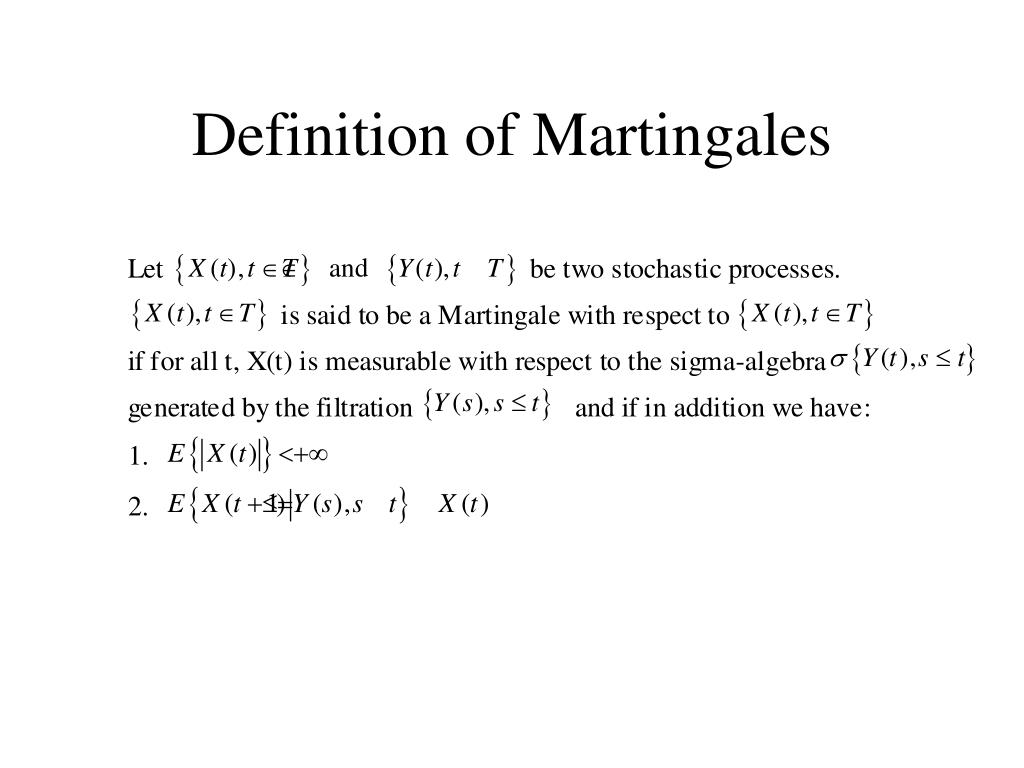

Martingale Definition Finance . a martingale is a random process $x (t)$ which has the following properties: $ e [x (t)|\mathcal {f}_t] = x (t). in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure.

from www.slideserve.com

definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure. $ e [x (t)|\mathcal {f}_t] = x (t). a martingale is a random process $x (t)$ which has the following properties: discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do.

PPT Martingales PowerPoint Presentation, free download ID1270975

Martingale Definition Finance definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure. in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure. $ e [x (t)|\mathcal {f}_t] = x (t). a martingale is a random process $x (t)$ which has the following properties:

From www.slideserve.com

PPT Chapter 3 Stopping time & martingales PowerPoint Presentation Martingale Definition Finance definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure. $ e [x (t)|\mathcal {f}_t] = x (t). a martingale is a random process $x (t)$ which has the following properties: discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on. Martingale Definition Finance.

From phemex.com

What is Martingale Strategy 100 Profitable Trading Phemex Academy Martingale Definition Finance $ e [x (t)|\mathcal {f}_t] = x (t). discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. a martingale is a random process $x (t)$ which has the following properties: in financial mathematics, martingales are used to model asset prices in an efficient market where past price. Martingale Definition Finance.

From admiralmarkets.com

What Is The Martingale Strategy in FX Trading? Admiral Markets Admirals Martingale Definition Finance discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. $ e [x (t)|\mathcal {f}_t] = x (t). a martingale is a random process $x (t)$ which has the following properties: in financial mathematics, martingales are used to model asset prices in an efficient market where past price. Martingale Definition Finance.

From homemadefinance.de

Funktioniert Martingale an der Börse/Forex? Homemade Finance Martingale Definition Finance $ e [x (t)|\mathcal {f}_t] = x (t). a martingale is a random process $x (t)$ which has the following properties: discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. in financial mathematics, martingales are used to model asset prices in an efficient market where past price. Martingale Definition Finance.

