How To Record Accruals In Accounting . To record accruals, accountants use accrual accounting principles in order to enter, adjust and track both expenses and revenues. While not everyone chooses to perform accounting. Accrual accounting is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the cash transactions occur. There are two main ways to account for income and expenses: This means you add income to your accounting journal when you complete a service. Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold and record expenses as they are. The accrued assets should appear. In accrual accounting, you record income and expenses as you earn or incur them. A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced.

from quickbooks.intuit.com

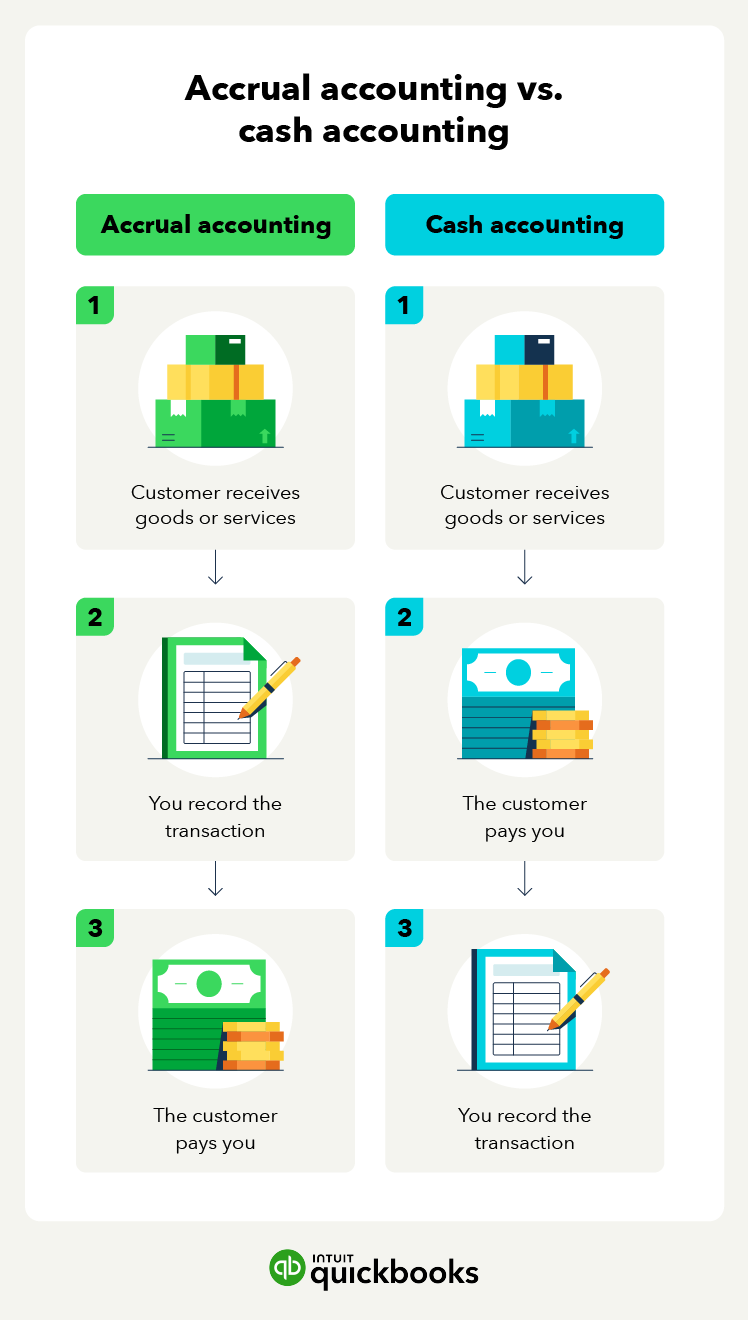

Accrual accounting is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the cash transactions occur. While not everyone chooses to perform accounting. There are two main ways to account for income and expenses: A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. In accrual accounting, you record income and expenses as you earn or incur them. This means you add income to your accounting journal when you complete a service. The accrued assets should appear. To record accruals, accountants use accrual accounting principles in order to enter, adjust and track both expenses and revenues. Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold and record expenses as they are.

