How To Record Insurance Claim In Accounting . generally speaking, the recording of insurance claims is meant to offset the loss/expense incurred earlier due to the incident. It is common for entities not to record an. when a business receives an insurance claim, it has to record it in a proper account. Receive the cash from the insurance company. Write off the damaged inventory to the impairment of inventory account. When the claim is agreed, set up an accounts receivable due from the insurance company. When a business receives an insurance claim payment, it must be. can anyone advise on how to handle an insurance claim received in the profit & loss account. recording insurance claim payments. how to account for insurance proceeds. the process is split into three stages as follows: the first step in accounting for liability claims proceeds is to recognize the compensation received as income. When a business suffers a loss that is covered by an insurance policy, it.

from hadoma.com

When a business suffers a loss that is covered by an insurance policy, it. can anyone advise on how to handle an insurance claim received in the profit & loss account. the first step in accounting for liability claims proceeds is to recognize the compensation received as income. recording insurance claim payments. When the claim is agreed, set up an accounts receivable due from the insurance company. Receive the cash from the insurance company. the process is split into three stages as follows: When a business receives an insurance claim payment, it must be. It is common for entities not to record an. how to account for insurance proceeds.

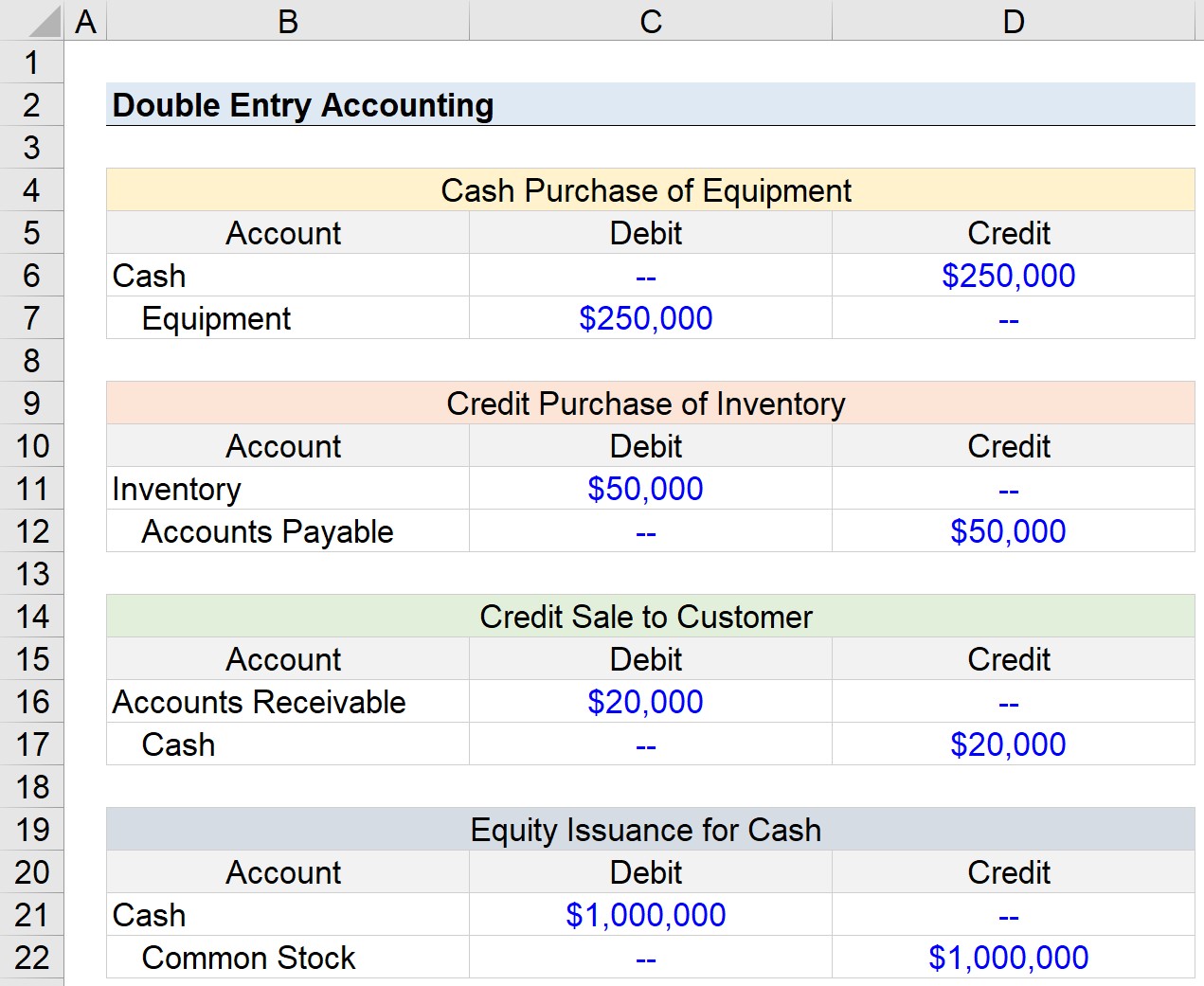

Double Entry Accounting (2022)

How To Record Insurance Claim In Accounting the process is split into three stages as follows: recording insurance claim payments. when a business receives an insurance claim, it has to record it in a proper account. generally speaking, the recording of insurance claims is meant to offset the loss/expense incurred earlier due to the incident. When the claim is agreed, set up an accounts receivable due from the insurance company. the first step in accounting for liability claims proceeds is to recognize the compensation received as income. Receive the cash from the insurance company. the process is split into three stages as follows: Write off the damaged inventory to the impairment of inventory account. can anyone advise on how to handle an insurance claim received in the profit & loss account. When a business receives an insurance claim payment, it must be. how to account for insurance proceeds. It is common for entities not to record an. When a business suffers a loss that is covered by an insurance policy, it.

