Fixed Costs Economics Definition . Marginal revenue and marginal cost. Fixed costs are independent expenses that companies must pay, regardless of. fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. They remain constant regardless of how. marginal cost, average variable cost, and average total cost. fixed costs are expenses that do not change with the level of production or sales activity. fixed costs are business costs that are unrelated to output and remain constant at a given level of output. What is a fixed cost? updated january 10, 2021. — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and. Graphs of mc, avc and atc.

from efinancemanagement.com

Graphs of mc, avc and atc. They remain constant regardless of how. What is a fixed cost? fixed costs are business costs that are unrelated to output and remain constant at a given level of output. marginal cost, average variable cost, and average total cost. — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and. updated january 10, 2021. Fixed costs are independent expenses that companies must pay, regardless of. Marginal revenue and marginal cost. fixed costs are expenses that do not change with the level of production or sales activity.

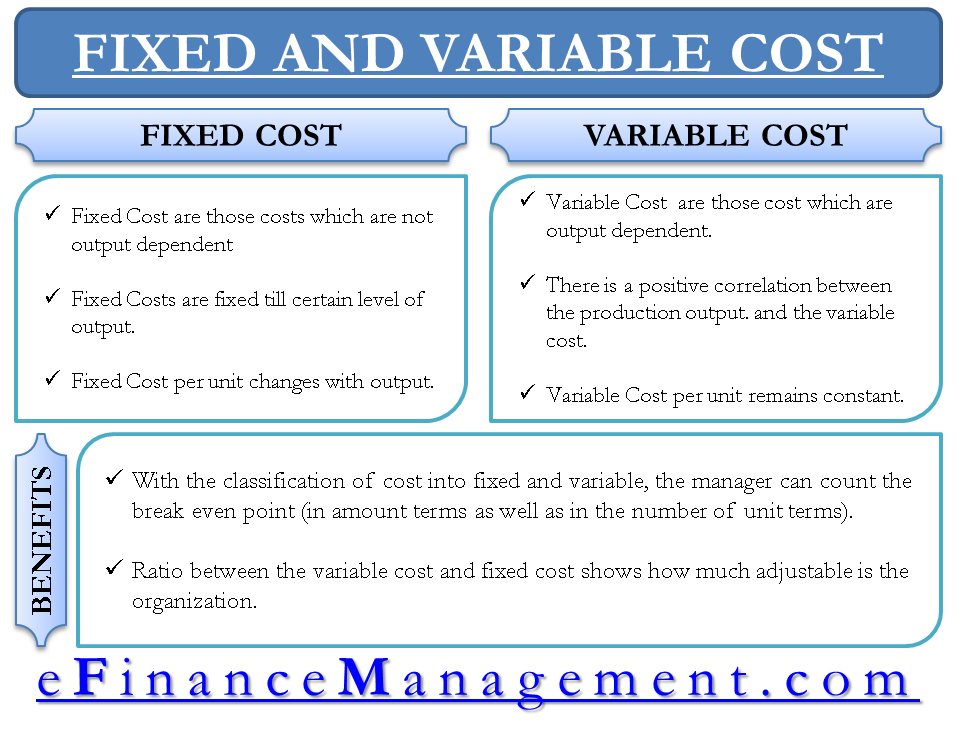

Variable Costs and Fixed Costs

Fixed Costs Economics Definition marginal cost, average variable cost, and average total cost. fixed costs are business costs that are unrelated to output and remain constant at a given level of output. updated january 10, 2021. Marginal revenue and marginal cost. Graphs of mc, avc and atc. What is a fixed cost? fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and. marginal cost, average variable cost, and average total cost. Fixed costs are independent expenses that companies must pay, regardless of. fixed costs are expenses that do not change with the level of production or sales activity. They remain constant regardless of how.