What is accrual accounting? A beginners guide QuickBooks

How To Record Accruals In Accounting In accrual accounting, you record income and expenses as you earn or incur them. This means you add income to your accounting journal when you complete a service. Accrual accounting is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the cash transactions occur. To record accruals, accountants use accrual accounting principles in order to enter, adjust and track both expenses and revenues. A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. In accrual accounting, you record income and expenses as you earn or incur them. While not everyone chooses to perform accounting. The accrued assets should appear. Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold and record expenses as they are. There are two main ways to account for income and expenses:

From www.principlesofaccounting.com

Loan/Note Payable (borrow, accrued interest, and repay How To Record Accruals In Accounting A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. Accrual accounting is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the cash transactions occur. While not everyone chooses to perform accounting. This means you add income to your accounting journal. How To Record Accruals In Accounting.

From synder.com

What Is Accrual Accounting How Does It Work and Why Should You Use It? How To Record Accruals In Accounting Accrual accounting is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the cash transactions occur. Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold and record expenses as they are. To record accruals, accountants use accrual accounting principles. How To Record Accruals In Accounting.

From nonprofitandpayrallonlinelessons.blogspot.com

NonProfit And Payroll Accounting Examples of Payroll Journal Entries How To Record Accruals In Accounting There are two main ways to account for income and expenses: The accrued assets should appear. A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. In accrual accounting, you record income and expenses as you earn or incur them. To record accruals, accountants use accrual accounting principles in order. How To Record Accruals In Accounting.

From slidetodoc.com

Accounting Basics Part 1 Accrual DoubleEntry Accounting Debits How To Record Accruals In Accounting This means you add income to your accounting journal when you complete a service. The accrued assets should appear. While not everyone chooses to perform accounting. A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. To record accruals, accountants use accrual accounting principles in order to enter, adjust and. How To Record Accruals In Accounting.

From success.mitratech.com

Create an Accrual Invoice Mitratech Success Center How To Record Accruals In Accounting This means you add income to your accounting journal when you complete a service. Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold and record expenses as they are. To record accruals, accountants use accrual accounting principles in order to enter, adjust and track both expenses and. How To Record Accruals In Accounting.

From accountingplay.com

Adjusting Journal Entries Defined Accounting Play How To Record Accruals In Accounting Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold and record expenses as they are. A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. There are two main ways to account for income and expenses: The. How To Record Accruals In Accounting.

From paysimple.com

Basic Accounting for Small Business Your Top Questions Answered How To Record Accruals In Accounting In accrual accounting, you record income and expenses as you earn or incur them. Accrual accounting is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the cash transactions occur. This means you add income to your accounting journal when you complete a service. A popular choice is through accrued expenses, in. How To Record Accruals In Accounting.

From www.educba.com

Accrual Accounting Examples Examples of Accrual Accounting How To Record Accruals In Accounting A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. The accrued assets should appear. In accrual accounting, you record income and expenses as you earn or incur them. Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services. How To Record Accruals In Accounting.

From quickbooks.intuit.com

How to record accrued revenue correctly QuickBooks How To Record Accruals In Accounting In accrual accounting, you record income and expenses as you earn or incur them. Accrual accounting is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the cash transactions occur. The accrued assets should appear. While not everyone chooses to perform accounting. A popular choice is through accrued expenses, in which you. How To Record Accruals In Accounting.

From www.principlesofaccounting.com

Reversing Entries How To Record Accruals In Accounting This means you add income to your accounting journal when you complete a service. Accrual accounting is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the cash transactions occur. Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold. How To Record Accruals In Accounting.

From www.investopedia.com

What Is Accrual Accounting, and How Does It Work? How To Record Accruals In Accounting The accrued assets should appear. Accrual accounting is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the cash transactions occur. To record accruals, accountants use accrual accounting principles in order to enter, adjust and track both expenses and revenues. This means you add income to your accounting journal when you complete. How To Record Accruals In Accounting.

