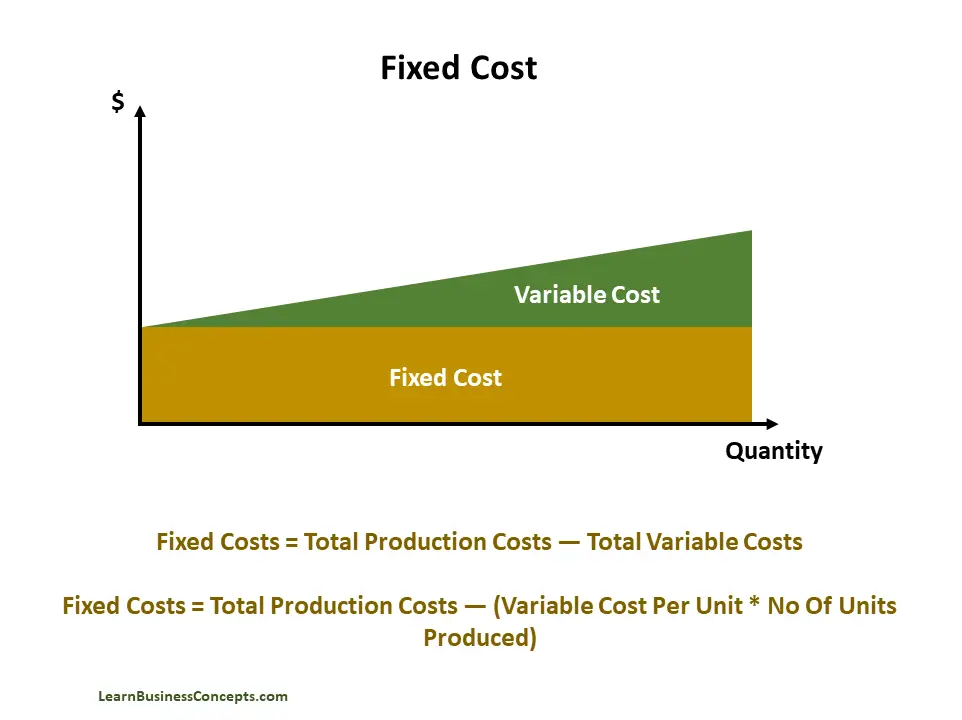

Fixed Cost Formula Microeconomics . There are seven cost curves in the short run: Total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. Whether you produce a lot or a little, the fixed costs are the same. Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. They are incurred regardless of how much a business produces. Fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. Total revenue = price × quantity. These costs are measured in. Examples of fixed costs include rent,. Fixed costs are expenses that do not change with the level of production or output. We calculate it by multiplying the price of the product times the quantity of output sold:

from learnbusinessconcepts.com

These costs are measured in. Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. Total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. Fixed costs are expenses that do not change with the level of production or output. We calculate it by multiplying the price of the product times the quantity of output sold: They are incurred regardless of how much a business produces. Whether you produce a lot or a little, the fixed costs are the same. There are seven cost curves in the short run: Fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. Examples of fixed costs include rent,.

Fixed Cost Explanation, Formula, Calculation, and Examples

Fixed Cost Formula Microeconomics They are incurred regardless of how much a business produces. We calculate it by multiplying the price of the product times the quantity of output sold: Whether you produce a lot or a little, the fixed costs are the same. Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. They are incurred regardless of how much a business produces. Fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. Total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. Total revenue = price × quantity. Examples of fixed costs include rent,. These costs are measured in. There are seven cost curves in the short run: Fixed costs are expenses that do not change with the level of production or output.

From penpoin.com

Total Variable Cost Examples, Curve, Importance Fixed Cost Formula Microeconomics We calculate it by multiplying the price of the product times the quantity of output sold: Examples of fixed costs include rent,. Fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. Fixed costs are expenses that do not change with the level of production or output. These costs. Fixed Cost Formula Microeconomics.

