Monte Carlo Simulation Derivative Pricing . Checkout various monte carlo methods for option pricing here! Monte carlo simulation of european options. 1.2 derivative pricing we now give some examples of pricing derivatives with monte carlo methods. In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. Brief overview of the multilevel monte carlo estimator. In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. In this work, we present a quantum algorithm for the monte carlo pricing of financial. Review of the importance sampling algorithm to reduce the overall variance of the. Monte carlo simulation is a commonly used method for derivatives pricing where the payoff depends on the history price of the underlying asset.

from www.tejwin.com

In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. Monte carlo simulation of european options. Checkout various monte carlo methods for option pricing here! Monte carlo simulation is a commonly used method for derivatives pricing where the payoff depends on the history price of the underlying asset. In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. Review of the importance sampling algorithm to reduce the overall variance of the. Brief overview of the multilevel monte carlo estimator. 1.2 derivative pricing we now give some examples of pricing derivatives with monte carlo methods. In this work, we present a quantum algorithm for the monte carlo pricing of financial.

Options Pricing with Monte Carlo Simulation TEJ

Monte Carlo Simulation Derivative Pricing In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. In this work, we present a quantum algorithm for the monte carlo pricing of financial. Monte carlo simulation of european options. Review of the importance sampling algorithm to reduce the overall variance of the. 1.2 derivative pricing we now give some examples of pricing derivatives with monte carlo methods. Brief overview of the multilevel monte carlo estimator. In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. Monte carlo simulation is a commonly used method for derivatives pricing where the payoff depends on the history price of the underlying asset. Checkout various monte carlo methods for option pricing here!

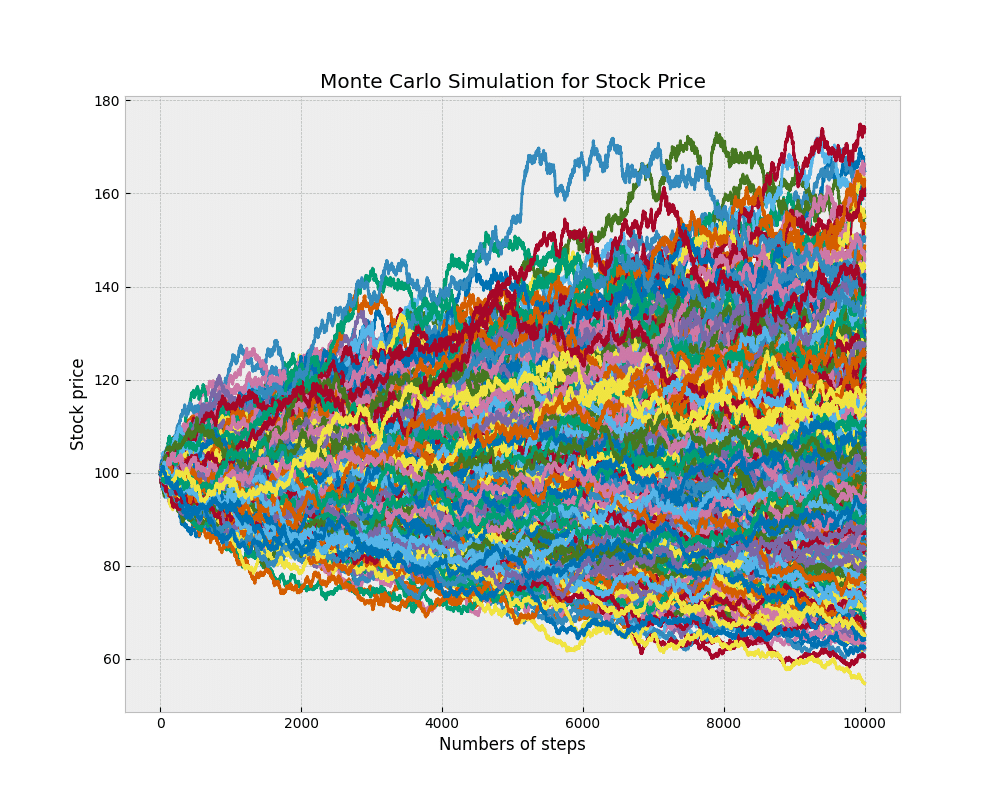

From quantpy.com.au

Monte Carlo Simulation of Temperature for Weather Derivative Pricing Monte Carlo Simulation Derivative Pricing 1.2 derivative pricing we now give some examples of pricing derivatives with monte carlo methods. In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. Review of the importance sampling algorithm to reduce the overall variance of the. Brief overview of the multilevel monte carlo estimator. In this work, we present a quantum. Monte Carlo Simulation Derivative Pricing.

