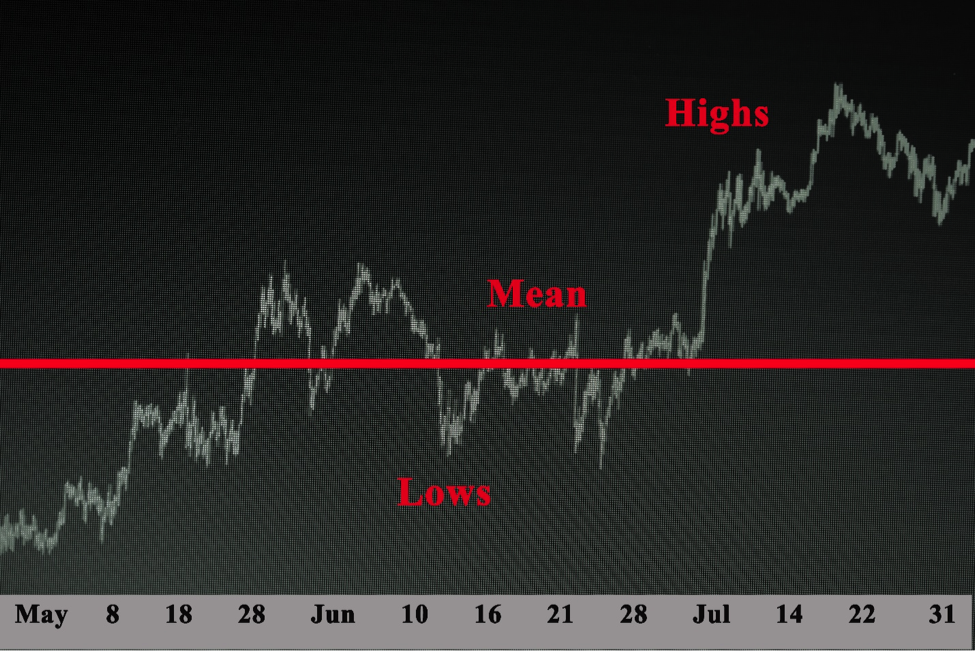

Testing For Mean Reversion . Can you use the variance ratio test to determine whether or not a time series is mean reverting? I'm using the lo.mac function in the vrtest library in r. In future articles we are going to consider full implementations of mean reverting trading strategies for daily equities and etfs data. In the case of mean reversion in time series, the stationarity test plays an integral role. In that article we looked at a couple of techniques that helped us determine whether a time. Structure function with lags 1 day to 2 yrs. A while back we began discussing statistical mean reversion testing. Spy is highly non stationary, as shown in the chart. In terms of two or more assets. The stationary test will help you analyse if. This equation is the key to test whether mean reversion really exists and then to make adjustments for mean reversion. This page explains how to you can use the research environment to develop and test a mean reversion hypothesis, then put the hypothesis in production.

from www.asiaforexmentor.com

In terms of two or more assets. This equation is the key to test whether mean reversion really exists and then to make adjustments for mean reversion. In that article we looked at a couple of techniques that helped us determine whether a time. Spy is highly non stationary, as shown in the chart. In future articles we are going to consider full implementations of mean reverting trading strategies for daily equities and etfs data. Can you use the variance ratio test to determine whether or not a time series is mean reverting? I'm using the lo.mac function in the vrtest library in r. This page explains how to you can use the research environment to develop and test a mean reversion hypothesis, then put the hypothesis in production. The stationary test will help you analyse if. In the case of mean reversion in time series, the stationarity test plays an integral role.

Mean Reversion A Complete Guide • Asia Forex Mentor

Testing For Mean Reversion In that article we looked at a couple of techniques that helped us determine whether a time. Structure function with lags 1 day to 2 yrs. In that article we looked at a couple of techniques that helped us determine whether a time. Spy is highly non stationary, as shown in the chart. I'm using the lo.mac function in the vrtest library in r. The stationary test will help you analyse if. In the case of mean reversion in time series, the stationarity test plays an integral role. A while back we began discussing statistical mean reversion testing. Can you use the variance ratio test to determine whether or not a time series is mean reverting? This equation is the key to test whether mean reversion really exists and then to make adjustments for mean reversion. This page explains how to you can use the research environment to develop and test a mean reversion hypothesis, then put the hypothesis in production. In terms of two or more assets. In future articles we are going to consider full implementations of mean reverting trading strategies for daily equities and etfs data.

