Marginal Cost Equilibrium . solving for equilibrium price and quantity. There are two settings where we derive equilibrium price and quantity. Changes in equilibrium price and quantity when supply and demand change. It is the additional cost of producing an additional. marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. in economics, marginal cost is the change in total production cost that comes from making or producing one additional unit. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. in a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal cost of attracting one more unit from one. changes in market equilibrium.

from 2012books.lardbucket.org

the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. in a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal cost of attracting one more unit from one. Changes in equilibrium price and quantity when supply and demand change. in economics, marginal cost is the change in total production cost that comes from making or producing one additional unit. changes in market equilibrium. marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. There are two settings where we derive equilibrium price and quantity. solving for equilibrium price and quantity. It is the additional cost of producing an additional.

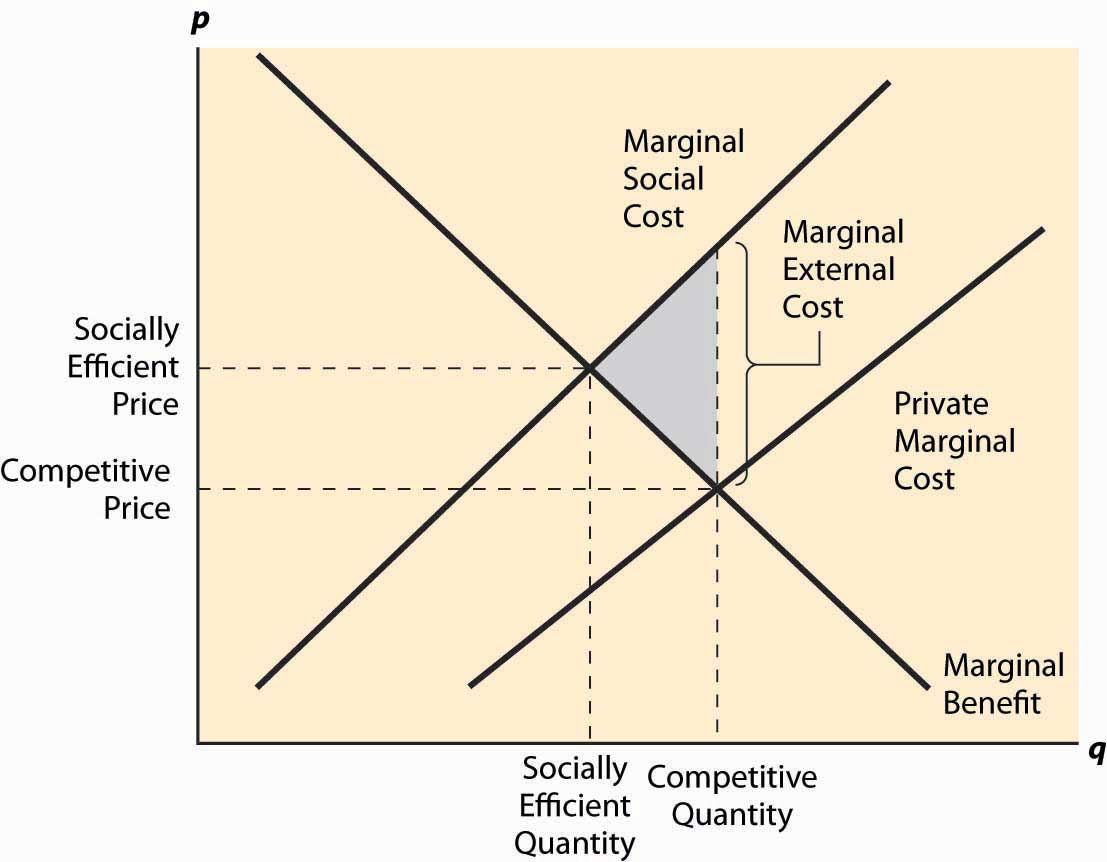

Externalities

Marginal Cost Equilibrium Changes in equilibrium price and quantity when supply and demand change. marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. changes in market equilibrium. It is the additional cost of producing an additional. Changes in equilibrium price and quantity when supply and demand change. There are two settings where we derive equilibrium price and quantity. solving for equilibrium price and quantity. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. in economics, marginal cost is the change in total production cost that comes from making or producing one additional unit. in a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal cost of attracting one more unit from one.

From www.youtube.com

Marginal revenue YouTube Marginal Cost Equilibrium changes in market equilibrium. Changes in equilibrium price and quantity when supply and demand change. marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. solving for equilibrium price and quantity. the marginal cost of production and marginal revenue are economic measures used to determine the amount. Marginal Cost Equilibrium.

From www.youtube.com

Marginal Cost and Benefit YouTube Marginal Cost Equilibrium the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. There are two settings where we derive equilibrium price and quantity. changes in market equilibrium. Changes in equilibrium price and quantity when supply and demand change. in a simple market under perfect competition, equilibrium occurs. Marginal Cost Equilibrium.

