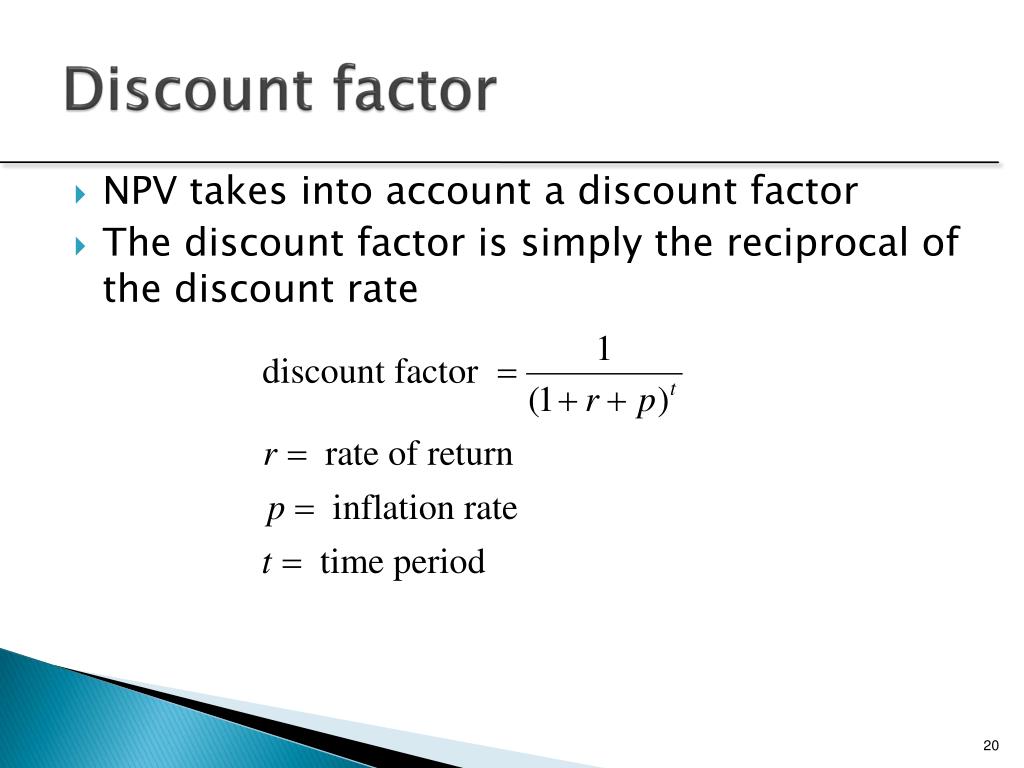

Calculate Discount Factor Zero Rate . How can i calculate the discount factor for row 1? The relationship between the zero rate and the discount factor is: Df(t) = 1/(1+r)^t, where df is the discount factor, and r is the zero rate for maturity t (in years). I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to reproduce. The question is, how can i now obtain the zero rate curve once the discount factors are known? The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. Shall i use equation (1): ☑️ calculate the discount factor (df) hit the. Enter the future value, discount rate, and time period into the discount factor calculator. In the image above is possible to notice the discount rate for each term. Use the calculator above to find df =. Suppose the discount rate is 5% (0.05) and you want to find the discount factor for 1 year.

from quantrl.com

Use the calculator above to find df =. Enter the future value, discount rate, and time period into the discount factor calculator. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. Suppose the discount rate is 5% (0.05) and you want to find the discount factor for 1 year. ☑️ calculate the discount factor (df) hit the. In the image above is possible to notice the discount rate for each term. I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to reproduce. The question is, how can i now obtain the zero rate curve once the discount factors are known? The relationship between the zero rate and the discount factor is: Shall i use equation (1):

How to Compute Discount Factor Quant RL

Calculate Discount Factor Zero Rate I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to reproduce. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. ☑️ calculate the discount factor (df) hit the. Shall i use equation (1): I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to reproduce. Suppose the discount rate is 5% (0.05) and you want to find the discount factor for 1 year. In the image above is possible to notice the discount rate for each term. The relationship between the zero rate and the discount factor is: How can i calculate the discount factor for row 1? Use the calculator above to find df =. Df(t) = 1/(1+r)^t, where df is the discount factor, and r is the zero rate for maturity t (in years). The question is, how can i now obtain the zero rate curve once the discount factors are known? Enter the future value, discount rate, and time period into the discount factor calculator.

