Spread Duration Maturity . Spread duration is the sensitivity of a security’s price to changes in its credit spread. For risky bonds, duration is defined as sensitivity of price due to change in underlying yield while spread duration is sensitivity of. A yield spread is a difference between the quoted rate of return on different debt instruments which often have varying maturities, credit ratings, and risk. It is equal to the maturity if and only if the bond is a zero. It measures the difference between the duration. Duration spread is a key metric used by investors to manage interest rate risk. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. If i am evaluating a coporate bond with both treasury risk and credit spread risk, then duration is just the % change of the price. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. For a standard bond, the macaulay duration will be between 0 and the maturity of the bond.

from www.slideserve.com

It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Duration spread is a key metric used by investors to manage interest rate risk. Spread duration is the sensitivity of a security’s price to changes in its credit spread. For a standard bond, the macaulay duration will be between 0 and the maturity of the bond. A yield spread is a difference between the quoted rate of return on different debt instruments which often have varying maturities, credit ratings, and risk. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. It is equal to the maturity if and only if the bond is a zero. If i am evaluating a coporate bond with both treasury risk and credit spread risk, then duration is just the % change of the price. It measures the difference between the duration. For risky bonds, duration is defined as sensitivity of price due to change in underlying yield while spread duration is sensitivity of.

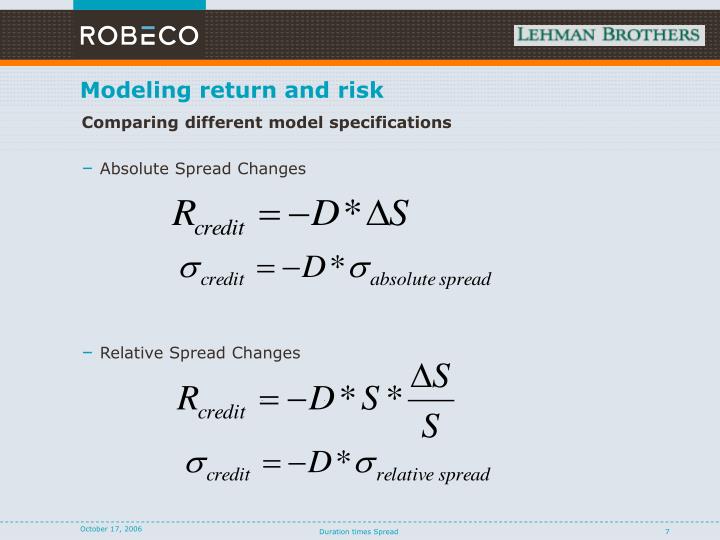

PPT Duration times spread PowerPoint Presentation ID3950949

Spread Duration Maturity For risky bonds, duration is defined as sensitivity of price due to change in underlying yield while spread duration is sensitivity of. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. If i am evaluating a coporate bond with both treasury risk and credit spread risk, then duration is just the % change of the price. A yield spread is a difference between the quoted rate of return on different debt instruments which often have varying maturities, credit ratings, and risk. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. For risky bonds, duration is defined as sensitivity of price due to change in underlying yield while spread duration is sensitivity of. Spread duration is the sensitivity of a security’s price to changes in its credit spread. It is equal to the maturity if and only if the bond is a zero. Duration spread is a key metric used by investors to manage interest rate risk. For a standard bond, the macaulay duration will be between 0 and the maturity of the bond. It measures the difference between the duration.

From ar.inspiredpencil.com

Yield To Maturity Spread Duration Maturity For a standard bond, the macaulay duration will be between 0 and the maturity of the bond. Duration spread is a key metric used by investors to manage interest rate risk. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. A yield spread is a difference between the. Spread Duration Maturity.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation, free download ID Spread Duration Maturity It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. Duration spread is a key metric used by investors to manage interest rate. Spread Duration Maturity.

From www.slideteam.net

Duration Maturity Yield In Powerpoint And Google Slides Cpb Spread Duration Maturity If i am evaluating a coporate bond with both treasury risk and credit spread risk, then duration is just the % change of the price. For a standard bond, the macaulay duration will be between 0 and the maturity of the bond. For risky bonds, duration is defined as sensitivity of price due to change in underlying yield while spread. Spread Duration Maturity.

From www.slideserve.com

PPT Bond Price Volatility PowerPoint Presentation ID159962 Spread Duration Maturity If i am evaluating a coporate bond with both treasury risk and credit spread risk, then duration is just the % change of the price. For a standard bond, the macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero. It quantifies the. Spread Duration Maturity.

From www.investopedia.com

Understanding Treasury Yield and Interest Rates Spread Duration Maturity For a standard bond, the macaulay duration will be between 0 and the maturity of the bond. It measures the difference between the duration. Duration spread is a key metric used by investors to manage interest rate risk. A yield spread is a difference between the quoted rate of return on different debt instruments which often have varying maturities, credit. Spread Duration Maturity.