From www.youtube.com

C.1 Fixed and variable costs Cost Microeconomics YouTube Fixed Cost Formula Microeconomics There are seven cost curves in the short run: Whether you produce a lot or a little, the fixed costs are the same. We calculate it by multiplying the price of the product times the quantity of output sold: Fixed costs are expenses that do not change with the level of production or output. Fixed cost, variable cost, total cost,. Fixed Cost Formula Microeconomics.

From www.educba.com

Average Fixed Cost Formula Step by Step Solutions (Calculator) Fixed Cost Formula Microeconomics We calculate it by multiplying the price of the product times the quantity of output sold: Fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. There are seven cost curves in the short run: These costs are measured in. Examples of fixed costs include rent,. Whether you produce. Fixed Cost Formula Microeconomics.

From www.pcecon.com

Key Formula Sheet for Microeconomics Fixed Cost Formula Microeconomics These costs are measured in. Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. Whether you produce a lot or a little, the fixed costs are the same. They are incurred regardless of how much a business produces. Total cost, fixed cost, and variable cost each reflect different aspects of the. Fixed Cost Formula Microeconomics.

From ecampusontario.pressbooks.pub

8.5 Economic Loss and Shut Down in the Short Run Principles of Fixed Cost Formula Microeconomics Fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. We calculate it by multiplying the price of the product times the quantity of output sold: They are incurred regardless of how much a business produces. Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average. Fixed Cost Formula Microeconomics.

From ar.inspiredpencil.com

Average Total Cost Formula Fixed Cost Formula Microeconomics Examples of fixed costs include rent,. Whether you produce a lot or a little, the fixed costs are the same. There are seven cost curves in the short run: Fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. Total cost, fixed cost, and variable cost each reflect different. Fixed Cost Formula Microeconomics.

From psu.pb.unizin.org

6.4 Cost Behavior Financial and Managerial Accounting Fixed Cost Formula Microeconomics We calculate it by multiplying the price of the product times the quantity of output sold: Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. These costs are measured in. Examples of fixed costs include rent,. Total cost, fixed cost, and variable cost each reflect different aspects of the cost of. Fixed Cost Formula Microeconomics.

From www.vrogue.co

Cost Plus Pricing Konsep Formula Cara Menghitung Pro vrogue.co Fixed Cost Formula Microeconomics Fixed costs are expenses that do not change with the level of production or output. Examples of fixed costs include rent,. They are incurred regardless of how much a business produces. Whether you produce a lot or a little, the fixed costs are the same. Total revenue = price × quantity. There are seven cost curves in the short run:. Fixed Cost Formula Microeconomics.

From www.microeconomicsap.com

Combining factor inputs AP Microeconomics AP MICROECONOMICS Fixed Cost Formula Microeconomics Examples of fixed costs include rent,. We calculate it by multiplying the price of the product times the quantity of output sold: There are seven cost curves in the short run: These costs are measured in. Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. They are incurred regardless of how. Fixed Cost Formula Microeconomics.

From thestudyeconomics.blogspot.com

The Study Economics for ma ignou Microeconomics macroeconomics Fixed Cost Formula Microeconomics Fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. They are incurred regardless of how much a business produces. Fixed costs are expenses that do not change with the level of production or output. There are seven cost curves in the short run: Whether you produce a lot. Fixed Cost Formula Microeconomics.

From www.slideshare.net

Microeconomics Cost Functions Fixed Cost Formula Microeconomics Total revenue = price × quantity. Whether you produce a lot or a little, the fixed costs are the same. Examples of fixed costs include rent,. Fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. There are seven cost curves in the short run: Total cost, fixed cost,. Fixed Cost Formula Microeconomics.

From www.geeksforgeeks.org

What is Total Cost ? Formula, Example and Graph Fixed Cost Formula Microeconomics Total revenue = price × quantity. Examples of fixed costs include rent,. Fixed costs are expenses that do not change with the level of production or output. Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. These costs are measured in. Whether you produce a lot or a little, the fixed. Fixed Cost Formula Microeconomics.

