Monte Carlo Simulation Vs . Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. This means it’s a method for simulating events that cannot be modelled implicitly. Monte carlo simulation (or method) is a probabilistic numerical technique used to estimate the outcome of a given, uncertain (stochastic) process. Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. Monte carlo simulation and historical simulation are both methods that can be used to determine the riskiness of a financial. What is monte carlo simulation? Simply put, monte carlo simulations provide a way to develop sequences of random market returns fitting predetermined characteristics, in order to test how financial. This method uses random sampling. The monte carlo method is a stochastic (random sampling of inputs) method to solve a statistical problem, and a simulation is a virtual representation of a problem.

from www.kitces.com

Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. What is monte carlo simulation? This method uses random sampling. Monte carlo simulation (or method) is a probabilistic numerical technique used to estimate the outcome of a given, uncertain (stochastic) process. Monte carlo simulation and historical simulation are both methods that can be used to determine the riskiness of a financial. Simply put, monte carlo simulations provide a way to develop sequences of random market returns fitting predetermined characteristics, in order to test how financial. This means it’s a method for simulating events that cannot be modelled implicitly. The monte carlo method is a stochastic (random sampling of inputs) method to solve a statistical problem, and a simulation is a virtual representation of a problem. A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system.

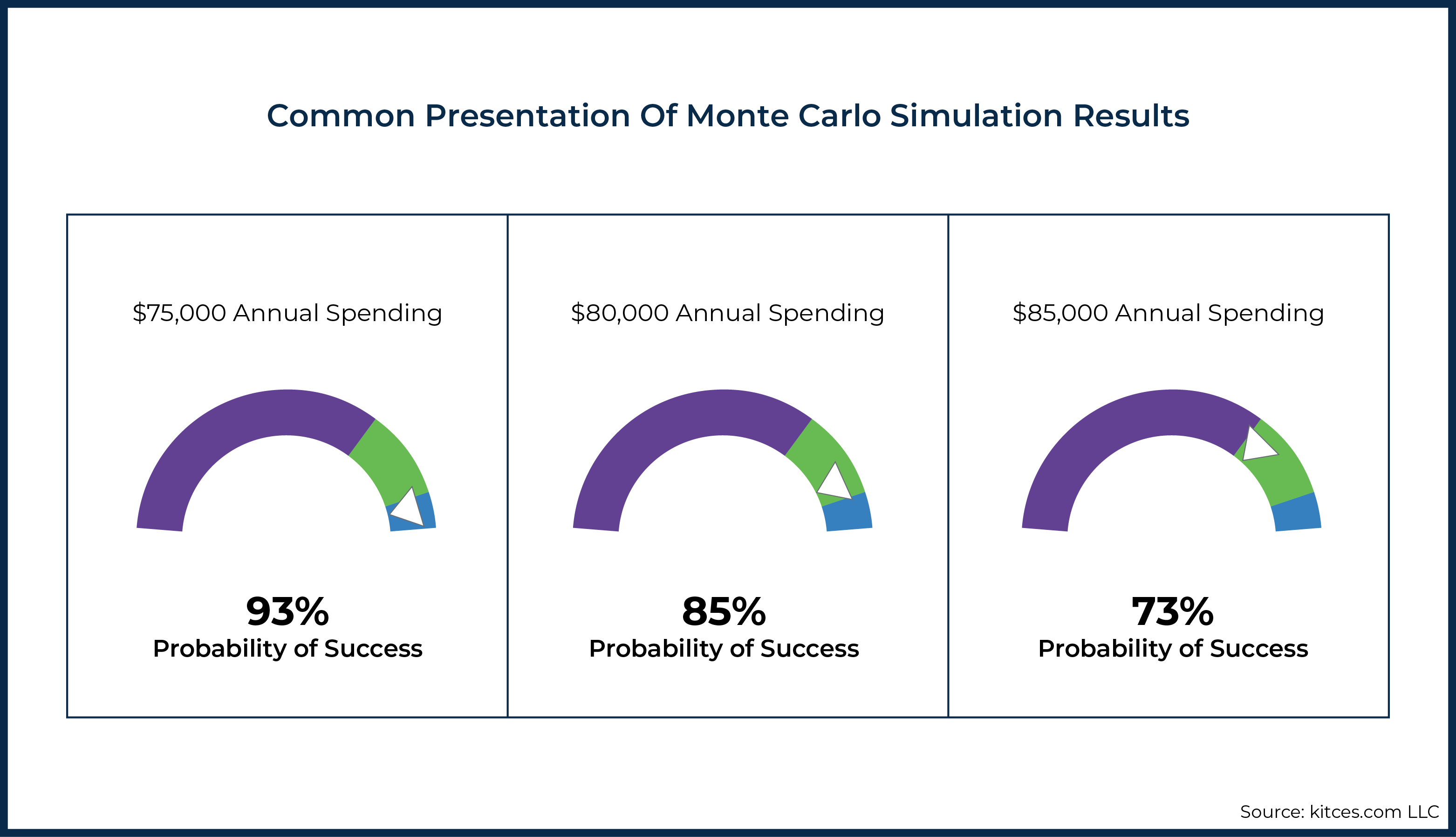

How Many Monte Carlo Simulations Are Enough?