From www.slideserve.com

PPT Lecture 2 Monte Carlo method in finance PowerPoint Presentation Monte Carlo Simulation Derivative Pricing In this work, we present a quantum algorithm for the monte carlo pricing of financial. In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. Checkout various. Monte Carlo Simulation Derivative Pricing.

From www.youtube.com

Monte Carlo Simulation of Temperature for Weather Derivative Pricing Monte Carlo Simulation Derivative Pricing 1.2 derivative pricing we now give some examples of pricing derivatives with monte carlo methods. In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. Checkout various monte carlo methods for option pricing here! Monte carlo simulation of european options. Brief overview of the. Monte Carlo Simulation Derivative Pricing.

From www.researchgate.net

(PDF) The value of Monte Carlo modelbased variance reduction Monte Carlo Simulation Derivative Pricing 1.2 derivative pricing we now give some examples of pricing derivatives with monte carlo methods. In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. In this. Monte Carlo Simulation Derivative Pricing.

From towardsdatascience.com

Monte Carlo Simulation in R with focus on Option Pricing by Ojasvin Monte Carlo Simulation Derivative Pricing In this work, we present a quantum algorithm for the monte carlo pricing of financial. Checkout various monte carlo methods for option pricing here! Brief overview of the multilevel monte carlo estimator. Review of the importance sampling algorithm to reduce the overall variance of the. Monte carlo simulation of european options. In the first part of this thesis, we review. Monte Carlo Simulation Derivative Pricing.

From www.youtube.com

Simple Monte Carlo Simulation of Stock Prices with Python YouTube Monte Carlo Simulation Derivative Pricing Review of the importance sampling algorithm to reduce the overall variance of the. Monte carlo simulation is a commonly used method for derivatives pricing where the payoff depends on the history price of the underlying asset. In this work, we present a quantum algorithm for the monte carlo pricing of financial. Brief overview of the multilevel monte carlo estimator. Checkout. Monte Carlo Simulation Derivative Pricing.

From dokumen.tips

(PDF) Pricing Derivatives on GPUs Using Monte Carlo Simulation Monte Carlo Simulation Derivative Pricing In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. Brief overview of the multilevel monte carlo estimator. Monte carlo simulation is a commonly used method for derivatives pricing where the payoff depends on the history price of the underlying asset. 1.2 derivative pricing we now give some examples of pricing derivatives with. Monte Carlo Simulation Derivative Pricing.

From slideplayer.com

Pricing Barrier Options Using Monte Carlo Simulation ppt download Monte Carlo Simulation Derivative Pricing Monte carlo simulation of european options. Brief overview of the multilevel monte carlo estimator. Checkout various monte carlo methods for option pricing here! Monte carlo simulation is a commonly used method for derivatives pricing where the payoff depends on the history price of the underlying asset. Review of the importance sampling algorithm to reduce the overall variance of the. In. Monte Carlo Simulation Derivative Pricing.

From www.slideserve.com

PPT Lecture 2 Monte Carlo method in finance PowerPoint Presentation Monte Carlo Simulation Derivative Pricing In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. Brief overview of the multilevel monte carlo estimator. Review of the importance sampling algorithm to reduce the overall variance of the. In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence. Monte Carlo Simulation Derivative Pricing.

From www.youtube.com

Option Pricing with derivmkts Option Greeks, Monte Carlo Simulation Monte Carlo Simulation Derivative Pricing In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. In this work, we present a quantum algorithm for the monte carlo pricing of financial. Brief overview. Monte Carlo Simulation Derivative Pricing.

From www.youtube.com

Monte Carlo Simulation for Pricing Derivatives YouTube Monte Carlo Simulation Derivative Pricing In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. Brief overview of the multilevel monte carlo estimator. Monte carlo simulation of european options. In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. Monte carlo simulation. Monte Carlo Simulation Derivative Pricing.

From www.youtube.com

Monte Carlo Simulations in Python to Price Financial Derivatives Asian Monte Carlo Simulation Derivative Pricing In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. Monte carlo simulation of european options. Review of the importance sampling algorithm to reduce the overall variance of the. In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of. Monte Carlo Simulation Derivative Pricing.

From www.linkedin.com

Hedged MonteCarlo Low Variance Derivative Pricing With Objective Monte Carlo Simulation Derivative Pricing In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. In this work, we present a quantum algorithm for the monte carlo pricing of financial. Checkout various monte carlo methods for option pricing here! Monte carlo simulation is a commonly used method for derivatives. Monte Carlo Simulation Derivative Pricing.