From www.youtube.com

Fixed Cost Vs Variable Cost Difference Between them with Example Fixed Cost Formula Microeconomics Examples of fixed costs include rent,. We calculate it by multiplying the price of the product times the quantity of output sold: They are incurred regardless of how much a business produces. Whether you produce a lot or a little, the fixed costs are the same. There are seven cost curves in the short run: Fixed costs are expenses that. Fixed Cost Formula Microeconomics.

From pdfeports728.web.fc2.com

How do you work out the Variable cost? Fixed Cost Formula Microeconomics We calculate it by multiplying the price of the product times the quantity of output sold: Total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. Fixed costs are expenditures that do not change regardless of the level of production, at least not in the short. Fixed Cost Formula Microeconomics.

From www.coursehero.com

[Solved] Fill in the missing values for total fixed cost, total Fixed Cost Formula Microeconomics Total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. These costs are measured in. Whether you produce a lot or a little, the fixed costs are the same. Total revenue = price × quantity. There are seven cost curves in the short run: Fixed costs. Fixed Cost Formula Microeconomics.

From ar.inspiredpencil.com

Marginal Cost Formula Fixed Cost Formula Microeconomics Whether you produce a lot or a little, the fixed costs are the same. There are seven cost curves in the short run: Total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. Fixed costs are expenses that do not change with the level of production. Fixed Cost Formula Microeconomics.

From www.educba.com

Fixed Cost Formula Calculator (Examples with Excel Template) Fixed Cost Formula Microeconomics There are seven cost curves in the short run: Total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. Fixed costs are expenses that do not change with the level of production or output. We calculate it by multiplying the price of the product times the. Fixed Cost Formula Microeconomics.

From www.tutor2u.net

Explaining Fixed and Variable Costs of Production tutor2u Economics Fixed Cost Formula Microeconomics We calculate it by multiplying the price of the product times the quantity of output sold: They are incurred regardless of how much a business produces. These costs are measured in. Total revenue = price × quantity. Whether you produce a lot or a little, the fixed costs are the same. Fixed cost, variable cost, total cost, average fixed cost,. Fixed Cost Formula Microeconomics.

From www.youtube.com

How to Calculate Total, Variable, and Fixed Costs in Microeconomics Fixed Cost Formula Microeconomics Examples of fixed costs include rent,. There are seven cost curves in the short run: They are incurred regardless of how much a business produces. We calculate it by multiplying the price of the product times the quantity of output sold: Whether you produce a lot or a little, the fixed costs are the same. Total revenue = price ×. Fixed Cost Formula Microeconomics.

From www.youtube.com

IB Economics Total Fixed Costs, Total Variable Costs, Total Costs Fixed Cost Formula Microeconomics Examples of fixed costs include rent,. Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. Fixed costs are expenses that do not change with the level of production or output. They are incurred regardless of how much a business produces. There are seven cost curves in the short run: Fixed costs. Fixed Cost Formula Microeconomics.

From ar.inspiredpencil.com

Average Total Cost Formula Fixed Cost Formula Microeconomics Fixed costs are expenses that do not change with the level of production or output. They are incurred regardless of how much a business produces. Whether you produce a lot or a little, the fixed costs are the same. Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. We calculate it. Fixed Cost Formula Microeconomics.

From saylordotorg.github.io

Production and Cost Fixed Cost Formula Microeconomics Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. Fixed costs are expenses that do not change with the level of production or output. Fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. They are incurred regardless of how. Fixed Cost Formula Microeconomics.

From ar.inspiredpencil.com

Average Variable Cost Formula Fixed Cost Formula Microeconomics Total revenue = price × quantity. There are seven cost curves in the short run: They are incurred regardless of how much a business produces. Examples of fixed costs include rent,. Total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. Fixed cost, variable cost, total. Fixed Cost Formula Microeconomics.

From www.wikihow.com

How to Find Marginal Cost 11 Steps (with Pictures) wikiHow Fixed Cost Formula Microeconomics There are seven cost curves in the short run: Whether you produce a lot or a little, the fixed costs are the same. Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. These costs are measured in. Fixed costs are expenditures that do not change regardless of the level of production,. Fixed Cost Formula Microeconomics.