Monte Carlo Simulation Vs Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. Monte carlo simulation (or method) is a probabilistic numerical technique used to estimate the outcome of a given, uncertain (stochastic) process. Monte carlo simulation and historical simulation are both methods that can be used to determine the riskiness of a financial. Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. Simply put, monte carlo simulations provide a way to develop sequences of random market returns fitting predetermined characteristics, in order to test how financial. This method uses random sampling. This means it’s a method for simulating events that cannot be modelled implicitly. What is monte carlo simulation? Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. The monte carlo method is a stochastic (random sampling of inputs) method to solve a statistical problem, and a simulation is a virtual representation of a problem.

From www.youtube.com

Monte Carlo Simulation In Trading YouTube Monte Carlo Simulation Vs Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. The monte carlo method is a stochastic (random sampling of inputs) method to solve a statistical problem, and a simulation is a virtual representation of a problem. This method uses random sampling. This means it’s a method for simulating events that cannot be modelled implicitly.. Monte Carlo Simulation Vs.

From studylib.net

Monte Carlo Simulation Monte Carlo Simulation Vs A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. This method uses random sampling. This means it’s a method for simulating events that cannot be modelled implicitly. Monte carlo simulation and historical simulation are both methods that can be used to determine the riskiness. Monte Carlo Simulation Vs.

From www.youtube.com

Monte Carlo Simulation in Regression/Econometric Using Excel AddIn Monte Carlo Simulation Vs A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. The monte carlo method is a stochastic (random sampling of inputs) method to solve a statistical problem, and a simulation is a virtual representation of a problem. What is monte carlo simulation? This means it’s. Monte Carlo Simulation Vs.

From www.youtube.com

Introduction to Monte Carlo Simulation YouTube Monte Carlo Simulation Vs This means it’s a method for simulating events that cannot be modelled implicitly. Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. What is monte carlo simulation? Monte carlo simulation (or method) is a probabilistic numerical technique used to estimate the outcome of a given, uncertain (stochastic) process. Monte carlo simulation and historical simulation. Monte Carlo Simulation Vs.

From www.youtube.com

Monte Carlo Simulation vs. Historical Simulation YouTube Monte Carlo Simulation Vs This method uses random sampling. Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. What is monte carlo simulation? Simply put, monte carlo simulations provide a way to develop sequences of random market returns fitting predetermined characteristics, in order to test how financial. Monte carlo. Monte Carlo Simulation Vs.

From www.mcleanam.com

Monte Carlo Simulations vs. Historical Simulations Monte Carlo Simulation Vs Monte carlo simulation (or method) is a probabilistic numerical technique used to estimate the outcome of a given, uncertain (stochastic) process. Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is. Monte Carlo Simulation Vs.

From projectmanagementacademy.net

Understanding the Monte Carlo Analysis in Project Management Project Monte Carlo Simulation Vs Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. Monte carlo simulation and historical simulation are both methods that can be used to determine the riskiness of a financial.. Monte Carlo Simulation Vs.

From www.researchgate.net

Direct Simulation Monte Carlo simulation of the interaction between the Monte Carlo Simulation Vs Simply put, monte carlo simulations provide a way to develop sequences of random market returns fitting predetermined characteristics, in order to test how financial. This method uses random sampling. This means it’s a method for simulating events that cannot be modelled implicitly. What is monte carlo simulation? Monte carlo simulation uses random sampling to produce simulated outcomes of a process. Monte Carlo Simulation Vs.

From www.slideserve.com

PPT Monte Carlo Simulation PowerPoint Presentation, free download Monte Carlo Simulation Vs This method uses random sampling. A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. What is monte carlo simulation? This. Monte Carlo Simulation Vs.

From www.analyticsvidhya.com

A Guide To Monte Carlo Simulation! Analytics Vidhya Monte Carlo Simulation Vs A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. What is monte carlo simulation? Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. This method uses random sampling. Monte carlo simulation and historical simulation are both methods that. Monte Carlo Simulation Vs.

