Franking Credits In Loss Trust . A trustee receiving a franked dividend includes both the amount of the dividend and the franking credit in the trust's assessable. A trust that is paid or credited franked dividends includes both the amount of. Claiming franking credits attached to a trust distribution. In order to be a qualified person the taxpayer must. The recent case of thomas v fct [2015] fca 968, reported at para [1424] of this bulletin, considers a number of key issues relating to the distribution. This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. This strategy, however, requires careful planning to ensure that there is sufficient distributable income so that franking credits aren’t lost. Beneficiaries of a unit trust may only claim franking credits if they are a “qualified person” in relation to the franked dividend. A very complex set of provisions.

from www.firstlinks.com.au

Claiming franking credits attached to a trust distribution. The recent case of thomas v fct [2015] fca 968, reported at para [1424] of this bulletin, considers a number of key issues relating to the distribution. This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. A trust that is paid or credited franked dividends includes both the amount of. Beneficiaries of a unit trust may only claim franking credits if they are a “qualified person” in relation to the franked dividend. A trustee receiving a franked dividend includes both the amount of the dividend and the franking credit in the trust's assessable. A very complex set of provisions. In order to be a qualified person the taxpayer must. This strategy, however, requires careful planning to ensure that there is sufficient distributable income so that franking credits aren’t lost.

Franking credits made easy

Franking Credits In Loss Trust In order to be a qualified person the taxpayer must. In order to be a qualified person the taxpayer must. A very complex set of provisions. Claiming franking credits attached to a trust distribution. This strategy, however, requires careful planning to ensure that there is sufficient distributable income so that franking credits aren’t lost. The recent case of thomas v fct [2015] fca 968, reported at para [1424] of this bulletin, considers a number of key issues relating to the distribution. This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. Beneficiaries of a unit trust may only claim franking credits if they are a “qualified person” in relation to the franked dividend. A trust that is paid or credited franked dividends includes both the amount of. A trustee receiving a franked dividend includes both the amount of the dividend and the franking credit in the trust's assessable.

From slideplayer.com

© National Core Accounting Publications ppt download Franking Credits In Loss Trust This strategy, however, requires careful planning to ensure that there is sufficient distributable income so that franking credits aren’t lost. In order to be a qualified person the taxpayer must. A trustee receiving a franked dividend includes both the amount of the dividend and the franking credit in the trust's assessable. A trust that is paid or credited franked dividends. Franking Credits In Loss Trust.

From sladen.com.au

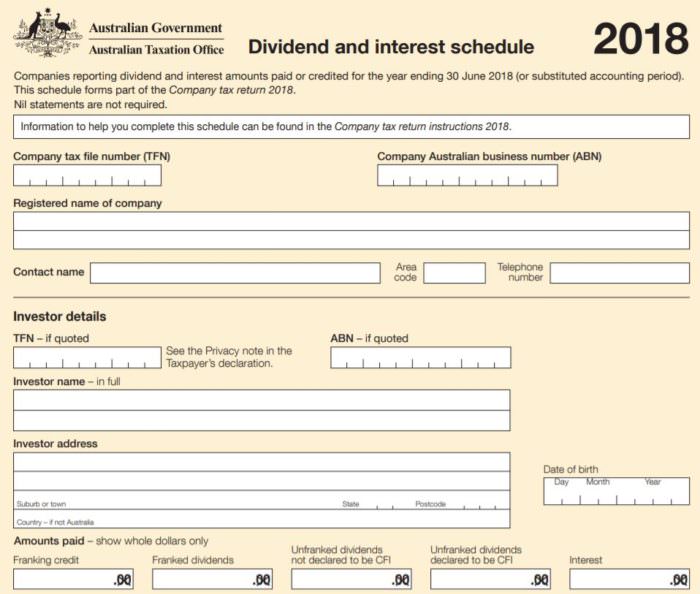

Trusts and the franking credits trap can we fix it? — Sladen Legal Franking Credits In Loss Trust Beneficiaries of a unit trust may only claim franking credits if they are a “qualified person” in relation to the franked dividend. A trust that is paid or credited franked dividends includes both the amount of. A trustee receiving a franked dividend includes both the amount of the dividend and the franking credit in the trust's assessable. Claiming franking credits. Franking Credits In Loss Trust.

