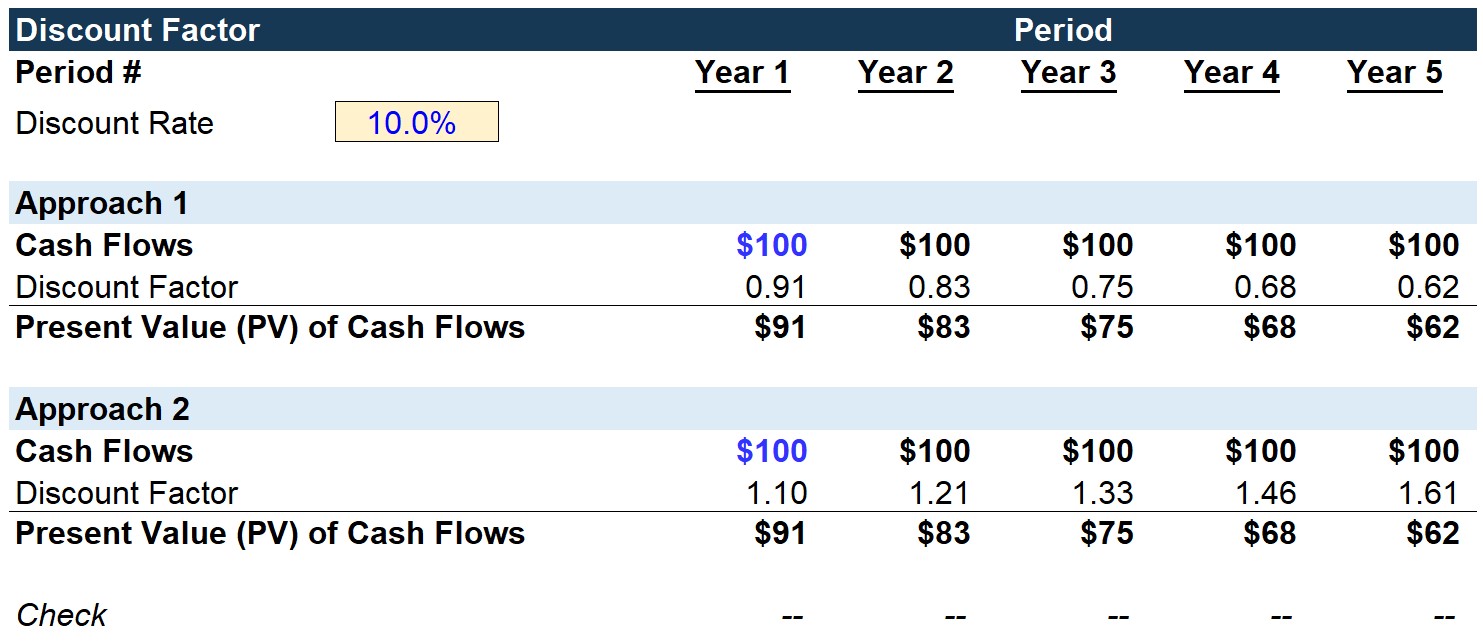

Calculate Discount Factor From Swap Rates . It is often helpful to use discount factors when pricing products such as interest rate swaps. The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. Calculate discount factors given interest rate swap rates. Let $df\left (t_1, t_2\right)$ represent the discount factor between the two periods. In the image above is possible to notice the discount rate for each term. Interest rate swaps are a type of plain vanilla swap. Interest rate swaps convert floating interest payments into fixed interest payments (and vice versa). For libor discounting this means cash market rates (for libor deposits) for the first twelve months. Calculate and interpret the impact of different compounding frequencies on a bond’s value. $df\left (t_0, t_2\right) =df\left (t_0, t_1\right).

from pubroden.weebly.com

Calculate and interpret the impact of different compounding frequencies on a bond’s value. It is often helpful to use discount factors when pricing products such as interest rate swaps. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. Calculate discount factors given interest rate swap rates. In the image above is possible to notice the discount rate for each term. For libor discounting this means cash market rates (for libor deposits) for the first twelve months. $df\left (t_0, t_2\right) =df\left (t_0, t_1\right). Interest rate swaps convert floating interest payments into fixed interest payments (and vice versa). Let $df\left (t_1, t_2\right)$ represent the discount factor between the two periods.

