Spread Duration Of Floating Rate Bond . The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate. Adding to the answer of tim: With zero spread the price of the bond is given by:. i need to calculate the duration of a floating rate bond with spread. The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of.

from thewire.fiig.com.au

Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. i need to calculate the duration of a floating rate bond with spread. The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. Adding to the answer of tim: floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate. With zero spread the price of the bond is given by:.

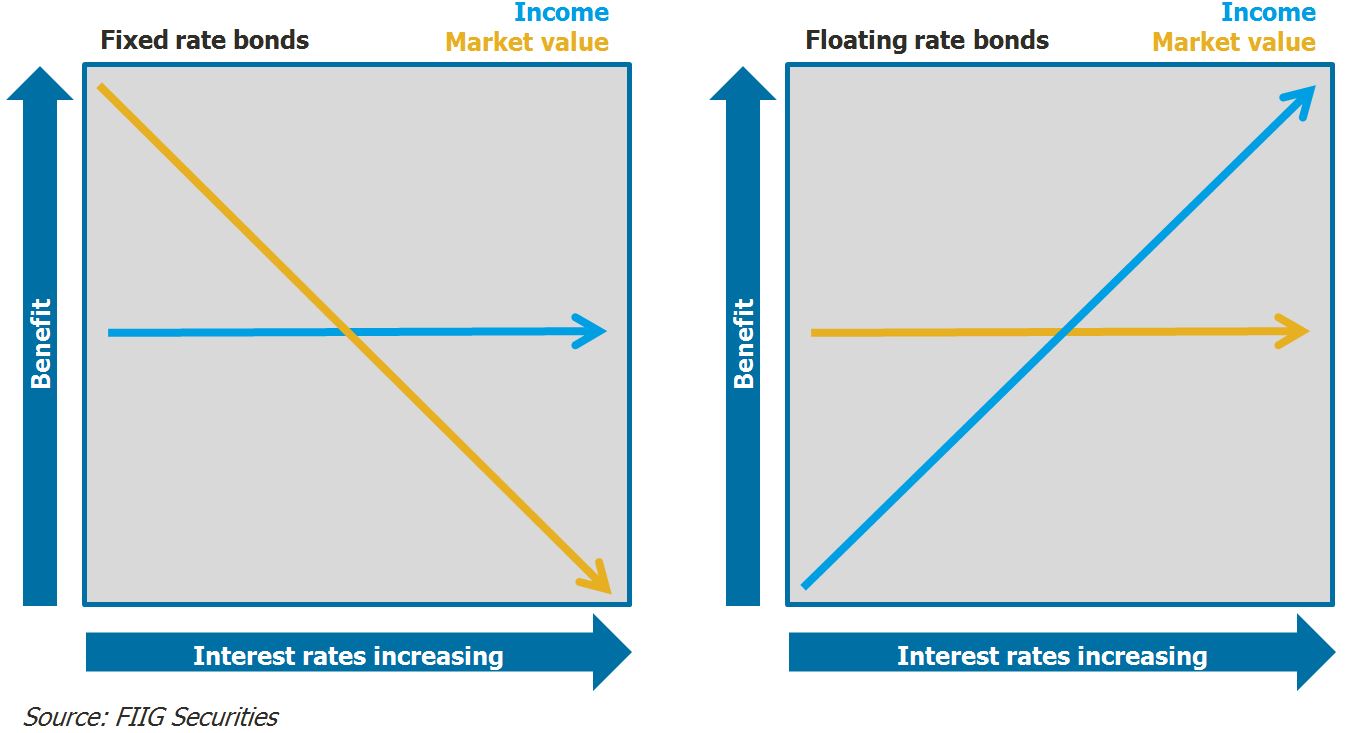

Inflation linked bonds A key component in your portfolio

Spread Duration Of Floating Rate Bond i need to calculate the duration of a floating rate bond with spread. Adding to the answer of tim: Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. i need to calculate the duration of a floating rate bond with spread. floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate. The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. With zero spread the price of the bond is given by:.

From www.youtube.com

Floating Rate savings Bonds2020(Taxable)Saving Bonds schemeFloating Spread Duration Of Floating Rate Bond The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. Adding to the answer of tim: Spread duration is a measure of price sensitivity to changes in dm (credit. Spread Duration Of Floating Rate Bond.

From www.wallstreetprep.com

Floating Interest Rate Formula + Calculator Spread Duration Of Floating Rate Bond The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. . Spread Duration Of Floating Rate Bond.

From blog.shoonya.com

Understanding Floating Rate Bonds Spread Duration Of Floating Rate Bond i need to calculate the duration of a floating rate bond with spread. floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate. The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. Spread duration is a. Spread Duration Of Floating Rate Bond.