From www.researchgate.net

Equilibrium for a linear marginal cost, with a = 14, b = c = 1, F = 3 Marginal Cost Equilibrium solving for equilibrium price and quantity. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. There are two settings where we derive equilibrium price and quantity. It is the additional cost of producing an additional. Changes in equilibrium price and quantity when supply and demand. Marginal Cost Equilibrium.

From analystprep.com

Price, Marginal Cost, Marginal Revenue, Economic Profit, and the Marginal Cost Equilibrium It is the additional cost of producing an additional. solving for equilibrium price and quantity. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. Changes. Marginal Cost Equilibrium.

From www.researchgate.net

2 Equilibrium when the new technology increases marginal cost Marginal Cost Equilibrium changes in market equilibrium. There are two settings where we derive equilibrium price and quantity. solving for equilibrium price and quantity. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. in a simple market under perfect competition, equilibrium occurs at a quantity and. Marginal Cost Equilibrium.

From saylordotorg.github.io

Beyond Perfect Competition Marginal Cost Equilibrium the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. in economics, marginal cost is the change in total production cost that comes from making or producing one additional unit. Changes in equilibrium price and quantity when supply and demand change. It is the additional cost. Marginal Cost Equilibrium.

From www.investopedia.com

Marginal Revenue Explained, With Formula and Example Marginal Cost Equilibrium in a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal cost of attracting one more unit from one. Changes in equilibrium price and quantity when supply and demand change. There are two settings where we derive equilibrium price and quantity. solving for equilibrium price and quantity. the marginal cost of. Marginal Cost Equilibrium.

From www.researchgate.net

Equilibrium for a smoothed marginal cost function, for a = 14, b = c Marginal Cost Equilibrium There are two settings where we derive equilibrium price and quantity. Changes in equilibrium price and quantity when supply and demand change. marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. changes in market equilibrium. the marginal cost of production and marginal revenue are economic measures used. Marginal Cost Equilibrium.

From oneclass.com

REM 321 Textbook Notes Fall 2019, Chapter 3 Demand Curve, Marginal Marginal Cost Equilibrium the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. changes in market equilibrium. marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. Changes in equilibrium price and quantity when supply and demand change. . Marginal Cost Equilibrium.

From analystprep.com

Marginal Cost and Revenue, Economic Profit CFA Level 1 AnalystPrep Marginal Cost Equilibrium in economics, marginal cost is the change in total production cost that comes from making or producing one additional unit. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. Changes in equilibrium price and quantity when supply and demand change. There are two settings where. Marginal Cost Equilibrium.

From www.researchgate.net

Equilibrium for a quadratic marginal cost, saturated constraint, with a Marginal Cost Equilibrium Changes in equilibrium price and quantity when supply and demand change. solving for equilibrium price and quantity. It is the additional cost of producing an additional. There are two settings where we derive equilibrium price and quantity. in economics, marginal cost is the change in total production cost that comes from making or producing one additional unit. . Marginal Cost Equilibrium.

From www.chegg.com

Solved Price Monopoly equilibrium Marginal cost, MC p* Marginal Cost Equilibrium marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. solving for equilibrium price and quantity. It is the additional cost of producing an additional. changes in market equilibrium. Changes in equilibrium price and quantity when supply and demand change. the marginal cost of production and marginal. Marginal Cost Equilibrium.

From www.researchgate.net

Importing Marginal Cost and Markup Equilibrium Download Marginal Cost Equilibrium marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. in economics, marginal cost is the change in total production cost that comes from making or. Marginal Cost Equilibrium.

From analystprep.com

Price, Marginal Cost, Marginal Revenue, Economic Profit, and the Marginal Cost Equilibrium marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. changes in market equilibrium. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. in a simple market under perfect competition, equilibrium occurs at a. Marginal Cost Equilibrium.

From synder.com

How to Calculate Marginal Cost Marginal Cost Formula Marginal Cost Equilibrium marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. solving for equilibrium price and quantity. changes in market equilibrium. It is the additional cost. Marginal Cost Equilibrium.

From www.scribd.com

Topic 3 Market Equilibrium PDF Economic Equilibrium Marginal Cost Marginal Cost Equilibrium in a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal cost of attracting one more unit from one. Changes in equilibrium price and quantity when supply and demand change. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per.. Marginal Cost Equilibrium.

From itlessoneducation.com

Marginal cost Definition, formulas, curves and more It Lesson Education Marginal Cost Equilibrium marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. It is the additional cost of producing an additional. There are two settings where we derive equilibrium price and quantity. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and. Marginal Cost Equilibrium.

From www.researchgate.net

Equilibrium for a quadratic marginal cost, with a = 14, b = c = 1, g Marginal Cost Equilibrium Changes in equilibrium price and quantity when supply and demand change. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. solving for equilibrium price and quantity. There are two settings where we derive equilibrium price and quantity. It is the additional cost of producing an. Marginal Cost Equilibrium.

From studylib.net

Bertrand Equilibrium with Increasing Marginal Costs Marginal Cost Equilibrium It is the additional cost of producing an additional. in economics, marginal cost is the change in total production cost that comes from making or producing one additional unit. changes in market equilibrium. There are two settings where we derive equilibrium price and quantity. solving for equilibrium price and quantity. Changes in equilibrium price and quantity when. Marginal Cost Equilibrium.