pubroden Blog

Calculate Discount Factor From Swap Rates Let $df\left (t_1, t_2\right)$ represent the discount factor between the two periods. Let $df\left (t_1, t_2\right)$ represent the discount factor between the two periods. Calculate discount factors given interest rate swap rates. The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. It is often helpful to use discount factors when pricing products such as interest rate swaps. For libor discounting this means cash market rates (for libor deposits) for the first twelve months. In the image above is possible to notice the discount rate for each term. Calculate and interpret the impact of different compounding frequencies on a bond’s value. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. $df\left (t_0, t_2\right) =df\left (t_0, t_1\right). Interest rate swaps convert floating interest payments into fixed interest payments (and vice versa). Interest rate swaps are a type of plain vanilla swap.

From haipernews.com

How To Calculate Discount Value Haiper Calculate Discount Factor From Swap Rates Let $df\left (t_1, t_2\right)$ represent the discount factor between the two periods. The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. Interest rate swaps are a type of plain vanilla swap. Interest rate swaps convert floating interest payments into fixed interest payments (and. Calculate Discount Factor From Swap Rates.

From www.slideserve.com

PPT Bootstrap Swaps in a multi curve framework PowerPoint Presentation ID2943396 Calculate Discount Factor From Swap Rates $df\left (t_0, t_2\right) =df\left (t_0, t_1\right). Calculate and interpret the impact of different compounding frequencies on a bond’s value. Let $df\left (t_1, t_2\right)$ represent the discount factor between the two periods. It is often helpful to use discount factors when pricing products such as interest rate swaps. For libor discounting this means cash market rates (for libor deposits) for the. Calculate Discount Factor From Swap Rates.

From www.exceldemy.com

How to Calculate Discount Factor in Excel (6 Common Ways) ExcelDemy Calculate Discount Factor From Swap Rates Interest rate swaps are a type of plain vanilla swap. $df\left (t_0, t_2\right) =df\left (t_0, t_1\right). For libor discounting this means cash market rates (for libor deposits) for the first twelve months. Let $df\left (t_1, t_2\right)$ represent the discount factor between the two periods. Interest rate swaps convert floating interest payments into fixed interest payments (and vice versa). In the. Calculate Discount Factor From Swap Rates.

From quant.stackexchange.com

interest rate swap Bloomberg SWPM Day count to calculate discount factor for US0003M Calculate Discount Factor From Swap Rates Interest rate swaps are a type of plain vanilla swap. The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. In the image above is possible to. Calculate Discount Factor From Swap Rates.

From www.youtube.com

How to Calculate Spot Rates, Forward Rates, and Discount Factors YouTube Calculate Discount Factor From Swap Rates Calculate discount factors given interest rate swap rates. In the image above is possible to notice the discount rate for each term. Calculate and interpret the impact of different compounding frequencies on a bond’s value. Let $df\left (t_1, t_2\right)$ represent the discount factor between the two periods. The short end, instruments from 1 dy up to 18 mo, is composed. Calculate Discount Factor From Swap Rates.

From www.slideserve.com

PPT Chapter 5 INTEREST RATE DERIVATIVES FORWARDS AND SWAPS PowerPoint Presentation ID6877977 Calculate Discount Factor From Swap Rates Interest rate swaps convert floating interest payments into fixed interest payments (and vice versa). For libor discounting this means cash market rates (for libor deposits) for the first twelve months. The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. $df\left (t_0, t_2\right) =df\left. Calculate Discount Factor From Swap Rates.

From quantrl.com

How to Calculate a Discount Rate Quant RL Calculate Discount Factor From Swap Rates $df\left (t_0, t_2\right) =df\left (t_0, t_1\right). The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. It is often helpful to use discount factors when pricing products such as interest rate swaps. Interest rate swaps are a type of plain vanilla swap. Calculate and. Calculate Discount Factor From Swap Rates.