From www.slideserve.com

PPT Exchange Rate Regimes PowerPoint Presentation, free download ID Spread Duration Of Floating Rate Bond The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. . Spread Duration Of Floating Rate Bond.

From slideplayer.com

Chapter 2 Pricing of Bonds ppt download Spread Duration Of Floating Rate Bond floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate. The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. i need to calculate the duration of a floating rate bond with spread. Adding to the. Spread Duration Of Floating Rate Bond.

From www.youtube.com

FLOATING RATE BOND YouTube Spread Duration Of Floating Rate Bond The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. i need to calculate the duration of a floating rate bond with spread. Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. With zero spread the price of the. Spread Duration Of Floating Rate Bond.

From www.youtube.com

Floating Rate Bonds Explained RBI Floating Rate Bonds How To Invest Spread Duration Of Floating Rate Bond Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate.. Spread Duration Of Floating Rate Bond.

From www.youtube.com

CFA Level 1 Fixed Yield Measures for Floatingrate Securities Spread Duration Of Floating Rate Bond i need to calculate the duration of a floating rate bond with spread. The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. Adding to the answer of tim: The duration of a floating rate bond is the time t until the next coupon payment, as your equation. Spread Duration Of Floating Rate Bond.

From www.investopedia.com

Duration and Convexity to Measure Bond Risk Spread Duration Of Floating Rate Bond The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. With zero spread the price of the bond is given by:. Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. i need to calculate the duration of a floating rate. Spread Duration Of Floating Rate Bond.

From seekingalpha.com

Floating Rate Bond Funds 7 (And Rising) Yields! (NYSEJFR) Seeking Spread Duration Of Floating Rate Bond The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate. i need to calculate the duration of a floating rate bond with spread. Adding to the. Spread Duration Of Floating Rate Bond.

From govtempdiary.com

Introduction Of Floating Rate Savings Bonds, 2020 (Taxable Spread Duration Of Floating Rate Bond The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate. With zero spread the price of the bond is given by:. i need to calculate the. Spread Duration Of Floating Rate Bond.

From www.cfajournal.org

Floating Rate Bonds Characteristics, Rate, and Important CFAJournal Spread Duration Of Floating Rate Bond The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. Adding to the answer of tim: i need to calculate the duration of a floating rate bond with. Spread Duration Of Floating Rate Bond.

From www.youtube.com

How To Buy RBI Floating Rate Bonds 2021 Interest rate Invest in RBI Spread Duration Of Floating Rate Bond floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate. Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. With zero spread the price of the bond is given by:. The effective spread is the average margin over the. Spread Duration Of Floating Rate Bond.

From www.slideteam.net

Fixed Rate Bond Floating Rate Bond Ppt Powerpoint Presentation Show Spread Duration Of Floating Rate Bond With zero spread the price of the bond is given by:. Adding to the answer of tim: The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. i. Spread Duration Of Floating Rate Bond.

From www.finpricing.com

Floating Rate Notes Pricing and Valuation FinPricing Spread Duration Of Floating Rate Bond The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. With zero spread the price of the bond is given by:. floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate. Adding to the answer of tim: Spread. Spread Duration Of Floating Rate Bond.

From www.youtube.com

06 Floating Rate Bonds YouTube Spread Duration Of Floating Rate Bond Adding to the answer of tim: Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. i need to calculate the duration of a floating rate bond with spread. With zero spread the price of the bond is given by:. floating rate bonds are also subject to spread duration [3]. Spread Duration Of Floating Rate Bond.

From thewire.fiig.com.au

Inflation linked bonds A key component in your portfolio Spread Duration Of Floating Rate Bond With zero spread the price of the bond is given by:. The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. i need to calculate the duration of a floating rate. Spread Duration Of Floating Rate Bond.

From corporatefinanceinstitute.com

Floating Exchange Rate Overview, Functions, Benefits, Limitations Spread Duration Of Floating Rate Bond floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate. The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. i need to calculate the duration of a floating rate bond with spread. The duration of. Spread Duration Of Floating Rate Bond.

From www.youtube.com

Floating Rate Bonds explained, How they are different from regular Spread Duration Of Floating Rate Bond floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate. With zero spread the price of the bond is given by:. Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. Adding to the answer of tim: The duration of. Spread Duration Of Floating Rate Bond.

From www.ishares.com

Riding the rising rate wave with floating rate notes iShares BlackRock Spread Duration Of Floating Rate Bond The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. i need to calculate the duration of a floating rate bond with spread. floating rate bonds are also subject. Spread Duration Of Floating Rate Bond.

