Suspended Loss Rules Cra . A suspended loss is a capital loss incurred in the current or previous years, but which is not eligible to be realized until a future year. Normally, capital losses are deductible against. Exceptions to superficial loss rules. A loss is suspended when the same or an identical property is purchased by or transferred to an affiliated person, other than in connection with a registered account. While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person. When the repurchased or substitute shares are sold, the loss can be claimed.

from www.financestrategists.com

When the repurchased or substitute shares are sold, the loss can be claimed. A suspended loss is a capital loss incurred in the current or previous years, but which is not eligible to be realized until a future year. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. Exceptions to superficial loss rules. Normally, capital losses are deductible against. A loss is suspended when the same or an identical property is purchased by or transferred to an affiliated person, other than in connection with a registered account. The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person. While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable.

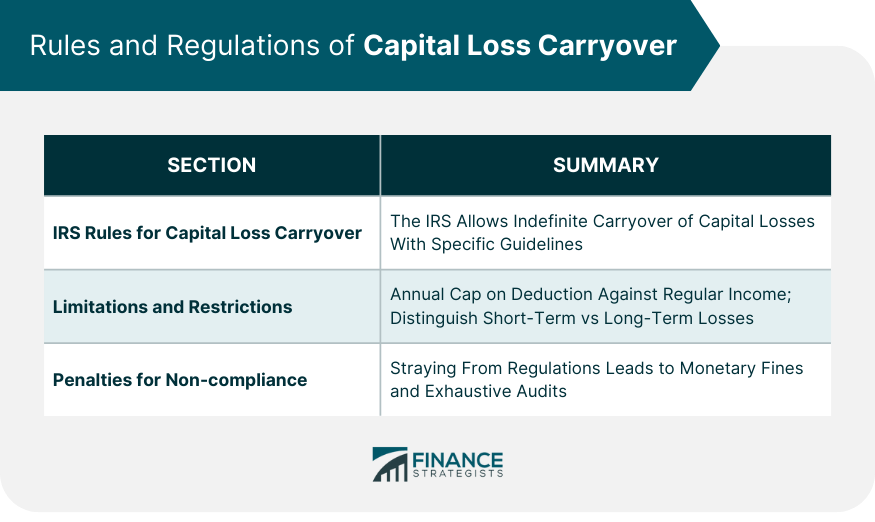

Capital Loss Carryover Definition, Conditions, Rules, Application

Suspended Loss Rules Cra A suspended loss is a capital loss incurred in the current or previous years, but which is not eligible to be realized until a future year. A suspended loss is a capital loss incurred in the current or previous years, but which is not eligible to be realized until a future year. A loss is suspended when the same or an identical property is purchased by or transferred to an affiliated person, other than in connection with a registered account. Exceptions to superficial loss rules. The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. Normally, capital losses are deductible against. While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. When the repurchased or substitute shares are sold, the loss can be claimed.

From www.slideserve.com

PPT Passive Loss Rules PowerPoint Presentation, free download ID Suspended Loss Rules Cra While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. When the repurchased or substitute shares are sold, the loss can be claimed. The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person. A loss is suspended when the same or an. Suspended Loss Rules Cra.

From www.chegg.com

Solved Rhonda has an adjusted basis and an atrisk amount of Suspended Loss Rules Cra When the repurchased or substitute shares are sold, the loss can be claimed. The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person. While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. Exceptions to superficial loss rules. A loss is suspended. Suspended Loss Rules Cra.

From www.slideserve.com

PPT Stop Loss Rules PowerPoint Presentation, free download ID3388185 Suspended Loss Rules Cra When the repurchased or substitute shares are sold, the loss can be claimed. Exceptions to superficial loss rules. While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. Normally, capital losses are deductible against. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation,. Suspended Loss Rules Cra.

From www.financestrategists.com

Capital Loss Carryover Definition, Conditions, Rules, Application Suspended Loss Rules Cra The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person. While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. Exceptions to superficial loss rules. When the repurchased or substitute shares are sold, the loss can be claimed. A suspended loss is. Suspended Loss Rules Cra.

From www.slideserve.com

PPT Chapter 11 PowerPoint Presentation, free download ID771696 Suspended Loss Rules Cra When the repurchased or substitute shares are sold, the loss can be claimed. While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. Normally, capital losses are deductible against. The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person. Exceptions to superficial. Suspended Loss Rules Cra.

From investors.wiki

Suspended Loss Investor's wiki Suspended Loss Rules Cra For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person. A. Suspended Loss Rules Cra.

From bvsa.co.za

Assessed Losses Brought Forward No Longer a Guarantee of Tax Relief Suspended Loss Rules Cra Exceptions to superficial loss rules. While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. Normally, capital losses are deductible against. A loss is suspended when the same or an identical. Suspended Loss Rules Cra.