From www.slideserve.com

PPT Chapter 6 PowerPoint Presentation, free download ID4021126 Spread Duration Maturity For risky bonds, duration is defined as sensitivity of price due to change in underlying yield while spread duration is sensitivity of. A yield spread is a difference between the quoted rate of return on different debt instruments which often have varying maturities, credit ratings, and risk. Spread duration is the sensitivity of a security’s price to changes in its. Spread Duration Maturity.

From helpfulprofessor.com

25 Maturity Examples (2024) Spread Duration Maturity It is equal to the maturity if and only if the bond is a zero. For a standard bond, the macaulay duration will be between 0 and the maturity of the bond. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. For risky bonds, duration is defined as. Spread Duration Maturity.

From www.researchgate.net

DurationMaturity Relationship Download Scientific Diagram Spread Duration Maturity It is equal to the maturity if and only if the bond is a zero. It measures the difference between the duration. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the. Spread Duration Maturity.

From www.nuveen.com

Duration a measure of bond price volatility Nuveen Spread Duration Maturity It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. It measures the difference between the duration. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. It is equal to the maturity. Spread Duration Maturity.

From analystprep.com

Credit Spread increasing with Longer Time to Maturity CFA, FRM, and Spread Duration Maturity For risky bonds, duration is defined as sensitivity of price due to change in underlying yield while spread duration is sensitivity of. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. It measures the difference between the duration. It quantifies the sensitivity of a bond’s price to credit. Spread Duration Maturity.

From www.slideserve.com

PPT Bond Portfolio Management PowerPoint Presentation, free download Spread Duration Maturity If i am evaluating a coporate bond with both treasury risk and credit spread risk, then duration is just the % change of the price. For a standard bond, the macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero. Duration spread is. Spread Duration Maturity.

From www.slideteam.net

Duration Maturity Relationship In Powerpoint And Google Slides Cpb PPT Spread Duration Maturity If i am evaluating a coporate bond with both treasury risk and credit spread risk, then duration is just the % change of the price. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. For risky bonds, duration is defined as sensitivity of. Spread Duration Maturity.

From www.erp-information.com

Digital Maturity Score (Examples, Levels, and Key elements) Spread Duration Maturity It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration is the sensitivity of a security’s price to changes in its credit spread. If i am evaluating a coporate bond with both treasury risk and credit spread risk, then duration is just. Spread Duration Maturity.

From www.slideserve.com

PPT CHAPTER 11 PowerPoint Presentation, free download ID1748907 Spread Duration Maturity Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. If i am evaluating a coporate bond with both treasury risk and credit spread risk, then duration is just the % change of the price. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors. Spread Duration Maturity.

From www.ejshin.org

Education Ultimate Fixed 101 What are Credit Spread, Spread Spread Duration Maturity It is equal to the maturity if and only if the bond is a zero. It measures the difference between the duration. Duration spread is a key metric used by investors to manage interest rate risk. For risky bonds, duration is defined as sensitivity of price due to change in underlying yield while spread duration is sensitivity of. It quantifies. Spread Duration Maturity.

From www.investopedia.com

Duration and Convexity to Measure Bond Risk Spread Duration Maturity It measures the difference between the duration. For a standard bond, the macaulay duration will be between 0 and the maturity of the bond. For risky bonds, duration is defined as sensitivity of price due to change in underlying yield while spread duration is sensitivity of. Spread duration is the sensitivity of a security’s price to changes in its credit. Spread Duration Maturity.

From www.slideteam.net

Difference Duration Maturity Ppt Powerpoint Presentation Ideas Master Spread Duration Maturity For a standard bond, the macaulay duration will be between 0 and the maturity of the bond. If i am evaluating a coporate bond with both treasury risk and credit spread risk, then duration is just the % change of the price. For risky bonds, duration is defined as sensitivity of price due to change in underlying yield while spread. Spread Duration Maturity.

From www.youtube.com

Bond maturity and duration YouTube Spread Duration Maturity For risky bonds, duration is defined as sensitivity of price due to change in underlying yield while spread duration is sensitivity of. A yield spread is a difference between the quoted rate of return on different debt instruments which often have varying maturities, credit ratings, and risk. Spread duration is the sensitivity of a security’s price to changes in its. Spread Duration Maturity.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation ID3950949 Spread Duration Maturity Spread duration is the sensitivity of a security’s price to changes in its credit spread. For a standard bond, the macaulay duration will be between 0 and the maturity of the bond. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration. Spread Duration Maturity.

From www.slideteam.net

Bond Duration Maturity In Powerpoint And Google Slides Cpb Spread Duration Maturity It measures the difference between the duration. For risky bonds, duration is defined as sensitivity of price due to change in underlying yield while spread duration is sensitivity of. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration is a measure. Spread Duration Maturity.