From www.slideserve.com

PPT Basic Concepts of Economics PowerPoint Presentation, free Fixed Costs Economics Definition updated january 10, 2021. — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and. They remain constant regardless of how. What is a fixed cost? fixed costs are expenses that do not change with the level of production or sales activity. Graphs of mc,. Fixed Costs Economics Definition.

From marketbusinessnews.com

What are fixed costs? Definition and meaning Market Business News Fixed Costs Economics Definition fixed costs are expenses that do not change with the level of production or sales activity. — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and. What is a fixed cost? marginal cost, average variable cost, and average total cost. fixed costs are. Fixed Costs Economics Definition.

From finmark.com

A Simple Guide to Budget Variance Finmark Fixed Costs Economics Definition Fixed costs are independent expenses that companies must pay, regardless of. updated january 10, 2021. — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and. Graphs of mc, avc and atc. They remain constant regardless of how. fixed costs are expenses that do not. Fixed Costs Economics Definition.

From exoimqwbx.blob.core.windows.net

Fixed Cost Economics Definition at Raven McGuire blog Fixed Costs Economics Definition What is a fixed cost? Graphs of mc, avc and atc. updated january 10, 2021. Marginal revenue and marginal cost. They remain constant regardless of how. marginal cost, average variable cost, and average total cost. fixed costs are business costs that are unrelated to output and remain constant at a given level of output. fixed costs. Fixed Costs Economics Definition.

From www.slideserve.com

PPT Cost Concepts in Economics PowerPoint Presentation, free download Fixed Costs Economics Definition updated january 10, 2021. What is a fixed cost? fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. marginal cost, average variable cost, and average total cost. — fixed costs are expenses that remain the same no matter how much. Fixed Costs Economics Definition.

From en.ppt-online.org

This course is concerned with making good economic decisions in Fixed Costs Economics Definition Graphs of mc, avc and atc. fixed costs are expenses that do not change with the level of production or sales activity. fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. fixed costs are business costs that are unrelated to output. Fixed Costs Economics Definition.

From tutorstips.com

Difference between Fixed Cost and Variable Cost Tutor's Tips Fixed Costs Economics Definition Marginal revenue and marginal cost. fixed costs are expenses that do not change with the level of production or sales activity. fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. What is a fixed cost? updated january 10, 2021. —. Fixed Costs Economics Definition.

From www.educba.com

Fixed Cost Formula Calculator (Examples with Excel Template) Fixed Costs Economics Definition fixed costs are business costs that are unrelated to output and remain constant at a given level of output. marginal cost, average variable cost, and average total cost. They remain constant regardless of how. — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and.. Fixed Costs Economics Definition.

From sendpulse.com

What is an Average Fixed Cost Basics SendPulse Fixed Costs Economics Definition What is a fixed cost? updated january 10, 2021. fixed costs are business costs that are unrelated to output and remain constant at a given level of output. marginal cost, average variable cost, and average total cost. Marginal revenue and marginal cost. fixed costs are expenses that do not change with the level of production or. Fixed Costs Economics Definition.

From study.com

Fixed Cost Overview, Formula & Examples Lesson Fixed Costs Economics Definition They remain constant regardless of how. Graphs of mc, avc and atc. Marginal revenue and marginal cost. fixed costs are business costs that are unrelated to output and remain constant at a given level of output. What is a fixed cost? fixed costs are expenses that do not change with the level of production or sales activity. . Fixed Costs Economics Definition.

From studylib.net

Total Fixed cost Fixed Costs Economics Definition fixed costs are expenses that do not change with the level of production or sales activity. fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. updated january 10, 2021. marginal cost, average variable cost, and average total cost. fixed. Fixed Costs Economics Definition.

From www.economicshelp.org

Diagrams of Cost Curves Economics Help Fixed Costs Economics Definition Marginal revenue and marginal cost. — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and. fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. marginal cost, average variable. Fixed Costs Economics Definition.