From www.reddit.com

Please explain Carryover Amounts and Capital Gains Deduction table from Suspended Loss Rules Cra When the repurchased or substitute shares are sold, the loss can be claimed. A loss is suspended when the same or an identical property is purchased by or transferred to an affiliated person, other than in connection with a registered account. The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated. Suspended Loss Rules Cra.

From www.alphaexcapital.com

Unlocking the Power of StopLoss Rules A Complete Guide Suspended Loss Rules Cra Exceptions to superficial loss rules. Normally, capital losses are deductible against. A loss is suspended when the same or an identical property is purchased by or transferred to an affiliated person, other than in connection with a registered account. When the repurchased or substitute shares are sold, the loss can be claimed. The loss will be suspended until the same. Suspended Loss Rules Cra.

From www.slideserve.com

PPT Stop Loss Rules PowerPoint Presentation, free download ID3388185 Suspended Loss Rules Cra For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. Normally, capital losses are deductible against. While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. Exceptions to superficial loss rules. When the repurchased or substitute shares are sold, the loss. Suspended Loss Rules Cra.

From www.slideserve.com

PPT Stop Loss Rules PowerPoint Presentation, free download ID3388185 Suspended Loss Rules Cra When the repurchased or substitute shares are sold, the loss can be claimed. Normally, capital losses are deductible against. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. Exceptions to superficial loss rules. While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they. Suspended Loss Rules Cra.

From slideplayer.com

Investor Losses © 2018 Cengage Learning. All Rights Reserved. May not Suspended Loss Rules Cra While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. When the repurchased or substitute shares are sold, the loss can be claimed. Exceptions to superficial loss rules. A loss is suspended when the same or an identical property is purchased by or transferred to an affiliated person, other than in connection. Suspended Loss Rules Cra.

From ncrc.flywheelsites.com

NCRC forecast Weakening the Community Reinvestment Act would reduce Suspended Loss Rules Cra A suspended loss is a capital loss incurred in the current or previous years, but which is not eligible to be realized until a future year. While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. When the repurchased or substitute shares are sold, the loss can be claimed. Exceptions to superficial. Suspended Loss Rules Cra.

From www.slideserve.com

PPT Passive Loss Rules PowerPoint Presentation, free download ID Suspended Loss Rules Cra Exceptions to superficial loss rules. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. A loss is suspended when the same or an identical property is purchased by or transferred to an affiliated person, other than in connection with a registered account. A suspended loss is a capital. Suspended Loss Rules Cra.

From www.slideserve.com

PPT Chapter 11 PowerPoint Presentation, free download ID771696 Suspended Loss Rules Cra While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. Exceptions to superficial loss rules. Normally, capital losses are deductible against. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. The loss will be suspended until the same or an. Suspended Loss Rules Cra.

From www.alphaexcapital.com

Discover the Powerful 2 Stop Loss Rule for Trading Success Suspended Loss Rules Cra For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. Normally, capital losses are deductible against. The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person. Exceptions to superficial loss rules. A suspended loss is a capital loss incurred. Suspended Loss Rules Cra.

From www.slideserve.com

PPT Contracts PowerPoint Presentation, free download ID1688836 Suspended Loss Rules Cra While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. A suspended loss is a capital loss incurred in the current or previous years, but which is not eligible to be realized until a future year. A loss is suspended when the same or an identical property is purchased by or transferred. Suspended Loss Rules Cra.

From www.slideserve.com

PPT Stop Loss Rules PowerPoint Presentation, free download ID3388185 Suspended Loss Rules Cra The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person. A suspended loss is a capital loss incurred in the current or previous years, but which is not eligible to be realized until a future year. When the repurchased or substitute shares are sold, the loss can be claimed. A. Suspended Loss Rules Cra.

From www.chegg.com

Example 68 Pro rata allocation S has investments in Suspended Loss Rules Cra A suspended loss is a capital loss incurred in the current or previous years, but which is not eligible to be realized until a future year. Exceptions to superficial loss rules. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. The loss will be suspended until the same. Suspended Loss Rules Cra.

From studylib.net

5GS21.1 StopLoss Rules eLearning (eBook) Suspended Loss Rules Cra Normally, capital losses are deductible against. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. The loss will be suspended until the same or an identical property is ultimately disposed. Suspended Loss Rules Cra.

From www.journalofaccountancy.com

Managing S Corporation AtRisk Loss Limitations Suspended Loss Rules Cra A suspended loss is a capital loss incurred in the current or previous years, but which is not eligible to be realized until a future year. When the repurchased or substitute shares are sold, the loss can be claimed. Exceptions to superficial loss rules. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the. Suspended Loss Rules Cra.

