Balancing Charge Deferred Tax . (1) taxable temporary differences that will. as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to. a deferred tax liability (dtl) or deferred tax asset (dta) is created when there are temporary differences between book (ifrs, gaap) tax and. There are two categories of temporary differences: this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to. when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing. under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. this $600k deferred tax will be charged to the income statement, increasing our deferred tax liability on the balance.

from habitwinner15.gitlab.io

(1) taxable temporary differences that will. under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to. this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to. this $600k deferred tax will be charged to the income statement, increasing our deferred tax liability on the balance. when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing. a deferred tax liability (dtl) or deferred tax asset (dta) is created when there are temporary differences between book (ifrs, gaap) tax and. There are two categories of temporary differences:

Impressive Ifrs 16 Deferred Tax Example Accounting Balance Sheet Sample

Balancing Charge Deferred Tax under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. a deferred tax liability (dtl) or deferred tax asset (dta) is created when there are temporary differences between book (ifrs, gaap) tax and. (1) taxable temporary differences that will. this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to. this $600k deferred tax will be charged to the income statement, increasing our deferred tax liability on the balance. when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing. There are two categories of temporary differences: as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to.

From patientcelery.substack.com

deferred tax asset and liability by Ngan Ha Balancing Charge Deferred Tax a deferred tax liability (dtl) or deferred tax asset (dta) is created when there are temporary differences between book (ifrs, gaap) tax and. under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. as ias 12 considers deferred tax from the perspective of temporary differences. Balancing Charge Deferred Tax.

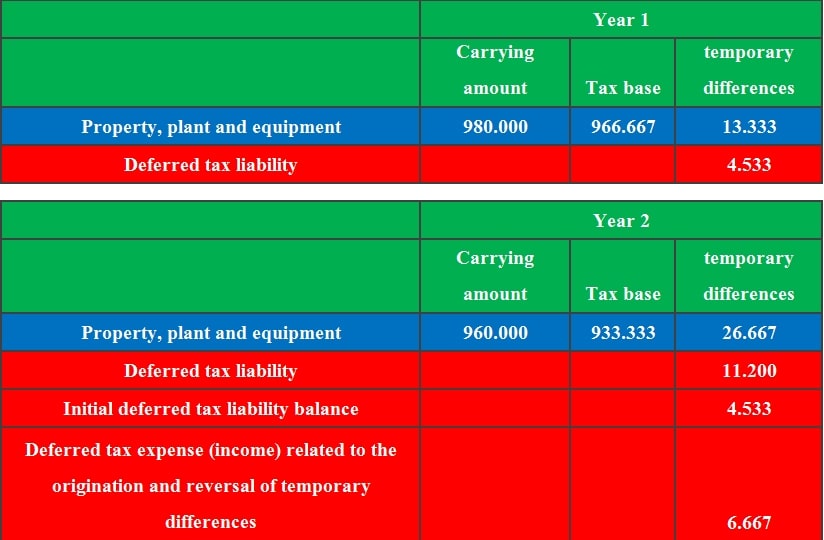

From studylib.net

Explanation of Deferred Tax Expense and Benefits The amount of Balancing Charge Deferred Tax a deferred tax liability (dtl) or deferred tax asset (dta) is created when there are temporary differences between book (ifrs, gaap) tax and. There are two categories of temporary differences: as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said. Balancing Charge Deferred Tax.

From slideplayer.com

Topic 8 Taxation IAS 12 tax 1) Current tax ppt download Balancing Charge Deferred Tax There are two categories of temporary differences: as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to. when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing.. Balancing Charge Deferred Tax.

From www.investopedia.com

Deferred Tax Asset Calculation, Uses, and Examples Balancing Charge Deferred Tax There are two categories of temporary differences: as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to. when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing.. Balancing Charge Deferred Tax.

From tradesmartonline.in

What Is Deferred Tax? Types & Methods to Calculate TradeSmart Balancing Charge Deferred Tax under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. There are two categories of temporary differences: when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing. a deferred tax liability (dtl) or. Balancing Charge Deferred Tax.

From www.youtube.com

Terminal Depreciation & Balancing Charge in PGBP in Tax How to calculate terminal Balancing Charge Deferred Tax as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to. a deferred tax liability (dtl) or deferred tax asset (dta) is created when there are temporary differences between book (ifrs, gaap) tax and. There are two categories of temporary. Balancing Charge Deferred Tax.