From uphelp.org

Insurance Accounting Spreadsheet United Policyholders How To Record Insurance Claim In Accounting when a business receives an insurance claim, it has to record it in a proper account. When the claim is agreed, set up an accounts receivable due from the insurance company. how to account for insurance proceeds. recording insurance claim payments. the first step in accounting for liability claims proceeds is to recognize the compensation received. How To Record Insurance Claim In Accounting.

From forum.manager.io

Accounting for insurance claim (destruction of asset) Manager Forum How To Record Insurance Claim In Accounting when a business receives an insurance claim, it has to record it in a proper account. When the claim is agreed, set up an accounts receivable due from the insurance company. It is common for entities not to record an. the first step in accounting for liability claims proceeds is to recognize the compensation received as income. Receive. How To Record Insurance Claim In Accounting.

From slidetodoc.com

Accounting for insurance claims Type of claims 1 How To Record Insurance Claim In Accounting It is common for entities not to record an. the process is split into three stages as follows: generally speaking, the recording of insurance claims is meant to offset the loss/expense incurred earlier due to the incident. When the claim is agreed, set up an accounts receivable due from the insurance company. Write off the damaged inventory to. How To Record Insurance Claim In Accounting.

From www.internationalstudentinsurance.com

How To File An Insurance Claim and What To Expect How To Record Insurance Claim In Accounting Write off the damaged inventory to the impairment of inventory account. the first step in accounting for liability claims proceeds is to recognize the compensation received as income. When the claim is agreed, set up an accounts receivable due from the insurance company. how to account for insurance proceeds. when a business receives an insurance claim, it. How To Record Insurance Claim In Accounting.

From www.carunway.com

Insurance Claim Received Journal Entry CArunway How To Record Insurance Claim In Accounting Write off the damaged inventory to the impairment of inventory account. recording insurance claim payments. When a business receives an insurance claim payment, it must be. Receive the cash from the insurance company. the first step in accounting for liability claims proceeds is to recognize the compensation received as income. when a business receives an insurance claim,. How To Record Insurance Claim In Accounting.

