Fixed Cost Kahulugan . Fixed costs are expenses that do not change with increases or decreases in production or sales volumes. Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm. To calculate fixed costs, identify all expenses that remain constant regardless of production levels. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. That is to say, fixed costs remain constant for a given period despite. Sum these costs, including rent, salaries, and insurance. Fixed cost is a cost that remains fixed regardless of the quantity produced, i.e., whether the company increases or decreases the production of the product the cost of the product will remain.

from www.vrogue.co

Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. That is to say, fixed costs remain constant for a given period despite. Fixed costs are expenses that do not change with increases or decreases in production or sales volumes. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm. To calculate fixed costs, identify all expenses that remain constant regardless of production levels. Sum these costs, including rent, salaries, and insurance. Fixed cost is a cost that remains fixed regardless of the quantity produced, i.e., whether the company increases or decreases the production of the product the cost of the product will remain.

The Difference Between Fixed Cost And Variable Cost E vrogue.co

Fixed Cost Kahulugan To calculate fixed costs, identify all expenses that remain constant regardless of production levels. Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm. To calculate fixed costs, identify all expenses that remain constant regardless of production levels. Sum these costs, including rent, salaries, and insurance. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed costs are expenses that do not change with increases or decreases in production or sales volumes. That is to say, fixed costs remain constant for a given period despite. Fixed cost is a cost that remains fixed regardless of the quantity produced, i.e., whether the company increases or decreases the production of the product the cost of the product will remain.

From www.hoonthai.co

Fixed Cost คืออะไร รู้ครบเรื่องต้นทุนคงที่ HoonThai.co Fixed Cost Kahulugan Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed costs are a type of expense or cost that remains unchanged with an. Fixed Cost Kahulugan.