From dokumen.tips

(PDF) Martingale Methods in Financial ModellingMusiela DOKUMEN.TIPS Martingale Definition Finance in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. a martingale is a random process $x (t)$ which has the following properties: definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure. $ e [x (t)|\mathcal {f}_t] =. Martingale Definition Finance.

From rumble.com

Martingale Trading Strategy (Backtest And Example) Quantified Strategies Martingale Definition Finance $ e [x (t)|\mathcal {f}_t] = x (t). definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure. in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. discussion of the applicability of martingales to finance (incorporating a few. Martingale Definition Finance.

From www.goodreads.com

Martingales and Financial Mathematics in Discrete Time by Benoîte de Martingale Definition Finance $ e [x (t)|\mathcal {f}_t] = x (t). in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots,. Martingale Definition Finance.

From www.forex.academy

The Martingale Strategy Usage, Procedures, and Methodology Forex Academy Martingale Definition Finance in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. a martingale is a random process $x (t)$ which has the following properties: $ e [x (t)|\mathcal {f}_t] = x (t). definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under. Martingale Definition Finance.

From theforexgeek.com

What Is A Forex Martingale Strategy The Forex Geek Martingale Definition Finance a martingale is a random process $x (t)$ which has the following properties: discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. $ e [x (t)|\mathcal {f}_t] = x (t). definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under. Martingale Definition Finance.

From capital.com

Martingale system Definition and Meaning Martingale Definition Finance in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. a martingale is a random process $x (t)$ which has the following properties: $ e [x (t)|\mathcal {f}_t] = x (t). discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on. Martingale Definition Finance.

From admiralmarkets.com

What Is The Martingale Strategy in FX Trading? Admiral Markets Admirals Martingale Definition Finance a martingale is a random process $x (t)$ which has the following properties: discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. $ e [x (t)|\mathcal {f}_t] = x (t). in financial mathematics, martingales are used to model asset prices in an efficient market where past price. Martingale Definition Finance.

From medium.com

Martingales and Markov Processes. Introduction to Quantitative Finance Martingale Definition Finance in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. $ e [x (t)|\mathcal {f}_t] = x (t). discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots,. Martingale Definition Finance.

From www.slideserve.com

PPT Martingales PowerPoint Presentation, free download ID1270975 Martingale Definition Finance discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. $ e [x (t)|\mathcal {f}_t] = x (t). a martingale is a random process $x (t)$ which has the following properties: in financial mathematics, martingales are used to model asset prices in an efficient market where past price. Martingale Definition Finance.

From investbro.id

Strategi Martingale Cara Menggunakan, Kelebihan, Kekurangan InvestBro Martingale Definition Finance a martingale is a random process $x (t)$ which has the following properties: definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure. $ e [x (t)|\mathcal {f}_t] = x (t). discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on. Martingale Definition Finance.

From offres-oem.blogspot.com

OEM How to trade with a Martingale Strategy? Martingale Definition Finance $ e [x (t)|\mathcal {f}_t] = x (t). a martingale is a random process $x (t)$ which has the following properties: definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure. discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on. Martingale Definition Finance.

From traderrr.com

Martingale Trading Strategy Trading definition and uses Martingale Definition Finance $ e [x (t)|\mathcal {f}_t] = x (t). definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure. a martingale is a random process $x (t)$ which has the following properties: in financial mathematics, martingales are used to model asset prices in an efficient market where past price. Martingale Definition Finance.

From www.profitf.com

Martingale manual system (Safe martingale trading method) Martingale Definition Finance a martingale is a random process $x (t)$ which has the following properties: $ e [x (t)|\mathcal {f}_t] = x (t). discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under. Martingale Definition Finance.

From bloghowtotrade.blogspot.com

How To Trade Blog 99 of Traders Lose Money With Martingale Method Martingale Definition Finance in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure.. Martingale Definition Finance.

From www.slideserve.com

PPT Martingales PowerPoint Presentation, free download ID1270975 Martingale Definition Finance in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. a martingale is a random process $x (t)$ which has the following properties: discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. definition 4.4 a sequence of. Martingale Definition Finance.