From www.mdpi.com

Mathematics Free FullText A Generalized Weighted Monte Carlo Monte Carlo Simulation Derivative Pricing Review of the importance sampling algorithm to reduce the overall variance of the. Brief overview of the multilevel monte carlo estimator. Checkout various monte carlo methods for option pricing here! In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. 1.2 derivative pricing we. Monte Carlo Simulation Derivative Pricing.

From www.semanticscholar.org

Figure 2 from A Generalized Weighted Monte Carlo Calibration Method for Monte Carlo Simulation Derivative Pricing Checkout various monte carlo methods for option pricing here! Review of the importance sampling algorithm to reduce the overall variance of the. 1.2 derivative pricing we now give some examples of pricing derivatives with monte carlo methods. In this work, we present a quantum algorithm for the monte carlo pricing of financial. In the first part of this thesis, we. Monte Carlo Simulation Derivative Pricing.

From investexcel.net

Monte Carlo Option Pricing in Excel Invest Excel Monte Carlo Simulation Derivative Pricing In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. Checkout various monte carlo methods for option pricing here! Brief overview of the multilevel monte carlo estimator. In this work, we present a quantum algorithm for the monte carlo pricing of financial. 1.2 derivative pricing we now give some examples of pricing derivatives. Monte Carlo Simulation Derivative Pricing.

From www.youtube.com

OPTION PRICING USING MONTE CARLO SIMULATION YouTube Monte Carlo Simulation Derivative Pricing Review of the importance sampling algorithm to reduce the overall variance of the. Brief overview of the multilevel monte carlo estimator. Checkout various monte carlo methods for option pricing here! Monte carlo simulation is a commonly used method for derivatives pricing where the payoff depends on the history price of the underlying asset. In this article, we discuss pricing options. Monte Carlo Simulation Derivative Pricing.

From quantpedia.com

Introduction and Examples of Monte Carlo Strategy Simulation QuantPedia Monte Carlo Simulation Derivative Pricing In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. Monte carlo simulation of european options. In this work, we present a quantum algorithm for the monte carlo pricing of financial. Checkout various monte carlo methods for option pricing here! In this article, we. Monte Carlo Simulation Derivative Pricing.

From www.backtick.ai

Introduction to Monte Carlo simulations and option pricing Monte Carlo Simulation Derivative Pricing Review of the importance sampling algorithm to reduce the overall variance of the. Brief overview of the multilevel monte carlo estimator. 1.2 derivative pricing we now give some examples of pricing derivatives with monte carlo methods. Monte carlo simulation of european options. In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. Checkout. Monte Carlo Simulation Derivative Pricing.

From www.semanticscholar.org

Figure 2 from THE APPLICATION OF MONTE CARLO SIMULATION BASED ON NORMAL Monte Carlo Simulation Derivative Pricing Monte carlo simulation is a commonly used method for derivatives pricing where the payoff depends on the history price of the underlying asset. In this work, we present a quantum algorithm for the monte carlo pricing of financial. Checkout various monte carlo methods for option pricing here! Monte carlo simulation of european options. In the first part of this thesis,. Monte Carlo Simulation Derivative Pricing.

From towardsdatascience.com

Monte Carlo Simulation in R with focus on Option Pricing by Ojasvin Monte Carlo Simulation Derivative Pricing Brief overview of the multilevel monte carlo estimator. 1.2 derivative pricing we now give some examples of pricing derivatives with monte carlo methods. Review of the importance sampling algorithm to reduce the overall variance of the. Monte carlo simulation of european options. In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. Checkout. Monte Carlo Simulation Derivative Pricing.

From github.com

GitHub zhengkaifeng/derivativepricingmontecarlo Option Monte Carlo Simulation Derivative Pricing 1.2 derivative pricing we now give some examples of pricing derivatives with monte carlo methods. Checkout various monte carlo methods for option pricing here! Review of the importance sampling algorithm to reduce the overall variance of the. Monte carlo simulation is a commonly used method for derivatives pricing where the payoff depends on the history price of the underlying asset.. Monte Carlo Simulation Derivative Pricing.

From www.slideserve.com

PPT Lecture 2 Monte Carlo method in finance PowerPoint Presentation Monte Carlo Simulation Derivative Pricing Checkout various monte carlo methods for option pricing here! Monte carlo simulation of european options. Monte carlo simulation is a commonly used method for derivatives pricing where the payoff depends on the history price of the underlying asset. In this work, we present a quantum algorithm for the monte carlo pricing of financial. In this article, we discuss pricing options. Monte Carlo Simulation Derivative Pricing.