From www.myaccountingcourse.com

Accounting Cycle Steps Flow Chart Example How to Use Explanation How To Record Accruals In Accounting A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. The accrued assets should appear. There are two main ways to account for income and expenses: Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold and record. How To Record Accruals In Accounting.

From financialfalconet.com

Accrued expenses journal entry and examples Financial How To Record Accruals In Accounting The accrued assets should appear. A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. This means you add income to your accounting journal when you complete a service. Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services. How To Record Accruals In Accounting.

From khatabook.com

Accrued Expenses Journal Entry How to Record Accrued Expenses With How To Record Accruals In Accounting This means you add income to your accounting journal when you complete a service. To record accruals, accountants use accrual accounting principles in order to enter, adjust and track both expenses and revenues. The accrued assets should appear. Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold. How To Record Accruals In Accounting.

From khatabook.com

Accrued Expenses Journal Entry How to Record Accrued Expenses With How To Record Accruals In Accounting To record accruals, accountants use accrual accounting principles in order to enter, adjust and track both expenses and revenues. Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold and record expenses as they are. This means you add income to your accounting journal when you complete a. How To Record Accruals In Accounting.

From www.slideserve.com

PPT ACCRUAL ACCOUNTING PowerPoint Presentation, free download ID How To Record Accruals In Accounting While not everyone chooses to perform accounting. In accrual accounting, you record income and expenses as you earn or incur them. A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. There are two main ways to account for income and expenses: Accrual accounting is a financial accounting method that. How To Record Accruals In Accounting.

From www.enkel.ca

Cash vs. Accrual Accounting What is the Difference? Enkel How To Record Accruals In Accounting There are two main ways to account for income and expenses: The accrued assets should appear. A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. In accrual accounting, you record income and expenses as you earn or incur them. To record accruals, accountants use accrual accounting principles in order. How To Record Accruals In Accounting.

From www.double-entry-bookkeeping.com

Accrual to Cash Conversion Excel Worksheet Double Entry Bookkeeping How To Record Accruals In Accounting Accrual accounting is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the cash transactions occur. The accrued assets should appear. There are two main ways to account for income and expenses: A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced.. How To Record Accruals In Accounting.

From goselfemployed.co

What is an Accrual? How To Record Accruals In Accounting There are two main ways to account for income and expenses: To record accruals, accountants use accrual accounting principles in order to enter, adjust and track both expenses and revenues. The accrued assets should appear. A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. This means you add income. How To Record Accruals In Accounting.

From quickbooks.intuit.com

Resolve AR or AP on the cash basis Balance Sheet with journal entries How To Record Accruals In Accounting This means you add income to your accounting journal when you complete a service. A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. The accrued assets should appear. Accrual accounting is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the. How To Record Accruals In Accounting.

From hadoma.com

Double Entry Accounting (2022) How To Record Accruals In Accounting While not everyone chooses to perform accounting. Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold and record expenses as they are. In accrual accounting, you record income and expenses as you earn or incur them. To record accruals, accountants use accrual accounting principles in order to. How To Record Accruals In Accounting.

From yourbookkeepingonlinelessons.blogspot.com

Your BookKeeping Free Lessons Online Adjusting Entries How To Record Accruals In Accounting To record accruals, accountants use accrual accounting principles in order to enter, adjust and track both expenses and revenues. This means you add income to your accounting journal when you complete a service. There are two main ways to account for income and expenses: Accrual accounting is an accounting method that records revenues and expenses when they are earned or. How To Record Accruals In Accounting.

From www.netsuite.co.uk

Accrual Accounting Concepts and Examples for Business NetSuite How To Record Accruals In Accounting In accrual accounting, you record income and expenses as you earn or incur them. The accrued assets should appear. To record accruals, accountants use accrual accounting principles in order to enter, adjust and track both expenses and revenues. While not everyone chooses to perform accounting. Accrual accounting is a financial accounting method that allows a company to record revenue before. How To Record Accruals In Accounting.