From einvestingforbeginners.com

Deferred Tax Liabilities Explained (with RealLife Example in a 10k) Balancing Charge Deferred Tax (1) taxable temporary differences that will. when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing. There are two categories of temporary differences: under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. . Balancing Charge Deferred Tax.

From saxafund.org

Deferred Tax Asset Calculation Uses and Examples SAXA fund Balancing Charge Deferred Tax under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. (1) taxable temporary differences that will. when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing. this $600k deferred tax will be charged. Balancing Charge Deferred Tax.

From www.investmentguide.co.uk

Understanding Deferred Tax A Comprehensive Guide 2024 Balancing Charge Deferred Tax this $600k deferred tax will be charged to the income statement, increasing our deferred tax liability on the balance. a deferred tax liability (dtl) or deferred tax asset (dta) is created when there are temporary differences between book (ifrs, gaap) tax and. as ias 12 considers deferred tax from the perspective of temporary differences between the carrying. Balancing Charge Deferred Tax.

From sheetbalance.canariasgestalt.com

Deferred Tax Assets And Liabilities Examples Balance Sheet Format Vertical Sheet Balance Balancing Charge Deferred Tax as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to. under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. There are two categories of temporary differences:. Balancing Charge Deferred Tax.

From corporatefinanceinstitute.com

Deferred Tax Liability (or Asset) How It's Created in Accounting Balancing Charge Deferred Tax under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. (1) taxable temporary differences that will. when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing. There are two categories of temporary differences: . Balancing Charge Deferred Tax.

From www.investopedia.com

Deferred Tax Definition, Purpose, and Examples Balancing Charge Deferred Tax under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. (1) taxable temporary differences that will. this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to. a deferred tax liability (dtl) or deferred tax asset (dta). Balancing Charge Deferred Tax.

From www.investopedia.com

Deferred Tax Asset What It Is and How to Calculate and Use It, With Examples Balancing Charge Deferred Tax when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing. (1) taxable temporary differences that will. under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. this guide summarises the approach to calculating. Balancing Charge Deferred Tax.

From www.scribd.com

41 Balance Sheet Deferred Tax Expense Balancing Charge Deferred Tax this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to. There are two categories of temporary differences: when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing. as ias 12 considers deferred tax from the perspective. Balancing Charge Deferred Tax.

From www.youtube.com

Deferred Tax Explained with Example Profit & Loss approach and Balance Sheet Approach Balancing Charge Deferred Tax under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to. when a fixed asset is sold, converted to trading stock or written off, you need to. Balancing Charge Deferred Tax.

From accountsexamples.com

IAS 12 paras 81(c), 81(g) tax reconciliation and deferred tax balances with detailed explanatory Balancing Charge Deferred Tax (1) taxable temporary differences that will. under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing. There are two categories of temporary differences: . Balancing Charge Deferred Tax.

From www.financialmodellinghandbook.org

What is deferred tax and how to model it Balancing Charge Deferred Tax There are two categories of temporary differences: as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to. (1) taxable temporary differences that will. when a fixed asset is sold, converted to trading stock or written off, you need to. Balancing Charge Deferred Tax.

From khatabook.com

Learn About Deferred Tax Asset & Deferred Tax Liability Meaning How Deferred Tax Is Classified Balancing Charge Deferred Tax as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to. (1) taxable temporary differences that will. There are two categories of temporary differences: this $600k deferred tax will be charged to the income statement, increasing our deferred tax liability. Balancing Charge Deferred Tax.

From ag.purdue.edu

Computation of Deferred Tax Liabilities Center for Commercial Agriculture Balancing Charge Deferred Tax under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. this $600k deferred tax will be charged to the income statement, increasing our deferred tax liability on the balance. as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount. Balancing Charge Deferred Tax.

From www.investopedia.com

Deferred Tax Asset Calculation, Uses, and Examples Balancing Charge Deferred Tax this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to. when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing. a deferred tax liability (dtl) or deferred tax asset (dta) is created when there are temporary. Balancing Charge Deferred Tax.

From verkana.robtowner.com

Deferred Tax Asset Journal Entry Example Balance Sheet Verkanarobtowner Balancing Charge Deferred Tax when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing. (1) taxable temporary differences that will. a deferred tax liability (dtl) or deferred tax asset (dta) is created when there are temporary differences between book (ifrs, gaap) tax and. this $600k deferred tax will be. Balancing Charge Deferred Tax.

From ag.purdue.edu

Computation of Deferred Tax Liabilities Center for Commercial Agriculture Balancing Charge Deferred Tax as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to. this $600k deferred tax will be charged to the income statement, increasing our deferred tax liability on the balance. a deferred tax liability (dtl) or deferred tax asset. Balancing Charge Deferred Tax.