From slideplayer.com

© National Core Accounting Publications ppt download Franking Credits In Loss Trust Claiming franking credits attached to a trust distribution. In order to be a qualified person the taxpayer must. Beneficiaries of a unit trust may only claim franking credits if they are a “qualified person” in relation to the franked dividend. A very complex set of provisions. The recent case of thomas v fct [2015] fca 968, reported at para [1424]. Franking Credits In Loss Trust.

From lodgeit.freshdesk.com

Q&A Share of Franking Credits / How to input dividend imputation Franking Credits In Loss Trust This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. In order to be a qualified person the taxpayer must. A trustee receiving a franked dividend includes both the amount of the dividend and the franking credit in the trust's assessable. Beneficiaries of a unit trust may only claim. Franking Credits In Loss Trust.

From corporatefinanceinstitute.com

Franking Credit Definition, How It Works, How to Calculate Franking Credits In Loss Trust In order to be a qualified person the taxpayer must. A trust that is paid or credited franked dividends includes both the amount of. A very complex set of provisions. Beneficiaries of a unit trust may only claim franking credits if they are a “qualified person” in relation to the franked dividend. The recent case of thomas v fct [2015]. Franking Credits In Loss Trust.

From www.forbes.com

How Do Franking Credits Work? Forbes Advisor Australia Franking Credits In Loss Trust A very complex set of provisions. A trustee receiving a franked dividend includes both the amount of the dividend and the franking credit in the trust's assessable. Claiming franking credits attached to a trust distribution. The recent case of thomas v fct [2015] fca 968, reported at para [1424] of this bulletin, considers a number of key issues relating to. Franking Credits In Loss Trust.

From medium.com

What are Franking Credits and How Do they Work? by West Court Family Franking Credits In Loss Trust In order to be a qualified person the taxpayer must. Beneficiaries of a unit trust may only claim franking credits if they are a “qualified person” in relation to the franked dividend. This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. A trust that is paid or credited. Franking Credits In Loss Trust.

From education.rask.com.au

Franking Credits Calculator & Video Explainer Franking Credits In Loss Trust A very complex set of provisions. A trust that is paid or credited franked dividends includes both the amount of. In order to be a qualified person the taxpayer must. This strategy, however, requires careful planning to ensure that there is sufficient distributable income so that franking credits aren’t lost. Beneficiaries of a unit trust may only claim franking credits. Franking Credits In Loss Trust.

From www.raskmedia.com.au

ATO franking credits explained Rask Media Franking Credits In Loss Trust In order to be a qualified person the taxpayer must. A very complex set of provisions. A trustee receiving a franked dividend includes both the amount of the dividend and the franking credit in the trust's assessable. This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. Claiming franking. Franking Credits In Loss Trust.

From www.sophisticatedaccess.com.au

Franking credits 101 Franking Credits In Loss Trust A trust that is paid or credited franked dividends includes both the amount of. A very complex set of provisions. The recent case of thomas v fct [2015] fca 968, reported at para [1424] of this bulletin, considers a number of key issues relating to the distribution. In order to be a qualified person the taxpayer must. A trustee receiving. Franking Credits In Loss Trust.

From www.livewiremarkets.com

The divide(nd) of how to invest for franking credits Sara Franking Credits In Loss Trust This strategy, however, requires careful planning to ensure that there is sufficient distributable income so that franking credits aren’t lost. The recent case of thomas v fct [2015] fca 968, reported at para [1424] of this bulletin, considers a number of key issues relating to the distribution. In order to be a qualified person the taxpayer must. A trustee receiving. Franking Credits In Loss Trust.

From www.solveaccounting.com.au

What are Franking Credits? How do Franking Credits work? Solve Accounting Franking Credits In Loss Trust This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. Claiming franking credits attached to a trust distribution. In order to be a qualified person the taxpayer must. The recent case of thomas v fct [2015] fca 968, reported at para [1424] of this bulletin, considers a number of. Franking Credits In Loss Trust.

From www.sharesight.com

How to calculate franking credits on your investment portfolio Sharesight Franking Credits In Loss Trust In order to be a qualified person the taxpayer must. A trustee receiving a franked dividend includes both the amount of the dividend and the franking credit in the trust's assessable. The recent case of thomas v fct [2015] fca 968, reported at para [1424] of this bulletin, considers a number of key issues relating to the distribution. This year,. Franking Credits In Loss Trust.