From www.slideserve.com

PPT Bonds PowerPoint Presentation, free download ID1346246 Spread Duration Of Floating Rate Bond Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. Adding to the answer of tim: i need to calculate the duration of a floating rate bond with spread. The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. The effective. Spread Duration Of Floating Rate Bond.

From www.chegg.com

Valuing a floored floating rate bond. Wha is Spread Duration Of Floating Rate Bond floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate. i need to calculate the duration of a floating rate bond with spread. The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. Spread duration is a. Spread Duration Of Floating Rate Bond.

From quant.stackexchange.com

bond Duration. Floating rate note Quantitative Finance Stack Exchange Spread Duration Of Floating Rate Bond Adding to the answer of tim: Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. i need to calculate the duration of a floating rate bond with spread. The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. The. Spread Duration Of Floating Rate Bond.

From www.financestrategists.com

FloatingRate Bonds Definition, Types, Benefits, and Risks Spread Duration Of Floating Rate Bond Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. Adding to the answer of tim: floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate. The effective spread is the average margin over the benchmark rate that is expected. Spread Duration Of Floating Rate Bond.

From www.slideserve.com

PPT LongTerm Debt and Lease Financing PowerPoint Presentation, free Spread Duration Of Floating Rate Bond With zero spread the price of the bond is given by:. Adding to the answer of tim: The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. The effective spread is the. Spread Duration Of Floating Rate Bond.

From www.bpwealth.com

Floating Rate Savings Bonds Archives BP Wealth Blog Spread Duration Of Floating Rate Bond With zero spread the price of the bond is given by:. i need to calculate the duration of a floating rate bond with spread. The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. floating rate bonds are also subject to spread duration [3] basically, spread duration approximately. Spread Duration Of Floating Rate Bond.

From www.amundi.com

FloatingRate Bonds May Help Protect Against Rising Rates Amundi US Spread Duration Of Floating Rate Bond The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate. i need to calculate the duration of a floating rate bond with spread. Adding to the answer. Spread Duration Of Floating Rate Bond.

From analystprep.com

Swap Rate Curve CFA, FRM, and Actuarial Exams Study Notes Spread Duration Of Floating Rate Bond The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. i need to calculate the duration of a floating rate bond with spread. With zero spread the price of the bond is given by:. The duration of a floating rate bond is the time t until the next. Spread Duration Of Floating Rate Bond.

From www.wallstreetprep.com

Floating Interest Rate Formula and Calculation Spread Duration Of Floating Rate Bond Adding to the answer of tim: The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. i need to calculate the duration of a floating rate bond with spread. With zero. Spread Duration Of Floating Rate Bond.

From www.indiabonds.com

What are Floating Rate Bonds? IndiaBonds Spread Duration Of Floating Rate Bond i need to calculate the duration of a floating rate bond with spread. The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. Adding to the answer of tim: The effective. Spread Duration Of Floating Rate Bond.

From www.apriem.com

Investment 101 Floating Rate Loans Apriem Spread Duration Of Floating Rate Bond With zero spread the price of the bond is given by:. Spread duration is a measure of price sensitivity to changes in dm (credit spread) assuming there is no. i need to calculate the duration of a floating rate bond with spread. The duration of a floating rate bond is the time t until the next coupon payment, as. Spread Duration Of Floating Rate Bond.

From seekingalpha.com

Arbitrage Opportunity In Floating Rate Bond Funds (NYSEJQC) Seeking Spread Duration Of Floating Rate Bond With zero spread the price of the bond is given by:. The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. The duration of a floating rate bond is the time t until the next coupon payment, as your equation shows. i need to calculate the duration of. Spread Duration Of Floating Rate Bond.

From www.adviservoice.com.au

Fixed vs. floating rate funds The winner is clear AdviserVoice Spread Duration Of Floating Rate Bond Adding to the answer of tim: floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate. The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. Spread duration is a measure of price sensitivity to changes in. Spread Duration Of Floating Rate Bond.

From www.mymoneykarma.com

RBI Floating Rate Bond Saving Bonds Interest Rates & Taxability Spread Duration Of Floating Rate Bond The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. floating rate bonds are also subject to spread duration [3] basically, spread duration approximately measures the change in a floating rate. i need to calculate the duration of a floating rate bond with spread. Spread duration is. Spread Duration Of Floating Rate Bond.

From www.slideserve.com

PPT Chapter PowerPoint Presentation, free download ID5190108 Spread Duration Of Floating Rate Bond i need to calculate the duration of a floating rate bond with spread. The effective spread is the average margin over the benchmark rate that is expected to be earned over the life of. Adding to the answer of tim: With zero spread the price of the bond is given by:. floating rate bonds are also subject to. Spread Duration Of Floating Rate Bond.