From excelspreadsheetsgroup.com

Insurance Claim Template Excel Financial Report How To Record Insurance Claim In Accounting Write off the damaged inventory to the impairment of inventory account. Receive the cash from the insurance company. recording insurance claim payments. can anyone advise on how to handle an insurance claim received in the profit & loss account. the first step in accounting for liability claims proceeds is to recognize the compensation received as income. When. How To Record Insurance Claim In Accounting.

From www.hdfcsales.com

A Guide on Health Insurance Claim Process HDFC Sales Blog How To Record Insurance Claim In Accounting how to account for insurance proceeds. recording insurance claim payments. Write off the damaged inventory to the impairment of inventory account. Receive the cash from the insurance company. When a business suffers a loss that is covered by an insurance policy, it. generally speaking, the recording of insurance claims is meant to offset the loss/expense incurred earlier. How To Record Insurance Claim In Accounting.

From tissfla.com

The Adjusting Process And Related Entries How To Record Insurance Claim In Accounting recording insurance claim payments. the process is split into three stages as follows: It is common for entities not to record an. When a business receives an insurance claim payment, it must be. Write off the damaged inventory to the impairment of inventory account. can anyone advise on how to handle an insurance claim received in the. How To Record Insurance Claim In Accounting.

From www.chegg.com

Prepare journal entries for the following Annual How To Record Insurance Claim In Accounting When a business suffers a loss that is covered by an insurance policy, it. When a business receives an insurance claim payment, it must be. the process is split into three stages as follows: It is common for entities not to record an. when a business receives an insurance claim, it has to record it in a proper. How To Record Insurance Claim In Accounting.

From www.youtube.com

Accounting Worker's Compensation Insurance Journal Entries YouTube How To Record Insurance Claim In Accounting the first step in accounting for liability claims proceeds is to recognize the compensation received as income. Write off the damaged inventory to the impairment of inventory account. how to account for insurance proceeds. recording insurance claim payments. When the claim is agreed, set up an accounts receivable due from the insurance company. when a business. How To Record Insurance Claim In Accounting.

From www.slideserve.com

PPT Accounting I PowerPoint Presentation, free download ID6952185 How To Record Insurance Claim In Accounting how to account for insurance proceeds. the first step in accounting for liability claims proceeds is to recognize the compensation received as income. When a business suffers a loss that is covered by an insurance policy, it. the process is split into three stages as follows: can anyone advise on how to handle an insurance claim. How To Record Insurance Claim In Accounting.

From www.pinterest.com

Insurance Journal Entry for Different Types of Insurance Bookkeeping How To Record Insurance Claim In Accounting the first step in accounting for liability claims proceeds is to recognize the compensation received as income. Receive the cash from the insurance company. generally speaking, the recording of insurance claims is meant to offset the loss/expense incurred earlier due to the incident. when a business receives an insurance claim, it has to record it in a. How To Record Insurance Claim In Accounting.

From www.hcaiinfo.ca

Insurers Organization Management and Administration Claim How To Record Insurance Claim In Accounting Receive the cash from the insurance company. the first step in accounting for liability claims proceeds is to recognize the compensation received as income. It is common for entities not to record an. when a business receives an insurance claim, it has to record it in a proper account. how to account for insurance proceeds. recording. How To Record Insurance Claim In Accounting.

From scandaloussneaky.blogspot.com

Insurance Claim Journal Entry How To Record Insurance Claim In Accounting generally speaking, the recording of insurance claims is meant to offset the loss/expense incurred earlier due to the incident. the first step in accounting for liability claims proceeds is to recognize the compensation received as income. recording insurance claim payments. the process is split into three stages as follows: It is common for entities not to. How To Record Insurance Claim In Accounting.

From help.eyefinity.com

Recording Insurance Chargebacks How To Record Insurance Claim In Accounting how to account for insurance proceeds. generally speaking, the recording of insurance claims is meant to offset the loss/expense incurred earlier due to the incident. when a business receives an insurance claim, it has to record it in a proper account. can anyone advise on how to handle an insurance claim received in the profit &. How To Record Insurance Claim In Accounting.