From www.forbes.com

Monte Carlo Simulations Versus Historical Simulations (Updated To 2018) Monte Carlo Simulation Vs Monte carlo simulation and historical simulation are both methods that can be used to determine the riskiness of a financial. Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. Simply put, monte carlo simulations provide a way to develop sequences of random market returns fitting. Monte Carlo Simulation Vs.

From www.youtube.com

Monte Carlo Simulation and Python 4 Plotting with Matplotlib YouTube Monte Carlo Simulation Vs Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. Monte carlo simulation (or method) is a probabilistic numerical technique used to estimate the outcome of a given, uncertain (stochastic) process.. Monte Carlo Simulation Vs.

From www.slideserve.com

PPT PhotonPomeron Interactions at RHIC PowerPoint Presentation, free Monte Carlo Simulation Vs Simply put, monte carlo simulations provide a way to develop sequences of random market returns fitting predetermined characteristics, in order to test how financial. A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. Monte carlo simulation uses random sampling to produce simulated outcomes of. Monte Carlo Simulation Vs.

From medium.com

Measuring Portfolio risk using Monte Carlo simulation in python — Part Monte Carlo Simulation Vs What is monte carlo simulation? This method uses random sampling. Monte carlo simulation (or method) is a probabilistic numerical technique used to estimate the outcome of a given, uncertain (stochastic) process. This means it’s a method for simulating events that cannot be modelled implicitly. The monte carlo method is a stochastic (random sampling of inputs) method to solve a statistical. Monte Carlo Simulation Vs.

From www.youtube.com

CompChem02.07 Simulations with MM Force Fields — Monte Carlo and Monte Carlo Simulation Vs This means it’s a method for simulating events that cannot be modelled implicitly. Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables. Monte Carlo Simulation Vs.

From www.researchgate.net

Monte Carlo Simulation sample output frequency chart nonretrofitted Monte Carlo Simulation Vs Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. Simply put, monte carlo simulations provide a way to develop sequences of random market returns fitting predetermined characteristics, in order to test how financial. Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to. Monte Carlo Simulation Vs.

From www.youtube.com

Basics of Monte Carlo Simulation YouTube Monte Carlo Simulation Vs Simply put, monte carlo simulations provide a way to develop sequences of random market returns fitting predetermined characteristics, in order to test how financial. This method uses random sampling. A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. Monte carlo methods, or monte carlo. Monte Carlo Simulation Vs.

From en.guidingdata.com

Monte Carlo Simulations for Portfolios The Power of Big Numbers (Part Monte Carlo Simulation Vs What is monte carlo simulation? This means it’s a method for simulating events that cannot be modelled implicitly. This method uses random sampling. Simply put, monte carlo simulations provide a way to develop sequences of random market returns fitting predetermined characteristics, in order to test how financial. Monte carlo simulation (or method) is a probabilistic numerical technique used to estimate. Monte Carlo Simulation Vs.

From www.researchgate.net

Monte Carlo simulation vs analytical solution for light output. (a Monte Carlo Simulation Vs This method uses random sampling. What is monte carlo simulation? Monte carlo simulation and historical simulation are both methods that can be used to determine the riskiness of a financial. Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. Simply put, monte carlo simulations provide a way to develop sequences of random market returns. Monte Carlo Simulation Vs.

From www.kitces.com

How Many Monte Carlo Simulations Are Enough? Monte Carlo Simulation Vs Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. Simply put, monte carlo simulations provide a way to develop sequences of random market returns fitting predetermined characteristics, in order to test how financial. This method uses random sampling. A monte carlo simulation is a model used to predict the probability of a variety of. Monte Carlo Simulation Vs.

From projectionlab.com

Run Monte Carlo Simulations ProjectionLab Monte Carlo Simulation Vs Simply put, monte carlo simulations provide a way to develop sequences of random market returns fitting predetermined characteristics, in order to test how financial. This method uses random sampling. This means it’s a method for simulating events that cannot be modelled implicitly. Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated. Monte Carlo Simulation Vs.

From www.researchgate.net

Monte Carlo simulations results incremental saving vs avoided Monte Carlo Simulation Vs This method uses random sampling. This means it’s a method for simulating events that cannot be modelled implicitly. Monte carlo simulation (or method) is a probabilistic numerical technique used to estimate the outcome of a given, uncertain (stochastic) process. Simply put, monte carlo simulations provide a way to develop sequences of random market returns fitting predetermined characteristics, in order to. Monte Carlo Simulation Vs.