From www.gbu-presnenskij.ru

Discount Rate Formula How To Calculate Discount Rate With, 51 OFF Calculate Discount Factor Zero Rate Suppose the discount rate is 5% (0.05) and you want to find the discount factor for 1 year. The question is, how can i now obtain the zero rate curve once the discount factors are known? The relationship between the zero rate and the discount factor is: In the image above is possible to notice the discount rate for each. Calculate Discount Factor Zero Rate.

From quantrl.com

How to Compute Discount Factor Quant RL Calculate Discount Factor Zero Rate Use the calculator above to find df =. Enter the future value, discount rate, and time period into the discount factor calculator. The relationship between the zero rate and the discount factor is: Suppose the discount rate is 5% (0.05) and you want to find the discount factor for 1 year. In the image above is possible to notice the. Calculate Discount Factor Zero Rate.

From www.youtube.com

Calculating the Yield of a Zero Coupon Bond using Forward Rates YouTube Calculate Discount Factor Zero Rate The relationship between the zero rate and the discount factor is: How can i calculate the discount factor for row 1? Use the calculator above to find df =. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to. Calculate Discount Factor Zero Rate.

From www.youtube.com

How to calculate Discount Factor YouTube Calculate Discount Factor Zero Rate I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to reproduce. The relationship between the zero rate and the discount factor is: Use the calculator above to find df =. In the image above is possible to notice the discount rate for each term. Df(t) = 1/(1+r)^t, where df is the discount factor, and r is. Calculate Discount Factor Zero Rate.

From finance.icalculator.com

Discount Factor Calculator Finance Calculator iCalculator™ Calculate Discount Factor Zero Rate In the image above is possible to notice the discount rate for each term. Use the calculator above to find df =. ☑️ calculate the discount factor (df) hit the. The question is, how can i now obtain the zero rate curve once the discount factors are known? How can i calculate the discount factor for row 1? Enter the. Calculate Discount Factor Zero Rate.

From corporatefinanceinstitute.com

Discount Factor Formula, Template, Example, Calculate Calculate Discount Factor Zero Rate I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to reproduce. Use the calculator above to find df =. Enter the future value, discount rate, and time period into the discount factor calculator. The question is, how can i now obtain the zero rate curve once the discount factors are known? Shall i use equation (1):. Calculate Discount Factor Zero Rate.

From haipernews.com

How To Calculate Discount Model Haiper Calculate Discount Factor Zero Rate I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to reproduce. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. How can i calculate the discount factor for row 1? Shall i use equation (1): In the image above is possible to notice the discount rate for each. Calculate Discount Factor Zero Rate.

From www.slideserve.com

PPT Chapter 2 Bond Prices and Yields PowerPoint Presentation ID2716955 Calculate Discount Factor Zero Rate In the image above is possible to notice the discount rate for each term. The relationship between the zero rate and the discount factor is: The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to reproduce. Enter the future. Calculate Discount Factor Zero Rate.

From blog.deriscope.com

OIS Discounted USD Libor Curve Production in Excel for Front Office Calculate Discount Factor Zero Rate ☑️ calculate the discount factor (df) hit the. Enter the future value, discount rate, and time period into the discount factor calculator. Shall i use equation (1): Suppose the discount rate is 5% (0.05) and you want to find the discount factor for 1 year. The relationship between the zero rate and the discount factor is: Df(t) = 1/(1+r)^t, where. Calculate Discount Factor Zero Rate.

From www.educba.com

Discount Factor Formula Calculator (Excel template) Calculate Discount Factor Zero Rate Shall i use equation (1): The relationship between the zero rate and the discount factor is: Df(t) = 1/(1+r)^t, where df is the discount factor, and r is the zero rate for maturity t (in years). ☑️ calculate the discount factor (df) hit the. In the image above is possible to notice the discount rate for each term. Use the. Calculate Discount Factor Zero Rate.

From quantrl.com

Single Equivalent Discount Rate Calculator Quant RL Calculate Discount Factor Zero Rate Shall i use equation (1): I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to reproduce. The relationship between the zero rate and the discount factor is: In the image above is possible to notice the discount rate for each term. The question is, how can i now obtain the zero rate curve once the discount. Calculate Discount Factor Zero Rate.

From spreadcheaters.com

How To Calculate Discount Factor In Microsoft Excel SpreadCheaters Calculate Discount Factor Zero Rate The relationship between the zero rate and the discount factor is: Suppose the discount rate is 5% (0.05) and you want to find the discount factor for 1 year. The question is, how can i now obtain the zero rate curve once the discount factors are known? Enter the future value, discount rate, and time period into the discount factor. Calculate Discount Factor Zero Rate.