From www.slideserve.com

PPT Chapter 5 INTEREST RATE DERIVATIVES FORWARDS AND SWAPS PowerPoint Presentation ID6877977 Calculate Discount Factor From Swap Rates In the image above is possible to notice the discount rate for each term. Calculate and interpret the impact of different compounding frequencies on a bond’s value. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. $df\left (t_0, t_2\right) =df\left (t_0, t_1\right). Interest rate swaps convert floating interest payments into fixed interest. Calculate Discount Factor From Swap Rates.

From www.thetechedvocate.org

How to calculate discount factor The Tech Edvocate Calculate Discount Factor From Swap Rates Interest rate swaps are a type of plain vanilla swap. Calculate and interpret the impact of different compounding frequencies on a bond’s value. Interest rate swaps convert floating interest payments into fixed interest payments (and vice versa). For libor discounting this means cash market rates (for libor deposits) for the first twelve months. Let $df\left (t_1, t_2\right)$ represent the discount. Calculate Discount Factor From Swap Rates.

From www.slideserve.com

PPT 금리스왑 (Interest Rate Swap) PowerPoint Presentation, free download ID81992 Calculate Discount Factor From Swap Rates The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. Interest rate swaps convert floating interest payments into fixed interest payments (and vice versa). $df\left (t_0, t_2\right) =df\left (t_0, t_1\right). The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the. Calculate Discount Factor From Swap Rates.

From www.slideserve.com

PPT Chapter 5 INTEREST RATE DERIVATIVES FORWARDS AND SWAPS PowerPoint Presentation ID6877977 Calculate Discount Factor From Swap Rates For libor discounting this means cash market rates (for libor deposits) for the first twelve months. Let $df\left (t_1, t_2\right)$ represent the discount factor between the two periods. The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. In the image above is possible. Calculate Discount Factor From Swap Rates.

From www.educba.com

Discount Rate Formula How to calculate Discount Rate with Examples Calculate Discount Factor From Swap Rates In the image above is possible to notice the discount rate for each term. Calculate and interpret the impact of different compounding frequencies on a bond’s value. Let $df\left (t_1, t_2\right)$ represent the discount factor between the two periods. Interest rate swaps convert floating interest payments into fixed interest payments (and vice versa). $df\left (t_0, t_2\right) =df\left (t_0, t_1\right). Calculate. Calculate Discount Factor From Swap Rates.

From www.slideserve.com

PPT Bootstrapping at par rate PowerPoint Presentation, free download ID2675057 Calculate Discount Factor From Swap Rates Calculate and interpret the impact of different compounding frequencies on a bond’s value. The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. Interest rate swaps convert floating interest payments into fixed interest payments (and vice versa). Let $df\left (t_1, t_2\right)$ represent the discount. Calculate Discount Factor From Swap Rates.

From www.youtube.com

Fixed Infer discount factors, spot, forwards and par rates from swap rate curve (FRM T4 Calculate Discount Factor From Swap Rates Calculate discount factors given interest rate swap rates. Calculate and interpret the impact of different compounding frequencies on a bond’s value. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. Let $df\left (t_1, t_2\right)$ represent the discount factor between the two periods. $df\left (t_0, t_2\right) =df\left (t_0, t_1\right). The discount factor is. Calculate Discount Factor From Swap Rates.

From www.scribd.com

Calculating Discount Factor PDF Calculate Discount Factor From Swap Rates $df\left (t_0, t_2\right) =df\left (t_0, t_1\right). Calculate and interpret the impact of different compounding frequencies on a bond’s value. In the image above is possible to notice the discount rate for each term. Calculate discount factors given interest rate swap rates. Interest rate swaps convert floating interest payments into fixed interest payments (and vice versa). For libor discounting this means. Calculate Discount Factor From Swap Rates.

From www.youtube.com

How to calculate discount rate in Excel YouTube Calculate Discount Factor From Swap Rates Let $df\left (t_1, t_2\right)$ represent the discount factor between the two periods. Interest rate swaps convert floating interest payments into fixed interest payments (and vice versa). Calculate discount factors given interest rate swap rates. For libor discounting this means cash market rates (for libor deposits) for the first twelve months. In the image above is possible to notice the discount. Calculate Discount Factor From Swap Rates.