From www.investopedia.com

The Predictive Powers of the Bond Yield Curve Spread Duration Maturity Spread duration is the sensitivity of a security’s price to changes in its credit spread. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration is a measure of the percentage change in a bond’s price for a given change in its. Spread Duration Maturity.

From analystprep.com

Riding the Yield Curve CFA, FRM, and Actuarial Exams Study Notes Spread Duration Maturity It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. If i am evaluating a coporate bond with both treasury risk and credit spread risk, then duration is just the % change of the price. For a standard bond, the macaulay duration will be. Spread Duration Maturity.

From www.financestrategists.com

Duration vs Maturity Similarities, Differences, & When to Use Spread Duration Maturity It measures the difference between the duration. If i am evaluating a coporate bond with both treasury risk and credit spread risk, then duration is just the % change of the price. For a standard bond, the macaulay duration will be between 0 and the maturity of the bond. Spread duration is a measure of the percentage change in a. Spread Duration Maturity.

From transacted.io

Spread Duration Explained Transacted Spread Duration Maturity It measures the difference between the duration. It is equal to the maturity if and only if the bond is a zero. For risky bonds, duration is defined as sensitivity of price due to change in underlying yield while spread duration is sensitivity of. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate. Spread Duration Maturity.

From www.researchgate.net

Yield Spread across Maturity Segments before and after Policy Spread Duration Maturity It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Duration spread is a key metric used by investors to manage interest rate risk. If i am evaluating a coporate bond with both treasury risk and credit spread risk, then duration is just the. Spread Duration Maturity.

From www.westernsouthern.com

An Innovative Approach to Measuring Spread Risk Spread Duration Maturity Duration spread is a key metric used by investors to manage interest rate risk. A yield spread is a difference between the quoted rate of return on different debt instruments which often have varying maturities, credit ratings, and risk. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread.. Spread Duration Maturity.

From www.slideserve.com

PPT Subsovereign Credit Markets PowerPoint Presentation, free Spread Duration Maturity It measures the difference between the duration. For risky bonds, duration is defined as sensitivity of price due to change in underlying yield while spread duration is sensitivity of. A yield spread is a difference between the quoted rate of return on different debt instruments which often have varying maturities, credit ratings, and risk. Spread duration is a measure of. Spread Duration Maturity.

From www.youtube.com

Average Time to Maturity on a Fund Factsheet YouTube Spread Duration Maturity Spread duration is the sensitivity of a security’s price to changes in its credit spread. Duration spread is a key metric used by investors to manage interest rate risk. It is equal to the maturity if and only if the bond is a zero. If i am evaluating a coporate bond with both treasury risk and credit spread risk, then. Spread Duration Maturity.

From www.slideserve.com

PPT Fixed Markets Part 2 Duration and convexity PowerPoint Spread Duration Maturity Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. If i am evaluating a coporate bond with both treasury risk and credit. Spread Duration Maturity.

From www.westernsouthern.com

An Innovative Approach to Measuring Spread Risk Spread Duration Maturity It is equal to the maturity if and only if the bond is a zero. Duration spread is a key metric used by investors to manage interest rate risk. Spread duration is the sensitivity of a security’s price to changes in its credit spread. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate. Spread Duration Maturity.

From www.poems.com.sg

Maturity distribution What is it, Impact, Understanding, Model POEMS Spread Duration Maturity For a standard bond, the macaulay duration will be between 0 and the maturity of the bond. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration is the sensitivity of a security’s price to changes in its credit spread. It is. Spread Duration Maturity.

From sarahnewswebb.blogspot.com

Which of the Following Bonds Has the Greatest Price Risk Spread Duration Maturity For a standard bond, the macaulay duration will be between 0 and the maturity of the bond. Duration spread is a key metric used by investors to manage interest rate risk. A yield spread is a difference between the quoted rate of return on different debt instruments which often have varying maturities, credit ratings, and risk. For risky bonds, duration. Spread Duration Maturity.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation ID3950949 Spread Duration Maturity It is equal to the maturity if and only if the bond is a zero. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration is the sensitivity of a security’s price to changes in its credit spread. It measures the difference. Spread Duration Maturity.

From www.columbiathreadneedleus.com

Chart Two types of steepening yield curves Columbia Threadneedle Blog Spread Duration Maturity It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. It measures the difference between the duration. For a standard bond, the macaulay. Spread Duration Maturity.

From www.educba.com

Macaulay Duration Formula Example with Excel Template Spread Duration Maturity Duration spread is a key metric used by investors to manage interest rate risk. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration is the sensitivity of a security’s price to changes in its credit spread. For a standard bond, the. Spread Duration Maturity.