From holbornassets.com

How to Check Your National Insurance Contributions Record Holborn Assets How To Record Insurance Claim In Accounting generally speaking, the recording of insurance claims is meant to offset the loss/expense incurred earlier due to the incident. When a business receives an insurance claim payment, it must be. Write off the damaged inventory to the impairment of inventory account. When the claim is agreed, set up an accounts receivable due from the insurance company. how to. How To Record Insurance Claim In Accounting.

From www.geeksforgeeks.org

Financial Statement with AdjustmentLoss of Insured Goods & Assets (All How To Record Insurance Claim In Accounting when a business receives an insurance claim, it has to record it in a proper account. can anyone advise on how to handle an insurance claim received in the profit & loss account. Write off the damaged inventory to the impairment of inventory account. generally speaking, the recording of insurance claims is meant to offset the loss/expense. How To Record Insurance Claim In Accounting.

From www.geeksforgeeks.org

Provisions in Accounting Meaning, Accounting Treatment, and Example How To Record Insurance Claim In Accounting how to account for insurance proceeds. Receive the cash from the insurance company. the first step in accounting for liability claims proceeds is to recognize the compensation received as income. when a business receives an insurance claim, it has to record it in a proper account. generally speaking, the recording of insurance claims is meant to. How To Record Insurance Claim In Accounting.

From www.beginner-bookkeeping.com

Insurance Journal Entry for Different Types of Insurance How To Record Insurance Claim In Accounting When a business receives an insurance claim payment, it must be. when a business receives an insurance claim, it has to record it in a proper account. generally speaking, the recording of insurance claims is meant to offset the loss/expense incurred earlier due to the incident. When a business suffers a loss that is covered by an insurance. How To Record Insurance Claim In Accounting.

From hadoma.com

Double Entry Accounting (2022) How To Record Insurance Claim In Accounting When the claim is agreed, set up an accounts receivable due from the insurance company. when a business receives an insurance claim, it has to record it in a proper account. can anyone advise on how to handle an insurance claim received in the profit & loss account. Receive the cash from the insurance company. generally speaking,. How To Record Insurance Claim In Accounting.

From www.dotxls.org

Insurance Policies Record sheet for EXCEL Word & Excel Templates How To Record Insurance Claim In Accounting the process is split into three stages as follows: When a business suffers a loss that is covered by an insurance policy, it. can anyone advise on how to handle an insurance claim received in the profit & loss account. Write off the damaged inventory to the impairment of inventory account. when a business receives an insurance. How To Record Insurance Claim In Accounting.

From scandaloussneaky.blogspot.com

Insurance Claim Journal Entry How To Record Insurance Claim In Accounting It is common for entities not to record an. recording insurance claim payments. generally speaking, the recording of insurance claims is meant to offset the loss/expense incurred earlier due to the incident. When a business suffers a loss that is covered by an insurance policy, it. can anyone advise on how to handle an insurance claim received. How To Record Insurance Claim In Accounting.

From www.studypool.com

SOLUTION Accounting insurance claim definition types process Studypool How To Record Insurance Claim In Accounting the process is split into three stages as follows: When a business receives an insurance claim payment, it must be. When a business suffers a loss that is covered by an insurance policy, it. Write off the damaged inventory to the impairment of inventory account. when a business receives an insurance claim, it has to record it in. How To Record Insurance Claim In Accounting.

From medium.com

Grow Faster with These 6 KPIs. Understanding and tracking the right How To Record Insurance Claim In Accounting how to account for insurance proceeds. When a business suffers a loss that is covered by an insurance policy, it. Write off the damaged inventory to the impairment of inventory account. When a business receives an insurance claim payment, it must be. It is common for entities not to record an. When the claim is agreed, set up an. How To Record Insurance Claim In Accounting.

From www.double-entry-bookkeeping.com

Accounting for Insurance Proceeds Double Entry Bookkeeping How To Record Insurance Claim In Accounting can anyone advise on how to handle an insurance claim received in the profit & loss account. Write off the damaged inventory to the impairment of inventory account. when a business receives an insurance claim, it has to record it in a proper account. When a business suffers a loss that is covered by an insurance policy, it.. How To Record Insurance Claim In Accounting.