From pubroden.weebly.com

pubroden Blog Calculate Discount Factor From Swap Rates The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. Interest rate swaps are a type of plain vanilla swap. It is often helpful to use discount factors when pricing products such as interest rate swaps. Calculate discount factors given interest rate swap rates.. Calculate Discount Factor From Swap Rates.

From mhderivatives.com

Swaps Pricing MH Derivatives Financial Education for Changing Markets Calculate Discount Factor From Swap Rates For libor discounting this means cash market rates (for libor deposits) for the first twelve months. Calculate and interpret the impact of different compounding frequencies on a bond’s value. The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. Interest rate swaps convert floating. Calculate Discount Factor From Swap Rates.

From www.slideserve.com

PPT Interest Rate Swaps PowerPoint Presentation, free download ID2050098 Calculate Discount Factor From Swap Rates Interest rate swaps are a type of plain vanilla swap. For libor discounting this means cash market rates (for libor deposits) for the first twelve months. In the image above is possible to notice the discount rate for each term. Calculate and interpret the impact of different compounding frequencies on a bond’s value. Let $df\left (t_1, t_2\right)$ represent the discount. Calculate Discount Factor From Swap Rates.

From corporatefinanceinstitute.com

Discount Factor Formula, Template, Example, Calculate Calculate Discount Factor From Swap Rates It is often helpful to use discount factors when pricing products such as interest rate swaps. Calculate discount factors given interest rate swap rates. Calculate and interpret the impact of different compounding frequencies on a bond’s value. Interest rate swaps are a type of plain vanilla swap. The short end, instruments from 1 dy up to 18 mo, is composed. Calculate Discount Factor From Swap Rates.

From www.slideserve.com

PPT Faculty of Business and Economics University of Hong Kong Dr. Huiyan Qiu PowerPoint Calculate Discount Factor From Swap Rates $df\left (t_0, t_2\right) =df\left (t_0, t_1\right). Interest rate swaps convert floating interest payments into fixed interest payments (and vice versa). The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. In the image above is possible to notice the discount rate for each term. Calculate discount factors given interest rate swap rates. The. Calculate Discount Factor From Swap Rates.

From www.slideserve.com

PPT Swaps PowerPoint Presentation, free download ID3807500 Calculate Discount Factor From Swap Rates Interest rate swaps convert floating interest payments into fixed interest payments (and vice versa). Calculate discount factors given interest rate swap rates. For libor discounting this means cash market rates (for libor deposits) for the first twelve months. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. Interest rate swaps are a. Calculate Discount Factor From Swap Rates.

From quantrl.com

How to Compute Discount Factor Quant RL Calculate Discount Factor From Swap Rates Let $df\left (t_1, t_2\right)$ represent the discount factor between the two periods. The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. $df\left (t_0, t_2\right) =df\left (t_0, t_1\right). Calculate and interpret the impact of different compounding frequencies on a bond’s value. In the image. Calculate Discount Factor From Swap Rates.

From toughnickel.com

How to Calculate Effective Interest Rate and Discount Rate Using Excel ToughNickel Calculate Discount Factor From Swap Rates For libor discounting this means cash market rates (for libor deposits) for the first twelve months. Calculate discount factors given interest rate swap rates. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. It is often helpful to use discount factors when pricing products such as interest rate swaps. Calculate and interpret. Calculate Discount Factor From Swap Rates.

From www.reddit.com

Derivatives Question Fixed Rate Calculations r/CFA Calculate Discount Factor From Swap Rates Calculate discount factors given interest rate swap rates. $df\left (t_0, t_2\right) =df\left (t_0, t_1\right). Interest rate swaps are a type of plain vanilla swap. Interest rate swaps convert floating interest payments into fixed interest payments (and vice versa). The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap. Calculate Discount Factor From Swap Rates.