From casinoalpha.com

Reverse Martingale Explained Betting Smart in Roulette Martingale Definition Finance discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. a martingale is a random process $x (t)$ which has the following properties: $ e [x (t)|\mathcal {f}_t] = x (t). definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under. Martingale Definition Finance.

From finance.gov.capital

What is Martingale Strategy in Forex? Finance.Gov.Capital Martingale Definition Finance discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. a martingale is a random process $x (t)$ which has the following properties: definition 4.4 a sequence of. Martingale Definition Finance.

From traderrr.com

Martingale Trading Strategy Trading definition and uses Martingale Definition Finance $ e [x (t)|\mathcal {f}_t] = x (t). discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure. in financial mathematics, martingales are used to model asset prices in. Martingale Definition Finance.

From paxforex.org

What Is The Martingale Strategy In Forex Trading? PAXFOREX Martingale Definition Finance in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure. discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral.. Martingale Definition Finance.

From www.slideserve.com

PPT Statistical Properties of Returns PowerPoint Presentation, free Martingale Definition Finance a martingale is a random process $x (t)$ which has the following properties: in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. definition 4.4 a sequence of. Martingale Definition Finance.

From www.mql5.com

Trading What is Martingale and Is It Reasonable to Use It? Trading Martingale Definition Finance discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. $ e [x (t)|\mathcal {f}_t] = x (t). in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. a martingale is a random process $x (t)$ which has the. Martingale Definition Finance.

From www.quantifiedstrategies.com

Martingale Trading Strategy Video, Rules, Setup, Backtest Quantified Martingale Definition Finance $ e [x (t)|\mathcal {f}_t] = x (t). definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure. a martingale is a random process $x (t)$ which has the following properties: discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on. Martingale Definition Finance.

From www.slideserve.com

PPT Hyperbolic Processes in Finance PowerPoint Presentation, free Martingale Definition Finance discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. a martingale is a random process $x (t)$ which has the following properties: $ e [x (t)|\mathcal {f}_t] = x (t). definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under. Martingale Definition Finance.

From investmentmath.com

Martingales Martingale Definition Finance $ e [x (t)|\mathcal {f}_t] = x (t). in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure. a martingale is a random process $x (t)$ which has the. Martingale Definition Finance.

From en.wikipedia.org

Martingale (probability theory) Wikipedia Martingale Definition Finance in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. a martingale is a random process $x (t)$ which has the following properties: $ e [x (t)|\mathcal {f}_t] = x (t). definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under. Martingale Definition Finance.

From blog.hsb.co.id

Berkenalan dengan Strategi Martingale dalam Trading HSB Investasi Martingale Definition Finance discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. $ e [x (t)|\mathcal {f}_t] = x (t). a martingale is a random process $x (t)$ which has the. Martingale Definition Finance.

From www.modalmais.com.br

Usar a Estratégia Martingale no Day Trade é vantajoso? Modal a Martingale Definition Finance discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. $ e [x (t)|\mathcal {f}_t] = x (t). in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots,. Martingale Definition Finance.

From capital.com

Martingale system Definition and Meaning Martingale Definition Finance discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure. $ e [x (t)|\mathcal {f}_t] = x (t). in financial mathematics, martingales are used to model asset prices in. Martingale Definition Finance.

From blog.hsb.co.id

Berkenalan dengan Strategi Martingale dalam Trading HSB Investasi Martingale Definition Finance $ e [x (t)|\mathcal {f}_t] = x (t). in financial mathematics, martingales are used to model asset prices in an efficient market where past price movements do. a martingale is a random process $x (t)$ which has the following properties: definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under. Martingale Definition Finance.

From fyoaayzjf.blob.core.windows.net

Martingale Progression at Jessica Hackett blog Martingale Definition Finance definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure. a martingale is a random process $x (t)$ which has the following properties: $ e [x (t)|\mathcal {f}_t] = x (t). discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on. Martingale Definition Finance.

From makemoneywithoutajob.com

How Does the Martingale System Work? Make Money Without A Job Martingale Definition Finance discussion of the applicability of martingales to finance (incorporating a few caveats) appears in the section on risk neutral. a martingale is a random process $x (t)$ which has the following properties: definition 4.4 a sequence of integrable random variables \(y_0, y_1, \cdots, y_t\) is called a martingale under the measure. in financial mathematics, martingales are. Martingale Definition Finance.