Joint bank accounts offer convenience, but managing shared finances can blur personal boundaries. Knowing how to separate a joint account ensures clarity, control, and peace of mind for both parties involved.

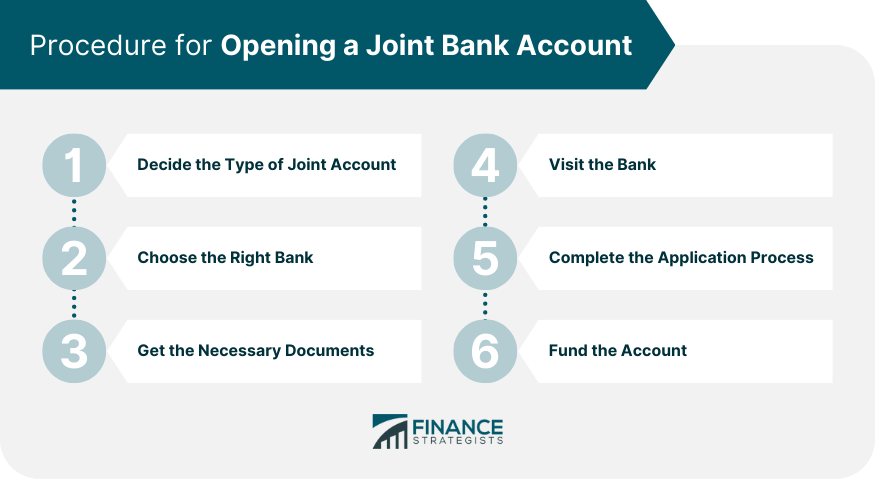

How to Separate a Joint Bank Account

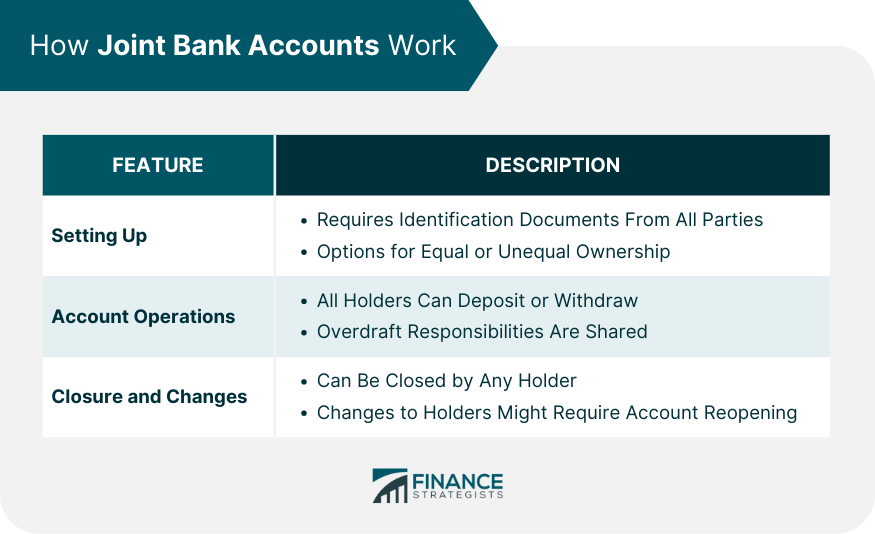

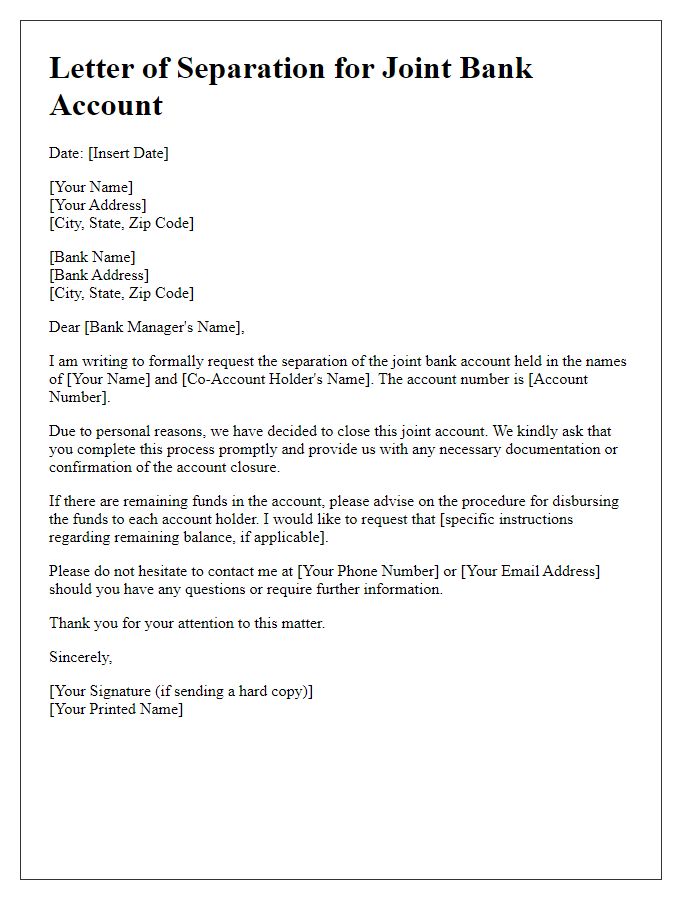

Separating a joint bank account requires careful coordination between both account holders. Begin by reviewing your bank’s policies on joint accounts, as procedures vary by institution. Inform both parties of your intent early to allow for shared planning. Request a formal release of joint access through the bank’s online portal or in-person at a branch. Withdraw outstanding balances into individual accounts, ensuring no shared transactions remain. Close shared liens, subscriptions, or automatic payments linked to the account. Finally, confirm account closure and retain all documentation for your records.

Why Proper Separation Matters

Failing to properly separate a joint account can lead to unintended financial exposure, including shared liabilities, unauthorized transactions, or conflicts over funds. A clear separation protects personal credit, simplifies tax reporting, and ensures each party maintains full control over their financial destiny.

Best Practices for a Smooth Transition

Schedule a meeting with your co-owner to discuss timelines and responsibilities. Set aside time to review account statements and reconcile balances. Use the separation process as an opportunity to establish individual financial goals and habits. Consider consulting a financial advisor to align your post-separation banking strategy with long-term objectives.

:max_bytes(150000):strip_icc()/should-you-have-joint-or-separate-bank-accounts-1289664-final-5bd08bd946e0fb0026ee9838-5bec6d0bc9e77c0051fcd280.png)

Separating a joint bank account is a straightforward yet critical step toward financial autonomy. By following clear procedures and prioritizing communication, you safeguard your assets and build confidence in independent banking. Take action today to reclaim control and ensure a fresh start for both parties.