From 2012books.lardbucket.org

Externalities Marginal Cost Equilibrium It is the additional cost of producing an additional. marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. in economics, marginal cost is the change. Marginal Cost Equilibrium.

From www.researchgate.net

Equilibrium for a smoothed marginal cost function, for a = 14, b = c Marginal Cost Equilibrium It is the additional cost of producing an additional. solving for equilibrium price and quantity. changes in market equilibrium. There are two settings where we derive equilibrium price and quantity. in economics, marginal cost is the change in total production cost that comes from making or producing one additional unit. in a simple market under perfect. Marginal Cost Equilibrium.

From www.meritnation.com

explain producer's equilibrium with help of marginal cost and marginal Marginal Cost Equilibrium It is the additional cost of producing an additional. Changes in equilibrium price and quantity when supply and demand change. in economics, marginal cost is the change in total production cost that comes from making or producing one additional unit. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output. Marginal Cost Equilibrium.

From www.studocu.com

Macroeconomics 2 Economic fundamentals marginal benefit = marginal Marginal Cost Equilibrium the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. It is the additional cost of producing an additional. in a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal cost of attracting one more unit from one. solving. Marginal Cost Equilibrium.

From www.youtube.com

2 Marginal Benefit and Marginal Cost YouTube Marginal Cost Equilibrium There are two settings where we derive equilibrium price and quantity. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. solving for equilibrium price and quantity. in economics, marginal cost is the change in total production cost that comes from making or producing one. Marginal Cost Equilibrium.

From www.youtube.com

Lindahl's Equilibrium Model Marginal social costs = sum of marginal Marginal Cost Equilibrium There are two settings where we derive equilibrium price and quantity. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. It is the additional cost of. Marginal Cost Equilibrium.

From www.scribd.com

Transactions and Strategies 1st Edition Michaels Test Bank PDF Marginal Cost Equilibrium in economics, marginal cost is the change in total production cost that comes from making or producing one additional unit. changes in market equilibrium. Changes in equilibrium price and quantity when supply and demand change. marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. in a. Marginal Cost Equilibrium.

From www.researchgate.net

Equilibrium of marginal utility and marginal cost of external Marginal Cost Equilibrium marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. solving for equilibrium price and quantity. There are two settings where we derive equilibrium price and quantity. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price. Marginal Cost Equilibrium.

From www.placeholder.vc

How To Think About Value — Placeholder Marginal Cost Equilibrium There are two settings where we derive equilibrium price and quantity. in a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal cost of attracting one more unit from one. changes in market equilibrium. It is the additional cost of producing an additional. marginal cost (mc) refers to the increase in. Marginal Cost Equilibrium.

From www.vrogue.co

The Diagram Shows The Demand Marginal Cost And Margin vrogue.co Marginal Cost Equilibrium in a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal cost of attracting one more unit from one. changes in market equilibrium. in economics, marginal cost is the change in total production cost that comes from making or producing one additional unit. solving for equilibrium price and quantity. . Marginal Cost Equilibrium.

From www.youtube.com

Equilibrium of Firm Marginal Cost Marginal Revenue Approach MC Marginal Cost Equilibrium the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. solving for equilibrium price and quantity. in economics, marginal cost is the change in total production cost that comes from making or producing one additional unit. in a simple market under perfect competition, equilibrium. Marginal Cost Equilibrium.

From www.scribd.com

Macroeconomics Worked Example PDF Economic Equilibrium Marginal Cost Marginal Cost Equilibrium the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. in a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal cost of attracting one more unit from one. It is the additional cost of producing an additional. changes. Marginal Cost Equilibrium.

From www.vrogue.co

The Diagram Shows The Demand Marginal Cost And Margin vrogue.co Marginal Cost Equilibrium in economics, marginal cost is the change in total production cost that comes from making or producing one additional unit. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. marginal cost (mc) refers to the increase in cost that is occasioned by the production. Marginal Cost Equilibrium.

From saylordotorg.github.io

Using the SupplyandDemand Framework Marginal Cost Equilibrium in a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal cost of attracting one more unit from one. It is the additional cost of producing an additional. the marginal cost of production and marginal revenue are economic measures used to determine the amount of output and the price per. marginal. Marginal Cost Equilibrium.

From www.scribd.com

Quiz 2 Matbis PDF Economic Equilibrium Marginal Cost Marginal Cost Equilibrium There are two settings where we derive equilibrium price and quantity. marginal cost (mc) refers to the increase in cost that is occasioned by the production of an extra unit. solving for equilibrium price and quantity. Changes in equilibrium price and quantity when supply and demand change. the marginal cost of production and marginal revenue are economic. Marginal Cost Equilibrium.

From www.vrogue.co

The Diagram Shows The Demand Marginal Cost And Margin vrogue.co Marginal Cost Equilibrium in economics, marginal cost is the change in total production cost that comes from making or producing one additional unit. Changes in equilibrium price and quantity when supply and demand change. It is the additional cost of producing an additional. changes in market equilibrium. solving for equilibrium price and quantity. the marginal cost of production and. Marginal Cost Equilibrium.