From www.slideserve.com

PPT Deferred Tax Examples PowerPoint Presentation, free download ID3506718 Balancing Charge Deferred Tax (1) taxable temporary differences that will. this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to. under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. when a fixed asset is sold, converted to trading stock. Balancing Charge Deferred Tax.

From slideplayer.com

Group International Taxation ppt download Balancing Charge Deferred Tax (1) taxable temporary differences that will. this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to. this $600k deferred tax will be charged to the income statement, increasing our deferred tax liability on the balance. a deferred tax liability (dtl) or deferred tax asset (dta) is created when. Balancing Charge Deferred Tax.

From www.hkcne.com

Press Release Balancing Charge Deferred Tax this $600k deferred tax will be charged to the income statement, increasing our deferred tax liability on the balance. a deferred tax liability (dtl) or deferred tax asset (dta) is created when there are temporary differences between book (ifrs, gaap) tax and. as ias 12 considers deferred tax from the perspective of temporary differences between the carrying. Balancing Charge Deferred Tax.

From www.financialmodellinghandbook.org

What is deferred tax and how to model it Balancing Charge Deferred Tax as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to. There are two categories of temporary differences: under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities.. Balancing Charge Deferred Tax.

From www.investopedia.com

Deferred Tax Liability Definition How It Works With Examples Balancing Charge Deferred Tax under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to. There are two categories of temporary differences: as ias 12 considers deferred tax from the perspective. Balancing Charge Deferred Tax.

From www.investopedia.com

Deferred Charge What it is, How it Works, Example Balancing Charge Deferred Tax There are two categories of temporary differences: this $600k deferred tax will be charged to the income statement, increasing our deferred tax liability on the balance. a deferred tax liability (dtl) or deferred tax asset (dta) is created when there are temporary differences between book (ifrs, gaap) tax and. this guide summarises the approach to calculating a. Balancing Charge Deferred Tax.

From habitwinner15.gitlab.io

Impressive Ifrs 16 Deferred Tax Example Accounting Balance Sheet Sample Balancing Charge Deferred Tax There are two categories of temporary differences: this $600k deferred tax will be charged to the income statement, increasing our deferred tax liability on the balance. as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to. a deferred. Balancing Charge Deferred Tax.

From www.slideserve.com

PPT Accounting for Taxes PowerPoint Presentation, free download ID6808959 Balancing Charge Deferred Tax a deferred tax liability (dtl) or deferred tax asset (dta) is created when there are temporary differences between book (ifrs, gaap) tax and. as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to. (1) taxable temporary differences that will.. Balancing Charge Deferred Tax.

From analystprep.com

Valuation Allowance for Deferred Tax Assets CFA Level 1 AnalystPrep Balancing Charge Deferred Tax under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. this $600k deferred tax will be charged to the income statement, increasing our deferred tax liability on the balance. this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge. Balancing Charge Deferred Tax.

From exouhvmie.blob.core.windows.net

Balancing Charge Def at Tracy Lewis blog Balancing Charge Deferred Tax this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to. this $600k deferred tax will be charged to the income statement, increasing our deferred tax liability on the balance. (1) taxable temporary differences that will. when a fixed asset is sold, converted to trading stock or written off,. Balancing Charge Deferred Tax.

From www.footnotesanalyst.com

Worked example accounting for deferred tax assets The Footnotes Analyst Balancing Charge Deferred Tax this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to. as ias 12 considers deferred tax from the perspective of temporary differences between the carrying amount and tax base of assets and liabilities, the standard can be said to. this $600k deferred tax will be charged to the. Balancing Charge Deferred Tax.

From www.educba.com

Deferred Tax Deferred Tax in Accounting Standards Balancing Charge Deferred Tax (1) taxable temporary differences that will. this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to. There are two categories of temporary differences: when a fixed asset is sold, converted to trading stock or written off, you need to calculate balancing allowance (ba) or balancing. a deferred tax. Balancing Charge Deferred Tax.

From www.youtube.com

Deferred Taxes The Basics YouTube Balancing Charge Deferred Tax under ias 12, deferred tax is calculated on a temporary difference approach, which focuses on the book values of assets and liabilities. (1) taxable temporary differences that will. There are two categories of temporary differences: this guide summarises the approach to calculating a deferred tax balance, allocating the deferred tax charge or credit to. this $600k deferred. Balancing Charge Deferred Tax.