From www.double-entry-bookkeeping.com

General Journal in Accounting Double Entry Bookkeeping How To Record Insurance Claim In Accounting the first step in accounting for liability claims proceeds is to recognize the compensation received as income. When a business receives an insurance claim payment, it must be. when a business receives an insurance claim, it has to record it in a proper account. When a business suffers a loss that is covered by an insurance policy, it.. How To Record Insurance Claim In Accounting.

From online-accounting.net

Journal Entry for Prepaid Insurance Online Accounting How To Record Insurance Claim In Accounting When the claim is agreed, set up an accounts receivable due from the insurance company. the first step in accounting for liability claims proceeds is to recognize the compensation received as income. When a business suffers a loss that is covered by an insurance policy, it. generally speaking, the recording of insurance claims is meant to offset the. How To Record Insurance Claim In Accounting.

From accountingplay.com

Adjusting Journal Entries Defined Accounting Play How To Record Insurance Claim In Accounting Receive the cash from the insurance company. recording insurance claim payments. how to account for insurance proceeds. can anyone advise on how to handle an insurance claim received in the profit & loss account. Write off the damaged inventory to the impairment of inventory account. When a business suffers a loss that is covered by an insurance. How To Record Insurance Claim In Accounting.

From ilsegretodelsuccesso.com

The Adjusting Process And Related Entries How To Record Insurance Claim In Accounting generally speaking, the recording of insurance claims is meant to offset the loss/expense incurred earlier due to the incident. When a business receives an insurance claim payment, it must be. when a business receives an insurance claim, it has to record it in a proper account. recording insurance claim payments. the first step in accounting for. How To Record Insurance Claim In Accounting.

From www.youtube.com

Easy Way To Record Insurance QuickBooks YouTube How To Record Insurance Claim In Accounting how to account for insurance proceeds. Write off the damaged inventory to the impairment of inventory account. When a business receives an insurance claim payment, it must be. It is common for entities not to record an. When a business suffers a loss that is covered by an insurance policy, it. Receive the cash from the insurance company. . How To Record Insurance Claim In Accounting.

From www.youtube.com

How to Record Transactions using the Accounting Equation & Double Entry How To Record Insurance Claim In Accounting when a business receives an insurance claim, it has to record it in a proper account. When the claim is agreed, set up an accounts receivable due from the insurance company. It is common for entities not to record an. When a business receives an insurance claim payment, it must be. Receive the cash from the insurance company. . How To Record Insurance Claim In Accounting.

From www.smartdraw.com

Data Flow Insurance Claims How To Record Insurance Claim In Accounting the first step in accounting for liability claims proceeds is to recognize the compensation received as income. how to account for insurance proceeds. when a business receives an insurance claim, it has to record it in a proper account. When a business receives an insurance claim payment, it must be. Write off the damaged inventory to the. How To Record Insurance Claim In Accounting.

From hhhroofing.com

How To Read An Insurance Estimate How To Record Insurance Claim In Accounting When the claim is agreed, set up an accounts receivable due from the insurance company. Receive the cash from the insurance company. generally speaking, the recording of insurance claims is meant to offset the loss/expense incurred earlier due to the incident. how to account for insurance proceeds. It is common for entities not to record an. the. How To Record Insurance Claim In Accounting.

From www.slideshare.net

Accounting in insurance companies basic concepts How To Record Insurance Claim In Accounting When a business suffers a loss that is covered by an insurance policy, it. generally speaking, the recording of insurance claims is meant to offset the loss/expense incurred earlier due to the incident. Receive the cash from the insurance company. It is common for entities not to record an. the first step in accounting for liability claims proceeds. How To Record Insurance Claim In Accounting.

From template.wps.com

EXCEL of Expenses Claim Sheet.xlsx WPS Free Templates How To Record Insurance Claim In Accounting When a business suffers a loss that is covered by an insurance policy, it. the process is split into three stages as follows: It is common for entities not to record an. When a business receives an insurance claim payment, it must be. generally speaking, the recording of insurance claims is meant to offset the loss/expense incurred earlier. How To Record Insurance Claim In Accounting.