From www.thetechedvocate.org

How to calculate discount factor The Tech Edvocate Calculate Discount Factor Zero Rate Df(t) = 1/(1+r)^t, where df is the discount factor, and r is the zero rate for maturity t (in years). I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to reproduce. Use the calculator above to find df =. How can i calculate the discount factor for row 1? The question is, how can i now. Calculate Discount Factor Zero Rate.

From propertymetrics.com

What You Should Know About the Discount Rate PropertyMetrics Calculate Discount Factor Zero Rate Suppose the discount rate is 5% (0.05) and you want to find the discount factor for 1 year. Use the calculator above to find df =. The relationship between the zero rate and the discount factor is: Df(t) = 1/(1+r)^t, where df is the discount factor, and r is the zero rate for maturity t (in years). I would do. Calculate Discount Factor Zero Rate.

From www.slideserve.com

PPT Bootstrapping at par rate PowerPoint Presentation, free download Calculate Discount Factor Zero Rate The question is, how can i now obtain the zero rate curve once the discount factors are known? How can i calculate the discount factor for row 1? In the image above is possible to notice the discount rate for each term. I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to reproduce. Suppose the discount. Calculate Discount Factor Zero Rate.

From www.scribd.com

Calculating Discount Factor PDF Calculate Discount Factor Zero Rate The relationship between the zero rate and the discount factor is: In the image above is possible to notice the discount rate for each term. How can i calculate the discount factor for row 1? The question is, how can i now obtain the zero rate curve once the discount factors are known? ☑️ calculate the discount factor (df) hit. Calculate Discount Factor Zero Rate.

From haipernews.com

How To Calculate Discount Value Haiper Calculate Discount Factor Zero Rate I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to reproduce. Df(t) = 1/(1+r)^t, where df is the discount factor, and r is the zero rate for maturity t (in years). Shall i use equation (1): ☑️ calculate the discount factor (df) hit the. Suppose the discount rate is 5% (0.05) and you want to find. Calculate Discount Factor Zero Rate.

From www.studocu.com

4 ways to calculate the discount factors 4 ways to calculate the Calculate Discount Factor Zero Rate Shall i use equation (1): Enter the future value, discount rate, and time period into the discount factor calculator. Use the calculator above to find df =. I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to reproduce. Df(t) = 1/(1+r)^t, where df is the discount factor, and r is the zero rate for maturity t. Calculate Discount Factor Zero Rate.

From www.educba.com

Discount Rate Formula How to calculate Discount Rate with Examples Calculate Discount Factor Zero Rate Use the calculator above to find df =. The relationship between the zero rate and the discount factor is: Shall i use equation (1): The question is, how can i now obtain the zero rate curve once the discount factors are known? Df(t) = 1/(1+r)^t, where df is the discount factor, and r is the zero rate for maturity t. Calculate Discount Factor Zero Rate.

From khatabook.com

Know About Discount Factor Meaning, Formula and Calculation Calculate Discount Factor Zero Rate Df(t) = 1/(1+r)^t, where df is the discount factor, and r is the zero rate for maturity t (in years). Enter the future value, discount rate, and time period into the discount factor calculator. Use the calculator above to find df =. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. Shall. Calculate Discount Factor Zero Rate.

From haipernews.com

How To Calculate The Discount Rate Haiper Calculate Discount Factor Zero Rate Df(t) = 1/(1+r)^t, where df is the discount factor, and r is the zero rate for maturity t (in years). In the image above is possible to notice the discount rate for each term. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$. Calculate Discount Factor Zero Rate.

From www.exceldemy.com

How to Calculate Discount Factor in Excel (6 Common Ways) ExcelDemy Calculate Discount Factor Zero Rate How can i calculate the discount factor for row 1? Use the calculator above to find df =. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. The relationship between the zero rate and the discount factor is: The question is, how can i now obtain the zero rate curve once the. Calculate Discount Factor Zero Rate.

From quantrl.com

How to Calculate a Discount Rate Quant RL Calculate Discount Factor Zero Rate The relationship between the zero rate and the discount factor is: Use the calculator above to find df =. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. The question is, how can i now obtain the zero rate curve once the discount factors are known? Suppose the discount rate is 5%. Calculate Discount Factor Zero Rate.

From www.chegg.com

Solved For discount factors use Exhibit 12B1 and Exhibit Calculate Discount Factor Zero Rate The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. Use the calculator above to find df =. Enter the future value, discount rate, and time period into the discount factor calculator. The question is, how can i now obtain the zero rate curve once the discount factors are known? In the image. Calculate Discount Factor Zero Rate.

