between production and costs, including average and marginal costs; Firms categorize. Fixed And Variable Costs Remain Constant In The Short Run.

From www.slideserve.com

PPT Production and Cost PowerPoint Presentation, free download ID5558499 Fixed And Variable Costs Remain Constant In The Short Run Understand that every factor of production has a corresponding factor price. Examples of fixed costs include rent on. Understand the terms associated with costs in the short run—total variable cost, total fixed cost, total cost, average variable cost, average fixed cost,. Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Firms categorize costs into. Fixed And Variable Costs Remain Constant In The Short Run.

From www.pedigogy.com

Fixed and Variable Costs Pedigogy Fixed And Variable Costs Remain Constant In The Short Run Fixed costs remain constant regardless of output. Firms categorize costs into fixed costs, which remain constant regardless of output level, and variable costs, which change with the level of production. Examples of fixed costs include rent on. Fixed costs remain constant in the short run because the firm cannot change its fixed inputs. Short run cost curves include total, fixed,. Fixed And Variable Costs Remain Constant In The Short Run.

From efinancemanagement.com

Variable Costs and Fixed Costs Fixed And Variable Costs Remain Constant In The Short Run Understand that every factor of production has a corresponding factor price. Short run cost curves include total, fixed, and variable costs, as well as marginal costs. Examples of fixed costs include rent on. Describe the relationship between production and costs, including average and marginal costs; Fixed costs remain constant regardless of output. Understand the terms associated with costs in the. Fixed And Variable Costs Remain Constant In The Short Run.