From www.slideserve.com

PPT 5th Lecture 10 th November 2003 PowerPoint Presentation, free download ID4564663 Calculate Discount Factor From Swap Rates Interest rate swaps are a type of plain vanilla swap. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. $df\left (t_0, t_2\right) =df\left (t_0, t_1\right). Interest. Calculate Discount Factor From Swap Rates.

From in.pinterest.com

Discount Factor Formula How to Use, Examples and More in 2021 Time value of money, Economics Calculate Discount Factor From Swap Rates It is often helpful to use discount factors when pricing products such as interest rate swaps. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. Calculate and interpret the impact of different compounding frequencies on a bond’s value. Interest rate swaps are a type of plain vanilla swap. Calculate discount factors given. Calculate Discount Factor From Swap Rates.

From spreadcheaters.com

How To Calculate Discount Factor In Microsoft Excel SpreadCheaters Calculate Discount Factor From Swap Rates Calculate and interpret the impact of different compounding frequencies on a bond’s value. It is often helpful to use discount factors when pricing products such as interest rate swaps. Interest rate swaps convert floating interest payments into fixed interest payments (and vice versa). In the image above is possible to notice the discount rate for each term. For libor discounting. Calculate Discount Factor From Swap Rates.

From www.bartleby.com

Answered What is the swap rate? (the fixed rate… bartleby Calculate Discount Factor From Swap Rates The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. Calculate discount factors given interest rate swap rates. $df\left (t_0, t_2\right) =df\left (t_0, t_1\right). Calculate and interpret the impact of different compounding frequencies on a bond’s value. It is often helpful to use discount. Calculate Discount Factor From Swap Rates.

From www.youtube.com

How to Calculate Discounting Factors on Calculator Financial Management YouTube Calculate Discount Factor From Swap Rates Let $df\left (t_1, t_2\right)$ represent the discount factor between the two periods. The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. It is often helpful to. Calculate Discount Factor From Swap Rates.

From spreadcheaters.com

How To Calculate Discount Factor In Microsoft Excel SpreadCheaters Calculate Discount Factor From Swap Rates It is often helpful to use discount factors when pricing products such as interest rate swaps. Interest rate swaps convert floating interest payments into fixed interest payments (and vice versa). Calculate and interpret the impact of different compounding frequencies on a bond’s value. For libor discounting this means cash market rates (for libor deposits) for the first twelve months. $df\left. Calculate Discount Factor From Swap Rates.

From mhderivatives.com

Swaps Pricing MH Derivatives Financial Education for Changing Markets Calculate Discount Factor From Swap Rates Let $df\left (t_1, t_2\right)$ represent the discount factor between the two periods. Interest rate swaps are a type of plain vanilla swap. It is often helpful to use discount factors when pricing products such as interest rate swaps. Calculate discount factors given interest rate swap rates. Calculate and interpret the impact of different compounding frequencies on a bond’s value. In. Calculate Discount Factor From Swap Rates.

From www.educba.com

Discount Factor Formula Calculator (Excel template) Calculate Discount Factor From Swap Rates The short end, instruments from 1 dy up to 18 mo, is composed by zero coupon swaps. It is often helpful to use discount factors when pricing products such as interest rate swaps. In the image above is possible to notice the discount rate for each term. For libor discounting this means cash market rates (for libor deposits) for the. Calculate Discount Factor From Swap Rates.

From quantrl.com

Single Equivalent Discount Rate Calculator Quant RL Calculate Discount Factor From Swap Rates For libor discounting this means cash market rates (for libor deposits) for the first twelve months. Interest rate swaps are a type of plain vanilla swap. The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. In the image above is possible to notice. Calculate Discount Factor From Swap Rates.

From analystprep.com

Spot, Forward, and Par Rates AnalystPrep FRM Part 1 Study Notes Calculate Discount Factor From Swap Rates $df\left (t_0, t_2\right) =df\left (t_0, t_1\right). In the image above is possible to notice the discount rate for each term. The discount factor is just 1 divided by the interest rate, if you want a quick proxy and don't want to bootstrap the ois swap curve. The short end, instruments from 1 dy up to 18 mo, is composed by. Calculate Discount Factor From Swap Rates.