From www.bestetfs.com.au

ETF tax, distributions, DRPs and franking credits EVERYTHING explained Franking Credits In Loss Trust A trust that is paid or credited franked dividends includes both the amount of. The recent case of thomas v fct [2015] fca 968, reported at para [1424] of this bulletin, considers a number of key issues relating to the distribution. In order to be a qualified person the taxpayer must. Beneficiaries of a unit trust may only claim franking. Franking Credits In Loss Trust.

From www.elliotwatson.com.au

Franking Credits Explained Where Are We Now? Franking Credits In Loss Trust This strategy, however, requires careful planning to ensure that there is sufficient distributable income so that franking credits aren’t lost. This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. A trustee receiving a franked dividend includes both the amount of the dividend and the franking credit in the. Franking Credits In Loss Trust.

From www.lexology.com

New Franking Credit & Capital Loss Rules Impact Share Buyback Pricing Franking Credits In Loss Trust Beneficiaries of a unit trust may only claim franking credits if they are a “qualified person” in relation to the franked dividend. In order to be a qualified person the taxpayer must. A trust that is paid or credited franked dividends includes both the amount of. This strategy, however, requires careful planning to ensure that there is sufficient distributable income. Franking Credits In Loss Trust.

From pearler.com

The Complete Guide to Franking Credits Pearler Franking Credits In Loss Trust This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. A trustee receiving a franked dividend includes both the amount of the dividend and the franking credit in the trust's assessable. The recent case of thomas v fct [2015] fca 968, reported at para [1424] of this bulletin, considers. Franking Credits In Loss Trust.

From plato.com.au

What are franking credits? (and how they can help Australian investors Franking Credits In Loss Trust This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. A very complex set of provisions. Beneficiaries of a unit trust may only claim franking credits if they are a “qualified person” in relation to the franked dividend. In order to be a qualified person the taxpayer must. A. Franking Credits In Loss Trust.

From www.slideserve.com

PPT Chapter 12 Dividend and Share Repurchase Decisions PowerPoint Franking Credits In Loss Trust This strategy, however, requires careful planning to ensure that there is sufficient distributable income so that franking credits aren’t lost. This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. In order to be a qualified person the taxpayer must. A trust that is paid or credited franked dividends. Franking Credits In Loss Trust.

From www.youtube.com

Explained What are franking credits? Rask [HD] YouTube Franking Credits In Loss Trust A trustee receiving a franked dividend includes both the amount of the dividend and the franking credit in the trust's assessable. The recent case of thomas v fct [2015] fca 968, reported at para [1424] of this bulletin, considers a number of key issues relating to the distribution. A very complex set of provisions. A trust that is paid or. Franking Credits In Loss Trust.

From www.sharesight.com

How to calculate franking credits on your investment portfolio Sharesight Franking Credits In Loss Trust The recent case of thomas v fct [2015] fca 968, reported at para [1424] of this bulletin, considers a number of key issues relating to the distribution. Beneficiaries of a unit trust may only claim franking credits if they are a “qualified person” in relation to the franked dividend. Claiming franking credits attached to a trust distribution. This year, there. Franking Credits In Loss Trust.

From lodgeit.freshdesk.com

Understanding Franking Credits LodgeiT Franking Credits In Loss Trust Claiming franking credits attached to a trust distribution. This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. A trustee receiving a franked dividend includes both the amount of the dividend and the franking credit in the trust's assessable. This strategy, however, requires careful planning to ensure that there. Franking Credits In Loss Trust.

From www.uslegalforms.com

Distribution Agreement Trust With Franking Credits US Legal Forms Franking Credits In Loss Trust Beneficiaries of a unit trust may only claim franking credits if they are a “qualified person” in relation to the franked dividend. This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. This strategy, however, requires careful planning to ensure that there is sufficient distributable income so that franking. Franking Credits In Loss Trust.

From www.sharecafe.com.au

Loss Of Franking Credit Is A Game Changer ShareCafe Franking Credits In Loss Trust The recent case of thomas v fct [2015] fca 968, reported at para [1424] of this bulletin, considers a number of key issues relating to the distribution. A very complex set of provisions. Beneficiaries of a unit trust may only claim franking credits if they are a “qualified person” in relation to the franked dividend. A trust that is paid. Franking Credits In Loss Trust.