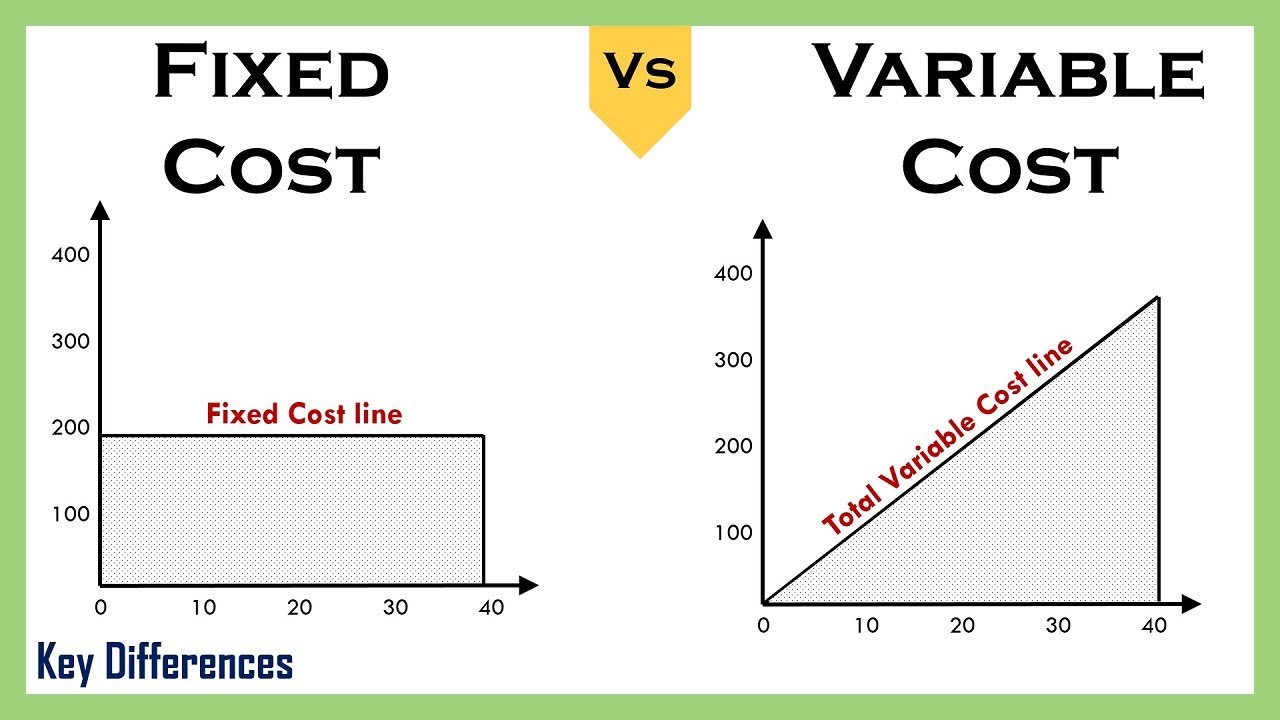

From www.jurnal.id

Mengenal Perbedaan Antara Fixed Cost dan Variable Cost dalam Bisnis Fixed Cost Kahulugan To calculate fixed costs, identify all expenses that remain constant regardless of production levels. That is to say, fixed costs remain constant for a given period despite. Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm. Sum these costs, including rent,. Fixed Cost Kahulugan.

From mungfali.com

Average Fixed Cost Graph Fixed Cost Kahulugan That is to say, fixed costs remain constant for a given period despite. Fixed cost is a cost that remains fixed regardless of the quantity produced, i.e., whether the company increases or decreases the production of the product the cost of the product will remain. Fixed cost is referred to as the cost that does not register a change with. Fixed Cost Kahulugan.

From www.educba.com

Fixed Cost Vs Variable Cost Top 12 Key Differences & Examples Fixed Cost Kahulugan Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm. Fixed costs are expenses that do not. Fixed Cost Kahulugan.

From exotikyfa.blob.core.windows.net

What Are The Example Of Fixed Cost at Paul Hickman blog Fixed Cost Kahulugan Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm. Sum these costs, including rent, salaries, and insurance. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services. Fixed Cost Kahulugan.

From www.vrogue.co

The Difference Between Fixed Cost And Variable Cost E vrogue.co Fixed Cost Kahulugan Sum these costs, including rent, salaries, and insurance. Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm. Fixed cost is a cost that remains fixed regardless of the quantity produced, i.e., whether the company increases or decreases the production of the. Fixed Cost Kahulugan.

From www.superfastcpa.com

What is a Fixed Cost? Fixed Cost Kahulugan That is to say, fixed costs remain constant for a given period despite. To calculate fixed costs, identify all expenses that remain constant regardless of production levels. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed cost is a cost that remains fixed regardless of the quantity produced, i.e., whether. Fixed Cost Kahulugan.

From www.vrogue.co

The Difference Between Fixed Cost And Variable Cost E vrogue.co Fixed Cost Kahulugan Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Sum these costs, including rent, salaries, and insurance. Fixed costs are a type of. Fixed Cost Kahulugan.

From sendpulse.ng

What is an Average Fixed Cost Basics Definition SendPulse Fixed Cost Kahulugan Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm. Fixed costs are expenses that do not change with increases or decreases in production. Fixed Cost Kahulugan.

From www.difference.wiki

Fixed Cost vs. Sunk Cost What’s the Difference? Fixed Cost Kahulugan To calculate fixed costs, identify all expenses that remain constant regardless of production levels. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs are expenses that do not change with increases or decreases in production or sales volumes. Fixed cost is referred. Fixed Cost Kahulugan.

From www.marketing91.com

Average Fixed Cost Definition, Formula and Examples Marketing91 Fixed Cost Kahulugan Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm. Fixed costs are a type of expense or cost that remains unchanged with an. Fixed Cost Kahulugan.

From exotikyfa.blob.core.windows.net

What Are The Example Of Fixed Cost at Paul Hickman blog Fixed Cost Kahulugan That is to say, fixed costs remain constant for a given period despite. Fixed costs are expenses that do not change with increases or decreases in production or sales volumes. Sum these costs, including rent, salaries, and insurance. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed cost is a. Fixed Cost Kahulugan.