From efinancemanagement.com

Mean Reversion Meaning, Indicators & Strategies eFM Testing For Mean Reversion Spy is highly non stationary, as shown in the chart. Structure function with lags 1 day to 2 yrs. In the case of mean reversion in time series, the stationarity test plays an integral role. I'm using the lo.mac function in the vrtest library in r. Can you use the variance ratio test to determine whether or not a time. Testing For Mean Reversion.

From www.tradinformed.com

A Simple RSI Mean Reversion Strategy Tradinformed Testing For Mean Reversion Can you use the variance ratio test to determine whether or not a time series is mean reverting? This equation is the key to test whether mean reversion really exists and then to make adjustments for mean reversion. I'm using the lo.mac function in the vrtest library in r. Spy is highly non stationary, as shown in the chart. Structure. Testing For Mean Reversion.

From dailypriceaction.com

Mean Reversion A Guide To Market Timing Daily Price Action Testing For Mean Reversion In the case of mean reversion in time series, the stationarity test plays an integral role. I'm using the lo.mac function in the vrtest library in r. This page explains how to you can use the research environment to develop and test a mean reversion hypothesis, then put the hypothesis in production. Spy is highly non stationary, as shown in. Testing For Mean Reversion.

From www.researchgate.net

Results of Mean Reversion "Classical Unit root Test" and Powerful Testing For Mean Reversion In that article we looked at a couple of techniques that helped us determine whether a time. Can you use the variance ratio test to determine whether or not a time series is mean reverting? In terms of two or more assets. In the case of mean reversion in time series, the stationarity test plays an integral role. The stationary. Testing For Mean Reversion.

From www.youtube.com

Mean Reversion Strategy Intraday technique for beginners YouTube Testing For Mean Reversion Structure function with lags 1 day to 2 yrs. In terms of two or more assets. Spy is highly non stationary, as shown in the chart. This equation is the key to test whether mean reversion really exists and then to make adjustments for mean reversion. Can you use the variance ratio test to determine whether or not a time. Testing For Mean Reversion.

From www.researchgate.net

Panel Mean Reversion Test Results Download Table Testing For Mean Reversion In the case of mean reversion in time series, the stationarity test plays an integral role. Can you use the variance ratio test to determine whether or not a time series is mean reverting? This page explains how to you can use the research environment to develop and test a mean reversion hypothesis, then put the hypothesis in production. A. Testing For Mean Reversion.

From www.tradingview.com

Meanreversion — Indicators and Signals — TradingView Testing For Mean Reversion In future articles we are going to consider full implementations of mean reverting trading strategies for daily equities and etfs data. Can you use the variance ratio test to determine whether or not a time series is mean reverting? This page explains how to you can use the research environment to develop and test a mean reversion hypothesis, then put. Testing For Mean Reversion.

From enlightenedstocktrading.com

Mean Reversion Trading The Ultimate Strategy Guide! Testing For Mean Reversion Structure function with lags 1 day to 2 yrs. In that article we looked at a couple of techniques that helped us determine whether a time. In the case of mean reversion in time series, the stationarity test plays an integral role. This equation is the key to test whether mean reversion really exists and then to make adjustments for. Testing For Mean Reversion.

From www.youtube.com

Mean Reversion Trading Secrets HOW TO IDENTIFY HIGH PROBABILITY Testing For Mean Reversion I'm using the lo.mac function in the vrtest library in r. In the case of mean reversion in time series, the stationarity test plays an integral role. The stationary test will help you analyse if. This equation is the key to test whether mean reversion really exists and then to make adjustments for mean reversion. Can you use the variance. Testing For Mean Reversion.

From www.theinvestorspodcast.com

What Mean Reversion Is, and How to Invest Using It Testing For Mean Reversion In that article we looked at a couple of techniques that helped us determine whether a time. Can you use the variance ratio test to determine whether or not a time series is mean reverting? This page explains how to you can use the research environment to develop and test a mean reversion hypothesis, then put the hypothesis in production.. Testing For Mean Reversion.

From miltonfmr.com

Mean Reversion Trading System Testing For Mean Reversion In the case of mean reversion in time series, the stationarity test plays an integral role. Structure function with lags 1 day to 2 yrs. The stationary test will help you analyse if. In future articles we are going to consider full implementations of mean reverting trading strategies for daily equities and etfs data. In terms of two or more. Testing For Mean Reversion.

From in.tradingview.com

Meanreversion — Indicators and Signals — TradingView — India Testing For Mean Reversion In that article we looked at a couple of techniques that helped us determine whether a time. This page explains how to you can use the research environment to develop and test a mean reversion hypothesis, then put the hypothesis in production. A while back we began discussing statistical mean reversion testing. Can you use the variance ratio test to. Testing For Mean Reversion.