From www.slideserve.com

PPT PAC PowerPoint Presentation, free download ID8783709 Suspended Loss Rules Cra The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. Exceptions to superficial loss rules. Normally, capital losses are deductible against. A loss is suspended when the same or. Suspended Loss Rules Cra.

From www.fatherskit.co

suspended passive losses suspended passive losses at death Lifecoach Suspended Loss Rules Cra Exceptions to superficial loss rules. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. Normally, capital losses are deductible against. The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person. When the repurchased or substitute shares are sold,. Suspended Loss Rules Cra.

From www.researchgate.net

Return loss of CRA_A with all switches OFF with/without DMSBSF Suspended Loss Rules Cra The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person. A loss is suspended when the same or an identical property is purchased by or transferred to an affiliated person, other than in connection with a registered account. When the repurchased or substitute shares are sold, the loss can be. Suspended Loss Rules Cra.

From www.slideserve.com

PPT Passive Loss Rules PowerPoint Presentation, free download ID Suspended Loss Rules Cra While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. Exceptions to superficial loss rules. A suspended loss is a capital loss incurred in the current or previous years, but which is not eligible to be realized until a future year. For a suspended loss, the deferred loss is deemed nil, is. Suspended Loss Rules Cra.

From www.chegg.com

Solved Problem 7a Investor Losses Manny Kant is invested Suspended Loss Rules Cra When the repurchased or substitute shares are sold, the loss can be claimed. Normally, capital losses are deductible against. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. A suspended loss is a capital loss incurred in the current or previous years, but which is not eligible to. Suspended Loss Rules Cra.

From www.studocu.com

ACCT226 Chapter 12 Exam Exercise 2 Exam Exercise Chapter 12 Stop Suspended Loss Rules Cra When the repurchased or substitute shares are sold, the loss can be claimed. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. A suspended loss is a capital loss incurred. Suspended Loss Rules Cra.

From www.youtube.com

IRS Form 8582 (Passive Activity Loss) Sale of Passive Activities with Suspended Loss Rules Cra A loss is suspended when the same or an identical property is purchased by or transferred to an affiliated person, other than in connection with a registered account. When the repurchased or substitute shares are sold, the loss can be claimed. Normally, capital losses are deductible against. The loss will be suspended until the same or an identical property is. Suspended Loss Rules Cra.

From voilanewyork20.com

The Science Behind StopLoss & Target Gain Learn When to Exit a Suspended Loss Rules Cra For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person. A. Suspended Loss Rules Cra.

From www.chegg.com

Solved Chandra was the sole shareholder of Pet Emporium, Suspended Loss Rules Cra A suspended loss is a capital loss incurred in the current or previous years, but which is not eligible to be realized until a future year. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. When the repurchased or substitute shares are sold, the loss can be claimed.. Suspended Loss Rules Cra.

From slideplayer.com

Losses Deductions and Limitations ppt download Suspended Loss Rules Cra A loss is suspended when the same or an identical property is purchased by or transferred to an affiliated person, other than in connection with a registered account. A suspended loss is a capital loss incurred in the current or previous years, but which is not eligible to be realized until a future year. The loss will be suspended until. Suspended Loss Rules Cra.

From slideplayer.com

Copyright ©2010 Cengage Learning ppt download Suspended Loss Rules Cra When the repurchased or substitute shares are sold, the loss can be claimed. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. Normally, capital losses are deductible against. The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person.. Suspended Loss Rules Cra.

From factsontaxes.com

How Do I Declare Capital Loss To CRA? Suspended Loss Rules Cra Normally, capital losses are deductible against. While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. When the repurchased or substitute shares are sold, the loss can be claimed. For a suspended loss, the deferred loss is deemed nil, is “suspended” and tracked by the original corporation, trust or partnership. The loss. Suspended Loss Rules Cra.

From www.thetaxadviser.com

Current developments in S corporations Suspended Loss Rules Cra While losses in your corporation, trust or partnership are undesirable from a conventional perspective, they can be valuable. When the repurchased or substitute shares are sold, the loss can be claimed. The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person. Exceptions to superficial loss rules. A suspended loss is. Suspended Loss Rules Cra.

From www.slideserve.com

PPT Passive Loss Rules PowerPoint Presentation, free download ID Suspended Loss Rules Cra A loss is suspended when the same or an identical property is purchased by or transferred to an affiliated person, other than in connection with a registered account. The loss will be suspended until the same or an identical property is ultimately disposed of by the affiliated person. Exceptions to superficial loss rules. While losses in your corporation, trust or. Suspended Loss Rules Cra.