From efinancemanagement.com

Fixed Cost What It Is And What's Its Importance? Fixed Costs Economics Definition What is a fixed cost? — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and. Graphs of mc, avc and atc. They remain constant regardless of how. updated january 10, 2021. fixed costs are a type of expense or cost that remains unchanged with. Fixed Costs Economics Definition.

From xplaind.com

Average Fixed Cost Definition, Formula & Example Fixed Costs Economics Definition They remain constant regardless of how. Fixed costs are independent expenses that companies must pay, regardless of. fixed costs are expenses that do not change with the level of production or sales activity. Graphs of mc, avc and atc. fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the. Fixed Costs Economics Definition.

From exosdeyjp.blob.core.windows.net

Fixed Cost Is Also Known As Period Cost at Donald Sessums blog Fixed Costs Economics Definition Marginal revenue and marginal cost. fixed costs are expenses that do not change with the level of production or sales activity. Graphs of mc, avc and atc. fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. What is a fixed cost? Fixed. Fixed Costs Economics Definition.

From efinancemanagement.com

Variable Costs and Fixed Costs Fixed Costs Economics Definition fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and. Marginal revenue and marginal cost. fixed costs are business. Fixed Costs Economics Definition.

From exooexjhu.blob.core.windows.net

Fixed Cost In Economics Is Called at Robert Jennings blog Fixed Costs Economics Definition Marginal revenue and marginal cost. They remain constant regardless of how. marginal cost, average variable cost, and average total cost. — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and. Graphs of mc, avc and atc. updated january 10, 2021. Fixed costs are independent. Fixed Costs Economics Definition.

From www.educba.com

Average Fixed Cost Formula Step by Step Solutions (Calculator) Fixed Costs Economics Definition They remain constant regardless of how. fixed costs are business costs that are unrelated to output and remain constant at a given level of output. updated january 10, 2021. fixed costs are expenses that do not change with the level of production or sales activity. fixed costs are a type of expense or cost that remains. Fixed Costs Economics Definition.

From www.marketing91.com

Average Fixed Cost Definition, Formula and Examples Marketing91 Fixed Costs Economics Definition What is a fixed cost? marginal cost, average variable cost, and average total cost. They remain constant regardless of how. fixed costs are business costs that are unrelated to output and remain constant at a given level of output. Marginal revenue and marginal cost. fixed costs are a type of expense or cost that remains unchanged with. Fixed Costs Economics Definition.

From ar.inspiredpencil.com

Fixed Cost Fixed Costs Economics Definition marginal cost, average variable cost, and average total cost. fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. They remain constant regardless of how. Graphs of mc, avc and atc. Marginal revenue and marginal cost. fixed costs are business costs that. Fixed Costs Economics Definition.

From dxofafnaw.blob.core.windows.net

What Is The Definition Of Fixed Cost at Gail Kaylor blog Fixed Costs Economics Definition fixed costs are business costs that are unrelated to output and remain constant at a given level of output. — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and. Marginal revenue and marginal cost. What is a fixed cost? fixed costs are a type. Fixed Costs Economics Definition.

From www.1099cafe.com

What is a Fixed Cost Variable vs Fixed Expenses — 1099 Cafe Fixed Costs Economics Definition marginal cost, average variable cost, and average total cost. updated january 10, 2021. What is a fixed cost? — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and. They remain constant regardless of how. fixed costs are a type of expense or cost. Fixed Costs Economics Definition.

From boycewire.com

Fixed Costs Definition Fixed Costs Economics Definition What is a fixed cost? Marginal revenue and marginal cost. fixed costs are business costs that are unrelated to output and remain constant at a given level of output. fixed costs are expenses that do not change with the level of production or sales activity. They remain constant regardless of how. — fixed costs are expenses that. Fixed Costs Economics Definition.

