Long Spread Duration . duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. the duration spread is a useful tool for predicting changes in interest rates. if an investor expects interest rates to fall during the course of the time the bond is held, a bond with a longer duration would be appealing because the bond’s value would increase more than comparable bonds with shorter durations. spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. A portfolio’s spread duration will equal the weighted. When the duration spread is positive, it. Duration can also be used.

from www.randomwalktrading.com

the duration spread is a useful tool for predicting changes in interest rates. When the duration spread is positive, it. duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. A portfolio’s spread duration will equal the weighted. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. Duration can also be used. if an investor expects interest rates to fall during the course of the time the bond is held, a bond with a longer duration would be appealing because the bond’s value would increase more than comparable bonds with shorter durations.

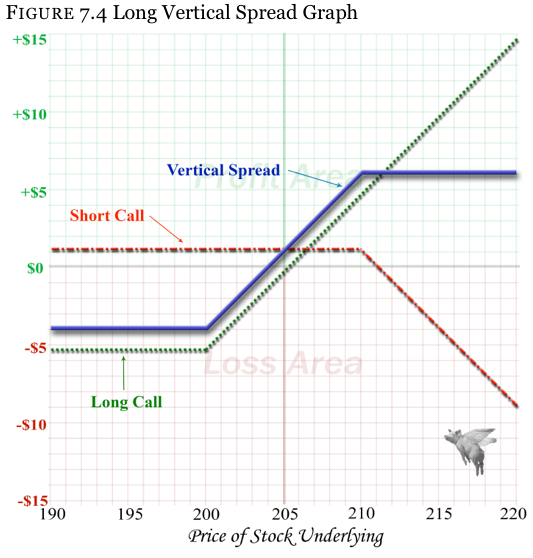

CH 7 Vertical Spread Random Walk Trading

Long Spread Duration Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. A portfolio’s spread duration will equal the weighted. duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. the duration spread is a useful tool for predicting changes in interest rates. if an investor expects interest rates to fall during the course of the time the bond is held, a bond with a longer duration would be appealing because the bond’s value would increase more than comparable bonds with shorter durations. Duration can also be used. When the duration spread is positive, it. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. spread duration will equal the percentage change in a security’s price when credit spreads change by 1%.

From www.myespresso.com

What Is Ratio Spread and Ratio Back Spread in Options Trading Long Spread Duration duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. the duration spread is a useful tool for predicting changes in interest rates. A portfolio’s spread duration will equal the weighted. When the duration spread is positive, it. Spread duration is a key metric that helps. Long Spread Duration.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation, free download ID Long Spread Duration When the duration spread is positive, it. duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. Duration can also be used. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. spread duration will. Long Spread Duration.

From www.columbiathreadneedleus.com

Chart Two types of steepening yield curves Columbia Threadneedle Blog Long Spread Duration duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. Duration can also be used. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. When the duration spread is positive, it. if an investor. Long Spread Duration.

From www.investopedia.com

Duration and Convexity to Measure Bond Risk Long Spread Duration When the duration spread is positive, it. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. spread duration will equal the percentage change in. Long Spread Duration.

From www.educba.com

Macaulay Duration Formula Example with Excel Template Long Spread Duration When the duration spread is positive, it. if an investor expects interest rates to fall during the course of the time the bond is held, a bond with a longer duration would be appealing because the bond’s value would increase more than comparable bonds with shorter durations. the duration spread is a useful tool for predicting changes in. Long Spread Duration.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation, free download ID Long Spread Duration spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. Duration can also be used. if an investor expects interest rates to fall during the course of the time the bond is held, a bond with a longer duration would be appealing because the bond’s value would increase more than comparable. Long Spread Duration.

From tabr.net

There's No "High" In High Yield Spreads TABR Long Spread Duration Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. Duration can also be used. spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. When the duration spread is positive, it. duration measures how long it takes, in years,. Long Spread Duration.

From spreadcharts.com

Groundbreaking change in the rates market Long Spread Duration duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. the duration spread is a useful tool for predicting changes in interest rates. if an investor expects. Long Spread Duration.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation, free download ID Long Spread Duration spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. if an investor expects interest rates to fall during the course of the time the bond is held, a bond. Long Spread Duration.

From www.researchgate.net

the spread durations of various proxy portfolios defined by four Long Spread Duration Duration can also be used. A portfolio’s spread duration will equal the weighted. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. duration measures how long it takes, in. Long Spread Duration.

From www.ejshin.org

Education Ultimate Fixed 101 What are Credit Spread, Spread Long Spread Duration Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. the duration spread is a useful tool for predicting changes in interest rates. Duration can also be used. duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its. Long Spread Duration.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation ID3950949 Long Spread Duration duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. When the duration spread is positive, it. if an investor expects interest rates to fall. Long Spread Duration.

From www.valuewalk.com

Why The Trade Weighted USD Index Major Currency and 10yr Spread are the Long Spread Duration duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. A portfolio’s spread duration will equal the weighted. When the duration spread is positive, it. Spread duration is a. Long Spread Duration.

From www.slideteam.net

Spread Duration Calculation In Powerpoint And Google Slides Cpb PPT Long Spread Duration Duration can also be used. if an investor expects interest rates to fall during the course of the time the bond is held, a bond with a longer duration would be appealing because the bond’s value would increase more than comparable bonds with shorter durations. duration measures how long it takes, in years, for an investor to be. Long Spread Duration.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation ID3950949 Long Spread Duration Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. A portfolio’s spread duration will equal the weighted. spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. if an investor expects interest rates to fall during the course of. Long Spread Duration.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation ID3950949 Long Spread Duration A portfolio’s spread duration will equal the weighted. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. if an investor expects interest rates to. Long Spread Duration.