From www.double-entry-bookkeeping.com

Sales Revenue in Accounting Double Entry Bookkeeping How To Record Accruals In Accounting Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold and record expenses as they are. Accrual accounting is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the cash transactions occur. There are two main ways to account for. How To Record Accruals In Accounting.

From www.personal-accounting.org

CashBasis Accounting Definition Personal Accounting How To Record Accruals In Accounting To record accruals, accountants use accrual accounting principles in order to enter, adjust and track both expenses and revenues. Accrual accounting is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the cash transactions occur. While not everyone chooses to perform accounting. In accrual accounting, you record income and expenses as you. How To Record Accruals In Accounting.

From quickbooks.intuit.com

What is accrual accounting? A beginners guide QuickBooks How To Record Accruals In Accounting This means you add income to your accounting journal when you complete a service. To record accruals, accountants use accrual accounting principles in order to enter, adjust and track both expenses and revenues. There are two main ways to account for income and expenses: A popular choice is through accrued expenses, in which you account for a future charge before. How To Record Accruals In Accounting.

From saylordotorg.github.io

Accrual Accounting How To Record Accruals In Accounting While not everyone chooses to perform accounting. The accrued assets should appear. A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold and record expenses as they are.. How To Record Accruals In Accounting.

From www.slideserve.com

PPT Accrual Accounting and the Financial Statements Chapter 3 How To Record Accruals In Accounting Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold and record expenses as they are. A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. To record accruals, accountants use accrual accounting principles in order to enter,. How To Record Accruals In Accounting.

From quickbooks.intuit.com

Accrued revenue how to record it in 2023 QuickBooks How To Record Accruals In Accounting In accrual accounting, you record income and expenses as you earn or incur them. While not everyone chooses to perform accounting. There are two main ways to account for income and expenses: This means you add income to your accounting journal when you complete a service. To record accruals, accountants use accrual accounting principles in order to enter, adjust and. How To Record Accruals In Accounting.

From business-accounting.net

The accrual basis of accounting Business Accounting How To Record Accruals In Accounting To record accruals, accountants use accrual accounting principles in order to enter, adjust and track both expenses and revenues. A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. There are two main ways to account for income and expenses: This means you add income to your accounting journal when. How To Record Accruals In Accounting.

From www.youtube.com

How to Record Accruals Basics of Accounting, Prof. Berkau YouTube How To Record Accruals In Accounting To record accruals, accountants use accrual accounting principles in order to enter, adjust and track both expenses and revenues. The accrued assets should appear. Accrual accounting is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the cash transactions occur. This means you add income to your accounting journal when you complete. How To Record Accruals In Accounting.

From quickbooks.intuit.com

Accrued revenue how to record it in 2023 QuickBooks How To Record Accruals In Accounting This means you add income to your accounting journal when you complete a service. The accrued assets should appear. A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. Accrual accounting is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the. How To Record Accruals In Accounting.

From stuffshelf.in

What Are Accruals? How Accrual Accounting Works, With Examples STUFFSHELF How To Record Accruals In Accounting A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. While not everyone chooses to perform accounting. Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold and record expenses as they are. In accrual accounting, you record. How To Record Accruals In Accounting.

From efinancemanagement.com

Accrued Expense Meaning, Accounting Treatment And More How To Record Accruals In Accounting Accrual accounting is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the cash transactions occur. A popular choice is through accrued expenses, in which you account for a future charge before it is actually invoiced. There are two main ways to account for income and expenses: Accrual accounting is a financial. How To Record Accruals In Accounting.

From www.slideserve.com

PPT Chapter 4 Accrual Accounting Concepts PowerPoint Presentation How To Record Accruals In Accounting This means you add income to your accounting journal when you complete a service. There are two main ways to account for income and expenses: Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold and record expenses as they are. The accrued assets should appear. Accrual accounting. How To Record Accruals In Accounting.