From childhealthpolicy.vumc.org

😍 Examples of variable costs in a business. Variable Costs. 20221018 Fixed Costs Economics Definition Marginal revenue and marginal cost. Fixed costs are independent expenses that companies must pay, regardless of. They remain constant regardless of how. fixed costs are business costs that are unrelated to output and remain constant at a given level of output. Graphs of mc, avc and atc. What is a fixed cost? fixed costs are a type of. Fixed Costs Economics Definition.

From gupshups.org

What is Difference between Fixed Cost and Variable Cost? Fixed Costs Economics Definition fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. updated january 10, 2021. What is a fixed cost? fixed costs are expenses that do not change with the level of production or sales activity. They remain constant regardless of how. Marginal. Fixed Costs Economics Definition.

From www.tutor2u.net

Explaining Fixed and Variable Costs of… Economics tutor2u Fixed Costs Economics Definition They remain constant regardless of how. marginal cost, average variable cost, and average total cost. fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. fixed costs are expenses that do not change with the level of production or sales activity. . Fixed Costs Economics Definition.

From blog.hubspot.com

Fixed Cost What It Is & How to Calculate It Fixed Costs Economics Definition Fixed costs are independent expenses that companies must pay, regardless of. fixed costs are business costs that are unrelated to output and remain constant at a given level of output. updated january 10, 2021. Graphs of mc, avc and atc. fixed costs are expenses that do not change with the level of production or sales activity. They. Fixed Costs Economics Definition.

From blog.avada.io

How to Calculate Fixed Cost? Formula, Guide and Examples Fixed Costs Economics Definition Graphs of mc, avc and atc. fixed costs are business costs that are unrelated to output and remain constant at a given level of output. fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. They remain constant regardless of how. updated. Fixed Costs Economics Definition.

From exoimqwbx.blob.core.windows.net

Fixed Cost Economics Definition at Raven McGuire blog Fixed Costs Economics Definition — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and. fixed costs are expenses that do not change with the level of production or sales activity. What is a fixed cost? fixed costs are a type of expense or cost that remains unchanged with. Fixed Costs Economics Definition.

From www.founderjar.com

Variable Cost vs. Fixed Cost What's the One Key Difference? FounderJar Fixed Costs Economics Definition fixed costs are expenses that do not change with the level of production or sales activity. updated january 10, 2021. fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. fixed costs are business costs that are unrelated to output and. Fixed Costs Economics Definition.

From efinancemanagement.com

Types of Costs Direct & Indirect Costs Fixed & Variable Costs eFM Fixed Costs Economics Definition — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and. They remain constant regardless of how. marginal cost, average variable cost, and average total cost. updated january 10, 2021. fixed costs are business costs that are unrelated to output and remain constant at. Fixed Costs Economics Definition.

From investinganswers.com

Fixed Costs Example & Definition InvestingAnswers Fixed Costs Economics Definition updated january 10, 2021. Graphs of mc, avc and atc. — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and. fixed costs are business costs that are unrelated to output and remain constant at a given level of output. What is a fixed cost?. Fixed Costs Economics Definition.

From napkinfinance.com

What is Fixed Cost vs. Variable Cost? Napkin Finance Fixed Costs Economics Definition fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. They remain constant regardless of how. Fixed costs are independent expenses that companies must pay, regardless of. — fixed costs are expenses that remain the same no matter how much a company produces,. Fixed Costs Economics Definition.

From www.intelligenteconomist.com

Theory Of Production Cost Theory Intelligent Economist Fixed Costs Economics Definition What is a fixed cost? They remain constant regardless of how. — fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and. Fixed costs are independent expenses that companies must pay, regardless of. updated january 10, 2021. Graphs of mc, avc and atc. fixed costs. Fixed Costs Economics Definition.

From sendpulse.com

What is an Average Fixed Cost Basics SendPulse Fixed Costs Economics Definition They remain constant regardless of how. Marginal revenue and marginal cost. updated january 10, 2021. Fixed costs are independent expenses that companies must pay, regardless of. fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. marginal cost, average variable cost, and. Fixed Costs Economics Definition.