From www.seeitmarket.com

Spread Trading Basics to Navigate Fed ZIRP Policy Long Spread Duration if an investor expects interest rates to fall during the course of the time the bond is held, a bond with a longer duration would be appealing because the bond’s value would increase more than comparable bonds with shorter durations. A portfolio’s spread duration will equal the weighted. spread duration will equal the percentage change in a security’s. Long Spread Duration.

From www.morningstar.co.uk

The US Treasury Yield Curve Recession Indicator is... Morningstar Long Spread Duration duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in. Long Spread Duration.

From www.randomwalktrading.com

CH 7 Vertical Spread Random Walk Trading Long Spread Duration Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. Duration can also be used. A portfolio’s spread duration will equal the weighted. When the duration spread is positive, it. spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. . Long Spread Duration.

From wcd.copernicus.org

WCD Large spread in the representation of compound longduration dry Long Spread Duration the duration spread is a useful tool for predicting changes in interest rates. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. duration measures how long it takes,. Long Spread Duration.

From www.investopedia.com

Understanding Treasury Yield and Interest Rates Long Spread Duration duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. the duration spread is a useful tool for predicting changes in interest rates. When the duration spread is positive, it. Spread duration is a key metric that helps investors assess the price sensitivity of a bond. Long Spread Duration.

From www.shiftingshares.com

What Is Spread Duration A Comprehensive Guide Shifting Shares Long Spread Duration duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. Duration can also be used. Spread duration is a key metric that helps investors assess the price sensitivity of. Long Spread Duration.

From www.pzacademy.com

Spread duration有问必答品职教育 专注CFA ESG FRM CPA 考研等财经培训课程 Long Spread Duration the duration spread is a useful tool for predicting changes in interest rates. spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. When the duration spread is positive, it.. Long Spread Duration.

From www.researchgate.net

Comparison of longspread reflection moveout from a horizontal Long Spread Duration if an investor expects interest rates to fall during the course of the time the bond is held, a bond with a longer duration would be appealing because the bond’s value would increase more than comparable bonds with shorter durations. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in. Long Spread Duration.

From thetradingbible.com

Spread in Forex Explained Definition & Examples Long Spread Duration When the duration spread is positive, it. spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. Duration can also be used. duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. if an investor expects interest rates. Long Spread Duration.

From gioigngts.blob.core.windows.net

Spread Duration In Years at Susan Burgoon blog Long Spread Duration the duration spread is a useful tool for predicting changes in interest rates. if an investor expects interest rates to fall during the course of the time the bond is held, a bond with a longer duration would be appealing because the bond’s value would increase more than comparable bonds with shorter durations. Duration can also be used.. Long Spread Duration.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation, free download ID Long Spread Duration spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. When the duration spread is positive, it. if an investor expects interest rates to fall during the course of the time the bond is held, a bond with a longer duration would be appealing because the bond’s value would increase more. Long Spread Duration.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation ID3950949 Long Spread Duration spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. A portfolio’s spread duration will equal the weighted. Duration can also be used. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. When the duration spread is positive, it. . Long Spread Duration.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation, free download ID Long Spread Duration Duration can also be used. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. A portfolio’s spread duration will equal the weighted. When the duration spread is positive, it. the duration spread is a useful tool for predicting changes in interest rates. if an investor expects. Long Spread Duration.

From www.researchgate.net

(PDF) Large spread in the representation of compound longduration dry Long Spread Duration Duration can also be used. spread duration will equal the percentage change in a security’s price when credit spreads change by 1%. When the duration spread is positive, it. A portfolio’s spread duration will equal the weighted. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. . Long Spread Duration.

From www.pzacademy.com

spread duration有问必答品职教育 专注CFA ESG FRM CPA 考研等财经培训课程 Long Spread Duration if an investor expects interest rates to fall during the course of the time the bond is held, a bond with a longer duration would be appealing because the bond’s value would increase more than comparable bonds with shorter durations. When the duration spread is positive, it. Spread duration is a key metric that helps investors assess the price. Long Spread Duration.

From www.shutterstock.com

Chart Long Spread Options Strategy Financial Stock Photo 2026305545 Long Spread Duration Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. A portfolio’s spread duration will equal the weighted. duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. When the duration spread is positive, it. Duration. Long Spread Duration.

From econbrowser.com

Time Series on Term Spreads, Yield Curve Snapshots Econbrowser Long Spread Duration When the duration spread is positive, it. Spread duration is a key metric that helps investors assess the price sensitivity of a bond to changes in credit spreads. A portfolio’s spread duration will equal the weighted. Duration can also be used. duration measures how long it takes, in years, for an investor to be repaid a bond’s price through. Long Spread Duration.

From www.biancoresearch.com

Time to Extend Duration? Bianco Research Long Spread Duration When the duration spread is positive, it. if an investor expects interest rates to fall during the course of the time the bond is held, a bond with a longer duration would be appealing because the bond’s value would increase more than comparable bonds with shorter durations. spread duration will equal the percentage change in a security’s price. Long Spread Duration.

From www.projectfinance.com

How to Trade Options Calendar Spreads (Visuals and Examples) Long Spread Duration if an investor expects interest rates to fall during the course of the time the bond is held, a bond with a longer duration would be appealing because the bond’s value would increase more than comparable bonds with shorter durations. Duration can also be used. duration measures how long it takes, in years, for an investor to be. Long Spread Duration.