From www.semanticscholar.org

Figure 1 from THE APPLICATION OF MONTE CARLO SIMULATION BASED ON NORMAL Monte Carlo Simulation Derivative Pricing Checkout various monte carlo methods for option pricing here! Brief overview of the multilevel monte carlo estimator. In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. In this work, we present a quantum algorithm for the monte carlo pricing of financial. Monte carlo simulation of european options. Monte carlo simulation is a. Monte Carlo Simulation Derivative Pricing.

From www.mdpi.com

Mathematics Free FullText A Generalized Weighted Monte Carlo Monte Carlo Simulation Derivative Pricing In this work, we present a quantum algorithm for the monte carlo pricing of financial. Review of the importance sampling algorithm to reduce the overall variance of the. Monte carlo simulation of european options. Monte carlo simulation is a commonly used method for derivatives pricing where the payoff depends on the history price of the underlying asset. In the first. Monte Carlo Simulation Derivative Pricing.

From www.slideserve.com

PPT Pricing Derivatives Securities using MATLAB PowerPoint Monte Carlo Simulation Derivative Pricing In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. 1.2 derivative pricing we now give some examples of pricing derivatives with monte carlo methods. In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. Monte carlo. Monte Carlo Simulation Derivative Pricing.

From onlinelibrary.wiley.com

Data transfer minimization for financial derivative pricing using Monte Monte Carlo Simulation Derivative Pricing In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. In this work, we present a quantum algorithm for the monte carlo pricing of financial. Brief overview. Monte Carlo Simulation Derivative Pricing.

From www.researchgate.net

19 Illustration of the Monte Carlo method in reliability analysis Monte Carlo Simulation Derivative Pricing Brief overview of the multilevel monte carlo estimator. Checkout various monte carlo methods for option pricing here! 1.2 derivative pricing we now give some examples of pricing derivatives with monte carlo methods. In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. Review of. Monte Carlo Simulation Derivative Pricing.

From www.tejwin.com

Options Pricing with Monte Carlo Simulation TEJ Monte Carlo Simulation Derivative Pricing In this work, we present a quantum algorithm for the monte carlo pricing of financial. 1.2 derivative pricing we now give some examples of pricing derivatives with monte carlo methods. Review of the importance sampling algorithm to reduce the overall variance of the. In the first part of this thesis, we review several methods that they have been proposed, in. Monte Carlo Simulation Derivative Pricing.

From dokumen.tips

(PDF) Monte Carlo Simulation in Derivative Pricing · PDF fileMONTE Monte Carlo Simulation Derivative Pricing In this work, we present a quantum algorithm for the monte carlo pricing of financial. In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. 1.2 derivative pricing we now give some examples of pricing derivatives with monte carlo methods. Monte carlo simulation is. Monte Carlo Simulation Derivative Pricing.

From www.scribd.com

1) Martingale Pricing & Monte Carlo Simulation Download Free PDF Monte Carlo Simulation Derivative Pricing 1.2 derivative pricing we now give some examples of pricing derivatives with monte carlo methods. In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. Monte carlo simulation is a commonly used method for derivatives pricing where the payoff depends on the history price of the underlying asset. Checkout various monte carlo methods. Monte Carlo Simulation Derivative Pricing.

From www.slideserve.com

PPT The Monte Carlo Method for pricing financial derivatives Monte Carlo Simulation Derivative Pricing In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. Brief overview of the multilevel monte carlo estimator. Review of the importance sampling algorithm to reduce the overall variance of the. In this article, we discuss pricing options by monte carlo simulation and geometric. Monte Carlo Simulation Derivative Pricing.

From www.scratchapixel.com

Monte Carlo Methods in Practice Monte Carlo Simulation Derivative Pricing In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. Review of the importance sampling algorithm to reduce the overall variance of the. In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. Monte carlo simulation of. Monte Carlo Simulation Derivative Pricing.

From www.youtube.com

Monte Carlo Simulation for Option Pricing with Python (Basic Ideas Monte Carlo Simulation Derivative Pricing Review of the importance sampling algorithm to reduce the overall variance of the. Monte carlo simulation is a commonly used method for derivatives pricing where the payoff depends on the history price of the underlying asset. Monte carlo simulation of european options. In the first part of this thesis, we review several methods that they have been proposed, in order. Monte Carlo Simulation Derivative Pricing.

From www.semanticscholar.org

Figure 4 from A parallel Monte Carlo simulation on cluster systems for Monte Carlo Simulation Derivative Pricing 1.2 derivative pricing we now give some examples of pricing derivatives with monte carlo methods. In this article, we discuss pricing options by monte carlo simulation and geometric brownian motion using python. In the first part of this thesis, we review several methods that they have been proposed, in order to improve the convergence rate of monte carlo. Monte carlo. Monte Carlo Simulation Derivative Pricing.