From analystprep.com

The Mean Reversion CFA, FRM, and Actuarial Exams Study Notes Testing For Mean Reversion Structure function with lags 1 day to 2 yrs. This page explains how to you can use the research environment to develop and test a mean reversion hypothesis, then put the hypothesis in production. In that article we looked at a couple of techniques that helped us determine whether a time. In terms of two or more assets. Can you. Testing For Mean Reversion.

From tradingstrategyguides.com

Mean Reversion Trading Strategy With A Sneaky Secret Testing For Mean Reversion Structure function with lags 1 day to 2 yrs. Spy is highly non stationary, as shown in the chart. Can you use the variance ratio test to determine whether or not a time series is mean reverting? The stationary test will help you analyse if. In terms of two or more assets. In future articles we are going to consider. Testing For Mean Reversion.

From tradersbulletin.co.uk

Trend vs Mean Reversion trend following and mean reversion) Testing For Mean Reversion In that article we looked at a couple of techniques that helped us determine whether a time. In future articles we are going to consider full implementations of mean reverting trading strategies for daily equities and etfs data. I'm using the lo.mac function in the vrtest library in r. Spy is highly non stationary, as shown in the chart. Structure. Testing For Mean Reversion.

From www.researchgate.net

Panel Test for industrial Mean reversion Download Table Testing For Mean Reversion The stationary test will help you analyse if. In terms of two or more assets. I'm using the lo.mac function in the vrtest library in r. Can you use the variance ratio test to determine whether or not a time series is mean reverting? This page explains how to you can use the research environment to develop and test a. Testing For Mean Reversion.

From blog.roboforex.com

Mean Reversion Trading Strategy Mean Reversion Channel Indicator Testing For Mean Reversion The stationary test will help you analyse if. In terms of two or more assets. A while back we began discussing statistical mean reversion testing. I'm using the lo.mac function in the vrtest library in r. This page explains how to you can use the research environment to develop and test a mean reversion hypothesis, then put the hypothesis in. Testing For Mean Reversion.

From www.researchgate.net

The results of Mean Reversion process Download Scientific Diagram Testing For Mean Reversion The stationary test will help you analyse if. In the case of mean reversion in time series, the stationarity test plays an integral role. Can you use the variance ratio test to determine whether or not a time series is mean reverting? In that article we looked at a couple of techniques that helped us determine whether a time. A. Testing For Mean Reversion.

From tradeciety.com

An Introduction To Mean Reversion Trading And The 4 Biggest Challenges Testing For Mean Reversion A while back we began discussing statistical mean reversion testing. I'm using the lo.mac function in the vrtest library in r. Can you use the variance ratio test to determine whether or not a time series is mean reverting? This equation is the key to test whether mean reversion really exists and then to make adjustments for mean reversion. In. Testing For Mean Reversion.

From www.tradinformed.com

A Simple RSI Mean Reversion Strategy Tradinformed Testing For Mean Reversion The stationary test will help you analyse if. This page explains how to you can use the research environment to develop and test a mean reversion hypothesis, then put the hypothesis in production. In future articles we are going to consider full implementations of mean reverting trading strategies for daily equities and etfs data. In terms of two or more. Testing For Mean Reversion.

From www.youtube.com

Mean Reversion Trading Strategy Clearly Explained! YouTube Testing For Mean Reversion This equation is the key to test whether mean reversion really exists and then to make adjustments for mean reversion. Structure function with lags 1 day to 2 yrs. In future articles we are going to consider full implementations of mean reverting trading strategies for daily equities and etfs data. I'm using the lo.mac function in the vrtest library in. Testing For Mean Reversion.

From www.asiaforexmentor.com

Mean Reversion A Complete Guide • Asia Forex Mentor Testing For Mean Reversion Structure function with lags 1 day to 2 yrs. Can you use the variance ratio test to determine whether or not a time series is mean reverting? This equation is the key to test whether mean reversion really exists and then to make adjustments for mean reversion. A while back we began discussing statistical mean reversion testing. The stationary test. Testing For Mean Reversion.

From www.tradingview.com

Meanreversion — Indicators and Signals — TradingView Testing For Mean Reversion I'm using the lo.mac function in the vrtest library in r. The stationary test will help you analyse if. In that article we looked at a couple of techniques that helped us determine whether a time. This equation is the key to test whether mean reversion really exists and then to make adjustments for mean reversion. In future articles we. Testing For Mean Reversion.