From www.educba.com

Marginal Cost Formula Calculator (Excel template) Fixed Cost Formula Microeconomics There are seven cost curves in the short run: Fixed costs are expenses that do not change with the level of production or output. Whether you produce a lot or a little, the fixed costs are the same. Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. Fixed costs are expenditures. Fixed Cost Formula Microeconomics.

From sendpulse.ng

What is an Average Fixed Cost Basics SendPulse Fixed Cost Formula Microeconomics Fixed costs are expenses that do not change with the level of production or output. Examples of fixed costs include rent,. Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. They are incurred regardless of how much a business produces. Total cost, fixed cost, and variable cost each reflect different aspects. Fixed Cost Formula Microeconomics.

From haipernews.com

How To Calculate Variable Cost Haiper Fixed Cost Formula Microeconomics We calculate it by multiplying the price of the product times the quantity of output sold: Total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. There are seven cost curves in the short run: Fixed costs are expenses that do not change with the level. Fixed Cost Formula Microeconomics.

From ar.inspiredpencil.com

Total Variable Cost Formula Fixed Cost Formula Microeconomics Examples of fixed costs include rent,. We calculate it by multiplying the price of the product times the quantity of output sold: Fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. Total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over. Fixed Cost Formula Microeconomics.

From www.1099cafe.com

What is a Fixed Cost Variable vs Fixed Expenses — 1099 Cafe Fixed Cost Formula Microeconomics Total revenue = price × quantity. Fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. There are seven cost curves in the short run: Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. We calculate it by multiplying the. Fixed Cost Formula Microeconomics.

From www.slideshare.net

Microeconomics Cost Functions Fixed Cost Formula Microeconomics These costs are measured in. Total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output being produced. They are incurred regardless of how much a business produces. Fixed costs are expenses that do not change with the level of production or output. We calculate it by multiplying the. Fixed Cost Formula Microeconomics.

From learnbusinessconcepts.com

Fixed Cost Explanation, Formula, Calculation, and Examples Fixed Cost Formula Microeconomics Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. Whether you produce a lot or a little, the fixed costs are the same. There are seven cost curves in the short run: Fixed costs are expenditures that do not change regardless of the level of production, at least not in the. Fixed Cost Formula Microeconomics.

From haipernews.com

How To Calculate Fixed Cost And Variable Costs In Cost Accounting Haiper Fixed Cost Formula Microeconomics There are seven cost curves in the short run: We calculate it by multiplying the price of the product times the quantity of output sold: Fixed costs are expenses that do not change with the level of production or output. They are incurred regardless of how much a business produces. Total revenue = price × quantity. Total cost, fixed cost,. Fixed Cost Formula Microeconomics.

From www.marketing91.com

Average Fixed Cost Definition, Formula and Examples Marketing91 Fixed Cost Formula Microeconomics They are incurred regardless of how much a business produces. There are seven cost curves in the short run: Fixed costs are expenditures that do not change regardless of the level of production, at least not in the short term. Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. Total cost,. Fixed Cost Formula Microeconomics.

From avada.io

How to Calculate Fixed Cost? Formula, Guide and Examples Fixed Cost Formula Microeconomics There are seven cost curves in the short run: They are incurred regardless of how much a business produces. Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. Total revenue = price × quantity. Fixed costs are expenses that do not change with the level of production or output. Fixed costs. Fixed Cost Formula Microeconomics.

From boycewire.com

Fixed Cost Definition BoyceWire Fixed Cost Formula Microeconomics Total revenue = price × quantity. There are seven cost curves in the short run: These costs are measured in. Fixed cost, variable cost, total cost, average fixed cost, average variable cost, average total cost, and marginal cost. Total cost, fixed cost, and variable cost each reflect different aspects of the cost of production over the entire quantity of output. Fixed Cost Formula Microeconomics.