From medium.com

A StepbyStep Guide to Monte Carlo Simulation in R by Pelin Okutan Monte Carlo Simulation Vs Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. What is monte carlo simulation? This method uses random sampling. Monte carlo simulation and historical simulation are both methods that can be used to determine the riskiness of a financial. Monte carlo simulation (or method) is. Monte Carlo Simulation Vs.

From www.linkedin.com

Monte Carlo Simulation in an Agile World Monte Carlo Simulation Vs Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. The monte carlo method is a stochastic (random sampling of inputs) method to solve a statistical problem, and a simulation is a virtual representation of a problem. What is monte carlo simulation? Monte carlo simulation and historical simulation are both methods that can be used. Monte Carlo Simulation Vs.

From alfasoft.com

Risk Monte Carlo Simulation Analysis in Excel Alfasoft Monte Carlo Simulation Vs A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. Simply put, monte carlo simulations provide a way to develop sequences of random market returns fitting predetermined characteristics, in order to test how financial. Monte carlo methods, or monte carlo experiments, are a broad class. Monte Carlo Simulation Vs.

From www.youtube.com

Monte Carlo Simulation and Simple Linear Regression YouTube Monte Carlo Simulation Vs A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. This means it’s a method for simulating events that cannot be modelled implicitly. Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. Monte carlo methods, or monte carlo experiments,. Monte Carlo Simulation Vs.

From www.youtube.com

Monte Carlo Simulation for the beginners C++ Code YouTube Monte Carlo Simulation Vs Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. Monte carlo simulation (or method) is a probabilistic numerical technique used to estimate the outcome of a given, uncertain (stochastic) process. What is monte carlo simulation? Monte carlo simulation and historical simulation are both methods that. Monte Carlo Simulation Vs.

From getnave.com

Monte Carlo Simulation Explained How to Make Reliable Forecasts Nave Monte Carlo Simulation Vs A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. What is monte carlo simulation? This method uses random sampling. Monte carlo simulation and historical simulation are both methods that can be used to determine the riskiness of a financial. Simply put, monte carlo simulations. Monte Carlo Simulation Vs.

From www.toptal.com

Comprehensive Monte Carlo Simulation Tutorial Toptal® Monte Carlo Simulation Vs The monte carlo method is a stochastic (random sampling of inputs) method to solve a statistical problem, and a simulation is a virtual representation of a problem. Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. This means it’s a method for simulating events that cannot be modelled implicitly. Monte carlo simulation (or method). Monte Carlo Simulation Vs.

From towardsdatascience.com

Monte Carlo Simulation in R with focus on Option Pricing by Ojasvin Monte Carlo Simulation Vs The monte carlo method is a stochastic (random sampling of inputs) method to solve a statistical problem, and a simulation is a virtual representation of a problem. Simply put, monte carlo simulations provide a way to develop sequences of random market returns fitting predetermined characteristics, in order to test how financial. Monte carlo methods, or monte carlo experiments, are a. Monte Carlo Simulation Vs.

From quantpedia.com

Introduction and Examples of Monte Carlo Strategy Simulation QuantPedia Monte Carlo Simulation Vs This method uses random sampling. Monte carlo simulation (or method) is a probabilistic numerical technique used to estimate the outcome of a given, uncertain (stochastic) process. A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. Simply put, monte carlo simulations provide a way to. Monte Carlo Simulation Vs.

From www.digitalvidya.com

A Complete Guide To Monte Carlo Simulation For Machine Learners Monte Carlo Simulation Vs A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. This means it’s a method for simulating events that cannot be modelled implicitly. Monte carlo simulation (or method) is a. Monte Carlo Simulation Vs.

From resources.altium.com

Monte Carlo Simulation vs. Sensitivity Analysis Zach Peterson Monte Carlo Simulation Vs This method uses random sampling. A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. This means it’s a method for simulating events that cannot be modelled implicitly. Monte carlo simulation (or method) is a probabilistic numerical technique used to estimate the outcome of a. Monte Carlo Simulation Vs.

From www.projectcubicle.com

Monte Carlo Simulation Example and Solution Monte Carlo Simulation Vs A monte carlo simulation is a model used to predict the probability of a variety of outcomes when the potential for random variables is present. The monte carlo method is a stochastic (random sampling of inputs) method to solve a statistical problem, and a simulation is a virtual representation of a problem. Monte carlo methods, or monte carlo experiments, are. Monte Carlo Simulation Vs.

From www.researchgate.net

A Monte Carlo simulation Probabilistic sensitivity analysis CRTP vs Monte Carlo Simulation Vs What is monte carlo simulation? Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. This means it’s a method for simulating events that cannot be modelled implicitly. The monte carlo. Monte Carlo Simulation Vs.