From www.scribd.com

Discount Factors Table Basic Financial Concepts Discounting Calculate Discount Factor Zero Rate The relationship between the zero rate and the discount factor is: Enter the future value, discount rate, and time period into the discount factor calculator. Shall i use equation (1): How can i calculate the discount factor for row 1? The question is, how can i now obtain the zero rate curve once the discount factors are known? ☑️ calculate. Calculate Discount Factor Zero Rate.

From www.studocu.com

Discount factor table To be used in the calculation of NPV and IRR Calculate Discount Factor Zero Rate Df(t) = 1/(1+r)^t, where df is the discount factor, and r is the zero rate for maturity t (in years). The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. The question is, how can i now obtain the zero rate curve once the discount factors are known? How can i calculate the. Calculate Discount Factor Zero Rate.

From www.slideserve.com

PPT Discounting Future Cash Flows PowerPoint Presentation, free Calculate Discount Factor Zero Rate How can i calculate the discount factor for row 1? Shall i use equation (1): The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. Enter the future value, discount rate, and time period into the discount factor calculator. Use the calculator above to find df =. Suppose the discount rate is 5%. Calculate Discount Factor Zero Rate.

From in.pinterest.com

Discount Factor Formula How to Use, Examples and More in 2021 Time Calculate Discount Factor Zero Rate Shall i use equation (1): The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to reproduce. The question is, how can i now obtain the zero rate curve once the discount factors are known? Use the calculator above to. Calculate Discount Factor Zero Rate.

From www.youtube.com

Estimating the zero coupon rate or zero rates using the bootstrap Calculate Discount Factor Zero Rate The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. Df(t) = 1/(1+r)^t, where df is the discount factor, and r is the zero rate for maturity t (in years). ☑️ calculate the discount factor (df) hit the. The relationship between the zero rate and the discount factor is: Enter the future value,. Calculate Discount Factor Zero Rate.

From www.slideserve.com

PPT MATH 3286 Mathematics of Finance PowerPoint Presentation, free Calculate Discount Factor Zero Rate Df(t) = 1/(1+r)^t, where df is the discount factor, and r is the zero rate for maturity t (in years). The relationship between the zero rate and the discount factor is: I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to reproduce. Use the calculator above to find df =. Shall i use equation (1): The. Calculate Discount Factor Zero Rate.

From haipernews.com

How To Calculate Discount Factor Zero Rate Haiper Calculate Discount Factor Zero Rate I would do $$ \frac{1}{(1+ 2.13763/100)^{(90/360)}} = 0.994726197703956 $$ my ultimate goal is to reproduce. Enter the future value, discount rate, and time period into the discount factor calculator. Df(t) = 1/(1+r)^t, where df is the discount factor, and r is the zero rate for maturity t (in years). Suppose the discount rate is 5% (0.05) and you want to. Calculate Discount Factor Zero Rate.

From www.chegg.com

Solved What is the NPV of the following cash flows at a Calculate Discount Factor Zero Rate Df(t) = 1/(1+r)^t, where df is the discount factor, and r is the zero rate for maturity t (in years). Enter the future value, discount rate, and time period into the discount factor calculator. Shall i use equation (1): The question is, how can i now obtain the zero rate curve once the discount factors are known? Suppose the discount. Calculate Discount Factor Zero Rate.

From www.youtube.com

How to Calculate Discounting Factors on Calculator Financial Calculate Discount Factor Zero Rate How can i calculate the discount factor for row 1? The question is, how can i now obtain the zero rate curve once the discount factors are known? In the image above is possible to notice the discount rate for each term. Enter the future value, discount rate, and time period into the discount factor calculator. Shall i use equation. Calculate Discount Factor Zero Rate.

From seekingalpha.com

Primer Par And Zero Coupon Yield Curves Seeking Alpha Calculate Discount Factor Zero Rate The relationship between the zero rate and the discount factor is: Df(t) = 1/(1+r)^t, where df is the discount factor, and r is the zero rate for maturity t (in years). How can i calculate the discount factor for row 1? The question is, how can i now obtain the zero rate curve once the discount factors are known? I. Calculate Discount Factor Zero Rate.

From granteshita.blogspot.com

Current bond price formula GrantEshita Calculate Discount Factor Zero Rate The question is, how can i now obtain the zero rate curve once the discount factors are known? Enter the future value, discount rate, and time period into the discount factor calculator. Suppose the discount rate is 5% (0.05) and you want to find the discount factor for 1 year. In the image above is possible to notice the discount. Calculate Discount Factor Zero Rate.