From indicatorspot.com

Mean Reversion Indicator for MT4 Download FREE IndicatorsPot Testing For Mean Reversion The stationary test will help you analyse if. I'm using the lo.mac function in the vrtest library in r. In terms of two or more assets. This equation is the key to test whether mean reversion really exists and then to make adjustments for mean reversion. This page explains how to you can use the research environment to develop and. Testing For Mean Reversion.

From indicatorspot.com

Mean Reversion Indicator for MT5 Download FREE IndicatorsPot Testing For Mean Reversion I'm using the lo.mac function in the vrtest library in r. This page explains how to you can use the research environment to develop and test a mean reversion hypothesis, then put the hypothesis in production. In terms of two or more assets. Spy is highly non stationary, as shown in the chart. In the case of mean reversion in. Testing For Mean Reversion.

From www.youtube.com

How to use the Bollinger Bands. Mean Reversion Strategy! YouTube Testing For Mean Reversion A while back we began discussing statistical mean reversion testing. Structure function with lags 1 day to 2 yrs. In the case of mean reversion in time series, the stationarity test plays an integral role. Can you use the variance ratio test to determine whether or not a time series is mean reverting? In future articles we are going to. Testing For Mean Reversion.

From www.tradingsim.com

Mean Reversion Trading Strategies Explained TradingSim Testing For Mean Reversion In that article we looked at a couple of techniques that helped us determine whether a time. I'm using the lo.mac function in the vrtest library in r. A while back we began discussing statistical mean reversion testing. This equation is the key to test whether mean reversion really exists and then to make adjustments for mean reversion. In the. Testing For Mean Reversion.

From tradeciety.com

An Introduction To Mean Reversion Trading And The 4 Biggest Challenges Testing For Mean Reversion I'm using the lo.mac function in the vrtest library in r. This page explains how to you can use the research environment to develop and test a mean reversion hypothesis, then put the hypothesis in production. The stationary test will help you analyse if. Spy is highly non stationary, as shown in the chart. A while back we began discussing. Testing For Mean Reversion.

From theforexgeek.com

Mean Reversion Indicator The Forex Geek Testing For Mean Reversion This page explains how to you can use the research environment to develop and test a mean reversion hypothesis, then put the hypothesis in production. In that article we looked at a couple of techniques that helped us determine whether a time. Can you use the variance ratio test to determine whether or not a time series is mean reverting?. Testing For Mean Reversion.

From www.tradingsim.com

Mean Reversion Trading Strategies Explained TradingSim Testing For Mean Reversion This equation is the key to test whether mean reversion really exists and then to make adjustments for mean reversion. Can you use the variance ratio test to determine whether or not a time series is mean reverting? In terms of two or more assets. Spy is highly non stationary, as shown in the chart. This page explains how to. Testing For Mean Reversion.

From learnpriceaction.com

Mean Reversion Trading Strategy With Free PDF Testing For Mean Reversion A while back we began discussing statistical mean reversion testing. Structure function with lags 1 day to 2 yrs. In future articles we are going to consider full implementations of mean reverting trading strategies for daily equities and etfs data. In terms of two or more assets. This page explains how to you can use the research environment to develop. Testing For Mean Reversion.

From dailypriceaction.com

Mean Reversion A Guide To Market Timing Daily Price Action Testing For Mean Reversion This equation is the key to test whether mean reversion really exists and then to make adjustments for mean reversion. Structure function with lags 1 day to 2 yrs. In terms of two or more assets. In future articles we are going to consider full implementations of mean reverting trading strategies for daily equities and etfs data. In the case. Testing For Mean Reversion.

From forextraininggroup.com

Finding An Edge With Mean Reversion Trading Strategies Forex Training Testing For Mean Reversion Structure function with lags 1 day to 2 yrs. Spy is highly non stationary, as shown in the chart. In terms of two or more assets. This page explains how to you can use the research environment to develop and test a mean reversion hypothesis, then put the hypothesis in production. The stationary test will help you analyse if. In. Testing For Mean Reversion.

From optionalpha.com

Mean Reversion Reverting to the Mean Option Alpha Testing For Mean Reversion In that article we looked at a couple of techniques that helped us determine whether a time. Structure function with lags 1 day to 2 yrs. The stationary test will help you analyse if. In terms of two or more assets. Can you use the variance ratio test to determine whether or not a time series is mean reverting? This. Testing For Mean Reversion.

From quantconnectscripts.com

Understanding Mean Reversion Trading Testing For Mean Reversion This page explains how to you can use the research environment to develop and test a mean reversion hypothesis, then put the hypothesis in production. In future articles we are going to consider full implementations of mean reverting trading strategies for daily equities and etfs data. A while back we began discussing statistical mean reversion testing. In the case of. Testing For Mean Reversion.