From klikpajak.id

Fixed Cost Pengertian, Jenis, dan Contohnya Klikpajak Fixed Cost Kahulugan Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed cost is a cost that remains fixed regardless of the quantity produced, i.e.,. Fixed Cost Kahulugan.

From blog.hubspot.com

Fixed Cost What It Is & How to Calculate It Fixed Cost Kahulugan Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. To calculate fixed costs, identify all expenses. Fixed Cost Kahulugan.

From haipernews.com

How To Calculate Fixed Cost From Total Cost Haiper Fixed Cost Kahulugan Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. To calculate fixed costs, identify all expenses that remain constant regardless of production levels. Fixed costs are expenses that do not change with increases or decreases in production or sales volumes. Sum these costs, including. Fixed Cost Kahulugan.

From www.educba.com

Fixed Cost Formula Calculator (Examples with Excel Template) Fixed Cost Kahulugan Fixed costs are expenses that do not change with increases or decreases in production or sales volumes. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. That is to say, fixed costs remain constant for a given period despite. Fixed cost is a cost that remains fixed regardless of the quantity. Fixed Cost Kahulugan.

From ar.inspiredpencil.com

Fixed Cost Fixed Cost Kahulugan Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Sum these costs, including rent, salaries, and insurance. Fixed costs are expenses that do not change with increases or decreases in production or sales volumes. Fixed cost is a cost that remains fixed regardless of. Fixed Cost Kahulugan.

From www.teknatekno.com

Pengertian Biaya Tetap (Fixed Cost) Dan Contohnya Fixed Cost Kahulugan Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. That is to say, fixed costs remain constant for a given period despite. Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity. Fixed Cost Kahulugan.

From blog.hubspot.com

Fixed Cost What It Is & How to Calculate It Fixed Cost Kahulugan Fixed cost is a cost that remains fixed regardless of the quantity produced, i.e., whether the company increases or decreases the production of the product the cost of the product will remain. That is to say, fixed costs remain constant for a given period despite. To calculate fixed costs, identify all expenses that remain constant regardless of production levels. Fixed. Fixed Cost Kahulugan.

From artikel.rumah123.com

Mengenal Apa Itu Fixed Cost. Ini Contohnya dalam Sektor Properti! Fixed Cost Kahulugan Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed costs are expenses that do not change with increases or decreases in production or sales volumes. Sum these costs, including rent, salaries, and insurance. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease. Fixed Cost Kahulugan.

From www.zippia.com

How To Calculate Fixed Cost (With Examples) Zippia Fixed Cost Kahulugan That is to say, fixed costs remain constant for a given period despite. Fixed costs are expenses that do not change with increases or decreases in production or sales volumes. To calculate fixed costs, identify all expenses that remain constant regardless of production levels. Fixed cost is referred to as the cost that does not register a change with an. Fixed Cost Kahulugan.

From www.intelligenteconomist.com

Theory Of Production Cost Theory Intelligent Economist Fixed Cost Kahulugan To calculate fixed costs, identify all expenses that remain constant regardless of production levels. Sum these costs, including rent, salaries, and insurance. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed cost is a cost that remains fixed regardless of the quantity produced, i.e., whether the company increases or decreases. Fixed Cost Kahulugan.

From www.marketeers.com

Fixed Cost Pengertian, Contoh dan Pengelolaan dalam Bisnis Fixed Cost Kahulugan Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed cost is a cost that remains fixed regardless of the quantity produced, i.e., whether the company increases or decreases the production of the product the cost of the product will remain. To calculate fixed costs, identify all expenses that remain constant. Fixed Cost Kahulugan.

From www.opaper.app

Fixed Cost dan Variable Cost Perbedaan, Pengertian, dan Contohnya Fixed Cost Kahulugan Fixed cost is a cost that remains fixed regardless of the quantity produced, i.e., whether the company increases or decreases the production of the product the cost of the product will remain. Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm.. Fixed Cost Kahulugan.