From businessstudycenter.com

What is a Franking Credit and How Does it Work? Business Study Center Franking Credits In Loss Trust A very complex set of provisions. The recent case of thomas v fct [2015] fca 968, reported at para [1424] of this bulletin, considers a number of key issues relating to the distribution. This strategy, however, requires careful planning to ensure that there is sufficient distributable income so that franking credits aren’t lost. Claiming franking credits attached to a trust. Franking Credits In Loss Trust.

From www.expatustax.com

Franking Credits (Guidelines) Expat US Tax Franking Credits In Loss Trust A trust that is paid or credited franked dividends includes both the amount of. Claiming franking credits attached to a trust distribution. In order to be a qualified person the taxpayer must. Beneficiaries of a unit trust may only claim franking credits if they are a “qualified person” in relation to the franked dividend. This year, there is an income. Franking Credits In Loss Trust.

From www.morningstar.com.au

How to calculate franking credits on your investment portfolio Franking Credits In Loss Trust A very complex set of provisions. Beneficiaries of a unit trust may only claim franking credits if they are a “qualified person” in relation to the franked dividend. In order to be a qualified person the taxpayer must. Claiming franking credits attached to a trust distribution. A trustee receiving a franked dividend includes both the amount of the dividend and. Franking Credits In Loss Trust.

From australiainstitute.org.au

Why the Government doesn’t want you to understand how franking credits Franking Credits In Loss Trust A very complex set of provisions. In order to be a qualified person the taxpayer must. The recent case of thomas v fct [2015] fca 968, reported at para [1424] of this bulletin, considers a number of key issues relating to the distribution. This strategy, however, requires careful planning to ensure that there is sufficient distributable income so that franking. Franking Credits In Loss Trust.

From www.youtube.com

What are franking credits? (Australia) YouTube Franking Credits In Loss Trust A very complex set of provisions. A trustee receiving a franked dividend includes both the amount of the dividend and the franking credit in the trust's assessable. In order to be a qualified person the taxpayer must. A trust that is paid or credited franked dividends includes both the amount of. Beneficiaries of a unit trust may only claim franking. Franking Credits In Loss Trust.

From www.elliotwatson.com.au

Franking Credits Explained Where Are We Now? Franking Credits In Loss Trust A trustee receiving a franked dividend includes both the amount of the dividend and the franking credit in the trust's assessable. This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. This strategy, however, requires careful planning to ensure that there is sufficient distributable income so that franking credits. Franking Credits In Loss Trust.

From www.firstlinks.com.au

Franking credits made easy Franking Credits In Loss Trust A trust that is paid or credited franked dividends includes both the amount of. In order to be a qualified person the taxpayer must. Claiming franking credits attached to a trust distribution. This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. This strategy, however, requires careful planning to. Franking Credits In Loss Trust.

From www.youtube.com

What are Franking Credits? YouTube Franking Credits In Loss Trust Beneficiaries of a unit trust may only claim franking credits if they are a “qualified person” in relation to the franked dividend. This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. A trust that is paid or credited franked dividends includes both the amount of. Claiming franking credits. Franking Credits In Loss Trust.

From support.simpleinvest360.com

Franking Credit Tax Offsets Simple Invest 360 Franking Credits In Loss Trust A very complex set of provisions. In order to be a qualified person the taxpayer must. Claiming franking credits attached to a trust distribution. The recent case of thomas v fct [2015] fca 968, reported at para [1424] of this bulletin, considers a number of key issues relating to the distribution. This strategy, however, requires careful planning to ensure that. Franking Credits In Loss Trust.

From www.halesdouglass.com.au

Franking credits and SMSFs Franking Credits In Loss Trust This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. A trustee receiving a franked dividend includes both the amount of the dividend and the franking credit in the trust's assessable. A very complex set of provisions. Beneficiaries of a unit trust may only claim franking credits if they. Franking Credits In Loss Trust.

From www.raskmedia.com.au

ATO franking credits explained Rask Media Franking Credits In Loss Trust In order to be a qualified person the taxpayer must. A trust that is paid or credited franked dividends includes both the amount of. Claiming franking credits attached to a trust distribution. This year, there is an income of $75,000 (include franking credit of $18,000), which makes the trust net income $5,000 after. Beneficiaries of a unit trust may only. Franking Credits In Loss Trust.