From www.investopedia.com

Fixed Cost What It Is and How It’s Used in Business Fixed Cost Kahulugan Fixed cost is a cost that remains fixed regardless of the quantity produced, i.e., whether the company increases or decreases the production of the product the cost of the product will remain. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Sum these costs,. Fixed Cost Kahulugan.

From www.spcdn.org

What is an Average Fixed Cost Basics Meaning SendPulse Fixed Cost Kahulugan Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. That is to say, fixed costs remain constant for a given period despite. Sum these costs, including rent, salaries, and insurance. Fixed costs are expenses that do not change with increases or decreases in production. Fixed Cost Kahulugan.

From www.1099cafe.com

What is a Fixed Cost Variable vs Fixed Expenses — 1099 Cafe Fixed Cost Kahulugan To calculate fixed costs, identify all expenses that remain constant regardless of production levels. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed cost is a cost that remains fixed regardless of the quantity produced, i.e., whether the company increases or decreases the. Fixed Cost Kahulugan.

From agiled.app

Differences Between Fixed Cost and Variable Cost Fixed Cost Kahulugan Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed cost is a cost that remains fixed regardless of the quantity produced, i.e., whether the company increases or decreases the production of the product the cost of the product will remain. Fixed costs are a type of expense or cost that. Fixed Cost Kahulugan.

From www.vrogue.co

How To Calculate Fixed Cost And Variable Cost vrogue.co Fixed Cost Kahulugan To calculate fixed costs, identify all expenses that remain constant regardless of production levels. Fixed costs are expenses that do not change with increases or decreases in production or sales volumes. Sum these costs, including rent, salaries, and insurance. That is to say, fixed costs remain constant for a given period despite. Fixed costs (or constant costs) are costs that. Fixed Cost Kahulugan.

From efinancemanagement.com

Fixed Cost What It Is And What's Its Importance? Fixed Cost Kahulugan Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. Fixed costs are expenses that do not change with increases or decreases in production or sales volumes. That is to say, fixed costs remain constant for a given period despite. Sum these costs, including rent, salaries, and insurance. Fixed costs are a. Fixed Cost Kahulugan.

From hxeyjbcem.blob.core.windows.net

Explain Fixed Cost And Variable Cost With The Help Of Diagram at Susan Fixed Cost Kahulugan Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Sum these costs, including rent, salaries, and insurance. Fixed cost is a cost that remains fixed regardless of the quantity produced, i.e., whether the company increases or decreases the production of the product the cost. Fixed Cost Kahulugan.

From www.youtube.com

How to Calculate Fixed Cost Per Unit Easy Way YouTube Fixed Cost Kahulugan That is to say, fixed costs remain constant for a given period despite. Fixed cost is a cost that remains fixed regardless of the quantity produced, i.e., whether the company increases or decreases the production of the product the cost of the product will remain. To calculate fixed costs, identify all expenses that remain constant regardless of production levels. Fixed. Fixed Cost Kahulugan.

From avada.io

How to Calculate Fixed Cost? Formula, Guide and Examples Fixed Cost Kahulugan Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm. Fixed costs (or constant costs) are costs that are not affected by an increase or decrease in production. To calculate fixed costs, identify all expenses that remain constant regardless of production levels.. Fixed Cost Kahulugan.

From definitionjull.blogspot.com

Fixed Cost Definition Economics definitionjull Fixed Cost Kahulugan Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs are expenses that do not change with increases or decreases in production or sales volumes. Sum these costs, including rent, salaries, and insurance. That is to say, fixed costs remain constant for a. Fixed Cost Kahulugan.

From www.educba.com

Average Fixed Cost Formula Step by Step Solutions (Calculator) Fixed Cost Kahulugan Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs (or constant costs) are costs. Fixed Cost Kahulugan.